Table of Contents

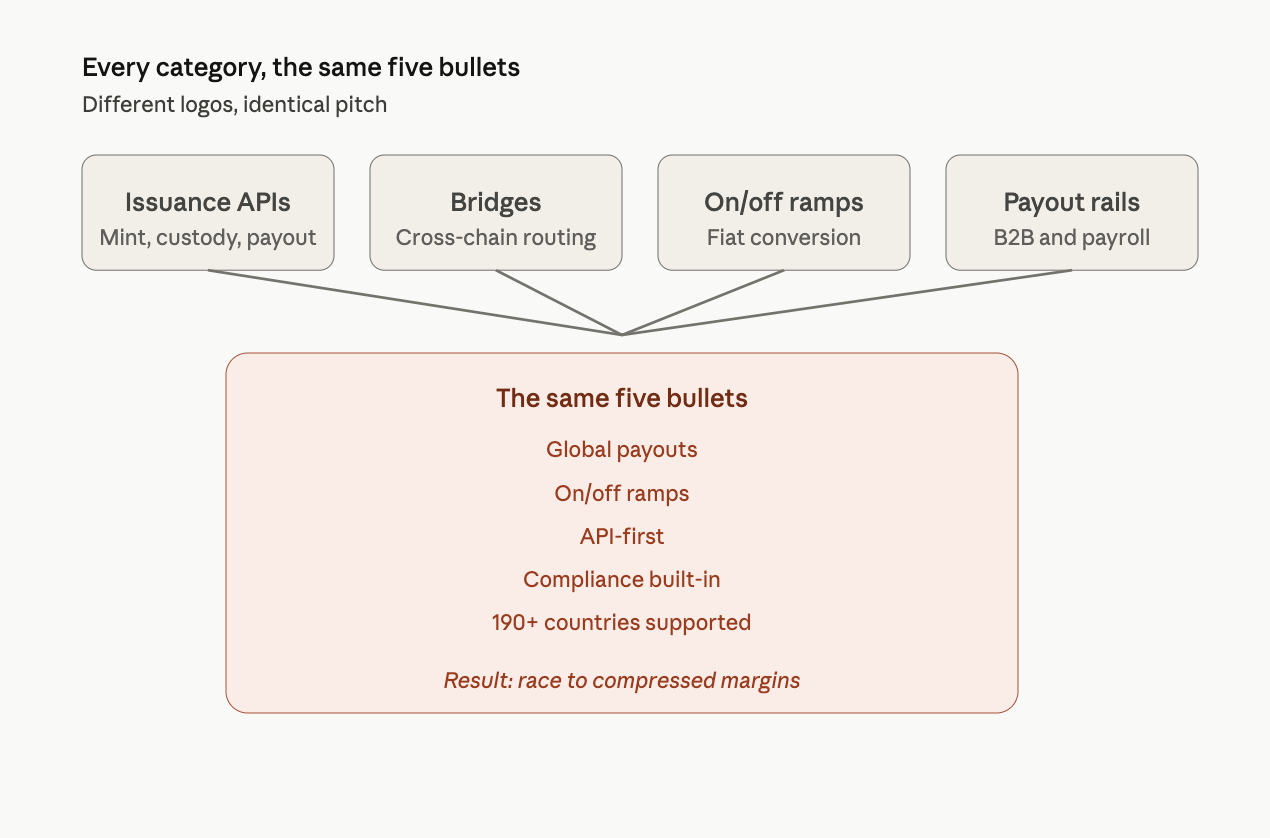

Scroll through any stablecoin infrastructure company's homepage and you'll see the same five bullets. Global payouts. On/off ramps. API-first. Compliance built-in. 190+ countries supported. Different logos, identical pitch.

For an institutional buyer or allocator evaluating this category, that surface-level sameness is the first signal something deeper is going on.

If every stablecoin API, bridge, and orchestration layer is selling the same product, where do the actual moats live, and which providers are positioned to still be standing in three years?

The answer has two sides.

Most of the category is genuinely undifferentiated, and the consolidation pressure is real. But a quieter subset is building durable advantages by going deep on geography or vertical instead of going wide.

