Table of Contents

Real-world asset (RWA) tokenization is the practice of representing claims on traditional financial instruments, like U.S. Treasury bills, money market funds, or bank deposits, using blockchain-based tokens.

In the stablecoin economy, the first large “product-market fit” for RWAs has been tokenized cash management, especially tokenized Treasuries: instruments designed to keep value stable (often targeting $1.00) while passing through short-term dollar yields.

Two strategies have become reference points:

- BlackRock’s BUIDL: a tokenized fund share designed for qualified investors, distributed on public blockchains through a regulated tokenization platform, with daily dividends and 24/7 peer-to-peer transfer features.

- Ondo Finance’s RWA suite (notably OUSG and USDY): a set of tokenized structures offering on-chain access to short-term U.S. Treasury exposure and dollar-denominated yield, with product designs that emphasize compliance, institutional asset handling, and (in some cases) stablecoin-based mint/redemption workflows.

As of December 29, 2025, RWA.xyz reports $8.86B in total tokenized Treasuries value across 62 products and 59,023 holders (its dashboard snapshot), illustrating that tokenized Treasuries have become a measurable on-chain category rather than a niche experiment.

Key Takeaways

- Tokenized Treasuries are best understood as on-chain cash management: stable value targets paired with short-duration U.S. dollar yield.

- BUIDL emphasizes an institutional fund-share model with daily dividend payouts and always-on transfers, rather than “payments-first” behavior.

- Ondo’s OUSG positions Treasury exposure via tokenized fund structures, while USDY is described as a tokenized note secured by short-term Treasuries and bank deposits for non-U.S. investors.

- When comparing products, the practical decision hinges on: (1) who can hold it, (2) how liquidity/redemption works, (3) what “yield delivery” looks like (dividends vs accumulating redemption value), and (4) the combined smart-contract + off-chain operational risk stack.

- Tokenized Treasuries and stablecoins often work together in a simple pattern: stablecoin for settlement + tokenized Treasuries for yield/cash management, then stablecoin again when funds are needed for payments.

What RWA Tokenization Means in a Stablecoin Context

RWA Tokenization vs Stablecoins

A fiat-backed stablecoin is usually designed to track a unit of currency (typically $1) and prioritize spendability, fast settlement, and wide acceptance.

By contrast, tokenized RWAs represent a broader range of financial exposures, often securities-like exposures, where transfer rules, investor eligibility, and redemption mechanics can be more restrictive.

Tokenized Treasuries sit near the stablecoin boundary because they often aim for stable value plus yield, so users treat them as a cash management sleeve rather than a volatile investment.

This is why they show up in conversations about stablecoin rails: stablecoins move value; tokenized Treasuries try to park value productively.

Tokenized Treasuries as the First Scaled RWA Category

Public dashboards tracking on-chain RWAs show tokenized Treasuries as a distinct, growing segment.

For example, RWA.xyz’s Treasury dashboard snapshot on 12/29/2025 reports $8.86B total tokenized Treasuries value and 59,023 holders.

Separately, a CoinGecko RWA report covering Jan 2024 to April 2025 describes tokenized Treasuries reaching $5.5B by April 2025 after growing by $4.7B over that period, and states that BlackRock/Securitize’s BUIDL had roughly 45% share at that time.

Because these metrics are time-sensitive, treat them as “as-of” snapshots, not permanent truths.

The Core Building Blocks of Tokenized Treasury Products

Tokenized Treasury products can look simple on the surface (“a $1 token that earns yield”), but the mechanics are a layered stack:

Legal Structure and Asset Ownership

At minimum, you need clarity on:

- What the token represents (fund share, note, beneficial interest, etc.)

- Who holds the underlying assets

- What claims token holders have (redemption rights, distributions, priority in a default)

In Ondo’s SEC submission (December 4, 2025), Ondo describes OUSG as a tokenized private fund involving on-chain institutional government securities and money market funds, and USDY as a tokenized note secured by short-term U.S. Treasuries and bank deposits for non-U.S. investors.

Custody, Administration, and Transparency

Tokenized funds and notes depend heavily on off-chain institutions:

- Custodians holding T-bills or fund assets

- Administrators and agents tracking ownership, redemptions, and distributions

- Reporting/attestation practices that provide evidence of reserves and operations

This is a key educational point: blockchain tokens do not eliminate the off-chain trust stack when the underlying asset is off-chain. They change how claims move, not necessarily where assets live.

