Table of Contents

Stablecoins in 2026 compete on more than peg charts. The market has matured into institutional questions:

- What backs the token?

- How minting and redemption are controlled?

- How supply expands and contracts under stress?

- Whether transparency and custody standards are credible enough for large allocators and regulated counterparties?

frxUSD sits directly in that institutional problem space. It is positioned as a fiat-redeemable, fully collateralized stablecoin where each token is backed 1:1 by permitted cash-equivalent reserves, including tokenized U.S. Treasury fund instruments.

Rather than presenting itself as a purely DeFi-native stablecoin, frxUSD is engineered around an explicit reserve and issuance model plus a cross-chain access layer that aims to make minting, redemption, and usage practical at scale.

Key Takeaways

- frxUSD is designed as a fully collateralized, fiat-redeemable stablecoin backed 1:1 by cash-equivalent reserves, including tokenized U.S. Treasury funds.

- Issuance relies on enshrined custodians that mint and burn frxUSD 1:1 against provable reserves they custody, under governance delegation.

- frxUSD is designed for multi-chain availability through an access layer that supports cross-chain minting and redemption flows rather than relying on a single bridged representation.

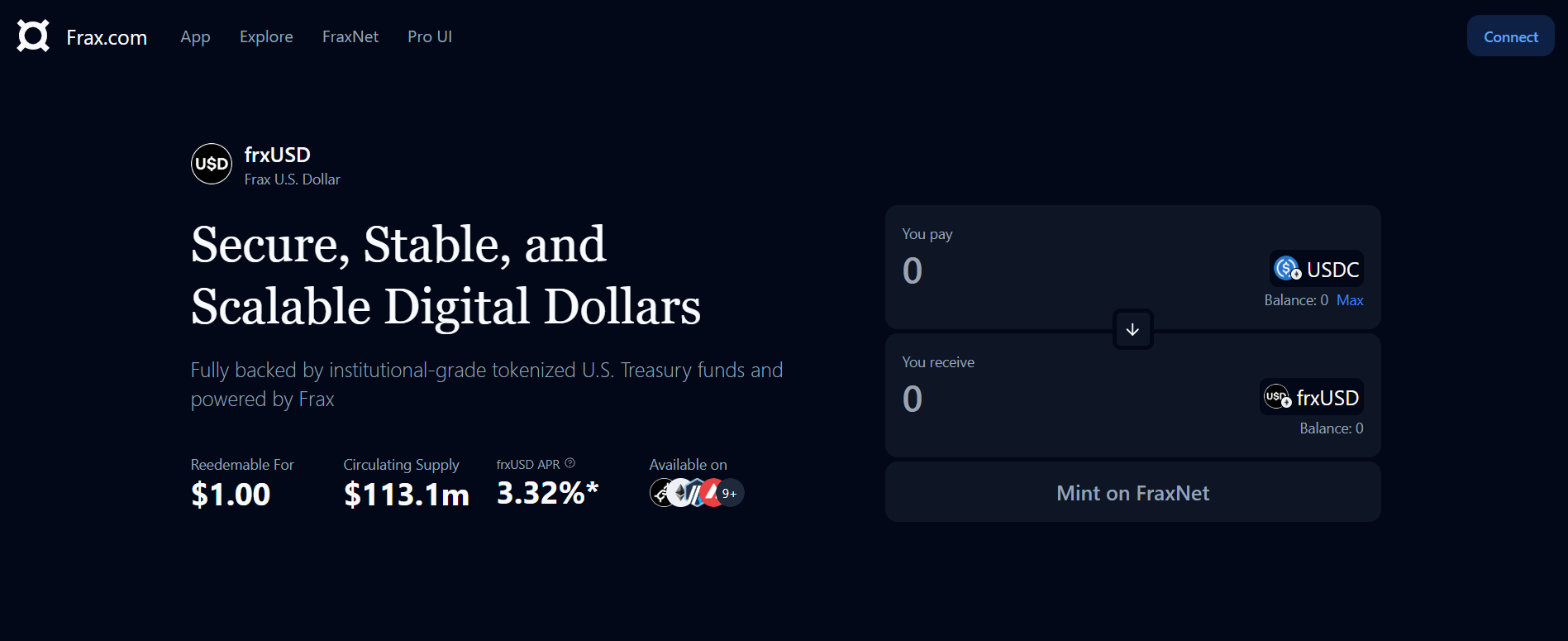

- Recent market snapshots place frxUSD around ~$113M in market cap and ~113M in circulating supply, with price trading close to $1.