Both things are true at once, and reading this market correctly means holding both ideas at the same time.

The Sea of Sameness

The pattern repeats across every sub-category.

Stablecoin issuance and treasury APIs all advertise programmatic USDC and USDT minting, custody, and global payouts. Compare any two homepages side by side and you have to squint to find a real difference.

Cross-chain bridges and orchestration layers all promise the cheapest, fastest routing with the deepest liquidity. Aggregators aggregate the same underlying sources, and the routing algorithms converge on similar outputs.

On and off ramps all sell the same fiat corridors with marginal fee differences and near-identical UX claims.

Payroll and B2B payout rails all claim global coverage, all claim compliance, and all show the same three reference customers in their decks.

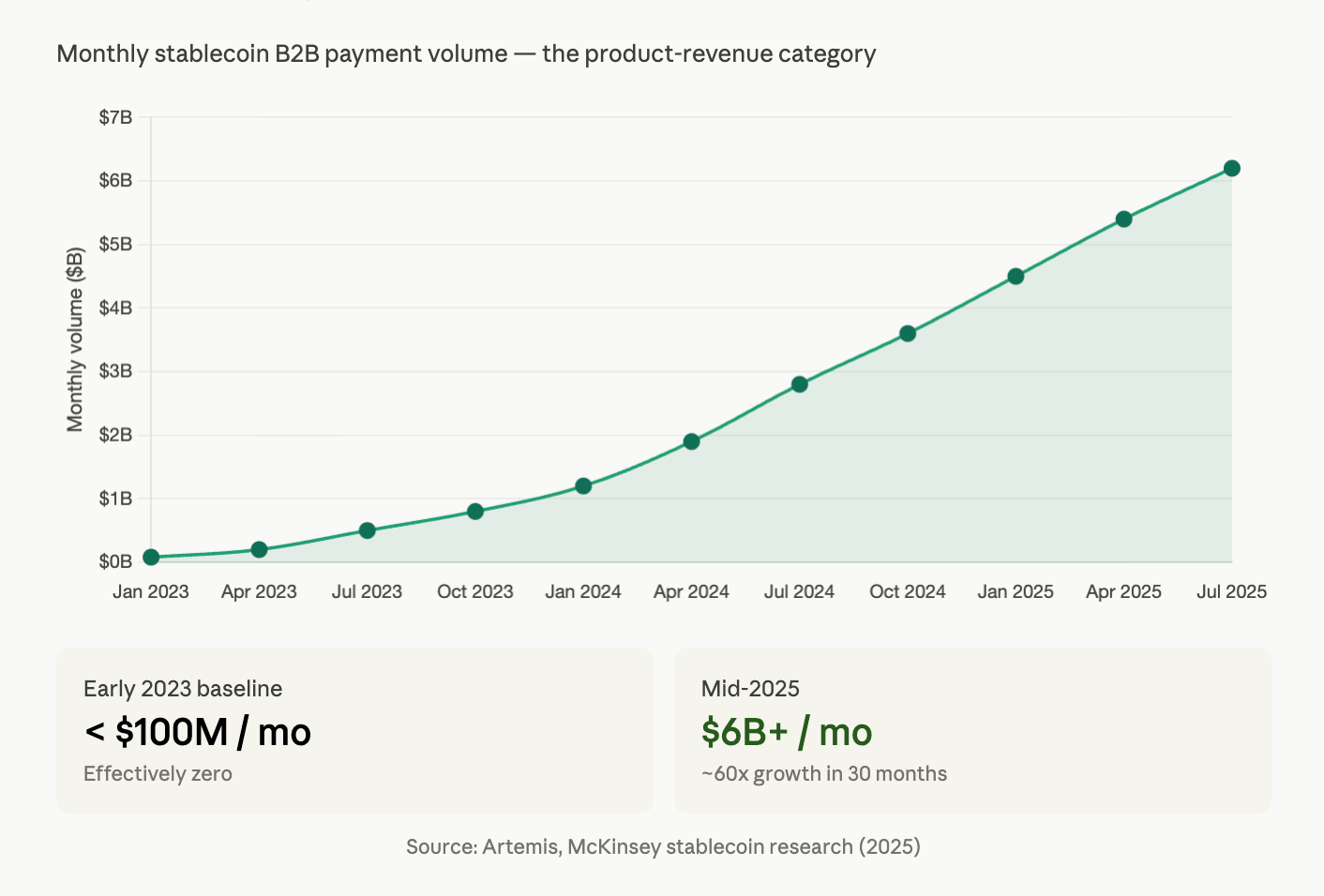

When feature lists converge this hard, buyers default to brand recognition, distribution, or price. That's a race to compressed margins, which is the trajectory take rates across the category are already on.

The Economics Beneath the Sameness

For an institutional reader, the more important question is why so many undifferentiated providers can sustain operations at all. The answer is structural.

Stablecoin infrastructure benefits from several revenue layers that don't depend on product differentiation:

- Float economics on stablecoin reserves. Holding customer balances generates yield on underlying treasuries. At current rates, this alone can fund significant operations.

- FX spread embedded in cross-border flows. "Free" transfers usually aren't free. The spread sits inside the conversion rate.

- Network fee markups layered on top of underlying gas and AMM fees in bridges and swap routers.

- Volume-based take rates that scale with near-zero incremental cost once the rails are operational.

The implication for institutional readers: revenue today is not a reliable signal of competitive position. A provider can generate meaningful top-line numbers from float and spread alone while having no defensible product moat.

When rates compress, when a dominant platform consolidates the category through acquisition, or when regulators tighten reserve requirements, the operators relying on these revenue layers face significant exposure all at once.

The float-rate environment is a tailwind, not a moat. Underwriting this category requires separating the two.

