Table of Contents

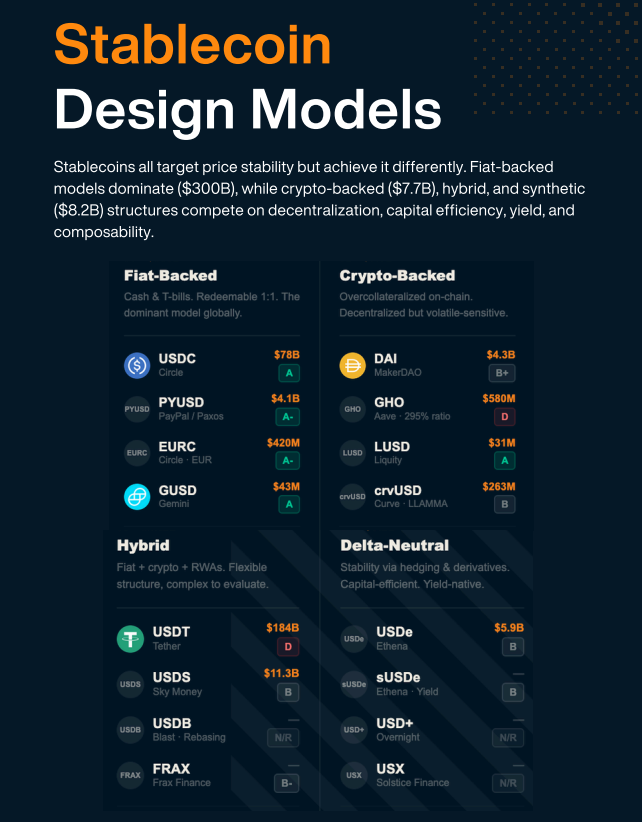

Stablecoin design models are the structural frameworks that determine how a stablecoin maintains its peg, with fiat-backed structures dominating at over $300 billion of the $320 billion total stablecoin market as of Q1 2026, according to the Stablecoin Issuance Landscape Q1 2026 Report.

While every stablecoin targets price stability, the way each one achieves that stability varies dramatically across four core models: fiat-backed, crypto-backed, hybrid, and delta-neutral/synthetic, each with distinct tradeoffs in decentralization, capital efficiency, yield, and risk.

This article breaks down all four design models in depth, explains how each peg mechanism actually works, maps which model fits which use case, and examines why some designs scale to hundreds of billions while others fail under market stress.

Key Takeaways

- Fiat-backed stablecoins dominate, holding over $300B of total market supply.

- Crypto-backed and synthetic models trade scale for decentralization and yield.

- Design choice directly determines a stablecoin's resilience, scale, and survival.

What Are Stablecoin Design Models

A stablecoin design model defines how a token maintains its peg to a reference asset, typically the U.S. dollar. The model determines what backs the token, how redemption works, how risk is managed, and ultimately how trustworthy and scalable the stablecoin becomes.

Per the Stablecoin Issuance Landscape Q1 2026 Report, the market currently breaks down into four primary models:

- Fiat-backed: ~$300B+ in market cap (the dominant model)

- Crypto-backed: ~$7.7B

- Hybrid: Multi-billion (combines reserve types)

- Delta-neutral/Synthetic: ~$8.2B

Despite hundreds of stablecoins existing, the top five: USDT, USDC, USDS, USDe, and USD1, control roughly 88–90% of total supply.

Design model is one of the strongest predictors of whether a stablecoin reaches scale or disappears.

Stablecoin Design Models At a Glance

The table below compares all four models across the dimensions that matter most for evaluation:

| Dimension | Fiat-Backed | Crypto-Backed | Hybrid | Synthetic |

|---|---|---|---|---|

| Collateral | Cash, T-Bills | Crypto (overcollateralized) | Mixed reserves | Spot + futures hedge |

| Market Cap (Q1 2026) | ~$300B+ | ~$7.7B | Multi-billion | ~$8.2B |

| Decentralization | Low | High | Medium | Medium |

| Capital Efficiency | 1:1 | Low (110–295%) | Variable | High |

| Yield Potential | Low (issuer keeps it) | Low | Often built-in | High (native) |

| Peg Mechanism | Direct redemption | Overcollateralization + liquidation | Mixed | Delta-neutral hedge |

| Primary Risk | Counterparty / banking | Volatility / liquidation | Complexity / opacity | Derivatives / funding rates |

| Example | USDC, USDT, PYUSD | DAI, LUSD, GHO | USDS, USDB | USDe, USD+ |

A Brief History of Stablecoin Design Models

Stablecoin design has changed through four clear phases:

- 2014–2017: Early fiat-backed experiments, led by USDT, prove that on-chain dollars work.