NAV, Pricing, and Yield Mechanics

For Treasury exposures, yield typically originates from:

- Interest on Treasury bills (and in some structures, repos or cash equivalents)

- Money market fund yields (if the tokenized vehicle holds MMFs)

But how that yield reaches the token holder can differ:

- Dividend distribution model: yield paid out regularly (e.g., daily dividends)

- Accumulating model: token’s redemption value rises over time

For BUIDL, public communications highlight daily dividend payouts.

For USDY, Ondo’s documentation describes yield delivered as increasing redemption value (an accumulating token approach).

Mint/Redemption and Liquidity Design

Two different “liquidity” concepts matter:

- Primary liquidity: can you mint or redeem with the issuer/administrator, and under what rules?

- Secondary liquidity: can you sell the token to someone else, and is there meaningful market depth?

A token can have 24/7 transferability while still having redemption constraints. This distinction is frequently misunderstood and is one of the biggest causes of “it says on-chain confirmed, why can’t I cash out instantly?” confusion.

Ondo Finance Strategy in Tokenized Treasuries

Ondo’s approach is best understood as building a compliant bridge between institutional-grade fixed income exposures and on-chain transfer rails.

1. OUSG: Treasury Exposure via Tokenized Fund Structure

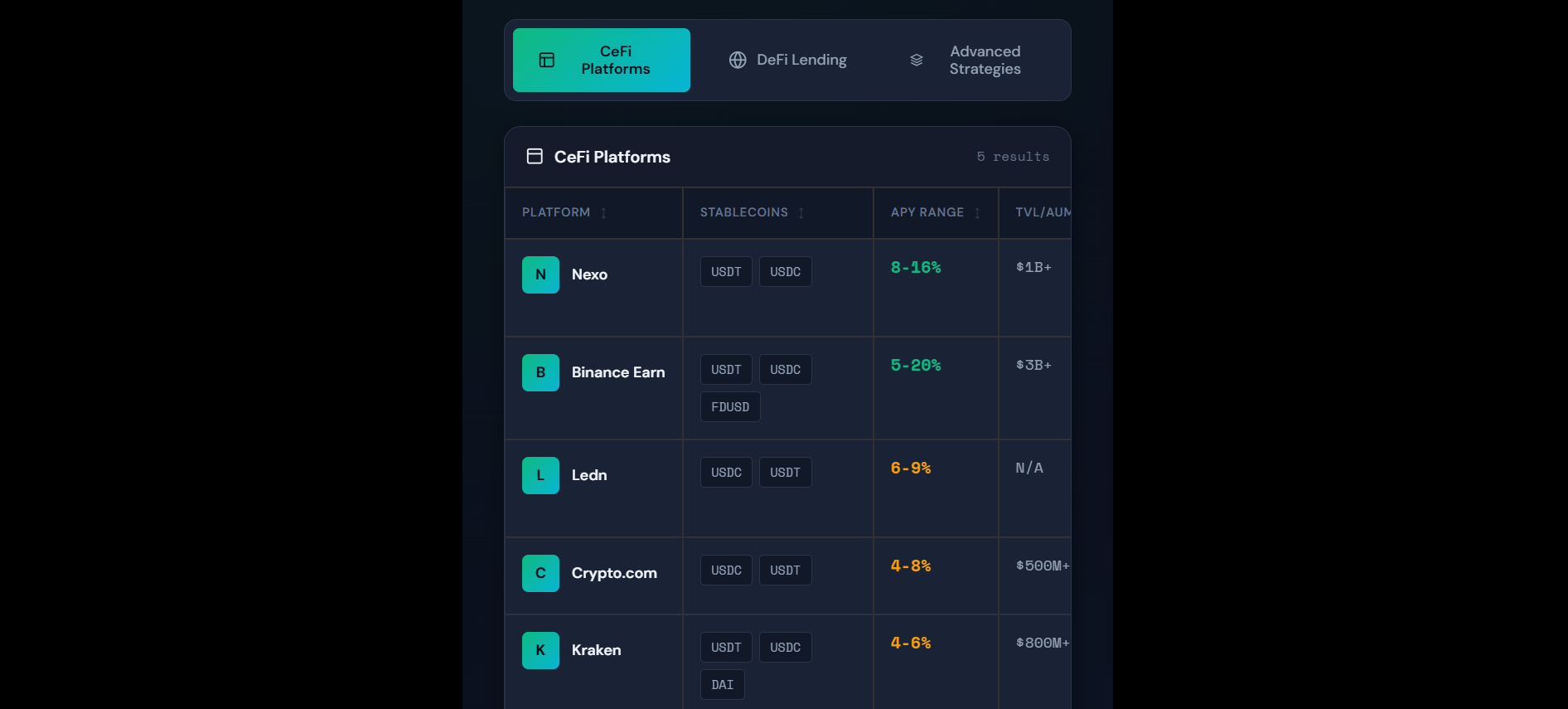

RWA.xyz lists OUSG as Ondo Short-Term US Government Bond Fund, with an inception date of 01/26/2023, eligible investors: U.S. Qualified Purchaser, and management fees of 0.15%.