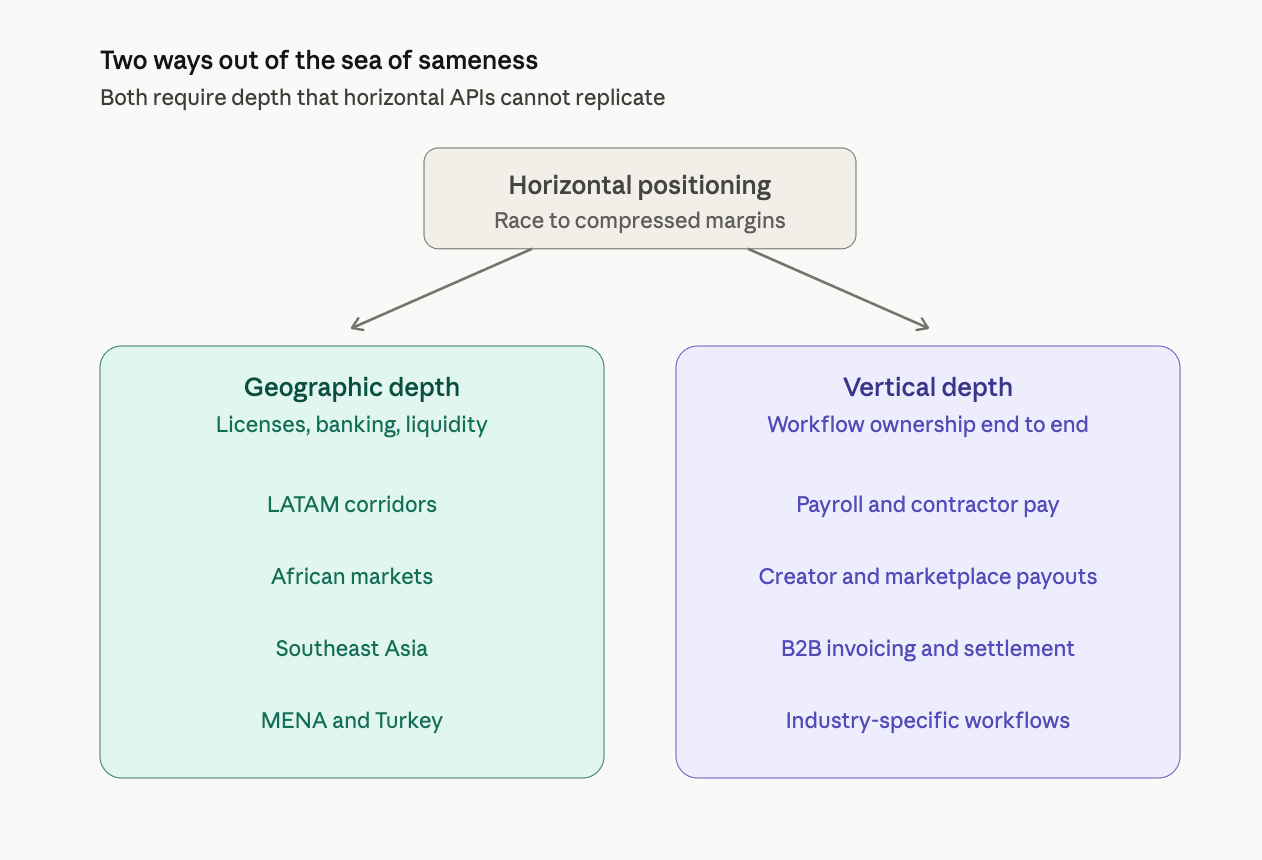

The Geography Play

This is where the more durable opportunities live. The operators building real defensibility have made the same realization: "global" is a marketing word, not an operational reality.

LATAM corridors require local banking relationships, regulator trust, and liquidity provider partnerships that take years to build. Peso, real, and bolivar off-ramps are not API integrations. They're licensing and banking strategies.

African markets are not one market, they're 54. Naira, cedi, rand, and shilling corridors require Bureau De Change networks, central bank registrations, and on-the-ground compliance teams. Generic global APIs cannot service these flows, and catching up is a multi-year capital and licensing exercise, not a product roadmap.

Southeast Asian corridors require local banking partnerships and regulator relationships that compound over time. Entering the Philippines, Indonesia, or Vietnam from a US-only license is a non-starter for most use cases.

MENA and Turkey are emerging as specialized corridors where geopolitical, regulatory, and capital control friction makes a generic global rail commercially unworkable.

This is real differentiation. Licenses, banking relationships, and local liquidity are not features that ship in a quarter. They take years and significant capital, and they compound. A provider with a Nigerian BDC partnership and central bank standing has a moat that no amount of US-licensed API engineering can replicate.

The same logic applies to vertical specialization. Operators focused narrowly on payroll, on creator payouts, on B2B invoicing, or on specific industry workflows are building product depth that horizontal APIs cannot match.

Picking a workflow and owning it end to end is the second escape route from the sea of sameness, because depth in one job beats breadth across ten when the buyer has a real operational need.

