Table of Contents

When a family abroad sends money home for Diwali, Onam, or Durga Puja, the transfer carries a deadline and an emotional weight that a routine payment never does, and a slow or failed app lets them down at the worst possible moment.

That pressure plays out across the largest remittance market in the world: India took in $135.4 billion in inflows in FY25 and has held the top global spot for more than 25 years running, according to the Economic Survey 2025-26, with the United States now the single biggest source and millions of senders moving money home every week for family, education, savings, and celebration.

This guide breaks down what it actually takes to build and win a remittance app in the India corridor: why the competition is so fierce, how stablecoin infrastructure changes the economics, and the India-specific decisions that won't transfer from any other market.

Key Takeaways

- India is the world's largest remittance market, exceeding $135 billion yearly.

- Winning the corridor requires speed, transparency, and trust, not lower rates.

- Stablecoin infrastructure makes payments cheaper, more reliable, and fully traceable end to end.

Why the India Remittance Corridor Is the Hardest to Win

The India remittance corridor is hard to win because it is already mature, crowded, and emotionally loaded in ways a pricing comparison never captures.

1. It's already a crowded, mature market

The first mistake builders make is assuming there's an empty seat at the table. There rarely is.

"People underestimate how crowded and mature the India corridor already is," says Edul Patel, co-founder and CEO of Saber Money. "A sender in New Jersey isn't choosing between two remittance apps. They're choosing between a bank wire, three remittance apps, and whatever their cousin used last week. To win, new-age remittance companies can't just match the incumbents on rate. They have to be faster, clearer, and more trustworthy at the exact moment someone is sending money they worked hard for."

2. Festivals make timing and reliability emotional

That moment of sending is where India diverges from other corridors. A large share of these transfers is tied directly to the calendar of home, and that emotional context reshapes the entire product.

"Remittance to India is rarely just a transaction. A lot of it is also tied to festivals, and that's where treating India as one market falls apart," Patel explains. "A Telugu family is sending money home for Ugadi and Sankranti, a Punjabi family for Baisakhi and Diwali, a Bengali family for Durga Puja, a Malayali family for Onam. Each peak lands on a different week, for a different reason, with a different emotional weight. That emotional context changes everything about the product. People forgive a slow or unreliable app far less when the money is meant to reach home in time for a celebration. Reliability and timing aren't features here, they're the whole relationship."

3. The NRE account is the corridor's quiet engine

Beneath the emotional layer sits a structural one that outsiders consistently miss: a large portion of what looks like remittance is actually long-term saving, routed to a specific type of bank account called the Non-Resident External (NRE) account.

"The NRE account is the quiet engine of this corridor," says Patel. "It lets Indians abroad move money home tax-efficiently, so a lot of what looks like 'remittance' is actually long-term saving and investment. If you're building for India and you don't understand how NRE flows, banking partners, and regulator’s expectations fit together, you'll build something that works in a demo but breaks in the real world."

The takeaway is clarifying: India isn't a rate war you can win with a thinner margin. It's a trust-and-timing market built on top of a regulated banking layer, and you have to be credible on all three at once.

