Table of Contents

The $1B stablecoin club is the group of stablecoins with a market cap above $1 billion, and as of Q1 2026 just 10 stablecoins meet that threshold while controlling approximately 95.7% of the entire $311 billion stablecoin market, according to the Stablecoin Issuance Landscape Q1 2026 Report.

Despite hundreds of stablecoins having launched, the market has remained extraordinarily concentrated, with USDT and USDC alone accounting for over $263 billion combined, and the entire $1B+ tier representing roughly $297.5 billion in supply.

This article profiles all 10 members of the $1B club, breaks down their reserve composition and Bluechip grades, examines the $1B graveyard of former giants that collapsed, identifies the next entrants approaching the threshold, and explains why concentration in stablecoins has barely shifted despite hundreds of launches.

Key Takeaways

- The top 10 stablecoins control ~95.7% of total stablecoin market supply.

- Time-to-$1B has dropped from 3 years (USDT) to weeks (USDe).

- Fiat-backed and reserve-led models still anchor the entire $1B tier.

What Is the $1B Stablecoin Club

The $1B stablecoin club refers to the group of stablecoins with a market capitalization above $1 billion. It is the small tier of tokens that have achieved the scale, liquidity, and trust required to function as systemic monetary infrastructure rather than experimental products.

Per the Stablecoin Issuance Landscape Q1 2026 Report, the $1B club currently has 10 members:

- USDT (Tether): $184.08B

- USDC (Circle): $79.16B

- USDS (Sky Money): $11.26B

- USDe (Ethena): $5.92B

- USD1 (World Liberty Financial): $4.59B

- DAI (Sky/MakerDAO): $4.30B

- PYUSD (PayPal): $4.13B

- USDG (Global Dollar): $1.77B

- USDF: $1.75B

- RLUSD (Ripple): $1.55B

Combined, these 10 stablecoins represent approximately $297.5 billion against a total stablecoin market of ~$311 billion, or roughly 95.7% concentration in just ten tokens.

Top 5 vs Top 10: Concentration Inside Concentration

Even within the $1B club, dominance is unevenly distributed. The top 5 stablecoins alone (USDT, USDC, USDS, USDe, and USD1) hold approximately $285 billion combined, representing roughly 88 to 90% of the entire stablecoin market. The next five members (DAI, PYUSD, USDG, USDF, RLUSD) collectively add another ~$12.5 billion to bring the top 10 to 95.7%.

This means the $1B club has two distinct tiers:

- Tier 1 (Top 5): Systemically dominant, accounting for nearly 90% of all supply.

- Tier 2 (Ranks 6 to 10): Important and fast-growing, but collectively smaller than USDS alone.

Concentration is not just "top 10 dominates." It is "top 2 dominates everything." USDT and USDC alone control roughly 84% of total stablecoin supply.

Why the $1B Threshold Matters

The $1B mark is more than a vanity number. It signals that a stablecoin has achieved:

- Deep liquidity across major exchanges and DeFi venues

- Reliable redemption at scale, even under stress

- Multi-chain distribution across leading networks

- Institutional or fintech trust required for treasury use

- Survivability, since most stablecoins never reach this scale

CoinGecko once tracked 370 stablecoins, and at least 23 have permanently lost their peg. Crossing $1B effectively separates the systemically relevant stablecoins from the long tail of experimental, regional, or failed projects.

The $1B Club At a Glance

The table below compares all 10 members across the dimensions that define their position:

| Stablecoin | Market Cap | Issuer | Design Model | Bluechip Grade | Primary Use Case |

|---|---|---|---|---|---|

| USDT | $184.08B | Tether | Hybrid (reserve-mix) | D | Exchange liquidity, offshore settlement |

| USDC | $79.16B | Circle | Fiat-backed | A | Institutional, payments, DeFi |

| USDS | $11.26B | Sky Money | Hybrid | n/a | DeFi-native dollar |

| USDe | $5.92B | Ethena | Synthetic | n/a | Yield-bearing dollar |

| USD1 | $4.59B | World Liberty Financial | Fiat-backed | n/a | Brand / political distribution |

| DAI | $4.30B | Sky / MakerDAO | Crypto-backed | B | DeFi composability |

| PYUSD | $4.13B | PayPal (Paxos) | Fiat-backed | A | Consumer payments |

| USDG | $1.77B | Global Dollar | Fiat-backed | n/a | MiCA-compliant European usage |

| USDF | $1.75B | various | Structured / dollar-linked | n/a | Structured collateral |

| RLUSD | $1.55B | Ripple | Fiat-backed | n/a | Enterprise cross-border settlement |

Note: Bluechip's SMIDGE framework evaluates Stability, Management, Implementation, Decentralization, Governance, and Externals. Grades for newer entrants are still being assigned. For the full grading methodology, see the design models pillar.

