Table of Contents

Stablecoin economics describes the business model that allows issuers to generate billions in revenue by holding user-deposited reserves, investing them in safe short-term instruments, and keeping the yield, and as of Q1 2026 it has become one of the most profitable business models in digital finance, according to the Stablecoin Issuance Landscape Q1 2026 Report.

Tether reported over $10 billion in net profit in 2025 and Circle earned $2.7 billion in revenue, both primarily from interest on the reserves backing their stablecoins, while a growing layer of issuers now monetize transaction fees, DeFi integration, and yield-bearing products on top.

This article breaks down the three core revenue streams powering stablecoin issuance, profiles the economics of each major issuer, examines how new entrants like PYUSD and Ethena monetize differently, explains why so many fintechs and banks are racing to issue stablecoins, and shows how stablecoin economics is reshaping the broader payments and DeFi landscape.

Key Takeaways

- Stablecoin issuance is one of the most profitable business models in digital finance.

- Treasury yield on reserves drives the vast majority of issuer revenue.

- Transaction fees and DeFi integration are the next major monetization layers.

What Are Stablecoin Economics

Stablecoin economics refers to how issuers generate revenue from minting, backing, and circulating their stablecoins. The model is structurally simple: issuers take in dollar assets, issue stablecoins against them at a 1:1 ratio, invest the reserves into safe interest-bearing instruments, and keep most or all of the interest earned while passing zero interest to stablecoin holders.

This dynamic turns stablecoin issuance into a high-margin business at scale. At $1 billion in reserves, even a 4% to 5% yield generates $40 to $50 million in annual revenue with minimal operating costs.

At $100 billion, the same spread produces multi-billion-dollar profits.

Per the Stablecoin Issuance Landscape Q1 2026 Report, stablecoin issuer revenue comes from three main layers:

- Treasury yield on reserves (dominant for Tether and Circle)

- Transaction and settlement fees (growing with payments adoption)

- DeFi-linked yield and liquidity monetization (key for crypto-native and synthetic issuers)

With Tether generating over $10 billion in profit and Circle earning $2.7 billion in 2025, stablecoins have become one of the most powerful business models in modern finance.

The Three Revenue Streams At a Glance

The table below compares how each revenue stream works, who depends on it most, and how it scales:

| Revenue Stream | How It Works | Primary Beneficiaries | Scaling Driver |

|---|---|---|---|

| Treasury yield | Interest from investing reserves in T-Bills and cash equivalents | Tether, Circle, PYUSD, USDG, RLUSD | Reserve size + interest rates |

| Transaction fees | Fees from merchant payments, conversions, and cross-border transfers | PYUSD, Visa, Mastercard, Fiserv | Payment volume + network reach |

| DeFi integration | Yield from lending, liquidity provision, and protocol fees | Sky (USDS/DAI), Ethena (USDe), Frax | DeFi adoption + TVL |

Most large issuers combine all three streams, but treasury yield dominates the revenue mix for fiat-backed stablecoins, while DeFi integration anchors the economics of crypto-native and synthetic issuers.

Revenue Stream 1: Treasury Yield on Reserves

Treasury yield is the dominant revenue stream for fiat-backed stablecoin issuers. The mechanics are straightforward.

How Treasury Yield Works

When a user deposits $1 with an issuer, they receive $1 worth of stablecoin in return.

- The issuer invests that $1 in short-term U.S. Treasuries, cash equivalents, repo agreements, or money market instruments, all of which yield interest in the 4% to 5% range in the current rate environment.

- The user receives zero interest on their stablecoin holding (with rare exceptions).

- The issuer keeps the spread between what the reserve earns and what the holder receives, which is effectively all of it.

At scale, this is one of the highest-margin financial businesses in existence. There is minimal capital risk (Treasuries are among the safest assets), low operating cost, and the revenue is essentially passive once the stablecoin is in circulation.

