Table of Contents

The stablecoin market has already surged past $320 billion in total supply as of mid-2026, with quarterly transfer volumes hitting records like $4.5 trillion in Q1 alone.

Yet most enterprises continue to use stablecoins primarily for basic cross-border transfers, liquidity parking, or simple settlements, essentially treating them as upgraded SWIFT or wire replacements.

This narrow approach leaves enormous value untapped.

Advanced features such as programmability, white-label issuance, structured yield models, and on-chain compliance tools have matured significantly, accelerated by ongoing GENIUS Act rulemakings from the OCC, FDIC, and Treasury.

Leaders who move beyond transactional use cases can transform treasury operations, create new revenue streams, strengthen customer relationships, and build durable competitive advantages in an increasingly automated economy.

The “Faster Wires” Trap: A Costly Mindset in 2026

Enterprises are right to celebrate stablecoins for delivering always-on availability, borderless reach, slashed FX drag, and near-instant settlement. These are genuine breakthroughs.

But here’s the uncomfortable truth: by viewing stablecoins through a purely transactional lens as nothing more than faster, cheaper wires, most companies are dramatically shortchanging their own potential.

They’re using 21st-century programmable money like it’s a slightly improved version of 20th-century infrastructure.

In today’s post-GENIUS Act landscape, with explicit green lights for bank participation and tokenized deposits, stablecoins have decisively left the “fringe experiment” phase behind.

What was once experimental is now strategic infrastructure.

Leading platforms from Stripe, Circle, Bridge, PayPal’s PYUSD, and forward-thinking banks are delivering enterprise-grade tools that don’t just move money, they let you program its behavior with precision.

Companies that cling to the “faster wires” mindset are quietly handing their competitors a powerful advantage: the ability to automate treasury functions at scale, roll out differentiated loyalty and ecosystem programs, and squeeze far more efficiency out of working capital.

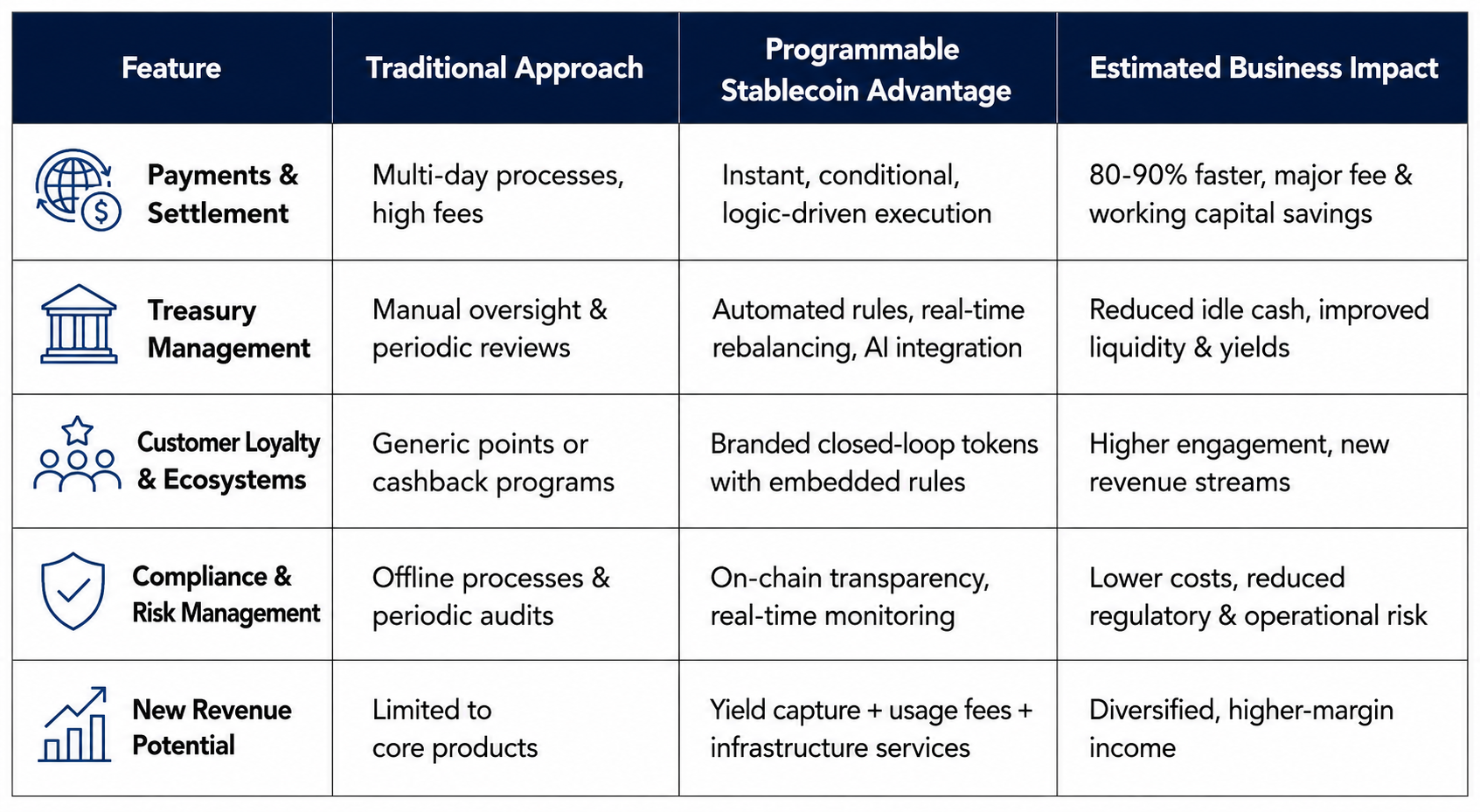

4 Overlooked Stablecoin Features Enterprises Should Prioritize Now

1. Programmability for Automated Workflows

Most companies still use stablecoins the same way they use bank wires: move money from Point A to Point B.