How to Build a Competitive Remittance App: Cost, Reliability, and Traceability

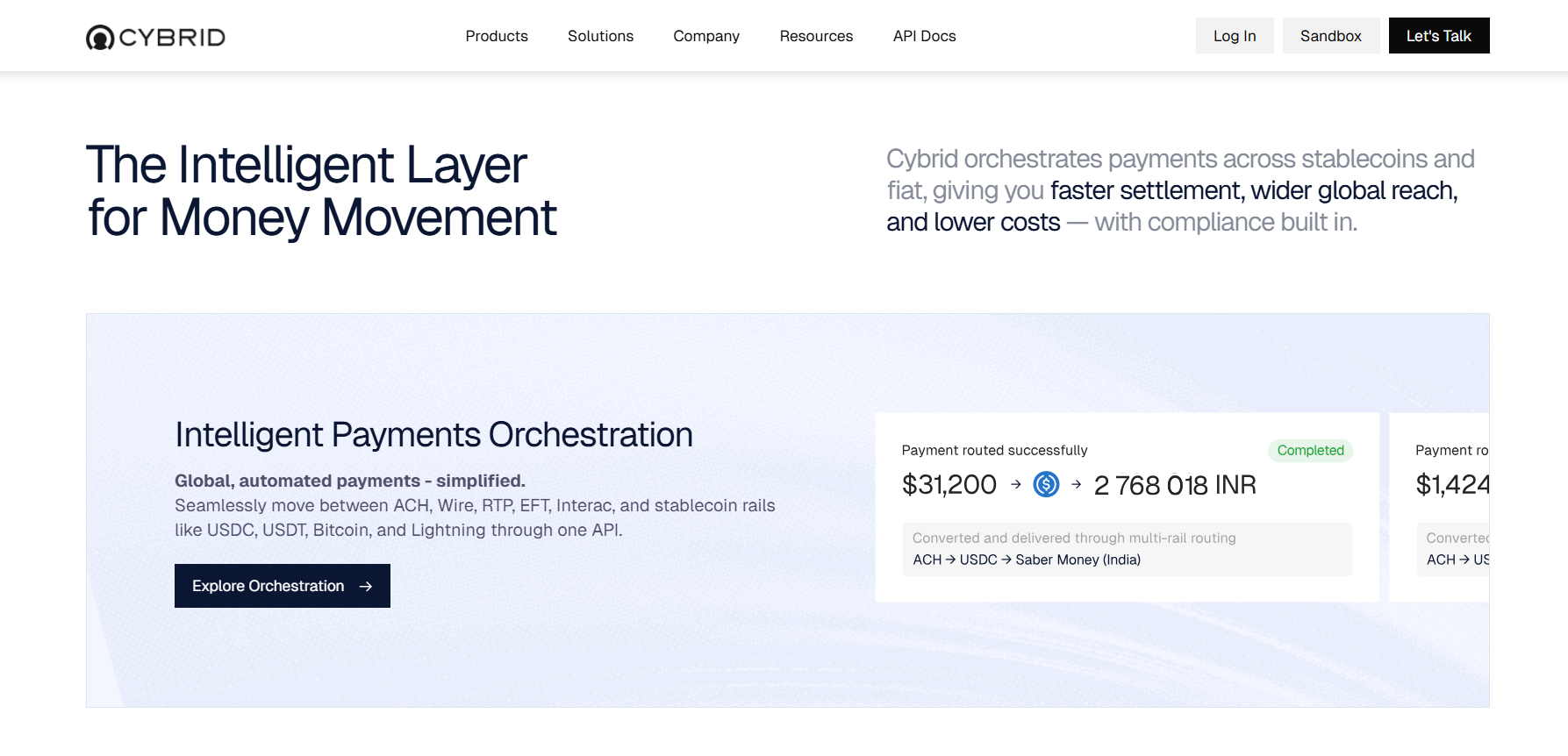

You build a competitive remittance app by winning on three things at once: cost, reliability, and traceability, rather than trading one against another. Stablecoin infrastructure is what makes that possible.

