Table of Contents

The answer is yes, but not for the reasons regulators usually cite.

KYC has always been the friction point where crypto ambitions meet regulatory reality.

For stablecoins specifically, the problem has become acute: the populations most likely to benefit from stablecoin payments are exactly the ones the compliance stack was never designed for.

The Regulatory Pressure Is Real

The compliance environment has tightened considerably in the past year.

The GENIUS Act established the first comprehensive federal framework for stablecoin regulation in the United States, mandating heightened KYC obligations and AML/CFT requirements for permitted payment stablecoin issuers.

In parallel, the EU's MiCA framework came into full effect in 2025, requiring proper licensing, 1:1 asset backing, and solid KYC and customer due diligence processes for stablecoin providers.

The compliance spend is following.

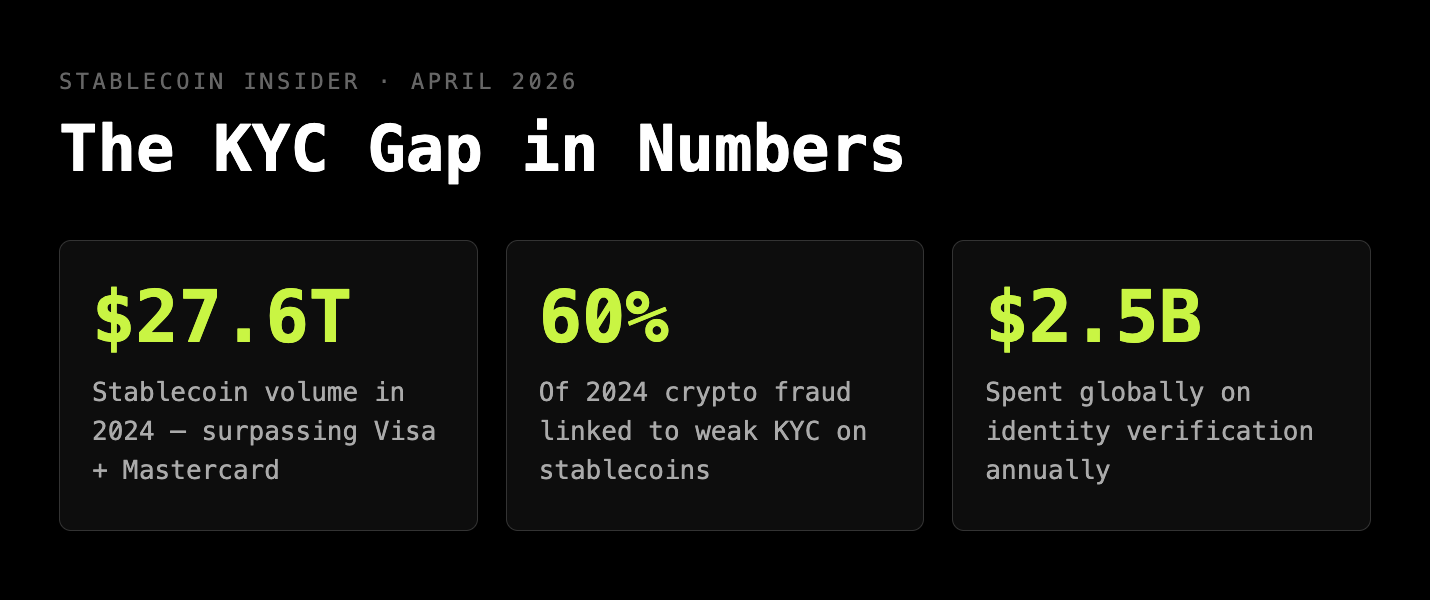

It is estimated that $2.5 billion is spent globally on identity verification services and compliance across the financial services industry, and that figure is growing.

Legacy compliance infrastructure simply can't cut it in a stablecoin environment, where speed is essential and near real-time alerting scenarios are critical.

The risk numbers are used to justify all of it.

In 2024, around 60% of crypto-related fraud was linked to stablecoins, with $12.4 billion in crypto fraud often exploiting weak KYC, per the Chainalysis 2025 Crypto Crime Report.

That's the case for more compliance. Now here's the problem with how it's being applied.

The Infrastructure Mismatch

Stablecoin-linked cards are rapidly emerging but highlight a growing tension between fast-moving crypto innovation and existing regulatory and compliance frameworks. As issuers partner with traditional payment networks, users are encountering repeated identity checks, frozen accounts, and opaque risk decisions.

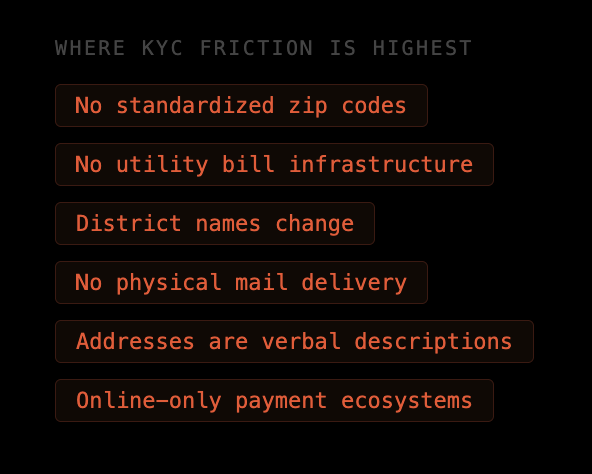

The structural issue runs deeper than product design. Standard KYC in a stablecoin context, as defined by industry guides, requires verification of identities through government-issued documentation, biometric verification, and proof-of-address mechanisms.

