Table of Contents

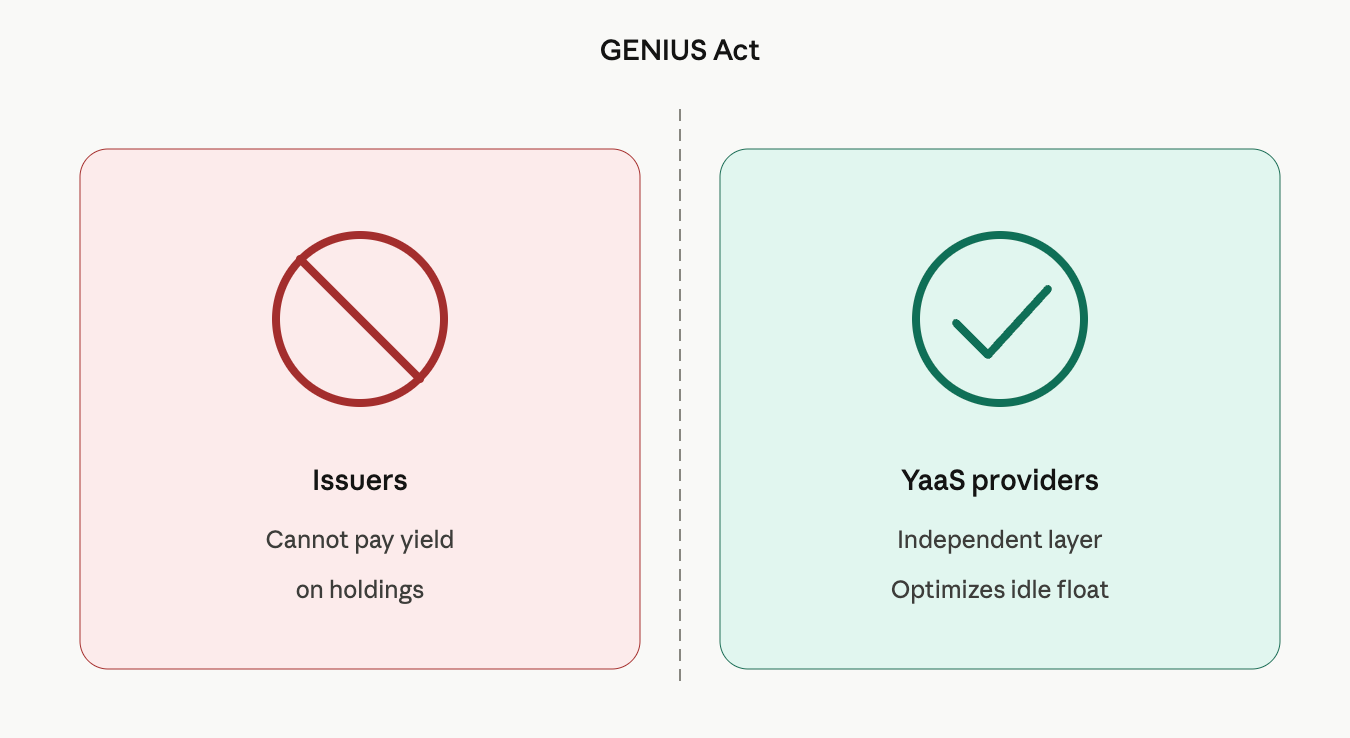

With the GENIUS Act and the OCC’s proposed rulemaking firmly in place, U.S. payment stablecoin issuers face a strict prohibition on paying interest or yield to holders simply for holding, using, or retaining the tokens.

The OCC’s NPRM even includes a rebuttable presumption against certain affiliate and third-party arrangements that could be seen as evasion.