RWA.xyz’s asset screener also describes OUSG as investing through institutional vehicles, and notes a portfolio that includes exposure via BlackRock’s BUIDL and other asset managers’ vehicles, with a reported AUM of ~$829M at the time of that snapshot.

Separately, Ondo’s SEC submission frames OUSG as a tokenized private fund tied to institutional government securities and money market funds, including BlackRock’s BUIDL.

Educational implication: OUSG is not “a Treasury bill on-chain.” It is a token that represents a structured exposure pathway, where the underlying instruments may include MMFs and other institutional cash equivalents.

2. USDY: “Stablecoin-Like” Yield Token for Non-U.S. Investors

RWA.xyz describes USDY as a tokenized note for non-U.S. individuals and institutions, secured by short-term U.S. Treasuries and bank demand deposits, with assets held by a collateral agent to safeguard holders.

Ondo’s documentation further states:

- USDY is a tokenized note secured by short-term Treasuries and bank demand deposits

- Yield is reflected via increasing redemption value

- USDY uses an upgradeable proxy pattern and includes blocklist restrictions (meaning transfers can be constrained by compliance controls)

This matters operationally: USDY may look and behave “stablecoin-adjacent” at the UI level, but it includes securities-style compliance controls and a different yield mechanism than a pure reserve-backed stablecoin.

Ondo’s “System” View: Interoperability and Stablecoin Conversion

In its SEC submission, Ondo also references infrastructure components such as a token bridge and a mechanism for redeeming tokenized Treasuries into stablecoins (described as converting to stablecoins like USDC), reflecting the broader strategy: connect tokenized yield products to stablecoin settlement rails.

