Table of Contents

The role of stablecoins in payments, settlement, and cross-border value transfer grew large enough that regulators began locking in enforceable rules instead of relying on informal guidance or fragmented oversight. The focus is consistent across jurisdictions: permissioned issuance, credible reserve coverage, predictable redemption at par, and transparency that can be supervised and enforced.

What follows is a clean breakdown of the stablecoin regulations that were enacted, commenced, or moved into operational effect in the 2025–2026 window, plus the near-term implementation items that matter in practice.

Key Takeaways

- If you issue or distribute stablecoins, assume permissioned issuance: licensing or regulated pathways are now the default in every major 2025–2026 regime.

- Your minimum control set is reserves, redemption, disclosures, and supervision readiness. Build these as ongoing operations, not one-time documents.

- EU MiCA is already in full force. The transitional window for unlicensed operators expires July 1, 2026, operators without authorization must have orderly wind-down plans in place now.

Scope and Method Used (What Counts as Implemented)

To keep this list verifiable, implemented in 2025–2026 here means either:

- Signed into law or enacted as binding legislation during 2025–2026, even if some provisions require follow-on rulemaking, or

- Commenced or entered into force during 2025–2026, meaning the regime became operational and enforceable.

Where a jurisdiction publicly committed to enactment in a defined 2026 window but the regime was not yet in force as of March 23, 2026, it is included with that status stated explicitly.

The EU MiCA regime is included because its stablecoin-specific titles entered application in mid-2024 and the full regime completed rollout on December 30, 2024, making it the earliest and most comprehensive regime in this analysis window. Its transitional deadline of July 1, 2026 makes it directly actionable in 2026.

Why 2025–2026 Became the Stablecoin Law and Enforcement Window

Regulators tightened stablecoin rules as the data increasingly resembled payments infrastructure scale rather than niche crypto usage:

- On-chain transfer volume: widely reported datasets put 2025 stablecoin transaction volumes in the tens of trillions of dollars.

- Supply growth: total stablecoin supply exceeded $200 billion in 2025, with major issuers' reserves now a meaningful input into short-term government debt markets.

- Treasury market linkage: stablecoin reserve management has been repeatedly linked to short-term government debt markets, raising financial stability and supervisory scrutiny.

- The MiCA effect: the EU's full MiCA rollout in December 2024 created a regulatory benchmark that accelerated policymaking in the US, UK, Hong Kong, and South Korea.

This is the backdrop for why laws in this period converged on the same requirements: eligible issuers, high-quality reserves, redemption at par, and direct supervisory powers.

Timeline (2025–2026): What Went Live, What Was Enacted, and What Is Scheduled

| Date | Jurisdiction | Instrument | What Changed (Practical Meaning) |

|---|---|---|---|

| December 30, 2024 | European Union | MiCA full application | Full MiCA rollout across all 27 member states, including stablecoin-specific rules (EMTs and ARTs), mandatory licensing, reserve requirements, and redemption obligations. |