Reserve Composition: What Actually Backs the $1B Club

Reserve composition is one of the strongest differentiators in the $1B tier. While all members claim full backing, what backs them varies significantly:

- USDT: A mix of cash and cash equivalents, U.S. Treasuries, secured loans, Bitcoin, gold, and other investments. The diverse reserve mix is why USDT is classified as a hybrid rather than pure fiat-backed.

- USDC: 100% cash and short-term U.S. Treasuries. Reserves are custodied at BNY Mellon and managed by BlackRock through the Circle Reserve Fund, with weekly disclosures and monthly attestations.

- PYUSD: 100% U.S. dollar deposits, U.S. Treasuries, and cash equivalents held in segregated, bankruptcy-remote accounts, with monthly Paxos attestations under OCC oversight.

- USDS / DAI: Backed by a mix of crypto collateral, real-world assets, and other on-chain reserves managed through the Sky protocol.

- USDe: Backed by spot crypto (ETH, BTC, and other assets) fully hedged with short futures positions, creating a delta-neutral synthetic dollar.

- USDG: Fully reserved with cash and short-term Treasuries under MiCA-compliant frameworks held at regulated European institutions.

- RLUSD: 100% backed by U.S. dollar deposits, short-term U.S. government Treasuries, and cash equivalents under NYDFS oversight.

The pattern: the most transparently reserved stablecoins (USDC, PYUSD, RLUSD) hold near-100% cash and Treasuries. USDT, the largest by far, holds the most diversified and least transparent reserve mix.

Profiling the $1B Club

1. USDT: The Undisputed Leader

USDT is the largest stablecoin by an enormous margin, with a market cap of approximately $184 billion, more than twice the size of every other stablecoin combined. Issued by Tether and backed by a mix of fiat, crypto, RWAs, and other assets, USDT dominates through unmatched exchange integration, deep liquidity, and global usage, particularly in offshore markets and emerging economies.

It earns a low Bluechip grade (D) due to transparency concerns, yet remains systemically important.

2. USDC: The Institutional Standard

USDC is the second-largest stablecoin and the institutional standard for fiat-backed digital dollars. With a market cap of approximately $79 billion, USDC is fully backed by cash and short-term U.S. Treasuries, with BNY Mellon as custodian and BlackRock managing the reserve fund.

Its weekly disclosures, monthly attestations, and regulated banking relationships make it the preferred choice for institutional treasury, regulated DeFi, and compliant payments.

3. USDS: Sky's DeFi-Native Dollar

USDS is Sky Money's upgraded stablecoin, converting 1:1 with DAI. With a market cap of approximately $11.3 billion, it crossed the $10B threshold in 2025, supported by the DAI-to-USDS transition and the yield-bearing sUSDS layer.

It combines DeFi-native strengths with deeper exposure to centralized assets, representing a hybrid design by economic intent.

4. USDe: The Synthetic Dollar Breakout

USDe is the leading synthetic dollar and the breakout story of the past two years. With a market cap of approximately $5.9 billion, it creates dollar stability through delta-neutral hedging, holding spot crypto fully hedged with futures, and offers native yield through sUSDe. It is the largest non-fiat-backed stablecoin in the $1B club and grew 145% in 2025.

5. USD1: Brand-Powered Distribution

USD1, issued by World Liberty Financial, has reached approximately $4.59 billion in market cap, demonstrating how brand power and political distribution can drive immediate scale. It is one of the clearest examples of how distribution and narrative can rival reserve design in driving adoption.

6. DAI: The Battle-Tested Original

DAI is the original decentralized crypto-backed stablecoin and remains one of the most battle-tested designs in the market. With a market cap of approximately $4.3 billion, it now coexists with USDS under the Sky ecosystem and continues to anchor DeFi composability and on-chain credit markets.

7. PYUSD: Fintech Distribution at Scale

PYUSD, PayPal's stablecoin issued by Paxos, has reached approximately $4.13 billion in market cap. Its strength lies in direct integration with PayPal's massive consumer and merchant network, plus expansion onto Solana (~$759M on Solana alone). PYUSD grew 726% in 2025, among the fastest growth rates in the entire market.