- 2018–2020: Crypto-backed designs mature, with DAI emerging as the leading decentralized alternative.

- 2021–2022: Algorithmic stablecoins surge, then collapse, TerraUSD's $40B implosion ends the pure-algorithmic era.

- 2023–2026: Synthetic and hybrid models emerge as the "next generation," while fiat-backed stablecoins absorb most of the market growth through fintech and institutional issuance.

This timeline matters because the market has effectively run a public experiment on each model.

- Fiat-backed survived and scaled.

- Crypto-backed survived but stayed small.

- Algorithmic failed.

- Synthetic is the newest entrant and still being stress-tested.

Fiat-Backed Stablecoins: The Dominant Model

Fiat-backed stablecoins are the most straightforward and widely used design. The issuer holds real-world reserves, cash, U.S. Treasuries, or cash equivalents, and users can redeem the token for one U.S. dollar (or equivalent) at any time.

How the Peg Works

The peg is maintained through direct 1:1 redemption with the issuer. Authorized participants can mint new tokens by depositing dollars and burn tokens by redeeming for dollars. Arbitrageurs keep the secondary market price tight to $1: if the token trades above $1, they mint and sell; if it trades below $1, they buy and redeem.

This is the simplest and most reliable peg mechanism, which is why this model dominates.

Leading Fiat-Backed Stablecoins

1. USDC (Circle): The leading transparent, institution-grade fiat-backed stablecoin. Backed 100% by cash and short-term U.S. Treasuries, with weekly disclosures, monthly independent audits, BNY Mellon as custodian, and BlackRock managing the reserve fund. Market cap is approximately $77–78 billion.

2. PYUSD (PayPal): The fintech-powered fiat-backed stablecoin. Issued by Paxos and fully backed by U.S. dollar deposits, Treasuries, and cash equivalents held in segregated, bankruptcy-remote accounts with monthly attestations. Market cap sits at around $4.0–4.3 billion.

3. EURC (Circle): Circle's euro-backed stablecoin, built with the same transparency standards as USDC. Market cap is approximately $420 million, demonstrating that high-quality non-USD stablecoins are viable but face lower demand than dollar versions.

4. GUSD (Gemini): The most conservative and regulation-focused fiat-backed stablecoin, earning a top Bluechip grade of A. Market cap is around $43 million.

Other notable fiat-backed stablecoins include TUSD, RLUSD, USDG, Paxos' USDP, exchange-focused FDUSD, Singapore's XSGD, and USDGLO.

Strengths and Weaknesses

- Strengths: Maximum scale, simple peg mechanism, strong regulatory positioning, easy institutional adoption.

- Weaknesses: Centralized issuer, counterparty risk, dependent on banking access, low yield for holders.

Crypto-Backed Stablecoins: Decentralization Over Scale

Crypto-backed stablecoins are backed by other cryptocurrencies instead of cash or Treasuries. They rely on overcollateralization, automated liquidations, and strict protocol rules to maintain their peg.

How the Peg Works

Users deposit crypto collateral (e.g., ETH) into a smart contract and mint stablecoins against it, typically at collateralization ratios of 110% to 295%. If the collateral value falls below a liquidation threshold, the position is automatically liquidated to protect the peg. Redemption is direct against the underlying collateral.

Some newer designs, like Curve's LLAMMA, use gradual rebalancing instead of sudden liquidations to smooth the experience.

