Table of Contents

For a decade, the case for bridge assets like XRP was simple. A neutral digital token could sit in the middle of a cross-border payment and route value between two currencies in seconds, with no need to pre-fund accounts on either end.

But regulated dollar stablecoins now do much of that job directly, and they do it without asking anyone to hold a floating asset mid-transaction. That single difference, the removal of price risk from the middle of a payment, has reshaped how institutions think about settlement.

So the question worth asking is whether a dollar token has quietly made the bridge-asset model redundant, or whether the two are settling into separate roles that each make sense in different corridors.

The data points in one direction more than the other. Here is what the 2026 settlement figures, deal flow, and price action actually reveal.

KEY TAKEAWAYS

- RLUSD reached a peak near $1.78B in market cap in May 2026, before settling back around $1.59B.

- XRP is down roughly 38% year-to-date and about 69% from its July 2025 high.

- Major 2026 Ripple deals settle in RLUSD, not XRP, with the token covering only fractions of a cent in network fees.

- Only around 40% of 300+ RippleNet institutions actually use XRP for settlement.

- Bridge assets survive at the edges, in corridors where deep stablecoin liquidity does not yet exist.

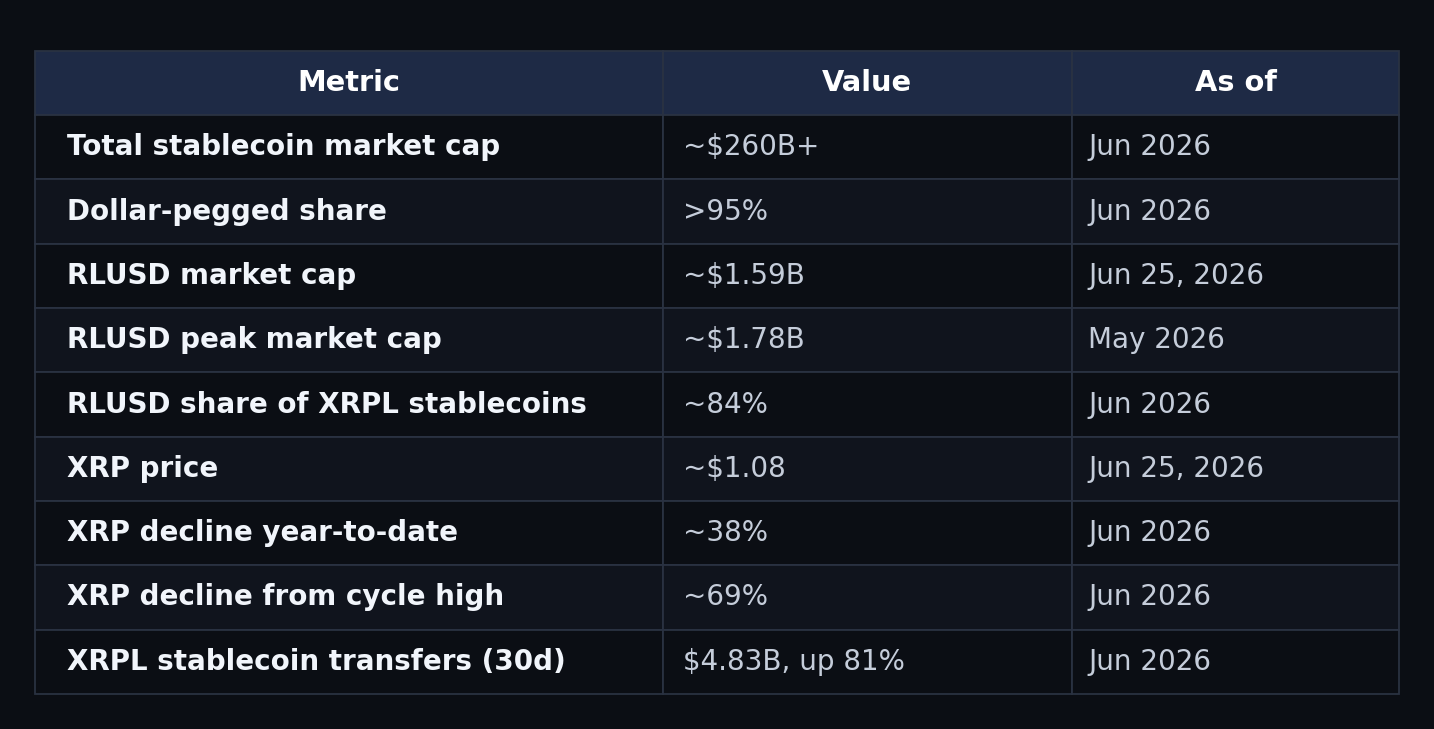

The Numbers at a Glance

Before the argument, the scoreboard. These are the figures that frame every question about whether stablecoins have displaced bridge assets in 2026.