8. USDG: MiCA-Compliant European Growth

USDG, the Global Dollar, reached approximately $1.77 billion in market cap and crossed $1B in just five months after its July 2025 launch. As a MiCA-compliant stablecoin, it has expanded rapidly in Europe through partnerships with Robinhood and Mastercard, showing how regulatory alignment can drive accelerated growth.

9. USDF: Structured Collateral Growth

USDF sits at approximately $1.75 billion in market cap, representing a category of dollar-linked stablecoins built around structured backing frameworks rather than pure fiat reserves. Its inclusion in the $1B tier signals growing market acceptance of more sophisticated reserve structures.

10. RLUSD: Ripple's Enterprise Play

RLUSD, issued by Ripple, has reached approximately $1.55 billion in market cap roughly 15 months after its December 2024 launch. Positioned for enterprise cross-border settlement, it represents the convergence of crypto-native and enterprise settlement models, bringing institutional credibility to on-chain dollars.

The $1B Graveyard: Stablecoins That Used to Be Here

The current $1B club tells only half the story. Several stablecoins once held positions in the club and have since collapsed, been forced to wind down, or permanently lost their peg. Their failures shaped the modern market structure.

TerraUSD (UST): The Largest Stablecoin Collapse in History

UST reached approximately $18 billion in market cap before its catastrophic collapse in May 2022. As an algorithmic stablecoin backed by the Luna token rather than real reserves, UST broke its peg when its reflexive mechanism failed under market stress. The collapse caused an estimated $40 billion in total investor losses and effectively ended the era of pure algorithmic stablecoins as a serious design category.

BUSD: Forced Wind-Down by Regulation

Binance USD (BUSD), issued by Paxos, peaked above $20 billion before the New York Department of Financial Services ordered Paxos to stop minting new BUSD in February 2023. The token was not a design failure. It was fully reserved and compliant. But regulatory action made it commercially unviable, demonstrating that even structurally sound stablecoins can be removed from the $1B club by external forces.

Other Notable Collapses

The broader graveyard includes TerraClassicUSD (USTC, the remnant of UST), Neutrino USD (USDN), Deus Finance's DEI, flexUSD, IRON Finance, Acala USD (aUSD, where a vulnerability allowed over $1.28 billion in extra tokens to be minted), Empty Set Dollar (ESD), Dynamic Set Dollar (DSD), and USDX (Kava).

The pattern across the graveyard is consistent: algorithmic designs, weak collateral, regulatory pressure, or protocol vulnerabilities. No fully reserved, transparently audited fiat-backed stablecoin has collapsed from the $1B tier, reinforcing why fiat-backed structures continue to dominate.

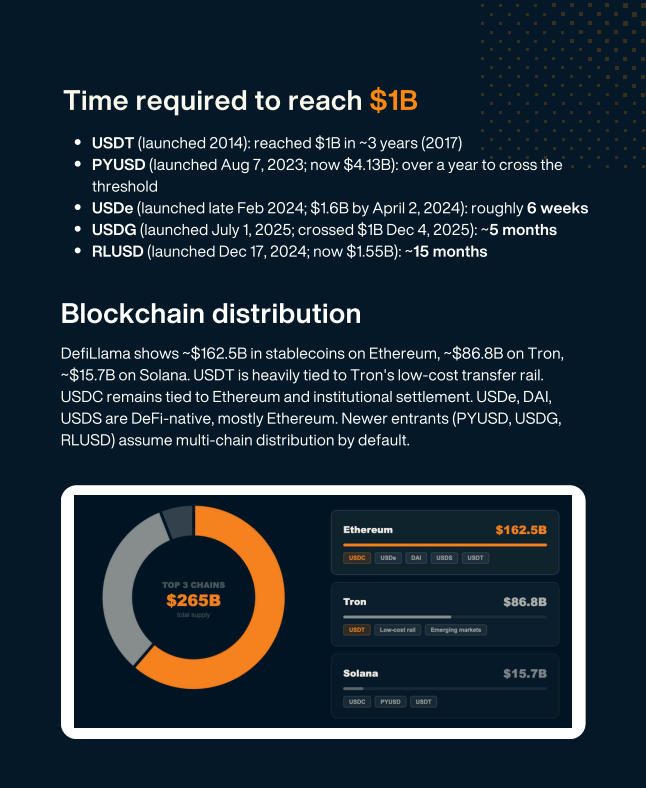

How Time-to-$1B Has Accelerated

One of the most striking findings in the report is how quickly stablecoins now reach the $1B threshold. What once took years now takes months, or even weeks.