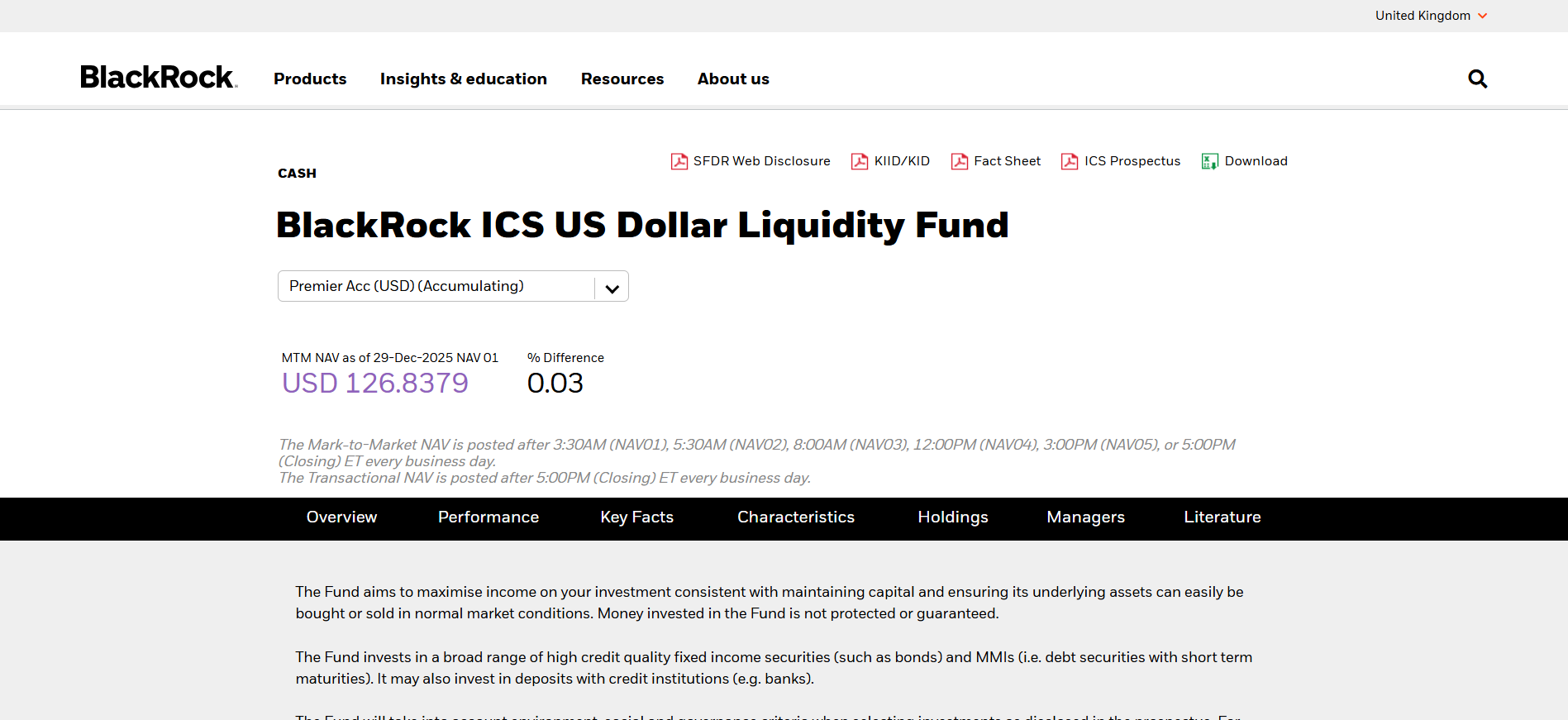

BlackRock BUIDL Strategy and What It Signals

BUIDL is frequently cited as a milestone because it combines:

- A large, mainstream asset manager

- Regulated distribution via a tokenization platform

- Public blockchain issuance and multi-chain expansion

- Operational features that match institutional expectations

What BUIDL Is Designed to Do

A March 13, 2025 Securitize release states that BUIDL surpassed $1B in AUM, that it launched in March 2024, and that it offers qualified investors on-chain U.S. dollar yields with daily dividend payouts and near real-time 24/7/365 peer-to-peer transfers.

An Avalanche ecosystem post adds product-level detail: it states that the fund aims to invest 100% of its assets in cash, U.S. Treasury bills, and repurchase agreements, targets a stable value of $1 per token, and pays daily accrued dividends to investors’ wallets.

Together, these points describe BUIDL as a tokenized cash management fund share with always-on transfer rails, not a payment stablecoin.

Growth and Position in Tokenized Treasuries

RWA.xyz’s BUIDL asset page lists (at time of capture):

- Inception date: 03/20/2024

- Eligible investors: U.S. Qualified Purchaser

- Management fees: 0.20%–0.50%

- Total value: approximately $1.73B

Given that tokenized Treasury totals are in the single-digit billions as of late 2025, BUIDL’s size is directionally meaningful for market structure discussions.

Multi-Chain Expansion and Collateral Utility

BUIDL’s expansion has been described through multiple channels:

- Debut of a new BUIDL share class on Solana and reiteration of daily dividends and 24/7 transfers.

- BUIDL live on BNB Chain and accepted as collateral on Binance.

- Similar “accepted as collateral” framing in broader PR distribution.

Educational implication:

When tokenized Treasuries become eligible collateral venues, the product shifts from “cash management” into “market plumbing”, supporting margining and secured financing flows.

Ondo vs BUIDL: A Practical Comparison Framework

| Dimension | Ondo OUSG | Ondo USDY | BlackRock BUIDL |

|---|---|---|---|

| Investor orientation | U.S. Qualified Purchaser (per listing) | Non-U.S. individuals/institutions (per listing) | U.S. Qualified Purchaser (per listing) |

| Structure (high level) | Tokenized private fund exposure to institutional cash equivalents (Ondo SEC framing) | Tokenized note secured by Treasuries + bank demand deposits | Tokenized fund share investing in cash/T-bills/repos with daily dividends |

| Yield delivery | “Accumulates” (per listing) | Redemption value increases | Daily dividend payouts |

| Fee signals | 0.15% management fee (listing) | Not stated in the cited snippets | 0.20%–0.50% management fee range (listing) |

| Key operational nuance | Fund exposure via institutional vehicles | Upgradeable contract + compliance controls (blocklist) | Multi-chain distribution + collateral narratives |

If you are evaluating stablecoin adjacency, USDY’s user experience may feel closer to stablecoins (because it aims at a stable value plus yield), but its controls and structure still differ from a typical reserve-backed payment stablecoin.

