Table of Contents

Stablecoin issuers are the companies and protocols that create and back stablecoins, and as of Q1 2026 the market has evolved into a multi-polar landscape spanning crypto-native protocols, fintech platforms, exchanges, payment networks, and traditional banks, according to the Stablecoin Issuance Landscape Q1 2026 Report.

What began as a crypto-internal experiment dominated by a handful of protocols has become a contested arena where PayPal, Fidelity, Visa, Mastercard, and major banks like Goldman Sachs and UBS now compete alongside Tether, Circle, and Ethena.

This article maps the full issuer market, who builds stablecoins, what advantages each category brings, how the next 20 issuers are reshaping the market, and why distribution increasingly matters more than reserve design alone.

Key Takeaways

- Stablecoin issuance now spans crypto-native, fintech, bank, and payment players.

- Tether and Circle dominate, but institutional and fintech issuers are scaling fast.

- Distribution and regulation now decide issuer success more than design.

What Is a Stablecoin Issuer

A stablecoin issuer is the entity responsible for minting a stablecoin, holding or managing its backing, and ensuring redemption. The issuer determines the stablecoin's reserve quality, regulatory positioning, distribution reach, and ultimately the trust users place in it.

Based on the Stablecoin Issuance Landscape Q1 2026 Report, issuers now fall into five broad categories:

- Crypto-native issuers: Tether, Circle (originally), MakerDAO/Sky, Ethena, Liquity

- Fintech companies: PayPal, Circle, Paxos, Robinhood, Revolut

- Exchanges: Binance-linked and exchange-focused issuers

- Payment networks: Visa, Mastercard, Fiserv

- Financial institutions: Goldman Sachs, UBS, Barclays, and bank consortia

The market is no longer defined by a single type of issuer. It is multi-polar, and the balance of power is actively shifting toward issuers with the strongest distribution and regulatory positioning.

The Issuer Market At a Glance

The table below compares the five issuer categories across the dimensions that determine their competitive advantage:

| Issuer Type | Core Advantage | Main Weakness | Regulatory Posture | Example Issuers |

|---|---|---|---|---|

| Crypto-native | Innovation, DeFi integration, speed | Transparency, regulatory gaps | Weaker / offshore | Tether, Ethena, Sky, Liquity |

| Fintech | Consumer distribution, compliance | Smaller crypto-native reach | Strong | PayPal, Circle, Paxos |

| Exchanges | Liquidity, trading integration | Concentration risk | Mixed | Exchange-focused issuers |

| Payment networks | Merchant acceptance, settlement rails | Not native issuers | Strong | Visa, Mastercard, Fiserv |

| Financial institutions | Trust, deposits, treasury access | Slow, cautious entry | Strongest | Goldman, UBS, Barclays |

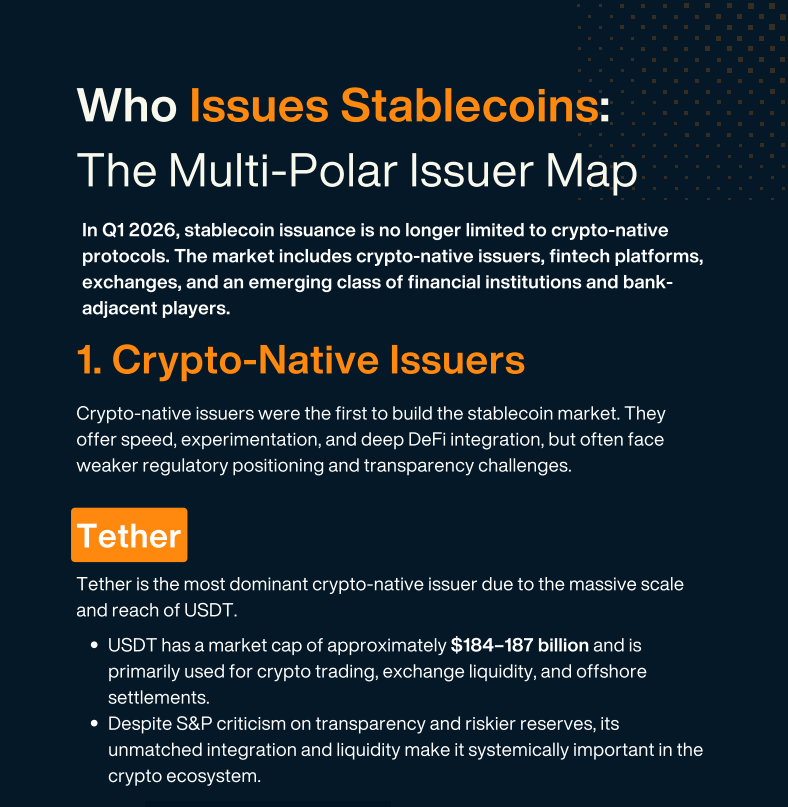

Crypto-Native Issuers: The Original Builders

Crypto-native issuers were the first to build the stablecoin market. They offer speed, experimentation, and deep DeFi integration, but often face weaker regulatory positioning and transparency challenges.