Sources: CoinGecko, CoinMarketCap, CoinDesk, The Block, RWA.xyz, Capital.com.

What Changed: The Stablecoin Sandwich

The original bridge-asset thesis solved a real problem. Dollar-pegged tokens solved it more cleanly.

Traditional cross-border payments route through a chain of correspondent banks. Each hop adds delay and cost, and institutions must park capital in destination-currency accounts just to keep the flow moving. A neutral asset like XRP was designed to remove that friction by serving as a universal intermediary between any two currencies.

The trouble was that the model still asked counterparties to hold a floating asset in the middle of a transaction. For a corporate treasurer, even a few seconds of price exposure on a large transfer is a risk they would rather not carry. Volatility is exactly the thing institutional payments are built to avoid.

Stablecoins answered that objection directly.

A payment now starts in fiat, settles through a dollar-pegged token in the middle, and arrives in fiat on the other end. The industry calls this the “stablecoin sandwich,” and it delivers blockchain speed without the volatility that made bridge assets a hard sell to finance teams.

The clearest example

Convera, the firm carved out of Western Union’s business payments arm, processes roughly $190 billion in annual volume across more than 200 countries and 140 currencies. When a payments network of that scale integrates with Ripple, the design choice it makes carries real weight.

Its 2026 partnership settles in RLUSD on the XRP Ledger and bypasses XRP entirely. The bridge step that the original thesis depended on is simply not in the flow. The same pattern repeats across most of Ripple’s 2026 enterprise deals.