How Tokenized Treasuries Interact With Stablecoins in Practice

Stablecoins for Settlement, Tokenized Treasuries for Yield

A common, operationally clean model is:

- Use stablecoins to move dollars 24/7

- Convert a portion into tokenized Treasuries for cash management/yield

- Convert back to stablecoins when liquidity is needed for payments

Ondo’s SEC submission explicitly references mechanisms for redemption into stablecoins, and BUIDL communications emphasize always-on transfer and institutional treasury utility, both consistent with the settlement + cash management pattern.

Scale Context: Stablecoins vs Tokenized Treasuries

Stablecoins are orders of magnitude larger than tokenized Treasuries in both market value and usage.

- RWA.xyz’s global overview snapshot shows Total Stablecoin Value: $298.51B and 214.82M stablecoin holders (at time of capture).

- A World Economic Forum article (March 2025) cites $27.6T in stablecoin transfer volume in 2024, exceeding combined Visa and Mastercard volume for that year.

This is why tokenized Treasuries are typically framed as a treasury/cash management sleeve inside a stablecoin-led payment and settlement world.

Risks, Constraints, and Failure Modes to Understand

This section is intentionally practical: the biggest mistakes in RWA tokenization analysis are usually not misreading yield, but misunderstanding liquidity, legal claims, and control surfaces.

Liquidity Risk: 24/7 Transfer Does Not Equal 24/7 Redemption

A token can be transferable at all times while redemption into cash/stablecoins happens only through defined processes (and may require eligibility, settlement windows, or administrator steps).

This is the most common stablecoin mental model error applied to tokenized securities.

Compliance and Transfer Controls

Ondo’s documentation states USDY includes blocklist constraints and uses an upgradeable proxy structure. These features are normal in regulated tokenized asset designs but materially different from how many users assume ERC-20 tokens behave.

Smart Contract Risk and Administrative Controls

Upgradeable contracts can be necessary for bug fixes and regulatory requirements, but they introduce governance and key-management risk. If you are integrating these assets into DeFi systems, upgradeability and administrative permissions are first-order considerations (especially for collateral use).

Counterparty and Operational Risk

Even with on-chain transfer, the underlying assets (Treasuries, repos, deposits, MMFs) are held and administered off-chain.

Therefore, the risk stack includes:

- Custodian/bank dependencies

- Administrator processes

- Legal enforceability of token-holder claims

- Disclosures, reporting, and governance discipline

BUIDL’s institutional posture is often highlighted as reducing certain counterparty concerns through established TradFi infrastructure, but the category still remains a hybrid of on-chain and off-chain dependencies.

Due Diligence Checklist for Buyers and Integrators

Below is a framework you can apply without relying on assumptions.

Token-Level Checks

- Contract permissions: upgradeability, admin roles, transfer restrictions

- Blacklist/freeze controls (if present)

- Issuance and redemption pathways (what is available to your entity class)

Off-Chain Structure Checks

- What the token legally represents (share, note, beneficial interest)

- Who holds the underlying assets and under what custody and administrative arrangement

- Distribution terms: dividends vs accumulating NAV/redemption value

Integration Checks

- How the asset behaves in DeFi contexts (if used): transfer constraints, redemption cycles, oracle/NAV timing

- Operational handling: accounting, treasury policies, and internal controls (especially for corporate treasuries)

Market Outlook Signals to Watch in 2026

These are not predictions; they are observable signal categories grounded in what has already happened in the market:

- Multi-chain distribution of regulated tokenized funds (BUIDL expansions illustrate this operational direction).

- Collateral acceptance at major venues and within structured on-chain credit systems (public collateral announcements illustrate this direction).

- Growth of tokenized Treasuries as a measurable on-chain category (RWA.xyz Treasury totals).

- Ongoing institutionalization of RWA tokenization, with market reporting increasingly treating tokenized Treasuries as a distinct segment.

Conclusion

Tokenized Treasuries have become the clearest, data-trackable example of RWA tokenization intersecting with stablecoin rails.

BUIDL demonstrates an institutional fund-share strategy with daily dividends and always-on transfers, while Ondo’s OUSG and USDY illustrate how different legal and operational structures can deliver Treasury-linked yield to different investor bases.

As you evaluate these products, focus less on marketing labels and more on the decision-critical mechanics: who can hold the asset, how redemption works, how yield is delivered, and what the combined smart-contract plus off-chain operational risk stack looks like.