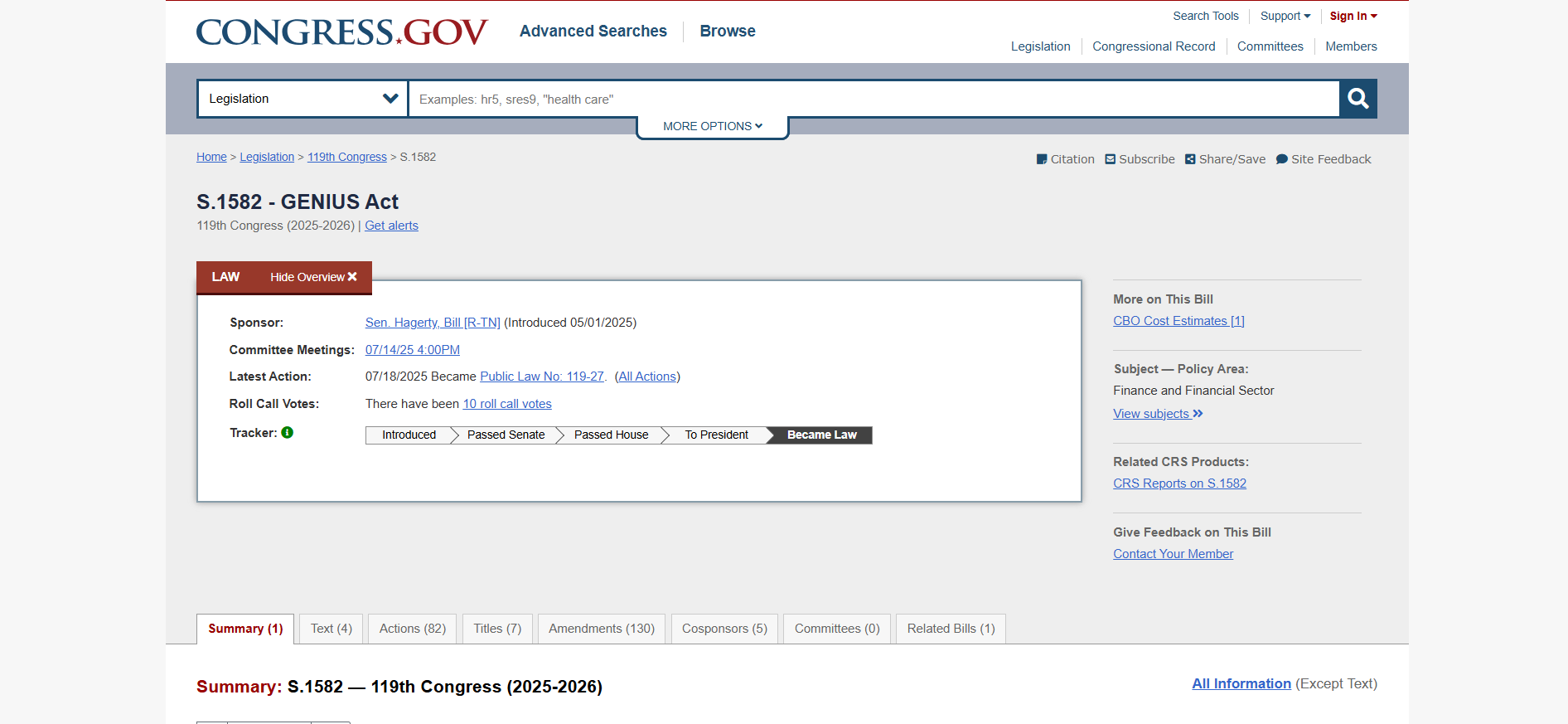

| July 18, 2025 | United States | GENIUS Act of 2025 | Creates a federal framework for payment stablecoins, including issuer permissioning, reserve requirements, disclosures, supervision, and enforcement. Classifies compliant stablecoins as neither securities nor commodities. |

| August 1, 2025 | Hong Kong | Stablecoins Ordinance commencement | Makes issuance of fiat-referenced stablecoins a regulated activity requiring HKMA licensing. Sets reserve, capital, and redemption expectations under supervision. First licenses expected in early 2026. |

| November 2025 | Brazil | Central Bank Resolutions 519–521 | Establishes authorization and operating rules for VASPs and brings stablecoin transactions into the foreign exchange regulatory perimeter. |

| February 2, 2026 | Brazil | Effectiveness date for key provisions | Rules take effect starting February 2, 2026, including FX classification treatment for stablecoin transactions. |

| March 4, 2026 | South Korea | FSC Virtual Asset Committee meeting | FSC held its first 2026 committee meeting, decisively advancing the Digital Asset Basic Act. Democratic Party submitted the bill with a 5 billion KRW minimum capital requirement for stablecoin issuers. Not yet fully enacted as of March 23, 2026. |

| Mid-2026 (target) | Singapore | MAS stablecoin framework legislative effect | MAS finalized its framework in August 2023; full legislative implementation targeting mid-2026. Applies to single-currency stablecoins pegged to SGD or G10 currencies. |

| July 1, 2026 | European Union | MiCA transitional deadline | Transitional period for existing crypto-asset service providers expires. Operators without authorization must have wind-down plans in place before this date. |

| 2026 (implementation focus) | United States | GENIUS implementation phase | By July 2026, regulators are expected to promulgate final implementing regulations. Full enforcement expected ahead of a January 2027 deadline. |

Every Major Stablecoin Regime in 2025–2026

1. European Union: MiCA (Full Application December 30, 2024; Transitional Deadline July 1, 2026)

Status: Stablecoin-specific titles (Titles III and IV) applied from June 30, 2024. Full MiCA entered application across all 27 member states on December 30, 2024.