What Is frxUSD

frxUSD (Frax U.S. Dollar) is a USD stablecoin in the Frax Finance ecosystem designed to function like a digital cash-equivalent instrument that can move across public blockchains while keeping reserve quality anchored in short-duration U.S. Treasury exposures.

The product intent is clear:

- Stable settlement asset: hold and transfer a dollar-denominated token that targets $1.00

- Institutional-grade backing: reserves are designed to be cash-equivalent and high quality

- Operationally legible issuance: minting and redemption are tied to approved entities and approved reserve assets, rather than opaque discretion

What fully collateralized means here

Fully collateralized in the frxUSD architecture is not a marketing label, it is a reserve claim.

The model is built around permitted cash-equivalent reserves, including tokenized Treasury fund instruments such as BlackRock’s BUIDL, Superstate’s USTB, and WisdomTree’s WTGXX.

Two practical implications follow:

- Reserve design becomes the product: The quality, liquidity, reporting cadence, and legal structure of reserve instruments are core to frxUSD’s credibility.

- Operational constraints matter: Tokenized fund rails can include settlement timing, eligibility constraints, and custody requirements.

Those details influence redemption throughput and how tight the peg stays during stress.

The enshrined custodian model is the control plane

frxUSD uses an “enshrined custodian” model. Conceptually, an enshrined custodian is a real-world entity approved under governance delegation that can:

- mint frxUSD 1:1 against $1 of provable reserves it custody-holds

- burn frxUSD 1:1 to release $1 of reserves

This is the system’s control plane. It determines:

- who can expand or contract supply

- which reserve assets qualify

- where counterparty risk sits (custody + reserve issuer rails)

- how governance can cap or restrict specific pathways

Where frxUSD sits in the Frax stablecoin ecosystem

frxUSD is best understood as a Treasury-backed stablecoin stack rather than a single token.

It is the combination of:

- a base stablecoin with reserve-backed solvency claims

- multi-chain access and canonical distribution design

- an optional yield wrapper (sfrxUSD) that targets benchmark-rate returns

Market Data And Observed Scale

Recent market snapshots by CoinMarketCap place frxUSD roughly around:

- ~$113M market cap

- ~113M circulating supply

- Price trading near $1.00

This scale implies two things:

- frxUSD is large enough to matter in on-chain liquidity engineering and collateral discussions, but it is not in the dominant stablecoin tier.

- the next scaling challenges are less about if frxUSD can stay near $1 and more about redemption throughput, liquidity depth at the peg, reserve diversification, and cross-chain canonicality.

Backing Assets: Tokenized Treasury Rails And Permitted Reserves

The reserve set is explicitly cash-equivalent and governance-permitted

The frxUSD reserve approach centers on cash-equivalent instruments, with tokenized Treasury funds playing a major role.

That choice positions frxUSD closer to tokenized cash management infrastructure than to DeFi-native CDP stablecoins.

A professional diligence view focuses on:

- reserve composition and concentration

- liquidity and redemption characteristics of each reserve instrument

- custody model and operational resilience

- transparency cadence and reconciliation between supply and reserves

Why tokenized Treasury funds change the stablecoin backing game

Tokenized Treasury funds can behave like:

- cash-equivalent base layer: short duration, low volatility, rate-linked

- yield source: bill yields / repo-style returns can feed yield products

- compliance primitive: institutional custody and reporting can support regulated use cases

In stablecoin terms, this can shift backing from a black box into something closer to tokenized money-market plumbing, if the operational rails hold up under stress.

Reserve concentration is a first-order monitoring variable

Early stablecoins often have concentrated backing across a few reserve sources.

Concentration is not automatically bad, but it is a measurable risk variable: the fewer reserve rails you rely on, the more you care about their operational continuity and legal constraints.

Minting And Redemption Mechanics

1. Baseline mint/redeem flow

In a simplified user path, frxUSD minting and redemption follows this pattern:

- approve the mint contract

- deposit a supported asset to mint frxUSD at 1:1 value

- hold frxUSD as a stable settlement asset or route into yield

- redeem frxUSD back into supported assets

The analytical point is that frxUSD frames mint/redeem as an explicit product surface, not a hidden institutional backdoor.