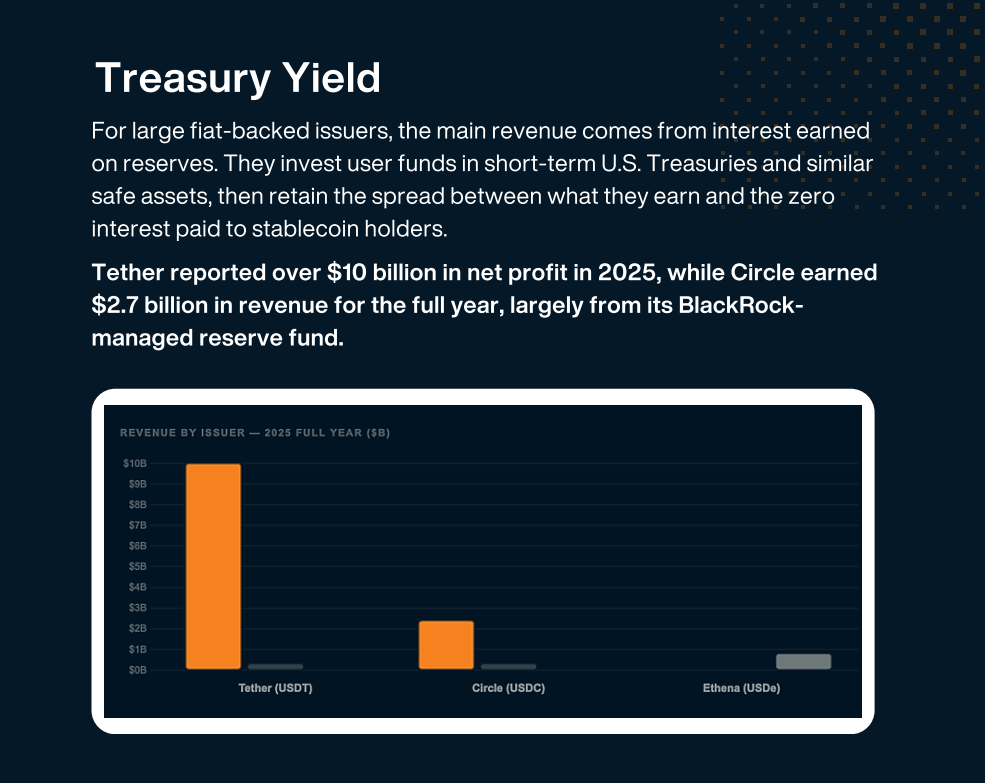

Tether's $10 Billion Profit Engine

Tether reported over $10 billion in net profit in 2025. With approximately $184 billion in USDT in circulation and reserves invested in Treasuries, secured loans, gold, Bitcoin, and other assets, even modest yield generates enormous revenue.

Tether's profitability now exceeds that of most global banks despite operating with a fraction of the headcount or regulatory overhead.

Tether's economics are also notable for the diversified reserve mix. Unlike pure fiat-backed issuers that hold only cash and Treasuries, Tether earns additional yield from secured loans and other higher-yielding assets, which is why its profit margins are among the highest in the industry.

Circle's $2.7 Billion Revenue Stream

Circle earned $2.7 billion in revenue in 2025, primarily from interest on the BlackRock-managed Circle Reserve Fund backing USDC. With approximately $79 billion in USDC supply, Circle holds reserves almost exclusively in cash and short-term Treasuries, generating consistent yield with minimal credit risk.

Circle's economics differ from Tether's in two important ways:

- Circle operates under tighter regulatory oversight and publishes weekly reserve disclosures, which constrains how it invests reserves but builds institutional trust.

- Circle shares more of its revenue with distribution partners (like Coinbase) than Tether does with its partners, which lowers headline profit margins but expands USDC's reach.

Other Fiat-Backed Issuers

The treasury-yield model also drives revenue for other major fiat-backed issuers:

- PYUSD (PayPal/Paxos): Reserve interest on U.S. dollar deposits and Treasuries held in segregated accounts.

- USDG (Global Dollar): Yield on MiCA-compliant reserves held at regulated European institutions.

- RLUSD (Ripple): Reserve interest on U.S. Treasuries and cash equivalents under NYDFS oversight.

For all of them, the formula is the same. Take in dollars, hold safe interest-bearing assets, keep the yield.

Revenue Stream 2: Transaction and Settlement Fees

As stablecoins shift from being primarily held to being actively used for payments and settlement, transaction-related revenue is becoming a growing share of issuer economics.

How Transaction Fees Work

Transaction fees come from several sources:

- Merchant payment fees when stablecoins are used to pay for goods and services

- Conversion fees when users move between fiat and stablecoin or between stablecoins

- Cross-border transfer fees for remittances and international settlement

- Platform integration fees when stablecoins are embedded into payment platforms

Unlike treasury yield, transaction-fee revenue scales with usage, not just reserve size. A stablecoin with $1 billion in reserves but $50 billion in annual transaction volume can generate meaningful fee revenue on top of its yield.