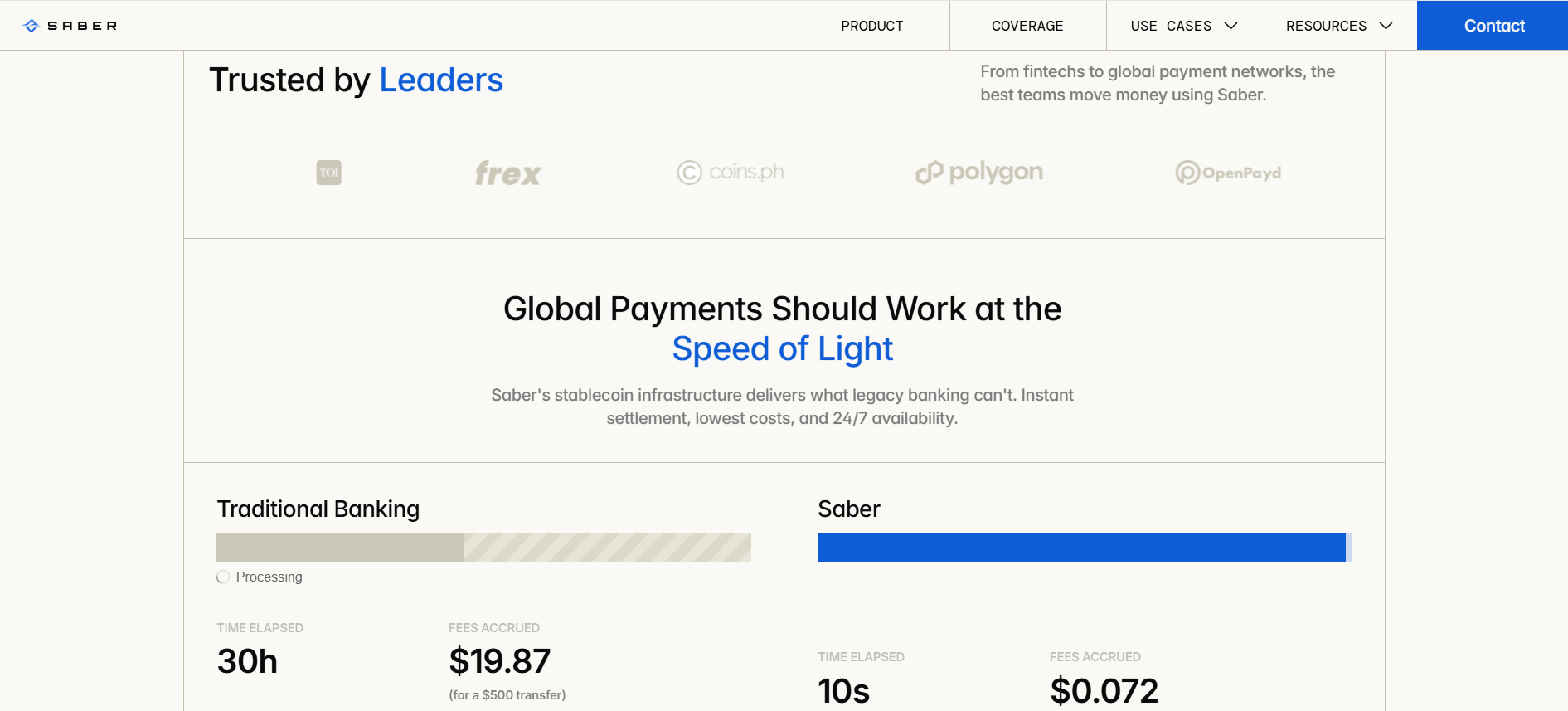

Settling on stablecoin rails strips out correspondent-banking hops, cutting both the fees and the delays that come with them. The contrast with a traditional bank wire is stark:

| Dimension | Traditional Bank Wire | Stablecoin Rails |

|---|---|---|

| Settlement speed | 1–5 business days | Minutes — on-chain confirmation in roughly 2 minutes |

| Cost | High; stacked correspondent-bank fees | Up to ~90% lower; intermediary hops removed |

| Traceability | Opaque — little visibility into when, or if, funds arrive | Fully traceable end to end, in real time |

| FX certainty | Rate often settles days later | Rate locked at the time of the transaction |

| Festival-week reliability | Variable; delays common at peak | Consistent, visible delivery |

Traceability is the most underrated advantage

The most underrated advantage is traceability, and it maps almost perfectly onto the emotional stakes that define the corridor.

"A key piece of the puzzle for all remittance is traceability (did the funds actually arrive and when?)" says Avinash Chidambaram, co-founder and CEO of Cybrid. "That's where stablecoins truly shine, because they are fully traceable from end to end. When you send a wire or traditional bank transfer, there is no transparency on when, or even if, money will arrive. With an app built on stablecoin infrastructure, your user can be on the phone with their grandma and trace the payment in real time. Or they can check in the app that their NRE remittance landed in their account."

In practice, that confirmation can land in roughly two minutes, an on-chain receipt the sender sees the moment the money arrives, rather than a multi-day wait with no signal. That is the difference between a sender anxiously refreshing and a sender who can watch the money move during a festival week, exactly the moment when a failed or opaque transfer does the most reputational damage.