| Stablecoin | Launch Date | Time to $1B |

|---|---|---|

| USDT | 2014 | ~3 years |

| PYUSD | August 2023 | over 1 year |

| RLUSD | December 2024 | ~15 months |

| USDG | July 2025 | ~5 months |

| USDe | February 2024 | ~6 weeks |

This acceleration reflects three structural changes in the market:

- Pre-built distribution channels: issuers tied to PayPal, Ripple, or established crypto exchanges launch with immediate audience access.

- Compliance credibility: MiCA-aligned and OCC-overseen stablecoins attract institutional capital quickly.

- Demand for yield: synthetic and yield-bearing stablecoins like USDe see explosive demand from yield-seeking holders.

A well-backed stablecoin with strong distribution, compliance positioning, or ecosystem alignment can now cross $1B faster than any prior wave of issuers.

The Near-$1B Tier: Who's Coming Next

Just below the $1B threshold sits a tier of stablecoins growing rapidly and likely to enter the club in the near term. These represent the next layer of competition for the top of the market.

- USYC (Circle): Tokenized Treasury product at ~$2.2 billion, growing 198% in 2025 and recently surpassing BlackRock's BUIDL. Driven by institutional collateral demand, especially after Binance accepted it as off-exchange collateral.

- BUIDL (BlackRock): Tokenized Treasury fund growing 30% in a single month after Uniswap integration, signaling institutional cash moving on-chain.

- GHO (Aave): Aave's native decentralized stablecoin reached ~$580 million in 2025, with holder count up ~300% and cross-chain expansion accelerating.

- EURC (Circle): The leading euro stablecoin at ~$428 million, representing over 40% of the total euro stablecoin market.

- crvUSD (Curve): Grew nearly 3x in 2025 to over $361 million, driven by deep integration as collateral within Curve's liquidity ecosystem.

- FDUSD: Exchange-focused fiat-backed stablecoin maintaining significant supply tied to trading flows.

- FRAX: DeFi-native stablecoin with blended collateral and yield-bearing variants positioning for renewed growth.

These near-$1B stablecoins share two characteristics: institutional or DeFi-native backing, and clear product-market fit in specific niches (tokenized Treasuries, euro, decentralized collateral).

The composition of the next $1B club entrants suggests the tier will become more diverse, with non-USD stablecoins and tokenized Treasury products likely to gain proportionally more representation.

Why Fiat-Backed Models Still Dominate the $1B Tier

The $1B club is overwhelmingly shaped by fiat-backed and reserve-led issuance. USDT, USDC, PYUSD, USDG, RLUSD, and USD1 are all fiat-backed or fiat-linked. Even USDS and USDF, while more nuanced, are dollar-linked with strong reserve, collateral, or structured-backing frameworks. The only true non-fiat outliers in the club are USDe (synthetic) and DAI (crypto-backed).

At scale, users still favor stablecoins that feel closest to digital cash, meaning directly redeemable, transparently backed, and regulatorily clear. Crypto-backed and synthetic designs survive and innovate, but the vast majority of capital concentrates in stablecoins built around clear reserve structures.

This pattern reinforces a finding from the broader Stablecoin Issuance Landscape Q1 2026 Report: design model is one of the strongest predictors of long-term scale.

Chain Distribution Patterns Across the $1B Club

The $1B stablecoins are not distributed evenly across blockchains. DeFiLlama data shows three networks anchoring the majority of supply:

- Ethereum: ~$162.5B in stablecoin supply (~52 to 55% of all stablecoins)

- Tron: ~$86.8B, heavily dominated by USDT

- Solana: ~$15.7B, growing through USDC and PYUSD

Chain Footprints by Stablecoin

Each $1B club member shows a distinct chain footprint:

- USDT is heavily tied to Tron's low-cost transfer rail, which dominates emerging-market remittances and offshore settlement.

- USDC remains anchored to Ethereum and institutional settlement, with growing multi-chain distribution including Solana.

- USDe, DAI, and USDS are DeFi-native and primarily live on Ethereum.

- PYUSD, USDG, and RLUSD assume multi-chain distribution by default, with significant Solana presence.