→ Proof of address.

That's where the system breaks, not in theory, but in practice, across most of the world where stablecoin adoption is highest.

Vietnam shows crypto as everyday infrastructure for remittances, gaming, and savings, and ranks third in APAC by on-chain transaction volume.

The Philippines ranks 9th worldwide in the Chainalysis 2025 Global Crypto Adoption Index, with analysts estimating roughly 10% of Filipinos, or over 12 million people, engaging with cryptocurrency.

These are not fringe markets. They are the core of global grassroots stablecoin adoption.

And they're precisely the markets where a Western compliance template built around utility bills, zip codes, and mailable correspondence fails completely.

Vietnam doesn't have a standardized address system of the kind that legacy KYC infrastructure assumes. Neither do large swaths of Southeast Asia, Sub-Saharan Africa, and South Asia which are regions that, together, account for the majority of the Chainalysis Global Crypto Adoption Index's top ten.

Vietnam's Level 3 verification (which unlocks unlimited trading) requires address proof, bank account verification, and a source of funds statement.

For a user in Ho Chi Minh City who describes their location by neighborhood and landmark, not by street number and zip code, that requirement is a wall, not a gate.

Hong Kong's stablecoin regime requires full KYC even for unhosted wallets, which reassures regulators and institutions but undermines the frictionless appeal that made stablecoins popular in the first place.

This is not a UX nuisance. It is a structural exclusion of the populations who need these tools most.

The Business Cost

The compliance friction is measurable at the product level.

On-chain assets do not carry the same embedded identity signals as traditional bank deposits. A stablecoin balance may be fully legitimate, but its provenance, how it moved across wallets, through which protocols, and under what conditions can be difficult to assess using conventional risk frameworks.

The result is conservative default behavior from compliance teams: if we can't verify, we decline or freeze.

Without a designated role responsible for real-time triage, institutions are left with a critical blind spot. Users in emerging markets, whose financial profiles simply don't fit the legacy model, bear the cost of that blind spot disproportionately.

The abandonment rates are a silent statistic as they are not publicly reported, but felt acutely by any operator running a stablecoin onboarding flow in Southeast Asia, West Africa, or Latin America.

Where the Solutions Are

The problem isn't enforcement, it's standards. The compliance tooling exists.

What's missing is infrastructure that assumes the world as it actually is, not as it looks from the vantage point of traditional financial centers.

Three directions are gaining traction:

1) Portable identity.

Reusable digital identity solutions allow a person to verify their identity once and reuse that trusted information across multiple services instead of repeating KYC, uploading documents again, or answering the same security questions.

Gartner predicts that by 2026, over 500 million smartphone users will routinely rely on digital identity wallets for verifiable claims.

The EU Digital Identity Wallet is a regulatory forcing function for this in Europe. For emerging markets, the case is even stronger: one verified credential, usable across every platform, removes the need to re-prove identity from scratch to every new service.

2) Zero-knowledge compliance.

Zero-knowledge KYC combines zero-knowledge proofs with selective disclosure, a user can prove they meet specific identity checks like being over 18 without revealing their age, or prove KYC eligibility without revealing personal data.

This approach allows compliance without the data-exposure risks that make repeated KYC particularly problematic in markets with weaker data protection infrastructure.

3) Risk-based tiering.

Not every transaction requires the same level of scrutiny. A risk-based approach tailors KYC intensity to risk levels, light checks for low-value transactions and rigorous verification for high-risk activities.

For remittance-focused stablecoin corridors in Southeast Asia, applying the same enhanced due diligence to a $50 USDT transfer that a bank applies to a corporate wire makes neither compliance nor business sense.

The Stakes

Overseas Filipino Workers remit approximately $38.3 billion yearly, and stablecoins have become a faster, cheaper option for many of them, with platforms like Coins.ph partnering with BCRemit to create stablecoin rails converting overseas transfers into USDC/USDT and cashing out to local pesos within minutes, cutting fees by roughly 80%.

That is the use case stablecoins were made for.

The KYC infrastructure standing between those workers and that access was designed for a different world - one with utility bills, permanent addresses, and reliable postal systems.

The fix is not more verification. It is better standards: portable credentials that travel with the user, risk tiers calibrated to actual transaction risk, and UX built for the world where stablecoin adoption is actually happening.

Regulators are writing the rules now.

The GENIUS Act implementation timeline, MiCA enforcement, and the wave of emerging-market frameworks coming online in 2026 will determine whether KYC becomes the door or the wall.

Related Reports

Partner/Advertise with Stablecoin Insider

Fill out this form to partner and advertise on the only publication, dedicated entirely to the Stablecoin ecosystem.

See you next week,

- The Stablecoin Insider team

{kind=link}