Read Next:

- Best Stablecoins for Cross-Border Payments in 2025

- The Role of Stablecoins in Monetary Policy Transmission

- The Neobank Transition Report

FAQs:

1. What is real-world asset tokenization in the context of stablecoins?

RWA tokenization is the creation of blockchain tokens that represent claims on off-chain financial assets such as Treasury bills, money market funds, repos, or bank deposits. In stablecoin workflows, tokenized Treasuries are commonly used as a cash management layer: funds move in stablecoins, then sit in tokenized Treasury exposure to earn yield, then move back into stablecoins when liquidity is needed.

2. Are tokenized Treasuries the same as yield-bearing stablecoins?

Not necessarily. Tokenized Treasuries typically represent fund shares or notes linked to Treasury exposure and often come with eligibility rules, transfer restrictions, and defined redemption processes. A yield-bearing stablecoin is usually framed as a payment token that also passes through yield, but many tokenized Treasury products are closer to regulated cash management instruments than payment money.

3. How does BUIDL differ from a typical stablecoin?

BUIDL is positioned as a tokenized fund share designed for qualified investors, targeting a stable $1 price and paying dividends, rather than a general-purpose payment token used broadly for commerce. Its value proposition is institutional-grade Treasury yield exposure on-chain, with always-on transfers, not merchant payment ubiquity.

4. How do Ondo’s OUSG and USDY differ from each other?

OUSG is framed as tokenized private fund exposure to institutional government securities and money market funds and is oriented toward U.S. qualified purchasers. USDY is described as a tokenized note secured by short-term Treasuries and bank demand deposits and is oriented toward non-U.S. investors, with yield reflected via increasing redemption value.

5. What does “daily dividends” mean for tokenized Treasury products?

Daily dividends typically mean the product accrues yield each day and distributes it as periodic payouts to token holders’ wallets. This differs from accumulating structures where the token’s redemption value increases over time and the holder realizes yield primarily at redemption.

6. What does “increasing redemption value” mean in practice?

It means the token is designed so that, over time, the amount you can redeem per token increases to reflect accrued yield. Instead of receiving separate dividend transfers, the token’s redemption rate rises, so yield is realized when you redeem or sell at a price that reflects that increased value.

7. Does 24/7 transferability mean I can cash out 24/7?

No. 24/7 transferability means you can typically transfer the token to another eligible wallet at any time. Cashing out depends on redemption rules, settlement cycles, eligibility checks, and administrator processes. Many products allow continuous transfers but have structured redemption workflows.

8. What is the biggest risk people misunderstand with tokenized Treasuries?

Liquidity and redemption. Users often apply a stablecoin mental model and assume instant cash-out at all times. In tokenized Treasury products, redemption access can be gated by investor eligibility, operational windows, and administrator procedures, even if the token itself can move instantly on-chain.

9. What are the main risk categories for tokenized Treasury products?

Four risk buckets matter most: (1) off-chain counterparty and operational risk (custody, administration, banking), (2) legal and compliance risk (what the token represents and who can hold it), (3) liquidity risk (primary redemption vs secondary market depth), and (4) smart contract and administrative control risk (upgradeability, permissions, restrictions).

10. Why do some tokenized RWA tokens include blocklists or transfer restrictions?

Because many RWA tokens are designed to operate within regulated frameworks that require KYC/AML checks, sanctions compliance, and controlled transfers. Transfer restrictions can limit who can receive tokens, which can affect liquidity, integrations, and “open DeFi” composability.

11. Can tokenized Treasuries be used as DeFi collateral?

They can be, but suitability depends on transfer restrictions, redemption mechanics, market liquidity, and how the protocol handles pricing and liquidations. Collateral use requires strong assumptions about who can acquire the asset during liquidation events and whether transfers can occur without compliance conflicts.

12. What should a treasury team check before allocating to tokenized Treasuries?

Focus on: investor eligibility, redemption terms, settlement expectations, fee stack, custody and administration setup, reporting transparency, smart contract permissions, transfer restrictions, and contingency planning for stress scenarios (redemption delays and liquidity gaps).

13. How should I decide between stablecoins and tokenized Treasuries for a business?

Use stablecoins for frequent payments, settlement, and operational liquidity. Use tokenized Treasuries for treasury cash management when you can tolerate redemption workflows and eligibility constraints in exchange for short-duration dollar yield exposure.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}