Leading Crypto-Backed Stablecoins

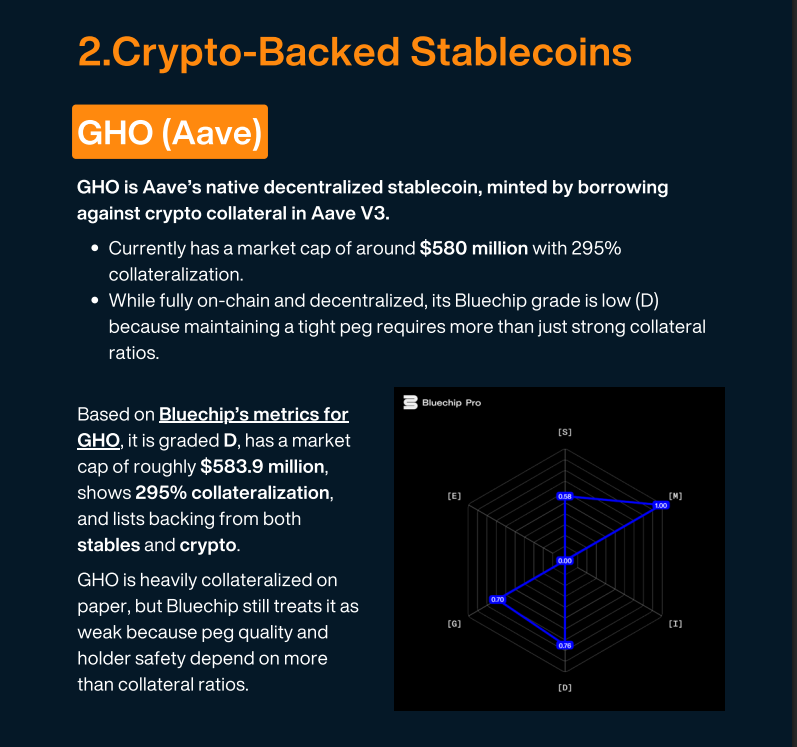

1. GHO (Aave): Aave's native decentralized stablecoin, minted by borrowing against crypto collateral in Aave V3. Market cap around $580 million with 295% collateralization. Bluechip grade D, overcollateralization alone doesn't guarantee a strong peg.

2. LUSD (Liquity): One of the purest crypto-backed designs. Fully decentralized with no admin keys, direct redeemability, and a 110% minimum collateral ratio. Bluechip grade A, market cap approximately $31 million.

3. crvUSD (Curve): Uses the innovative LLAMMA mechanism for gradual rebalancing instead of hard liquidations. Market cap around $263 million.

Other notable crypto-backed stablecoins include DAI (the most battle-tested), RAI (a niche non-pegged design), and BOLD (Liquity's newer product).

Strengths and Weaknesses

- Strengths: Fully on-chain, transparent, no banking dependency, censorship-resistant.

- Weaknesses: Capital-inefficient, vulnerable to volatility, struggles to scale, peg can wobble under stress.

Hybrid Stablecoins: Mixing Models for Flexibility

Hybrid stablecoins mix different backing methods. There are two distinct types of hybrids worth distinguishing:

- Reserve-hybrid: Holds mixed reserve types (cash + crypto + RWAs). Example: USDT.

- Mechanism-hybrid: Combines collateralization with algorithmic or yield-generating mechanisms. Example: FRAX, USDB.

How the Peg Works

Reserve-hybrids maintain the peg through redemption against a basket of mixed reserves, similar to fiat-backed but with more diverse collateral. Mechanism-hybrids combine multiple stabilizing forces: overcollateralization, algorithmic supply adjustment, yield strategies, or ecosystem incentives, making them harder to evaluate but more flexible.

Leading Hybrid Stablecoins

1. USDT (Tether): The largest stablecoin globally at approximately $184 billion. Backed by a mix of fiat, crypto, RWAs, and other assets. Bluechip grade D due to transparency concerns, but dominates through unmatched exchange integration and liquidity.

2. USDS (Sky Money): Sky Money's upgraded stablecoin, converting 1:1 with DAI. Market cap around $11.3 billion. Combines DeFi-native strengths with deeper exposure to centralized assets.

3. USDB (Blast): Blast's auto-rebasing stablecoin that earns yield from on-chain T-Bill strategies. Redeemable for DAI when exiting the ecosystem.

Other notable hybrid stablecoins include FRAX (blended collateral with algorithmic elements), USDD, and smaller ecosystem-specific dollars.

Strengths and Weaknesses

- Strengths: Flexibility, can layer yield, often pragmatic in regulatory and capital terms.

- Weaknesses: Harder to evaluate, can mask risk, transparency varies widely between issuers.

Delta-Neutral / Synthetic Stablecoins: Capital Efficiency Through Hedging

Delta-neutral and synthetic stablecoins create dollar stability through hedging, derivatives, and yield strategies rather than direct asset backing.

How the Peg Works

The issuer holds spot crypto (e.g., ETH) and simultaneously opens an equivalent short futures position. The two positions cancel each other out, creating a net-zero exposure to crypto price moves, a "delta-neutral" position worth a stable dollar amount. The funding rate paid by long futures traders to short traders becomes a source of yield, passed to holders through products like sUSDe.

This makes the model highly capital-efficient and yield-bearing, but tightly coupled to derivatives market health.

Leading Synthetic Stablecoins

1. USDe (Ethena): The leading synthetic dollar, holding spot crypto fully hedged with futures. Market cap approximately $5.9 billion, making up the majority of the synthetic category. Offers native yield through sUSDe.