Managing the corridor's regulatory complexity

The harder part is everything sitting behind that smooth experience. The India corridor carries real operational weight: tax and regulatory reporting, NRE and NRO account handling, regulator’s expectations, and banking-partner relationships.

A builder either masters all of it or partners with someone who has.

"Building a successful remittance app in the Indian corridor means managing a lot of complexity, or partnering with a vendor who manages it for you," says Chidambaram. "Cybrid's partnership with Saber Money means everything end to end, tax and regulatory reporting, NRE accounts, NRO accounts, and more, is handled in a single API. We brought together all the pieces to make it easy for remittance app builders to focus on what matters: customer acquisition and user experience."

That division of labor is the practical answer to the demo that breaks in the real world. The regulated plumbing runs underneath; the builder spends energy on the parts users actually feel.

How Stablecoin Remittance to India Works

Stablecoin remittance to India works by converting the sender's money into a dollar-backed stablecoin, settling it on-chain, and paying out in rupees to the recipient's account through an Authorised Dealer (AD) bank, replacing the slow correspondent-banking chain with a single, traceable rail.

In practice, the flow looks like this:

- On-ramp: The sender funds the transfer in their local currency (for example, USD via ACH, wire, or card), which is converted into a regulated stablecoin such as USDC or USDT.

- On-chain settlement: The stablecoin moves on-chain in minutes, with the FX rate locked at the time of the transaction rather than days later.

- Compliance and reporting: KYC, AML, and the corridor's tax and regulatory reporting run in the background, in line with the regulator’s expectations.

- INR payout: The funds are processed to the beneficiary's bank account through an authorised dealer bank partner which covers payouts to Savings, NRO and NRE accounts.

- Real-time confirmation: Both sides can trace the payment end to end and confirm the exact moment funds land.

This is the mechanism that lets a single API replace what used to require stitching together banks, custody, compliance, and payout partners.

How to Build for India Specifically

You build for India specifically by treating it as many markets, not one. The strategies that work in other corridors do not automatically apply here, and the teams that scale are the ones that internalize that early.

Treat India as many markets, not one

"The biggest mistake people make is treating India as one large country. It isn't," says Saurabh Kumar, Business Head at Saber Money. "It's 28 states, each with its own language, culture, and money habits. And that diversity travels with the diaspora. A Telugu family in Dallas, a Punjabi family in Toronto, a Malayali family in New York send money home for different reasons, to different banks, at different times of year. The next generation of remittance apps won't win by serving 'Indians abroad' as one block. They'll win by understanding these cohorts precisely and building language- and state-specific experiences for them. That's still a largely untapped strategy."

Know your community and serve it on its own terms

Cybrid frames the same lesson as a discipline: pick your community and serve it on its own terms.

"India is an incredibly diverse country with multiple different languages, heritages, and communities," says Chidambaram. "Make sure you know your community’s focus and work to serve them in ways that work for them, not just for you."

Build for both senders and receivers

And the experience cannot begin at the destination. The corridor is two-sided, and the sender's feeling matters as much as the receiver's outcome.

"When you build for the Indian corridor, build for both the senders and the receivers," Chidambaram adds. "It's not just about what will happen once the money lands in India, it's the feeling someone has using your app to send money in the first place."

That through-line connects every section here: the India corridor rewards builders who understand it as a set of precise, emotionally specific cohorts, and who can deliver cost, reliability, and traceability to each of them without drowning in regulatory complexity.

How to Choose Your Remittance Infrastructure Partner

Choosing a remittance infrastructure partner for India comes down to how much of the corridor's complexity they remove for you.

The right partner should cover:

- Settlement on fast, low-cost, traceable rails so payments are cheap, reliable, and visible end to end.

- Native NRE and NRO account flows handled directly, not bolted on.

- Tax and regulatory reporting in line with the regulator’s expectations built into the product, not left to you.

- Banking relationships that keep money moving during peak weeks, the festival periods when reliability matters most.

The clearest signal of a strong partner is consolidation: the more of that stack you can access through a single integration, the more of your own time goes to acquisition, user experience, and serving your specific community, and the less goes to stitching together vendors.