The pattern: incumbent stablecoins concentrate where their primary use case lives (Tron for transfers, Ethereum for DeFi), while newer entrants launch multi-chain from day one.

Supply vs Transaction Volume: Holdings Aren't Usage

Market cap measures how much of a stablecoin is held, not how much is actually used. The two diverge significantly across the $1B club.

The broader stablecoin market handled approximately $33 trillion in on-chain transaction volume in 2025, up 72% year-over-year. Visa separately reports approximately $10.2 trillion in adjusted stablecoin transaction volume over the past 12 months.

Average circulating supply hovers around $250 billion, meaning the supply turns over many times per year.

Activity Profile of Each Member

The pattern across the $1B club:

- USDT drives a disproportionate share of total transaction volume, particularly on Tron, where its low-fee transfers dominate emerging-market remittances and offshore settlement flows.

- USDC sees high transaction volume in institutional and DeFi contexts but lower retail transfer activity than USDT.

- PYUSD is growing rapidly in transaction volume relative to supply through PayPal's payment integrations.

- USDe has high holdings activity (deposits into sUSDe for yield) but lower payment-style transaction volume.

A useful framing: USDT is the world's transactional stablecoin, USDC is the world's institutional reserve stablecoin, and the rest of the $1B club is still defining its primary activity profile.

Stablecoin Economics: Why $1B Status Is So Valuable

Reaching $1B is not just a scale milestone. It is the threshold at which stablecoin issuance becomes one of the most profitable business models in digital finance. Issuers earn revenue primarily by investing user-deposited reserves into safe short-term instruments and keeping the interest, while passing zero interest to stablecoin holders.

Revenue Profiles at the Top of the Club

The economics at the top of the $1B club:

- Tether reported over $10 billion in net profit in 2025, primarily from interest on its $184B+ reserve base.

- Circle earned $2.7 billion in revenue in 2025, largely from the BlackRock-managed Circle Reserve Fund backing USDC.

- PYUSD captures additional revenue through transaction fees from PayPal's consumer and merchant network on top of reserve interest.

- Sky (USDS/DAI) earns through protocol fees, RWA yields, and the savings rate spread.

- Ethena (USDe) generates revenue from funding-rate capture on hedging positions, with a portion passed to sUSDe holders as yield.

At $1B+ market cap, even a modest reserve interest spread compounds into hundreds of millions of dollars in annual revenue. This is precisely why so many issuers (fintechs, banks, payment networks, and political entities) are racing to launch stablecoins.

The economics make the category one of the most attractive business models in modern finance. For deeper coverage of stablecoin business models, see the stablecoin economics pillar.

Market Share Trends: Who's Gaining, Who's Losing

Within the $1B club, market share is shifting more than overall concentration suggests:

- USDT continues to grow in absolute terms but its share of the total stablecoin market has slowly compressed as new entrants scale.

- USDC rebounded strongly after the March 2023 SVB exposure, with Banxa reporting USDC volumes surged ~400% in 2025 driven by MiCA-related shifts in Europe.

- USDT volumes on Banxa's platform dropped ~60% in 2025 due to MiCA delistings, a localized but telling indicator of regulatory pressure.

- PYUSD, USDG, and RLUSD are all newer entrants gaining share rapidly, particularly in regions where compliance positioning matters.

- DAI/USDS as a combined Sky ecosystem is holding share through the migration rather than growing aggressively.

The takeaway: total concentration in the top 10 remains stable (~95.7%), but the composition inside the club is shifting toward more regulated, more distributed, and more diversified issuers.

Concentration and Systemic Risk

The level of concentration in the $1B club creates real systemic considerations. A depeg or collapse at the top of the tier would have outsized market consequences:

- USDT at $184B is now larger than most national money market funds. A loss of confidence would have cascading effects across exchanges, DeFi, and emerging-market remittance flows.

- USDC at $79B is deeply embedded in regulated DeFi, institutional treasury, and payment platforms. Its 2023 SVB exposure caused a temporary depeg that rippled through DeFi for days.

- The combined ~$263B in USDT and USDC represents single-issuer risk concentrations that didn't exist in earlier crypto cycles.

The history of the $1B graveyard (UST's $18B collapse, BUSD's $20B forced wind-down) shows that even the largest stablecoins are not immune to failure. Regulators worldwide, including the Bank of England, the EU under MiCA, and U.S. authorities under the GENIUS Act framework, are increasingly focused on this concentration risk.