PYUSD and PayPal's Payment Integration

PYUSD benefits directly from PayPal's enormous consumer and merchant network. Every time PYUSD is used in a checkout flow, converted to fiat, or transferred between PayPal accounts, the broader PayPal ecosystem captures payment-style revenue.

PYUSD grew 726% in 2025, driven in large part by integrations like YouTube creator payouts, where transaction volume directly translates into platform monetization.

This is a fundamentally different economic model than holding-based stablecoins. PYUSD's value to PayPal is not just the reserve interest, but the way it deepens consumer engagement, reduces conversion costs, and creates new payment flows that PayPal can monetize.

Payment Network Economics: Visa, Mastercard, and Fiserv

Payment networks have emerged as a major economic layer in stablecoin transactions:

- Visa runs stablecoin settlement programs at approximately a $4.5 billion annualized rate, live across 18 countries with plans to expand to 100+ by the end of 2026. Visa earns fees on every settlement that flows through its network.

- Mastercard operates a stablecoin card ecosystem with 150 million+ merchant acceptance points, capturing card-network fees on stablecoin spending.

- Fiserv runs a white-label stablecoin platform (FIUSD) live across 10,000 banks and 6 million merchants, monetizing the infrastructure that enables bank-branded stablecoin issuance.

These networks are not stablecoin issuers, but they capture a growing share of the economic value created when stablecoins are spent rather than held.

On-Ramp and Infrastructure Economics

Infrastructure providers like Banxa monetize fiat-to-stablecoin conversion at a different layer. Banxa processes a transaction every 18 seconds across more than 200 countries, supports over 400 partner integrations including MetaMask, Trust Wallet, and Ledger, serves more than 8 million users globally, and processes over $10 billion in cumulative annual transactions.

Each transaction generates fee revenue tied to regulated on-ramp services.

The lesson: the more stablecoins shift toward being spent rather than just held, the more revenue flows to the infrastructure layer (payment networks, on-ramps) on top of issuer reserve yield.

Revenue Stream 3: DeFi Integration and Yield Strategies

Crypto-native and synthetic stablecoin issuers earn revenue through fundamentally different mechanisms. Instead of (or in addition to) treasury yield, they capture value through DeFi lending, liquidity provision, protocol fees, and yield-strategy execution.

How DeFi Integration Generates Revenue

DeFi-linked revenue comes from several sources:

- Lending interest when stablecoins are borrowed against collateral

- Liquidity provision fees when stablecoins are used in trading pairs

- Funding-rate capture from delta-neutral hedging positions

- Real-world asset (RWA) yields when protocols allocate reserves to tokenized Treasuries

- Savings rate spreads when protocols offer holders a yield below what they earn on reserves

The economics of DeFi-native issuers depend heavily on Total Value Locked (TVL), protocol activity, and the quality of yield-generation strategies.

1. Sky (USDS/DAI) Protocol Economics

Sky, the rebranded MakerDAO, earns revenue from multiple sources tied to USDS and DAI:

- Stability fees charged on crypto-collateralized debt positions

- RWA yields from allocations to tokenized Treasuries and other real-world assets

- Savings rate spread between what Sky earns on reserves and what it pays sUSDS holders

- Protocol fees from ecosystem integrations

With combined USDS and DAI supply exceeding $15 billion, Sky's revenue model is one of the most sophisticated in DeFi, blending DeFi-native fees with traditional reserve yield.

2. Ethena's Funding-Rate Capture

Ethena (USDe) operates a fundamentally different revenue model: funding-rate capture from delta-neutral positions. By holding spot crypto fully hedged with short futures positions, Ethena captures the funding rate paid by long futures traders to short traders during periods of bullish sentiment.

A portion of this yield is passed to sUSDe holders (Ethena's yield-bearing variant), and a portion is retained by the protocol.

With USDe at approximately $5.9 billion and historically attractive funding rates, Ethena has built one of the fastest-growing revenue models in crypto, though it is also more cyclical and sensitive to derivatives market conditions than treasury-yield-based models.

Other DeFi-Native Revenue Models

Other DeFi-native issuers monetize differently:

- Frax Finance earns through protocol fees, RWA exposure, and yield-bearing variants like sfrxUSD.

- Curve Finance (crvUSD) captures value through LLAMMA mechanics and integration with Curve's liquidity ecosystem.

- Aave (GHO) earns interest from minting GHO against collateral in Aave V3.