What This Means for Institutional Readers

For allocators and corporate buyers underwriting exposure in this category, the practical takeaways are direct.

When evaluating a provider, the homepage is not the product. The relevant diligence questions are: which corridors do they own with their own licenses and direct banking partners, versus which do they pass through to a third party?

- What share of revenue is float-dependent versus product-dependent?

- What happens to their unit economics in a 200 basis point rate cut?

- Which jurisdictions can they actually settle in same-day?

- Which require manual workarounds?

The answers separate operators with real moats from operators riding a favorable macro environment.

For founders and investors building in the category, the strategic conclusion is the same.

Horizontal positioning is a losing posture against incumbent payment networks that are now entering the space with distribution advantages no startup can match.

The durable opportunities are geographic specialization with real licensing depth, or vertical specialization with real workflow depth. Anything in between is competing on price against companies that can subsidize indefinitely.

Stablecoin infrastructure is not all the same. But most of it is.

The next 18 to 24 months will sort the operators with structural moats from the ones currently benefiting from a tailwind, and institutional readers paying attention now will see the divergence well before it shows up in the financials.

Upcoming Events

Related Reports

Partner/Advertise with Stablecoin Insider

Fill out this form to partner and advertise on the only publication, dedicated entirely to the Stablecoin ecosystem.

See you next week,

- The Stablecoin Insider team

{kind=link}