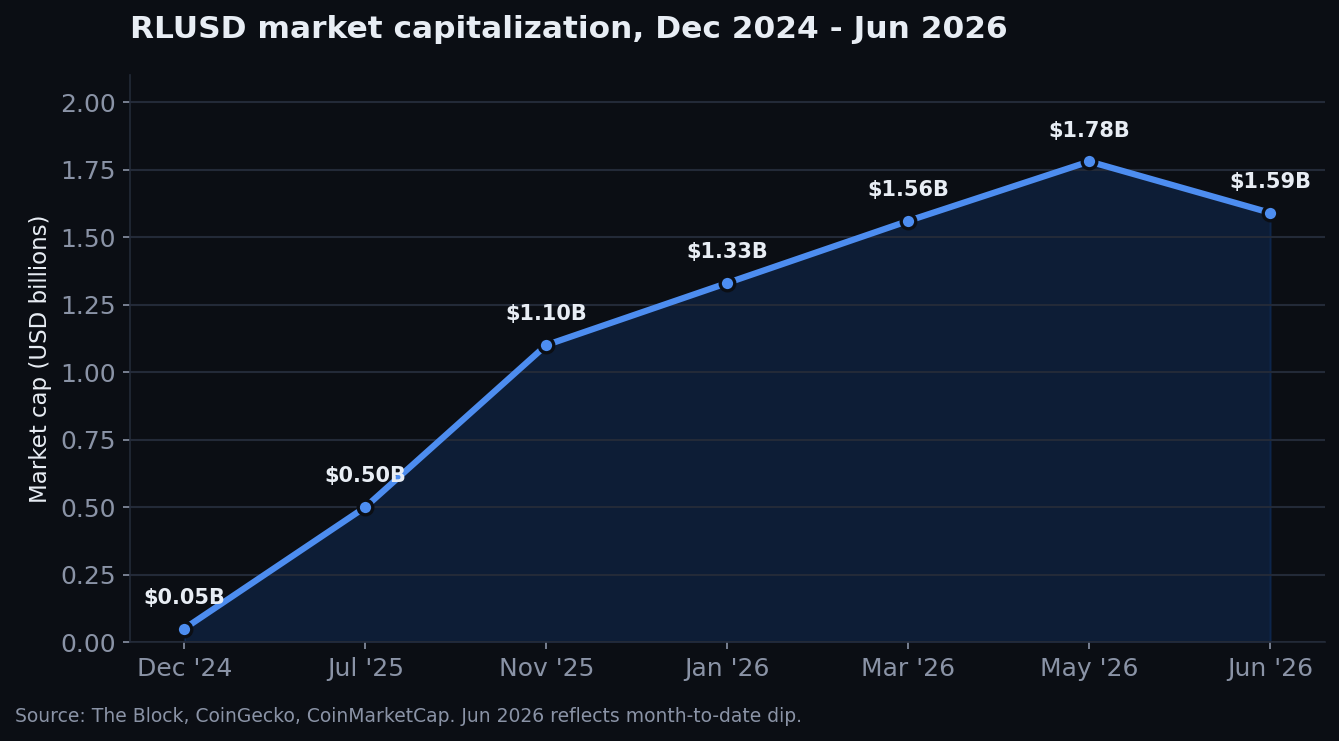

RLUSD Growth Tells the Story

Ripple’s own dollar stablecoin has scaled quickly, even as XRP has not. That divergence is the heart of the matter.

RLUSD market capitalization, December 2024 to June 2026. Source: The Block, CoinGecko, CoinMarketCap.

RLUSD went from roughly $50 million at launch in December 2024 to a peak near $1.78 billion in May 2026.

On the XRP Ledger specifically, total stablecoin market cap climbed from about $277 million at the start of 2026 to $907 million by June, with RLUSD holding roughly an 84% share of that figure.

This is genuine, fast adoption. But it is important to be precise about what kind of adoption it represents. It is stablecoin growth, and it strengthens Ripple’s business and proves the ledger’s technical capacity. It does not, on its own, create demand for the bridge asset.

What the Settlement Data Shows

Two figures tell the story better than any amount of narrative framing.

The JPMorgan pilot

In May 2026, a pilot run by JPMorgan, Mastercard, Ondo, and Ripple cleared a tokenized U.S. Treasury trade on the XRP Ledger in under five seconds. It proved the ledger works for institutional settlement at scale.

But the mechanics matter. The settlement value moved through RLUSD, while XRP covered only minimal network fees of about $0.00001 per transaction. The ledger did the work; the token barely participated.

The 300-banks problem

Ripple regularly cites 300+ financial institutions on RippleNet, and that number anchors most bullish adoption stories. What it hides is that only about 40% of those institutions actually use XRP for On-Demand Liquidity settlement.

The remaining 60% use RippleNet’s messaging rails, which move fiat payments without ever touching the token. A bank “on RippleNet” is a Ripple business customer, not necessarily a source of XRP demand. Conflating the two inflates the apparent adoption story considerably.