1. Tether

Tether is the most dominant crypto-native issuer due to the massive scale and reach of USDT. USDT has a market cap of approximately $184–187 billion and is primarily used for crypto trading, exchange liquidity, and offshore settlements.

Despite S&P criticism on transparency and riskier reserves, its unmatched integration and liquidity make it systemically important in the crypto ecosystem.

2. MakerDAO (Sky)

MakerDAO, now rebranded as Sky, pioneered protocol-governed stablecoin issuance with DAI. Users can seamlessly convert between DAI and the newer USDS at a 1:1 ratio. It proved that a decentralized protocol could create a durable on-chain dollar deeply integrated across DeFi, and Sky continues to evolve by building a broader ecosystem.

3. Ethena

Ethena represents the next wave of crypto-native innovation with its synthetic dollar USDe. It creates dollar stability through hedging strategies rather than holding fiat or overcollateralizing loans. Fast-moving and product-focused, it integrates both DeFi and centralized markets while offering native yield.

4. Liquity

Liquity offers one of the most extreme crypto-native designs with its LUSD stablecoin. The protocol is fully immutable with no admin keys, making issuance credibly neutral and non-discretionary. It prioritizes maximum decentralization at the expense of speed, marketing, and large-scale distribution.

Strengths and Weaknesses

- Strengths: Fastest innovation, deepest DeFi integration, credibly neutral options, first-mover liquidity.

- Weaknesses: Transparency concerns, weaker regulatory positioning, reputational risk under scrutiny.

Fintech Companies: Compliance Meets Consumer Distribution

Fintech companies bring strong regulatory compliance, banking relationships, and seamless payment integration, making them well-suited for embedding stablecoins into everyday commerce and treasury use.

1. PayPal

PayPal is the most visible mainstream fintech entering stablecoins with PYUSD. Issued by Paxos under regulatory oversight, PYUSD connects directly to PayPal's huge consumer and merchant network. It enables easy conversion between crypto, stablecoins, and fiat, helping stablecoins move into everyday payments and commerce.

2. Circle

Circle is the leading fintech company built specifically around stablecoin infrastructure with USDC. USDC is fully backed by regulated USD assets, with reserves managed by BlackRock and custodied at BNY Mellon. It combines issuance, transparent reserves, and asset management, positioning Circle as a trusted bridge between traditional finance and crypto.

3. Paxos

Paxos serves as a regulated infrastructure provider for stablecoins. It issues PYUSD for PayPal and its own USDP, both under OCC oversight with 100% cash-equivalent reserves. Paxos allows other companies to launch stablecoins quickly without building their own full compliance and custody infrastructure.

Strengths and Weaknesses

- Strengths: Built-in consumer distribution, strong compliance, banking relationships, enterprise readiness.

- Weaknesses: Less crypto-native depth, dependence on traditional rails, slower DeFi integration.

Payment Networks: Turning Stablecoins into Spendable Rails

Payment networks represent one of the most important shifts in the issuer landscape. They show that the next wave isn't only about issuing more tokens, it's about turning stablecoins into usable payment instruments at global scale.

1. Visa (with Bridge / Stripe)

Visa is building a stablecoin settlement network, already live in 18 countries with plans to expand to 100+ by the end of 2026. Visa's stablecoin settlement programs run at roughly a $4.5 billion annualized rate. This makes stablecoins spendable at global scale by integrating them as an additional settlement layer across Visa's existing network.

2. Mastercard (with MoonPay)

Mastercard is building a stablecoin card ecosystem, live with 150 million+ merchant acceptance points. Its card-linked model extends stablecoins into mainstream merchant acceptance, allowing stablecoin balances to be spent wherever Mastercard is accepted.

3. Fiserv

Fiserv operates a white-label stablecoin platform (FIUSD), live across 10,000 banks and 6 million merchants. Rather than issuing one dominant stablecoin, Fiserv is an infrastructure layer that could enable thousands of institutions to launch their own bank-branded stablecoins.