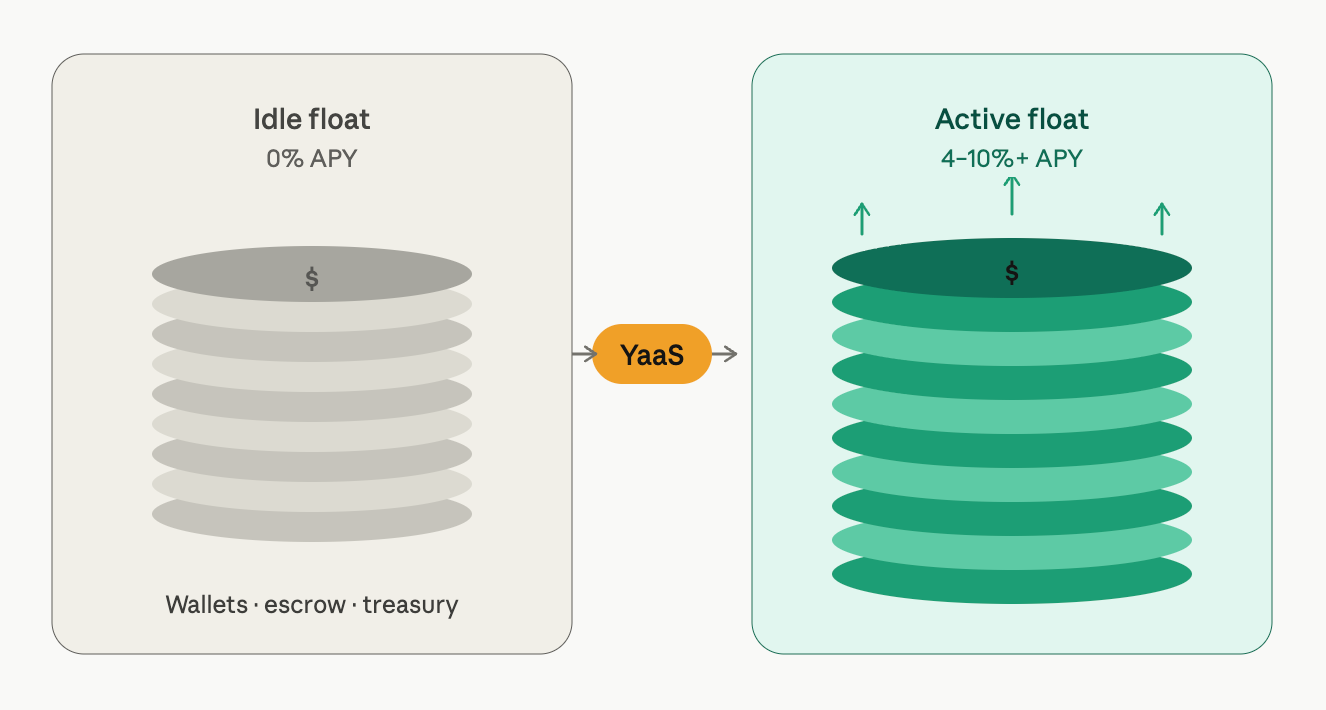

Billions in stablecoin float sitting in wallets, escrows, marketplaces, and treasury buffers now earn nothing by default.

Enter Yield-as-a-Service (YaaS): a specialized middleware layer that lets platforms, wallets, fintechs, and B2B companies automatically optimize idle stablecoins for compliant returns via simple API integrations, without issuers or platforms building complex DeFi operations themselves.

Most Important Points:

- Regulatory shift creates opportunity: GENIUS Act yield bans push value creation downstream to independent infrastructure providers.