Why the Market Remains So Concentrated

Despite hundreds of stablecoins existing, market concentration has barely budged. The top three (USDT, USDC, DAI) represented 94% of total market cap in 2024, and the top 10 represent ~95.7% in Q1 2026. The market has broadened in count but not in power.

Concentration persists for four reasons:

- Liquidity begets liquidity: the largest stablecoins offer the deepest order books, attracting more users and reinforcing dominance.

- Trust accumulates slowly: stablecoins that survive multiple market cycles (USDT through 2018 to 2026, USDC through SVB exposure in 2023) earn structural trust that newcomers cannot replicate quickly.

- Distribution moats: Tether's exchange integration and Circle's institutional relationships are not easily reproduced.

- Switching costs: businesses, exchanges, and DeFi protocols built around incumbent stablecoins face real friction in migrating.

The $1B club expands, but the top of the club barely changes.

Use Case Mapping: Which $1B Stablecoin Fits What

Different members of the $1B club dominate different applications:

- Crypto trading and offshore settlement: USDT.

- Institutional treasury and regulated DeFi: USDC.

- DeFi composability and on-chain credit: DAI, USDS.

- Yield-bearing holdings: USDe (via sUSDe), USDS (via sUSDS).

- Consumer payments and commerce: PYUSD.

- European MiCA-compliant flows: USDG.

- Enterprise cross-border settlement: RLUSD.

- Brand- and narrative-driven exposure: USD1.

Conclusion

The $1B stablecoin club is the structural backbone of the entire stablecoin market, with just 10 tokens controlling ~95.7% of the $311 billion total supply and demonstrating that scale, distribution, reliable redemption, and reserve quality matter more than launch volume.

While USDT and USDC continue to dominate and the $1B graveyard of UST and BUSD warns of how fast giants can fall, the broader tier shows how quickly new entrants like USDG, RLUSD, and USDe can scale when they combine credible backing with strong distribution and regulatory alignment.

For the full breakdown of the top 100 stablecoins, the four design models, the multi-polar issuer map, and the next 20 stablecoins likely to launch, download the full Stablecoin Issuance Landscape Q1 2026 Report.

Read Next:

- The Complete Guide to Stablecoin Design Models

- New Report: Mapping the Top 100 Stablecoins and Their Future

FAQs:

1. What is the $1B stablecoin club?

The $1B stablecoin club is the group of stablecoins with a market capitalization above $1 billion, currently consisting of just 10 tokens: USDT, USDC, USDS, USDe, USD1, DAI, PYUSD, USDG, USDF, and RLUSD. Combined, they hold approximately $297.5 billion against a total stablecoin market of ~$311 billion, representing roughly 95.7% concentration in just ten stablecoins.

2. Which stablecoin has the largest market cap?

The stablecoin with the largest market cap is USDT (Tether), at approximately $184 billion as of Q1 2026, more than twice the size of every other stablecoin combined. USDC, issued by Circle, is the second-largest at roughly $79 billion. Together, USDT and USDC account for over $263 billion, or about 84% of total stablecoin supply.

3. How long does it take a new stablecoin to reach $1 billion?

The time it takes a new stablecoin to reach $1 billion has accelerated dramatically, from roughly three years for USDT (launched in 2014) to just six weeks for Ethena's USDe (launched in February 2024). USDG crossed the threshold in about five months after its July 2025 launch, while RLUSD took roughly 15 months. Strong distribution, compliance credibility, or ecosystem alignment can now drive a stablecoin to $1B in months rather than years.

4. Why are stablecoins so concentrated in just a few tokens?

Stablecoins are so concentrated in just a few tokens because liquidity, trust, distribution, and switching costs all reinforce incumbent dominance. The largest stablecoins offer the deepest order books, have survived multiple market cycles, and are deeply embedded in exchanges, DeFi protocols, and payment platforms. While many new stablecoins launch each year, the top 10 still control approximately 95.7% of total market supply.

5. Which stablecoins grew the fastest in 2025?

The fastest-growing stablecoins in 2025 included PYUSD (+726%), USDG (+169%), USDe (+145%), and USDS (+74%). PYUSD's growth was driven by PayPal's consumer network and YouTube creator payouts, USDe by its native yield through sUSDe, USDG by MiCA-compliant European expansion, and USDS by the DAI-to-USDS transition. The fastest-growing stablecoins generally combine yield-bearing design, regulatory alignment, or strong distribution partnerships.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}