Strengths and Weaknesses

- Strengths: Unmatched merchant acceptance, settlement infrastructure, ability to make stablecoins spendable.

- Weaknesses: Not native issuers themselves, dependent on partner issuers, focused on rails rather than reserves.

Financial Institutions: The Cautious New Entrants

Traditional banks are increasingly exploring stablecoins and tokenized money, often preferring tokenized bank deposits over pure stablecoins.

Major banks such as Barclays, Goldman Sachs, and UBS are investing in stablecoin-related projects or forming consortia for G7 currency-pegged solutions. Some institutions, including the Bank of England, are considering whether tokenized commercial bank deposits might be more suitable than standalone stablecoins.

This approach keeps digital money inside the regulated banking system rather than outside it.

Strengths and Weaknesses

- Strengths: Highest trust, deep deposit relationships, treasury infrastructure, institutional flow access.

- Weaknesses: Slow and cautious, often prefer tokenized deposits over true stablecoins, regulatory conservatism.

The Infrastructure Layer: Issuers Aren't the Whole Story

A complete issuer map must account for participants that don't issue stablecoins at all but control critical access and movement of value. The report highlights two examples that sit on either side of the distribution layer.

1. On-ramp infrastructure (Banxa)

Banxa is not a stablecoin issuer or a blockchain, but it powers the integration of digital assets into existing platforms, processing a transaction every 18 seconds across more than 200 countries. It operates under Money Transmitter Licenses in the U.S. alongside full authorizations in the UK, Canada, Europe, and Australia, giving it one of the widest compliant footprints in the on-ramp category.

Its share of stablecoin issuance is zero by design, but its role in legally moving value between fiat and stablecoins makes it a distinct category of market participant.

2. Consumer ecosystems (TON)

TON is not an issuer either, but it has become a leading distribution surface by embedding stablecoin transfers directly into Telegram, where hundreds of millions of users can send and receive digital dollars natively. This gives certain stablecoins a structurally different path to adoption than chains that depend primarily on exchanges or DeFi protocols.

The lesson is that stablecoin issuance is increasingly tied to distribution rails, wallet access, app ecosystems, and payment infrastructure, not reserve design alone.

The Next 20 Issuers Reshaping the Map

The next wave of issuance is broader, more regulated, more regionally diversified, and tied to real payment and settlement infrastructure. Banks are protecting payment roles, fintechs are deepening consumer ecosystems, payment networks are turning stablecoins into spendable rails, and DeFi continues pushing yield-bearing programmable money.

Notable Upcoming Issuers by Category

Fintech:

- Fidelity Investments (FIDD, USD): Launched February 4, 2026, signaling major Wall Street validation that large financial platforms view stablecoins as core infrastructure.

- Tether (USAT, USD): Launched January 27, 2026, as a domestic U.S. compliant complement to offshore USDT, showing even the market leader needs domestic alignment.

- Tetra Digital Group (CADD, CAD): A credible Canadian dollar stablecoin backed by major Canadian institutions.

- Revolut (GBP stablecoin): In the FCA sandbox; a potential consumer-scale GBP stablecoin with major app distribution.

- Robinhood (USD stablecoin): Exploring since September 2024; could become a major retail-investor-facing stablecoin.

Payment Networks:

- Fiserv (FIUSD): Live across 10,000 banks and 6 million merchants; infrastructure enabling many bank-branded stablecoins.

- Visa / Bridge (Stripe): Settlement network live in 18 countries, targeting 100+ by end of 2026.

- Mastercard / MoonPay: Card-linked ecosystem with 150 million+ merchant acceptance points.

DeFi Protocols:

- Frax Finance (frxUSD / sfrxUSD): Yield-bearing, compliance-aware DeFi stablecoin model.

- Curve Finance (crvUSD / scrvUSD): Strong DeFi-native scaling path backed by deep liquidity.

- Ripple (RLUSD): Already at $1B scale, positioned for enterprise cross-border settlement.

Enterprise / Political:

- World Liberty Financial (USD1): One of the largest stablecoins at $5B+, showing the power of brand and political distribution.

- AllUnity (DWS / Galaxy / Flow Traders) (EURAU + CHFAU): Institutional non-USD on-chain cash, MiCAR-compliant.

A second major shift is currency diversification: next-cohort issuance includes EUR, HKD, JPY, CAD, GBP, and CHF alongside USD and multi-currency initiatives.

How Fast Can a New Issuer Reach Scale?