- Liquity (LUSD/BOLD) captures redemption fees and protocol-level revenue.

These models are smaller in absolute terms than treasury-yield issuers, but they represent the leading edge of how stablecoin economics are evolving in DeFi.

How Yield-Bearing Stablecoins Change the Economics

Yield-bearing stablecoins represent a structural shift in stablecoin economics. Instead of issuers keeping all of the reserve yield, a portion is passed to holders, creating a new competitive dynamic.

The Yield-Bearing Model

Yield-bearing stablecoins (like Ethena's sUSDe, Sky's sUSDS, Blast's USDB, and Frax's sfrxUSD) pay holders a portion of the underlying reserve or strategy yield. This forces issuers to compete on the size of the spread between what they earn and what they pass through.

The competitive implications are significant. A traditional fiat-backed stablecoin keeps the full reserve yield. A yield-bearing stablecoin might keep only 50% to 80% of the yield, passing the rest to holders. This narrows margins but expands demand by giving holders a reason to hold the stablecoin beyond just price stability.

Why Issuers Are Adopting It

Despite the lower margin per token, yield-bearing models are spreading because:

- They drive faster growth by attracting yield-seeking capital

- They differentiate against incumbents like USDT and USDC

- They are increasingly expected by sophisticated DeFi and institutional users

- They open new product categories like savings accounts and tokenized money markets

Yield-bearing stablecoins were among the fastest-growing in 2025:

- USDe (+145%)

- USDS (+74%)

- GHO (+245% growth in supply with sGHO layer)

- Tokenized Treasury products like USYC (+198%) and BUIDL (+30% in a single month)

Why So Many New Issuers Are Entering the Market

The economics of stablecoin issuance explain why such a diverse range of players is now racing to issue stablecoins.

The Stablecoin Issuance Landscape Q1 2026 Report identifies a wave of new entrants spanning fintechs (Fidelity, Tether's USAT, Tetra, Revolut, Robinhood), payment networks (Fiserv, Visa, Mastercard), DeFi protocols (Frax, Curve, Ripple), and banks and political entities (World Liberty's USD1, AllUnity's EURAU/CHFAU).

The common thread is economics:

- At $1B+ market cap, reserve yield alone generates tens of millions in annual revenue

- Issuers with built-in distribution (PayPal, Robinhood, Fidelity) layer transaction fees on top

- Yield-bearing models expand demand and accelerate scale

- Regulatory clarity (MiCA, GENIUS Act, NYDFS) reduces the cost of compliant operation

Combined, these factors make stablecoin issuance one of the most attractive business opportunities in financial services, which is why traditional banks, fintech giants, and crypto-native protocols are all entering simultaneously.

The Cost Side: What Issuers Spend To Operate

Stablecoin economics are not purely revenue. Issuers face real operating costs that scale with size and complexity.

Primary Cost Categories

- Compliance and legal: licensing, attestations, audits, and ongoing regulatory engagement

- Custody and banking: custodian fees (e.g., BNY Mellon for USDC), banking relationships, and reserve management

- Technology and operations: smart contract development, multi-chain deployment, security audits, and infrastructure

- Distribution partnerships: revenue shares with exchanges, wallets, and platforms that drive adoption (Circle reportedly shares a meaningful portion of USDC reserve yield with Coinbase)

- Risk management: insurance, hedging, and capital buffers for stress scenarios

For the largest issuers, total operating costs remain a small fraction of revenue, which is why headline profitability is so high.

Tether's lean operating model is the most extreme example, with reportedly under 100 employees managing over $184 billion in reserves.

Why Scale Is So Valuable

The cost structure of stablecoin issuance is heavily fixed. Compliance, technology, and infrastructure costs do not grow proportionally with reserves.

This means margins expand as issuers scale, which is why incumbents like Tether and Circle have such commanding economic advantages, and why new entrants are racing to reach $1B in supply (see the $1B club pillar for detail on what reaching that threshold unlocks).

How Stablecoin Economics Are Reshaping Payments

The economic flywheel of stablecoin issuance is starting to reshape the broader payments industry. Three shifts are underway.

1. Stablecoins Are Competing With Card Networks

Stablecoins offer near-zero transaction costs for transfers, compared to the 1.5% to 3% that card networks charge merchants.

As stablecoin payment infrastructure matures (through Visa, Mastercard, and Fiserv integrations), merchants gain a real alternative for settlement, and a share of payment revenue shifts from traditional networks to stablecoin issuers and infrastructure providers.