2. Cross-chain minting and redemption

frxUSD’s cross-chain design is expressed through FraxNet and a canonical distribution philosophy: reduce fragmentation by enabling native flows rather than proliferating wrapped variants.

A typical cross-chain concept is:

- deposit assets on a source chain

- mint frxUSD on the destination chain

- redeem by returning frxUSD and settling into a redemption asset on a supported settlement path

FraxNet references established messaging and settlement standards such as LayerZero and Circle's CCTP as part of its interoperability approach.

Why canonicality is a first-order feature

Many multi-chain stablecoins fail at being one asset everywhere. They become a family of bridged representations with:

- uneven liquidity per chain

- higher smart contract surface area

- ambiguous canonical version during stress

Cross-Chain Infrastructure: FraxZero And The Hub Model

FraxZero is described as a hub-and-spoke style cross-chain infrastructure intended to route liquidity and operations through Fraxtal as a hub.

From a risk and performance standpoint, the important idea is:

- consolidating liquidity routing and security assumptions can reduce the complexity of having separate bridge systems per chain

- it also concentrates operational importance in the hub, which must remain resilient

For analysis, you monitor:

- hub security and uptime assumptions

- how quickly hub issues would propagate to mint/redeem and cross-chain availability

- whether canonicality holds across all supported networks during market shocks

sfrxUSD: The Yield-Bearing Layer On Top Of frxUSD

Token design and accounting

sfrxUSD is the yield-bearing companion to frxUSD.

It is designed as an ERC4626-style vault/share token:

- users stake frxUSD and receive sfrxUSD

- yield accrues over time

- redemption back into frxUSD occurs at an increasing exchange rate rather than via rebasing balances

This structure is integration-friendly: ERC4626-style share tokens tend to be easier to account for in DeFi than rebasing tokens.

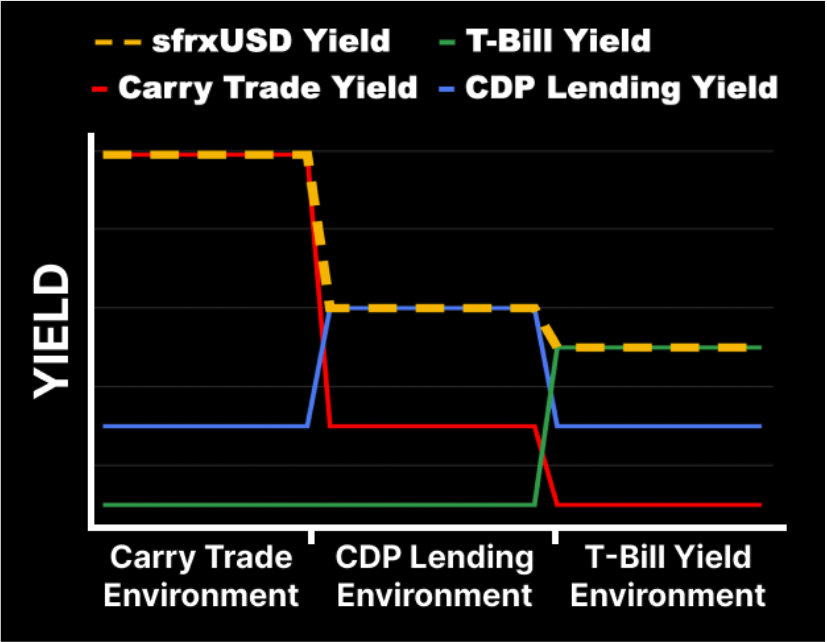

Benchmark Yield Strategy (BYS): policy engine design

sfrxUSD is positioned as a benchmark-yield stablecoin that can rotate among governance-approved strategy categories such as:

- carry-trade style strategies

- DeFi deployments through AMO-style allocation

- IORB / T-bill-linked yield approaches

The non-marketing significance is that yield is framed as a governed policy engine rather than a single venue dependency.

Governance expansions and caps

A concrete example is strategy expansion via governance proposals that add new venues, pools, or integrations under explicit caps.

These proposals function like risk policy updates and are a key part of how you evaluate the product’s evolution: what is added, what is capped, and why.

Partnerships And Institutional Rails

This section focuses on roles, because stablecoin infrastructure scales through role coverage: fund issuer, tokenization partner, custodian, liquidity partner, and distribution partner.

1. Tokenized treasury and tokenization rails

The frxUSD reserve narrative includes tokenized Treasury fund instruments, with tokenization infrastructure and fund issuers as key components.