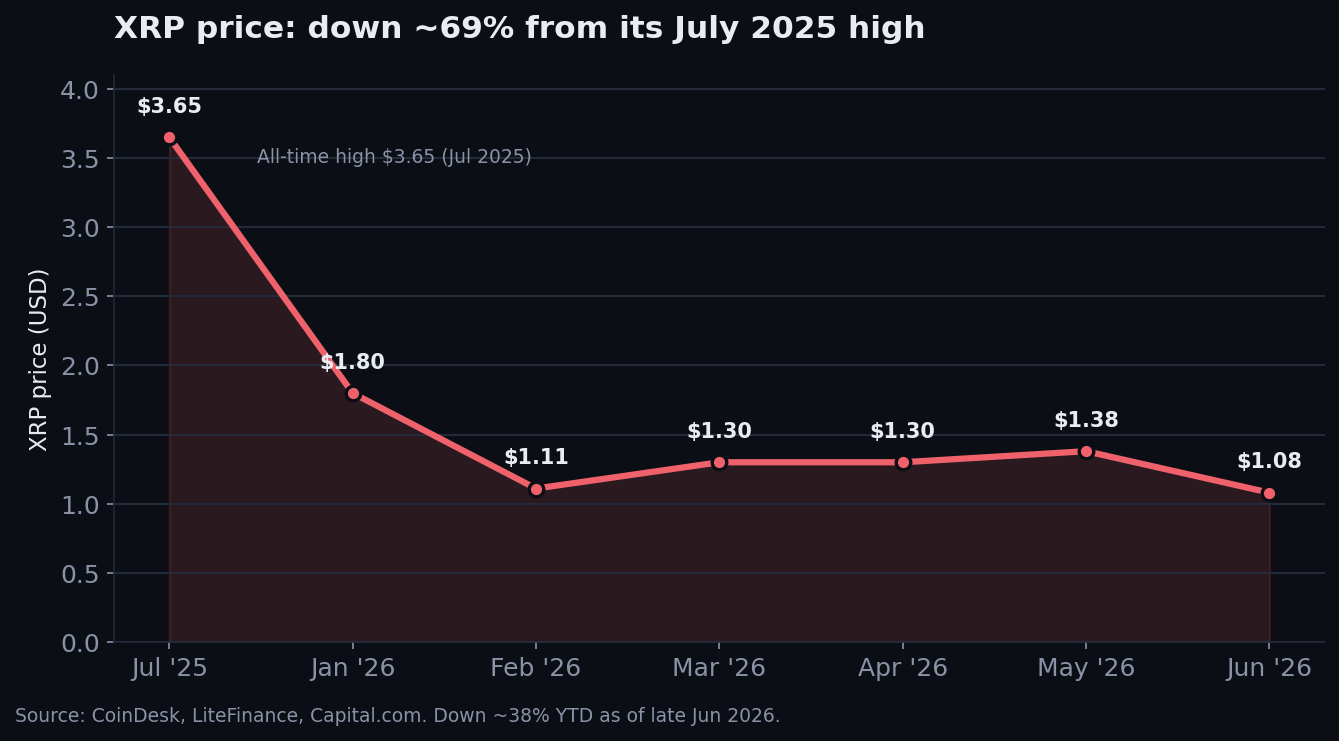

Why XRP Price Reflects This

If stablecoin growth were translating into bridge-asset demand, the token price would show it. It has not.

XRP price, down about 69% from its July 2025 high. Source: CoinDesk, LiteFinance, Capital.com.

XRP peaked near $3.65 in July 2025 immediately after its SEC settlement, then drifted lower throughout 2026 to around $1.08 by late June. That works out to roughly 38% down year-to-date and about 69% below the cycle high.

Spot XRP ETFs launched in late 2025 and gathered over $1 billion in assets, yet daily net inflows trended downward rather than up. Even Standard Chartered, long among the more bullish institutional voices, cut its 2026 target from $8.00 to $2.80. The disconnect is structural rather than sentimental: as long as banks can use the ledger without holding the token, ledger activity and token price stay decoupled.