2. USD+ (Overnight Protocol): A rebasing stablecoin paying yield via supply expansion based on yield-farming returns.

Other notable synthetic stablecoins include USX (Solstice Finance) and sUSDe (the yield-bearing version of USDe).

Strengths and Weaknesses

- Strengths: Capital-efficient, native yield, no banking dependency, crypto-native.

- Weaknesses: Depends on derivatives markets, funding-rate exposure, operational complexity, counterparty risk on hedging venues.

Synthetic vs Algorithmic: Clearing Up the Confusion

These two terms are often confused but represent very different designs.

- Algorithmic stablecoins maintain their peg purely through supply expansion and contraction driven by code, with little or no real collateral. TerraUSD (UST) was the most prominent example — and its $40 billion collapse effectively ended this design category.

- Synthetic stablecoins are fully collateralized but use derivatives to neutralize price exposure rather than holding a 1:1 dollar reserve. USDe is fully backed by spot crypto plus a short hedge, it is collateralized, just not in the way fiat-backed stablecoins are.

The key distinction: synthetic models have real backing; pure algorithmic models do not. This is why synthetic stablecoins are still operating at scale while algorithmic designs have largely disappeared from serious market consideration.

Use Case Mapping: Which Model Fits What

Different models are optimized for different real-world applications:

- Payments and merchant settlement: Fiat-backed (USDC, PYUSD, USDT). Redemption certainty and regulatory clarity matter most.

- Cross-border transfers: Fiat-backed on low-fee chains (USDT on Tron, USDC multi-chain). Speed and cost dominate the decision.

- DeFi collateral and lending: Crypto-backed (DAI, LUSD, crvUSD). Composability and on-chain transparency are essential.

- Treasury holdings (corporate / DAO): Fiat-backed with strong attestations (USDC, GUSD). Counterparty quality is paramount.

- Yield-seeking holdings: Synthetic (USDe/sUSDe) or hybrid (USDB, USDS with sUSDS). Native yield is the differentiator.

- Censorship-resistant savings: Crypto-backed with immutable contracts (LUSD). Decentralization is non-negotiable.

- Regional / non-USD use cases: Fiat-backed regional stablecoins (EURC, BRZ, XSGD). Local currency alignment removes FX friction.

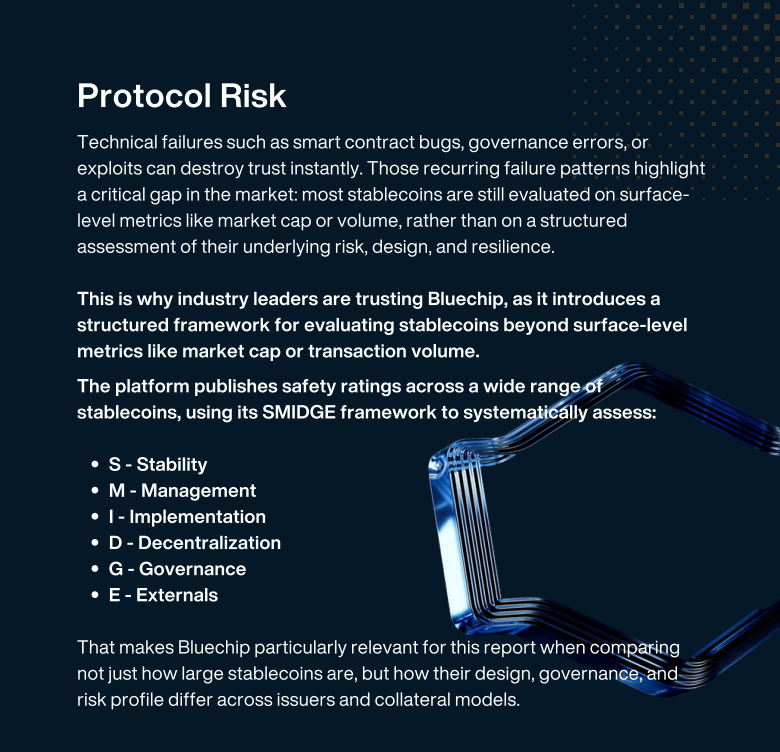

Understanding the Bluechip SMIDGE Framework

The Bluechip ratings referenced throughout this article come from the SMIDGE framework, which evaluates stablecoins beyond surface-level metrics like market cap.

SMIDGE stands for:

- S - Stability: How reliably the peg holds under stress.