Securitize is a notable example of tokenization rails used in the tokenized fund ecosystem around these instruments.

2. Institutional custody and distribution

Institutional scale requires credible custody and distribution.

Partners in this category include:

- BitGo (qualified custody positioning in public announcements)

- Crypto.com (institutional custody and liquidity service positioning)

- ATW Partners (deployment and institutional adoption program framing)

The analytical reason these partnerships matter is that they expand the real-world pathways through which frxUSD can be held, moved, and deployed beyond purely retail DeFi usage.

Independent Risk Perspectives And Integration Readiness

Stablecoins become real infrastructure when external risk teams review them and large protocols debate onboarding.

Governance and risk discussions in major DeFi ecosystems (including Aave contexts) are useful signals because they focus on:

- reserve quality and transparency

- redemption credibility and operational risk

- integration risk (oracle, liquidity, liquidation behavior)

- governance and change-management risk

These discussions do not prove safety, but they indicate the product is being evaluated with institutional-style controls.

Risk Analysis: What To Monitor As frxUSD Scales

1. Reserve and counterparty risk

Even with cash-equivalent reserves, a reserve-backed stablecoin depends on:

- reserve token issuers and their legal/operational constraints

- custodian resilience and settlement operations

- governance processes that can change caps and reserve eligibility

What you monitor:

- reserve concentration by instrument and by custodian

- reconciliation between circulating supply and reported reserves

- reporting cadence and change logs

2. Redemption credibility and throughput

Stablecoins break when redemption is constrained under stress. This is a throughput problem as much as it is a solvency problem.

What you monitor:

- whether redemption windows remain open across major rails

- where settlement delays occur (on-chain vs off-chain steps)

- whether DEX liquidity remains deep enough to prevent persistent discounts when redemptions spike

3. Liquidity and market structure risk

Volume is not liquidity quality. For a stablecoin, liquidity quality is:

- depth at peg

- slippage at meaningful size

- persistence of liquidity during volatility

- diversification of liquidity venues and chains

4. Strategy-layer risk (sfrxUSD)

sfrxUSD’s benchmark strategy design can include DeFi and carry-trade exposures alongside Treasury-linked approaches. That expands yield opportunity but increases complexity.

What you monitor:

- strategy category exposure over time

- venue concentration and smart contract risk for DeFi allocations

- governance responsiveness to adverse conditions

Conclusion

frxUSD is a Treasury-backed stablecoin designed for on-chain USD settlement with cash-equivalent reserves, including tokenized U.S. Treasury funds.

It uses a custodian-based mint and redeem model to keep issuance and backing operationally verifiable.

Its cross-chain architecture aims to reduce fragmentation by supporting canonical availability across networks. sfrxUSD adds a governed benchmark-yield layer with strategy rotation and explicit caps.

The key execution risks to monitor are reserve concentration, redemption throughput, and liquidity depth under stress.

Read Next:

- What Are USDC Gateway Wallets?

- Top Stablecoins and Pegged Assets on Solana in 2026

- Tokenized Money Market Funds: Everything you Need to Know for 2026

FAQs:

1. What is frxUSD?

frxUSD is a USD stablecoin in the Frax ecosystem designed to be fiat-redeemable and fully collateralized, backed 1:1 by permitted cash-equivalent reserves including tokenized U.S. Treasury fund instruments.

2. How does frxUSD maintain a $1 peg?

frxUSD targets a $1 peg through reserve-backed solvency and redemption credibility: supply can expand or contract via approved minting and redemption pathways tied to cash-equivalent reserves, which supports arbitrage around $1.

3. What are enshrined custodians in frxUSD?

Enshrined custodians are governance-approved entities that custody approved reserve assets and can mint and burn frxUSD 1:1 against those reserves, acting as the operational control plane for issuance.

4. How do users mint and redeem frxUSD?

Users mint frxUSD by depositing supported assets at 1:1 value through the minting pathway, and redeem by converting frxUSD back into supported assets through the redemption pathway.

5. What is FraxNet and why does it matter for frxUSD?

FraxNet is a cross-chain access layer designed to support minting and redemption of Frax assets across multiple networks, aiming to reduce fragmentation and improve canonical stablecoin availability across chains.

6. What is FraxZero?

FraxZero is the Frax cross-chain infrastructure design intended to route cross-chain operations through a hub model centered on Fraxtal, supporting canonical transfers and operational consistency across networks.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}