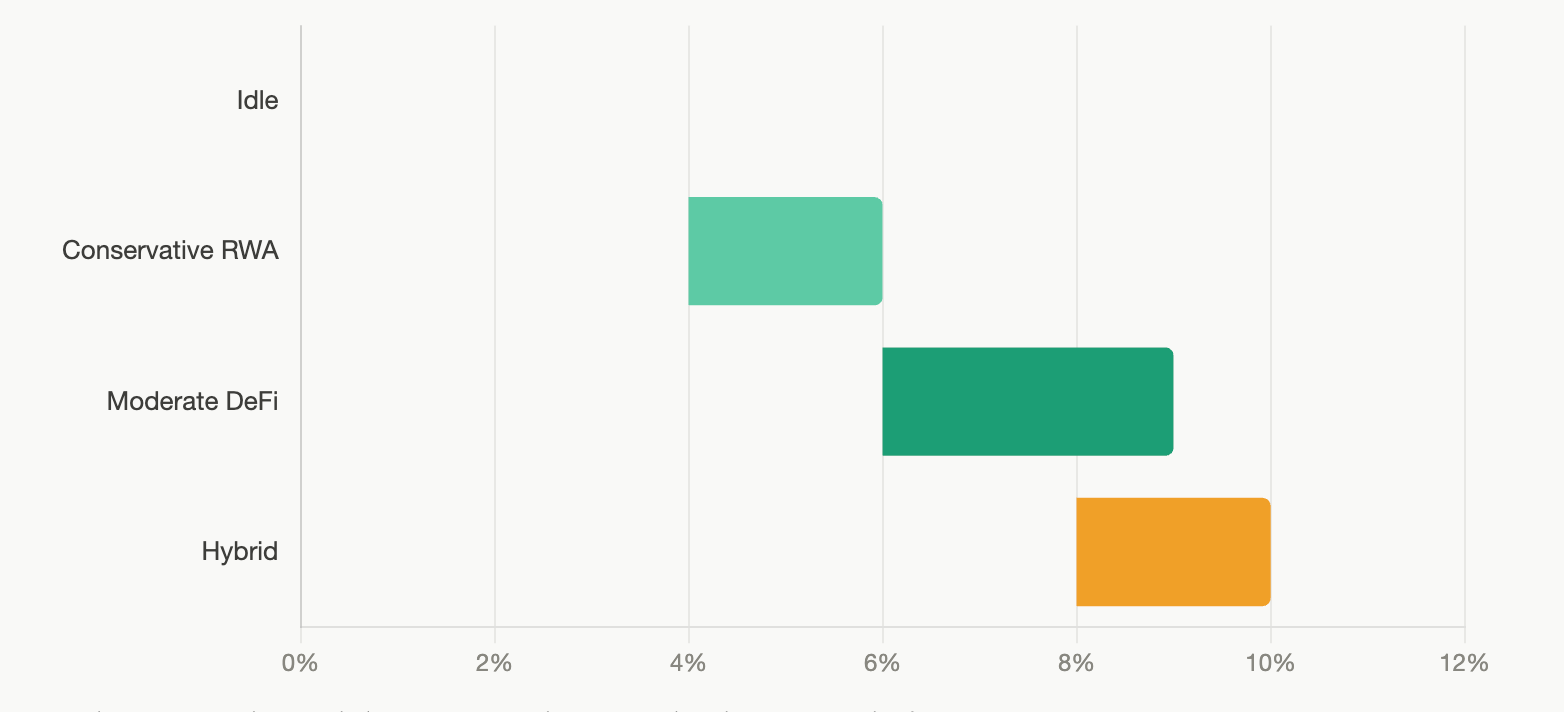

- New revenue rail for platforms: Wallets, exchanges, and B2B fintechs can capture 20-50% shares of optimized yields (typically 4–10%+ APY in 2026, with some hybrid products reaching higher) on otherwise dead capital.

- Early but growing market: Providers like Aegis, OpenTrade, Coinchange, and Stay Liquid offer plug-and-play solutions focused on risk-managed, daily-liquidity strategies across DeFi and RWAs.

The GENIUS Act’s Unintended Gift: Billions in Idle Stablecoins Waiting to Work

The GENIUS Act was designed to make stablecoins safer and more like digital cash, not interest-bearing deposits.

Recent White House analysis (April 8, 2026) suggested the yield ban would have minimal impact on bank lending, while bankers’ groups pushed back, arguing it remains a prudent safeguard against deposit outflows.

The OCC’s detailed rules reinforce the prohibition and target potential workarounds, sharpening the line between permitted payment stablecoins and yield-bearing products.

The result? A massive vacuum.

Stablecoin supply continues climbing toward and potentially past the $1 trillion mark, with significant portions sitting idle in user wallets, escrow accounts, marketplace holds, payroll reserves, and corporate treasuries.

That “dead capital” represents one of the largest untapped opportunities in the post-GENIUS landscape and independent YaaS providers are stepping in to capture it without triggering issuer restrictions.

Decoding YaaS: From API Plug-In to Automatic Alpha

At its core, Yield-as-a-Service abstracts away the complexity of chasing yield in DeFi or tokenized real-world assets (RWAs). Platforms don’t need to manage protocols, rebalance portfolios, or navigate smart-contract risks themselves.

Here’s how it works in practice:

- Seamless integration — Add via clean API or SDK. Users might see an optional “Earn on idle balance” toggle in the app, or the optimization runs silently on backend floats and escrows.