For builders entering the India corridor, the practical question isn't "who has the cheapest rail?" but "who lets me launch a compliant, reliable, India-ready product without becoming a remittance company first?"

About the Partners

About Cybrid

Cybrid is a global payments infrastructure platform that connects fiat rails and stablecoin settlement through a single, API-first integration.

Founded in 2022 and headquartered in New Jersey and Toronto, the company lets fintechs, remittance providers, B2B payment platforms, and banks launch compliant domestic and cross-border payments with onboarding, compliance, custody, and liquidity built in.

Cybrid's orchestration layer moves money across rails like ACH, wire, RTP, and stablecoins such as USDC and USDT, with real-time settlement and end-to-end traceability designed to cut cost and complexity out of global money movement.

Led by co-founder and CEO Avinash Chidambaram, a payments veteran with more than 25 years building fintech products, Cybrid focuses on abstracting away the hard parts of payments so its customers can build on simple APIs.

About Saber Money

Saber Money is a stablecoin-powered remittance infrastructure platform built for the Asian corridor. It provides licensed, compliant rails, including native NRE and NRO account handling in India, FX, and regulatory reporting, so fintechs and remittance operators can launch cross-border payments to India without building a remittance company from scratch.

By packaging the corridor's regulatory and banking complexity into developer-friendly infrastructure, Saber lets teams that already have users' trust extend global transfers to them quickly and at scale.

The company is led by co-founder and CEO Edul Patel, with Saurabh Kumar serving as Business Head, and works with fintechs and remittance brands serving the global Indian diaspora.

Conclusion

The India corridor is the biggest prize in remittance and one of the hardest to win. Rate alone won't do it. What wins is a product that's fast and transparent at the emotional moments that matter, credible on the NRE and regulatory layer beneath it, and built specifically for the community it serves.

That is the logic behind the Cybrid and Saber Money partnership: stablecoin-powered, fully traceable settlement on top of a single API that handles NRE and NRO accounts, tax and regulatory reporting, and the banking relationships the corridor demands, so builders can focus on the senders, the receivers, and the trust between them.

If you're building for the India corridor, the fastest path forward is to see the integration in action: explore how Cybrid and Saber Money handle settlement, NRE and NRO accounts, and compliance through a single API, and talk to the team about launching your product.

Read Next:

FAQs:

1. What is the India remittance corridor?

The India remittance corridor is the flow of money sent home to India by its global diaspora, and it is the largest remittance market in the world, with inflows reaching $135.4 billion in FY25. The United States is now the single largest source country, followed by the Gulf, the UK, Canada, and Singapore, and a significant share of the money funds family support, education, and long-term savings rather than one-off transfers.

2. Why is the India remittance corridor so competitive?

The India remittance corridor is so competitive because it is already mature and crowded, with senders choosing among bank wires, multiple remittance apps, and informal recommendations for every transfer. Winning it requires being faster, clearer, and more trustworthy than incumbents — especially during festival periods, when timing and reliability carry far more weight than a marginally better exchange rate.

3. How do stablecoins improve remittance apps?

Stablecoins improve remittance apps by making payments cheaper, faster, and fully traceable from end to end. Because stablecoin transfers settle without the correspondent-banking hops of traditional wires, they reduce both cost and delay, and they let a sender confirm in real time exactly when funds arrive — including when an NRE remittance lands in the recipient's account.

4. What is an NRE account and why does it matter for remittance?

An NRE (Non-Resident External) account is an Indian bank account that lets Indians living abroad move money home in a tax-efficient, repatriable way, which is why much of what looks like remittance is actually long-term saving and investment. It matters for builders because a product that doesn't account for how NRE flows, banking partners, and regulatory expectations fit together may demo well but break in real-world use.

5. How do you build a remittance app for India?

You build a remittance app for India by winning on cost, reliability, and traceability while treating India as many distinct markets rather than one. That means using infrastructure that settles on fast, traceable rails, handles NRE and NRO accounts and regulatory reporting natively, and lets you tailor language- and state-specific experiences for the specific diaspora community you serve — for both the senders and the receivers.

Sponsored by Cybrid and Saber Money

{kind=link}