One of the most striking findings in the report is how quickly well-positioned issuers now reach the $1 billion mark, a milestone that once took years:

- USDT (Tether, launched 2014): ~3 years to reach $1B

- PYUSD (PayPal, launched Aug 2023): over a year

- USDe (Ethena, launched Feb 2024): roughly 6 weeks

- USDG (launched July 2025): ~5 months

- RLUSD (Ripple, launched Dec 2024): ~15 months

A well-backed stablecoin with strong distribution, compliance credibility, or ecosystem alignment can now cross the threshold in months rather than years, which is precisely why so many new issuers are entering the market.

Use Case Mapping: Which Issuer Type Fits What

Different issuer categories dominate different applications:

- Crypto trading and exchange liquidity: Crypto-native issuers (Tether's USDT).

- Consumer payments and commerce: Fintech issuers (PayPal's PYUSD).

- Merchant acceptance and settlement: Payment networks (Visa, Mastercard, Fiserv).

- DeFi lending and composability: Crypto-native DeFi protocols (Sky, Aave, Curve).

- Institutional treasury and tokenized cash: Financial institutions and regulated fintechs (Circle, banks).

- Regional / non-USD settlement: Regulated institutional issuers (AllUnity for EUR/CHF, Tetra for CAD).

- Cross-border enterprise settlement: Enterprise-aligned issuers (Ripple's RLUSD).

Why Distribution Now Beats Reserve Design

The clearest theme across the issuer map is that distribution and regulatory reach increasingly determine success more than reserve design alone.

Tether dominates not because it scores well on transparency, it earns a low Bluechip grade, but because of unmatched exchange integration and liquidity. PYUSD's advantage is PayPal's network, not a novel reserve structure. Visa and Mastercard matter because they make stablecoins spendable, not because they hold superior reserves.

The report frames this directly: stablecoin issuance is increasingly tied to who controls access, interfaces, and user flow.

Issuers that integrate with payment providers and consumer platforms gain an advantage because they meet users where they already are. This is why the next phase of competition is less about who can design the best reserve and more about who can reach the most users through the most channels.

Conclusion

The stablecoin issuer landscape in Q1 2026 is decisively multi-polar, spanning crypto-native protocols, fintech platforms, payment networks, financial institutions, and infrastructure players that don't issue at all but control access and movement.

While Tether and Circle still dominate by supply, the fastest-moving developments are coming from fintechs like PayPal and Fidelity, payment giants like Visa and Mastercard, and a growing wave of regulated, regionally diversified issuers, all competing on distribution and compliance as much as reserve design.

Read Next:

FAQs:

1. Who is the largest stablecoin issuer?

The largest stablecoin issuer is Tether, whose USDT stablecoin has a market cap of approximately $184–187 billion as of Q1 2026. Tether is a crypto-native issuer that dominates through unmatched exchange integration, liquidity, and global usage, despite ongoing transparency concerns and a low Bluechip rating. Circle, the issuer of USDC, is the second-largest at roughly $77–79 billion.

2. What types of companies issue stablecoins?

The types of companies that issue stablecoins fall into five main categories: crypto-native issuers (like Tether and Ethena), fintech companies (like PayPal and Circle), exchanges, payment networks (like Visa and Mastercard), and traditional financial institutions (like Goldman Sachs and UBS). As of Q1 2026, the market is multi-polar, with each category bringing different advantages in innovation, distribution, compliance, and trust.

3. Do banks issue stablecoins?

Banks are beginning to enter the stablecoin space, but cautiously, and many prefer tokenized bank deposits over standalone stablecoins. Major institutions like Barclays, Goldman Sachs, and UBS are investing in stablecoin projects or forming consortia for G7 currency-pegged solutions, while bodies like the Bank of England are exploring whether tokenized commercial bank deposits keep digital money safely inside the regulated banking system.

4. What is the difference between a stablecoin issuer and a payment network?

The difference between a stablecoin issuer and a payment network is their role in the stack: an issuer mints and backs the stablecoin itself, while a payment network like Visa or Mastercard makes stablecoins spendable by integrating them into settlement and merchant acceptance rails. Payment networks generally are not direct issuers, instead, they turn stablecoins issued by others into usable payment instruments at global scale.

5. How quickly can a new stablecoin issuer reach $1 billion?

A new stablecoin issuer can now reach $1 billion in months rather than years if it has strong distribution, compliance credibility, or ecosystem alignment. For example, Ethena's USDe crossed the threshold in roughly six weeks and USDG in about five months, compared with the three years it took Tether's USDT after its 2014 launch. This acceleration reflects how much distribution and regulatory positioning now matter for new issuers.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}