- M - Management: Quality and competence of the issuing team.

- I - Implementation: Technical and operational execution.

- D - Decentralization: Degree of decentralization across governance and infrastructure.

- G - Governance: Quality of governance design and decision-making.

- E - Externals: Regulatory positioning, banking relationships, and external dependencies.

Grades range from A (highest) to D (lowest). The framework helps explain seeming contradictions in the market, for example, why USDT can dominate distribution while scoring poorly on Bluechip, or why LUSD scores higher than much larger competitors.

For deeper coverage of issuer evaluation, see the full breakdown in the Stablecoin Issuance Landscape Q1 2026 Report.

How the Four Models Compare in Practice

- USDT dominates distribution but scores poorly on Bluechip.

- USDC and PYUSD combine transparency with scale.

- LUSD scores well structurally despite its small size.

- GHO shows that overcollateralization alone doesn't guarantee a strong stablecoin.

- Synthetic models like USDe add yield and efficiency but compress more market and execution risk into one design.

The pattern is consistent: stablecoins that combine credible reserves with deep distribution win at scale; stablecoins that prioritize decentralization or yield win in narrower segments; stablecoins that rely on algorithmic mechanisms or opaque backing tend not to survive market stress.

Why Design Model Determines Survival

Most stablecoins do not survive. While CoinGecko once tracked 370 stablecoins, only a small number remain economically relevant today, and at least 23 stablecoins have permanently lost their peg.

Major failures including TerraUSD (UST), TerraClassicUSD (USTC), Deus Finance's DEI, flexUSD, Basis Cash (BAC), IRON Finance, Neutrino USD (USDN), Empty Set Dollar (ESD), USDX (Kava), and Acala USD (aUSD), share a common thread: weak collateral design, often combined with algorithmic mechanisms that couldn't withstand market stress.

The Stablecoin Issuance Landscape Q1 2026 Report identifies design model as one of the strongest predictors of long-term survival, alongside liquidity, regulation, distribution, and protocol security.

- Fiat-backed designs have proven the most resilient at scale

- Pure algorithmic models have repeatedly failed

- Crypto-backed and synthetic designs survive but face inherent capital and complexity ceilings.

Conclusion

Stablecoin design models: fiat-backed, crypto-backed, hybrid, and synthetic, define how a stablecoin maintains its peg, scales, and survives market stress, with fiat-backed structures dominating over $300 billion of the $320 billion total market.

While every model has tradeoffs, the data is clear: stablecoins that combine credible reserves, deep distribution, and reliable redemption consistently outperform more experimental designs at scale, while synthetic and crypto-backed models carve out important niches in yield and decentralization.

For the full breakdown, issuer maps, the $1B club, and the next 20 stablecoins likely to launch, download the full report.

FAQs:

1. What is the most dominant stablecoin design model?

The most dominant stablecoin design model is the fiat-backed model, accounting for over $300 billion of the $320 billion total stablecoin market as of Q1 2026.

2. What is the difference between fiat-backed and crypto-backed stablecoins?

The difference between fiat-backed and crypto-backed stablecoins is the nature of their collateral. Fiat-backed stablecoins are backed by real-world assets like cash and U.S. Treasuries held by an issuer, while crypto-backed stablecoins are backed by other cryptocurrencies held in overcollateralized on-chain vaults. Fiat-backed models scale larger and feel more like digital cash, while crypto-backed models prioritize decentralization and transparency.

3. What are synthetic stablecoins and how do they work?

Synthetic stablecoins are stablecoins that maintain a dollar peg through hedging strategies and derivatives rather than holding fiat or overcollateralized crypto reserves. The leading example is Ethena's USDe, which holds spot crypto assets fully hedged with futures contracts, creating a delta-neutral position.

4. What is the difference between synthetic and algorithmic stablecoins?

The difference between synthetic and algorithmic stablecoins is collateral. Synthetic stablecoins like USDe are fully collateralized with crypto assets but use derivatives to neutralize price exposure, while algorithmic stablecoins like the failed TerraUSD relied purely on code-driven supply adjustments with little or no real collateral. Synthetic designs remain operational at scale, whereas pure algorithmic designs have largely collapsed.

5. Why do most stablecoins fail?

Most stablecoins fail due to weak collateral design, lack of liquidity, regulatory pressure, weak distribution, or protocol vulnerabilities. The most catastrophic failures, like TerraUSD (UST), which caused an estimated $40 billion in losses, have been algorithmic or partially collateralized stablecoins whose backing mechanisms broke under market stress.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}