2. Cross-Border Remittances Are Being Disrupted

Cross-border remittances historically cost 5% to 7% in fees. Stablecoins on low-cost chains like Tron can move dollars internationally for cents.

The economic value created by this disruption flows to USDT (which dominates Tron-based transfers), to on-ramp providers like Banxa, and to consumer ecosystems like TON that embed stablecoin transfers natively in Telegram.

3. Treasury Operations Are Going On-Chain

Corporate and DAO treasuries are increasingly holding stablecoins rather than bank deposits, both for operational efficiency and because tokenized Treasury products (USYC, BUIDL) offer competitive yield with on-chain liquidity.

This shifts deposit revenue from traditional banks to stablecoin issuers and tokenized money market funds.

Why Stablecoin Economics Matter for Failure

The same economics that make successful stablecoins so profitable also explain why so many stablecoins fail. Without sufficient reserves, distribution, or operational scale, the model breaks down.

CoinGecko once tracked 370 stablecoins, and at least 23 have permanently lost their peg.

The main failure modes tied to economics:

- Weak collateral design: insufficient or reflexive backing collapses under stress (e.g., TerraUSD's $40B collapse)

- Lack of liquidity: thin markets accelerate depegs and erode trust

- Regulatory pressure: loss of banking access or licensing makes operations commercially unviable (e.g., BUSD's forced wind-down)

- Weak distribution: without scale, fixed operating costs exceed reserve yield revenue

- Protocol vulnerabilities: exploits like Acala USD's $1.28 billion over-mint destroy trust instantly

Profitable stablecoin issuance is not automatic. It requires reaching scale, maintaining regulatory clarity, and operating with discipline. The few issuers who manage all three earn billions; the many who do not, fail.

Conclusion

Stablecoin economics have turned the category into one of the most profitable business models in digital finance, with Tether earning over $10 billion in profit and Circle generating $2.7 billion in revenue in 2025 through treasury yield, transaction fees, and increasingly through DeFi integration and yield-bearing products.

While the revenue formula looks simple (hold reserves, invest in safe assets, keep the yield), executing it at scale requires reaching $1B+ in supply, maintaining regulatory clarity, and building durable distribution, which is precisely why so many fintechs, banks, payment networks, and DeFi protocols are now racing to issue stablecoins.

For the full breakdown of the top 100 stablecoins, the four design models, the multi-polar issuer map, and the $1B club, download the full Stablecoin Issuance Landscape Q1 2026 Report.

Read Next:

- New Report: Mapping the Top 100 Stablecoins and Their Future

- The Complete Guide to Stablecoin Design Models

- The $1B Stablecoin Club: Inside the Top 10 and Why They Dominate 95% of the Market

- Who Actually Issues Stablecoins: Inside the Multi-Polar Issuer Map

FAQs:

1. How do stablecoin issuers make money?

Stablecoin issuers make money primarily by investing user-deposited reserves into short-term U.S. Treasuries and similar safe assets, then keeping the interest while paying zero to stablecoin holders.

2. Why is Tether so profitable?

Tether is so profitable because it operates the largest stablecoin in the world (USDT at approximately $184 billion) with a lean operating model and a diversified reserve mix that includes Treasuries, secured loans, gold, and Bitcoin.

3. What are the three main revenue streams for stablecoin issuers?

The three main revenue streams for stablecoin issuers are treasury yield on reserves (the dominant source for fiat-backed stablecoins like USDT and USDC), transaction and settlement fees (growing with payments adoption through PYUSD, Visa, and Mastercard), and DeFi-linked yield and liquidity monetization (key for crypto-native and synthetic issuers like Sky and Ethena).

4. Do stablecoin holders earn interest?

Stablecoin holders typically do not earn interest on traditional fiat-backed stablecoins like USDT and USDC. The issuers keep the interest earned on reserves. However, a growing category of yield-bearing stablecoins (including Ethena's sUSDe, Sky's sUSDS, Blast's USDB, and Frax's sfrxUSD) does pass a portion of the underlying yield to holders, narrowing issuer margins but expanding demand by giving holders a reason to hold beyond price stability.

5. Why are so many companies launching stablecoins?

So many companies are launching stablecoins because the economics are exceptionally attractive: at $1 billion in reserves, even a 4% to 5% yield generates $40 to $50 million in annual revenue with minimal operating costs, scaling to multi-billion-dollar profits at $100 billion+ in supply.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

){kind=link}