That mindset misses one of the technology's most powerful features.

For example, a supplier payment can remain locked in escrow until delivery is verified, while a treasury system automatically reallocates excess cash into approved yield-generating opportunities once predefined thresholds are reached.

The applications are already emerging across global finance.

- Payments can be held in escrow and released only after delivery is verified through external data feeds or connected devices.

- Treasury systems can automatically rebalance liquidity across currencies, accounts, and yield opportunities without waiting for human approval.

- Payroll, subscriptions, and vendor contracts can shift from periodic batch payments to continuous, real-time payment streams.

For CFOs and treasury teams, the appeal isn't blockchain innovation for its own sake. It's operational efficiency.

Companies piloting programmable payment systems are reporting dramatically lower settlement costs, faster access to working capital, and fewer manual touchpoints across critical financial workflows.

The implications become even more significant when artificial intelligence enters the equation.

Protocols such as x402 are laying the groundwork for AI agents that can not only make decisions, but also execute payments. In that model, software can negotiate, approve, and settle routine transactions autonomously, creating a future where money moves as seamlessly as information does today.

For enterprises, programmability may ultimately prove more transformative than faster settlement itself. The real breakthrough isn't moving money faster. It's teaching money how to work.

2. White-Label & Closed-Loop Branded Tokens

Corporations and banks can issue their own fully backed, compliant stablecoins tailored for internal use, loyalty programs, supplier networks, or customer ecosystems.

C-suite impact: Lower internal transaction costs, capture permitted reserve yield, increase customer stickiness, and open entirely new revenue models. White-label platforms are growing rapidly for closed-loop systems from corporate expense management to supply chain finance.

This shifts stablecoins from a pure cost-saving tool to a profit-generating infrastructure layer.

3. Structured Yield-Bearing Models Under Regulatory Guardrails

While direct yield-sharing faces constraints, compliant wrappers, affiliate structures, and tokenized money market integrations allow institutions to earn returns on stablecoin reserves with daily liquidity.

C-suite impact: Transform idle cash holdings into productive assets that often outperform traditional money market funds, especially when paired with automation. This segment expanded significantly in 2025–2026 as regulatory clarity improved, offering treasury teams better risk-adjusted returns without sacrificing programmability.

4. On-Chain Compliance & Real-Time Audit Tools

Modern stablecoin platforms include built-in KYC/AML screening, geographic restrictions, transaction monitoring, and immutable audit trails at the token level.

C-suite impact: Substantially lower compliance overhead, faster audit processes, and stronger risk controls compared to legacy systems. These features help satisfy both internal governance and evolving GENIUS Act requirements, turning compliance from a cost center into a strategic advantage.

Real-World Momentum: Who’s Already Moving Ahead

- Banks & Tokenized Deposits: Institutions are launching programmable tokenized bank deposits that combine stablecoin speed with traditional regulatory protections.

- Payment Giants: Stripe and PayPal are expanding programmable capabilities for subscriptions, merchant settlements, and B2B flows.

- Enterprises: Multinationals are piloting closed-loop stablecoins for global supplier payments and automated treasury operations.

2026 marks the shift from experimentation to production deployments across treasury, payments, and embedded finance.

Strategic Implications for C-Level Leadership

The competitive gap is widening. Organizations that continue treating stablecoins as simple rails will face increasing pressure as peers build more efficient, automated, and differentiated financial operations.

Risks and Considerations to Address Proactively

While the upside is significant, programmability introduces new complexities: smart contract vulnerabilities, over-automation risks, and the need for robust governance.

Enterprises should prioritize audited contracts, multi-signature controls, fallback mechanisms, and clear policies for agentic payments. GENIUS Act compliance will remain a moving target through late 2026, so early engagement with regulated partners is essential.

Actionable Next Steps

- Internal Assessment: Map your highest-friction treasury, payments, and compliance processes against programmable capabilities.

- Strategic Pilots: Launch a contained test such as programmable supplier escrow, white-label closed-loop for internal transfers, or x402 agent payment integration.

- Ecosystem Partnerships: Collaborate with established players (Circle, Paxos, Stripe, or bank issuers) for faster, lower-risk deployment.

- Board & Stakeholder Alignment: Position this as core infrastructure modernization with clear ROI metrics, not experimental blockchain activity.

- Timeline: Target meaningful pilots in Q3/Q4 2026, with scaled production in 2027 as GENIUS Act rules finalize.

The window between basic adoption and full strategic leverage is closing fast. In 2026 and beyond, the winners won’t simply use stablecoins, they will build with them to reimagine how money moves, works, and creates value inside their organizations.

This newsletter was sponsored by Rise Payroll

Related Reports

- Is All Stablecoin Infrastructure Actually the Same?

- Q1 2026 Stablecoin Report: Acceleration Continues

Partner/Advertise with Stablecoin Insider

Fill out this form to partner and advertise on the only publication, dedicated entirely to the Stablecoin ecosystem.

See you next week,

- The Stablecoin Insider team

{kind=link}