- Dynamic optimization engine — Algorithms scan lending protocols, tokenized Treasuries, structured vaults, and hybrid strategies in real time, applying risk controls and diversification rules.

- Flexible yield distribution — Platforms decide the economics: pass most returns to users for better retention, retain a meaningful share (often 20–50%) as new platform revenue, or structure rewards as credits, discounts, or loyalty incentives that may sit more comfortably within regulatory gray zones.

- Liquidity-first design — Most solutions emphasize daily or near-instant withdrawals, audited protocols, and institutional-grade custody.

Realistic 2026 yields for conservative-to-moderate strategies on major stablecoins (USDC/USDT) currently range from 4-10%+ APY, depending on market conditions and risk appetite.

Some hybrid products, such as OpenTrade’s staking-backed vaults powered by Figment, have delivered higher risk-adjusted returns in testing.

The Players Quietly Building the Post-GENIUS Yield Layer

Several specialized providers have already carved out strong positions in this emerging category, such as...

Aegis turns idle user balances into automatically yielding versions (e.g., YUSD wrappers) that behave like regular stablecoins. Platforms get flexible delegation options to keep a share as revenue or pass it through to users.

OpenTrade delivers institutional-grade, RWA-backed infrastructure that powers white-labeled yield products for fintechs, neobanks, and exchanges (clients include Belo, BuenBit, and others across Latin America and Europe). Its recent funding rounds and partnerships (including with Figment for staking-hybrid products) underscore the momentum.

Coinchange offers multi-manager stablecoin portfolios across CeFi and DeFi venues, with daily pricing, no lockups, and easy API integration for fintech platforms and treasury teams.

Stay Liquid brings AI-driven dynamic optimization across chains and protocols, with a sharp focus on corporate treasury use cases and continuous risk-adjusted rebalancing.

AQRU and similar entrants provide white-label solutions with regulated vehicles and access to crypto/DeFi opportunities.

What sets the stronger players apart is their emphasis on compliance wrappers, asset segregation, and clear operational independence from stablecoin issuers, exactly what helps platforms navigate the OCC’s rebuttable presumption.

Real-World Wins: Who’s Already Cashing In on Idle Float

Early adopters are seeing tangible results.

Wallets and exchanges are activating margin or user balances that previously earned zero. B2B payment platforms are optimizing escrow and supplier payout floats.

Neobanks are embedding YaaS to differentiate from traditional banking, where yields often lag.

A platform sitting on just $10-50 million in average idle escrow or operational balances can now generate meaningful incremental revenue at even modest capture rates.

For consumer-facing apps, the “earn on idle” feature materially improves retention in a market where users increasingly expect their digital dollars to work harder.

The Risk Matrix: What Could Go Wrong (and How Smart Players Are Mitigating It)

No yield strategy is risk-free. Regulatory interpretations around indirect arrangements remain fluid, structures must maintain clear independence from issuers to avoid triggering anti-evasion rules.

Smart-contract and counterparty risks persist in any DeFi or hybrid component. Yields are inherently variable, and operational burdens around tax reporting, AML monitoring, and custody choices are real.

Forward-thinking teams are starting small: conservative RWA-heavy strategies first, single-use-case pilots (escrow optimization or user savings vaults), and close collaboration with legal and compliance teams. Diversification, audited protocols, and daily liquidity are becoming table stakes.

2026 and Beyond: Why YaaS Is Poised for Explosive Growth

As final GENIUS rules take shape and jurisdictions like Hong Kong advance their own (sometimes more permissive) frameworks, the separation between pure payment rails and yield generation is solidifying.

Stablecoin volumes keep growing, AI agents are beginning to execute machine-to-machine payments, and tokenized RWAs are expanding the menu of compliant yield sources.

In this environment, competitive advantage increasingly belongs to platforms that quietly turn regulatory constraints into new product value and revenue streams rather than issuers alone fighting over reserve basis points.

The bigger picture?

Yield-as-a-Service is evolving from a niche infrastructure play into a must-have layer in the stablecoin stack. Platforms that integrate it today won’t just capture new revenue, they’ll future-proof their offerings in a world where idle capital is no longer acceptable.

Related Reports

Partner/Advertise with Stablecoin Insider

Fill out this form to partner and advertise on the only publication, dedicated entirely to the Stablecoin ecosystem.

See you next week,

- The Stablecoin Insider team

{kind=link}