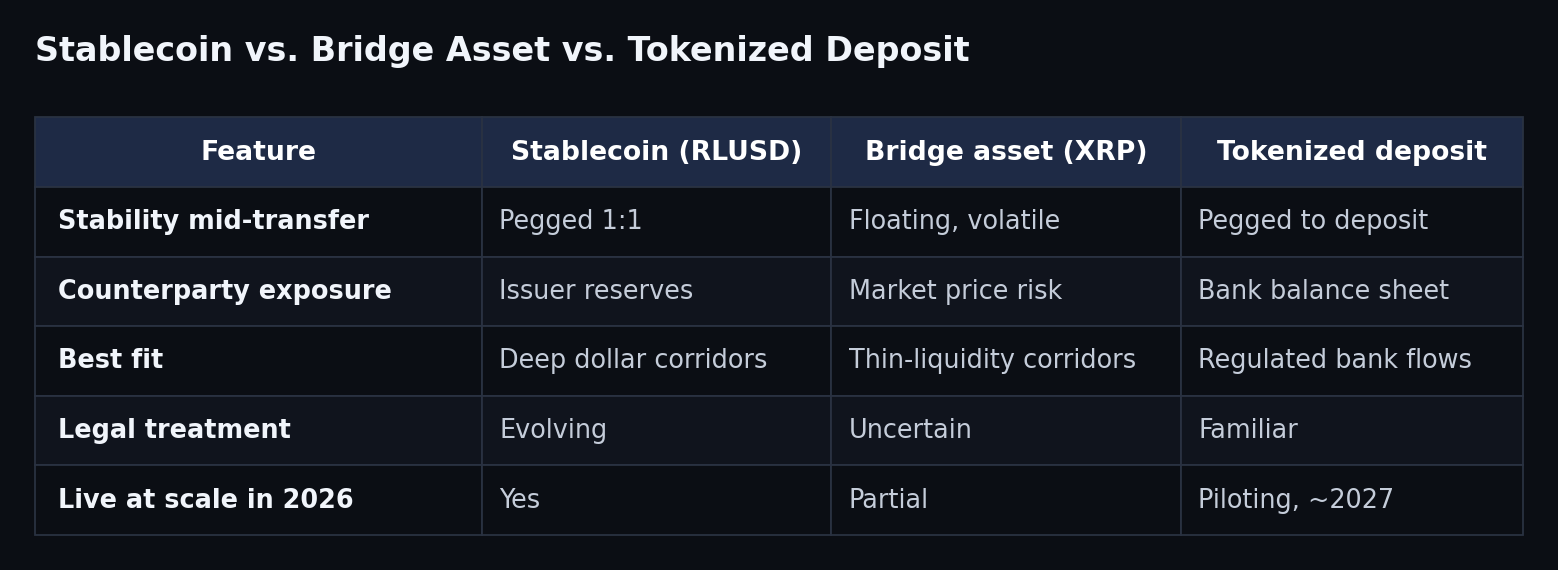

Stablecoin vs. Bridge Asset vs. Tokenized Deposit

The contest is no longer two-sided. A third settlement model is now entering the picture, and treasurers are watching it closely. Here is how the three compare.

America’s largest banks, including JPMorgan, Bank of America, and Citigroup, plan a shared tokenized deposit network through The Clearing House by the first half of 2027. For a treasurer, a tokenized bank deposit carries familiar legal treatment that neither a stablecoin nor a bridge asset offers today, which makes it a serious third contender rather than a footnote.

Where Bridge Assets Still Have a Role

The replacement story has real limits, and they come down to liquidity.

Stablecoin liquidity is deep in dollar pairs but thin in many emerging-market corridors. In those routes, a bridge asset still earns its place by sourcing liquidity on demand where no deep stablecoin market exists. You cannot settle in a stablecoin that has no local market on the other side.

Ripple itself now frames this as a hybrid model: the stablecoin provides stability, and the bridge asset provides liquidity. On-Demand Liquidity processed an estimated $15 billion in volume in 2024, growing 30 to 40% annually, with direct token demand built into each transaction it touches. That is a smaller, more defensible niche than the original “XRP replaces SWIFT” pitch, but it is a real one.

Challenges Facing the Replacement Thesis

The picture is not a clean victory for either side.

Stablecoin liquidity remains shallow outside core dollar pairs, which is precisely what keeps bridge assets relevant. Regulatory treatment of settlement assets still varies sharply by jurisdiction, adding friction that neither model has fully escaped.

And the scale gap cuts both ways. RLUSD’s roughly $1.59 billion sits far behind USDT and USDC, so it is not yet a liquidity giant. Meanwhile XRP’s utility demand has stayed largely static for over a year, which undercuts the case that adoption is quietly building beneath the price.

What Comes Next

The second half of 2026 should sharpen the contest considerably.

- Ripple keeps pushing RLUSD into regulated settlement, including its Singapore trade-finance pilot and new payments corridors.

- Bank-issued tokenized deposits move toward their 2027 launch window, adding a third settlement option for institutions.

- Bridge assets defend the thin-liquidity corridors where on-demand sourcing still beats holding stablecoin inventory.

The honest answer is that stablecoins replaced the default case for bridge assets, not the entire category.

Where a deep dollar market exists, a regulated stablecoin is now the path of least resistance, and the data shows institutions choosing it consistently. The bridge asset survives at the edges, in the corridors where liquidity is scarce and on-demand sourcing still wins.

For decision-makers, the practical takeaway is to stop asking which model wins outright and start evaluating settlement assets corridor by corridor. The right answer in a USD-EUR flow is rarely the right answer in a thin emerging-market route.

Partner/Advertise with Stablecoin Insider

Fill out this form to partner and advertise on the only publication, dedicated entirely to the Stablecoin ecosystem.

See you next week,

- The Stablecoin Insider team

{kind=link}