What it regulates (Scope)

MiCA is the most comprehensive stablecoin regime currently in force globally. It covers two categories of stablecoin: e-money tokens (EMTs), which are fiat-pegged stablecoins like USDC or EURC, and asset-referenced tokens (ARTs), which reference a basket of assets. Both require authorization and meet ongoing compliance obligations.

Issuer permissioning (Who can issue)

EMT issuers must be authorized as credit institutions or electronic money institutions under EU law. ART issuers must obtain a specific MiCA authorization. Algorithmic stablecoins and crypto-collateralized tokens cannot be marketed as stablecoins under MiCA.

Reserve standards (What backing must look like)

EMT issuers must hold reserves in low-risk, highly liquid assets in the same denomination as the peg, fully segregated from operational funds. ART issuers face additional requirements around reserve composition and third-party custody.

Redemption rules (Operational reality)

Redemption at par is mandatory. Issuers must publish clear redemption policies and honor them without unreasonable delay or fee structures that undermine the par value claim.

Disclosure and supervision

MiCA requires white papers, ongoing disclosures, and supervisory access across all member states. The passporting regime means one authorization enables EU-wide operation — but also EU-wide enforcement exposure.

The 2026 transitional deadline (Critical for operators)

National transitional periods vary by member state. Several — including the Netherlands, Poland, Germany, Austria, and Ireland — have already expired or expire by end-2025. All EU-wide transitional provisions expire July 1, 2026. Operators without authorization by that date must implement orderly wind-down plans. ESMA has warned explicitly that non-compliant operators should not assume extensions.

Practical checklist for EU stablecoin operations (MiCA-aligned)

- Confirm whether your token is an EMT or ART, and map your issuer authorization pathway.

- Verify your national transitional period status, several member states' windows have already closed.

- Build white paper, disclosure, and reserve reporting as continuous production.

- If you operate in multiple EU markets, confirm that passporting covers your activities rather than requiring local filings.

2. United States: GENIUS Act of 2025 (Signed July 18, 2025)

Status: Signed into law July 18, 2025. 2026 is an implementation and rulemaking year, with full enforcement expected ahead of a January 2027 deadline.

What it regulates (Scope)

The GENIUS Act establishes a national framework for payment stablecoins — a defined category that excludes algorithmic tokens and crypto-collateralized instruments. It covers who may issue, how reserves must be managed, and how oversight and enforcement apply.

Issuer permissioning (Who can issue)

The framework is permissioned. Permitted issuers include federally chartered banks, credit unions, and non-bank issuers approved by the OCC. Issuers with less than $10 billion in outstanding tokens may elect state-level regulation if that state framework meets federal standards. Foreign issuers may participate only under strict comparability requirements.

Reserve standards (What backing must look like)

A central design goal is 1:1 backing with restricted, high-quality reserve assets. The compliance posture is designed to make reserve claims verifiable through recurring transparency and supervisory access.

Securities and commodities classification (Key structural change)

The GENIUS Act explicitly classifies compliant payment stablecoins as neither securities nor commodities, removing them from SEC and CFTC jurisdiction. This is the clearest regulatory classification of stablecoins in US history and affects how issuers and distributors structure their legal and product operations.

Redemption rules (Operational reality)

The Act is structured around the concept that payment stablecoins must be redeemable for a fixed amount of monetary value under publicly disclosed redemption policies, including clear disclosure of associated fees and procedures.

Disclosure, attestation, and supervisory touchpoints

A core compliance pillar is recurring transparency on reserves and redemption mechanics and the ability of supervisors to examine issuers and enforce compliance. Treat disclosures and attestations as recurring production, with governance sign-offs and audit trails.

AML and illicit finance expectations

The regime ties stablecoin issuance and distribution into financial crime compliance expectations. For operators, this means you must design for KYC, sanctions controls, monitoring, and recordkeeping as operating requirements.

2026 implementation reality (Why timing still matters)

By July 2026, regulators are expected to promulgate final implementing regulations. Full enforcement is expected ahead of a January 2027 deadline. Build compliance operations now rather than waiting for full rulemaking maturity.

Practical checklist if you issue or distribute a USD stablecoin into the US market (GENIUS-aligned)

- Document payment stablecoin classification and your regulatory pathway (federal vs. state, bank vs. non-bank).

- Encode reserve eligibility, liquidity, and concentration limits into treasury controls; map them to disclosure outputs.

- Publish redemption policy with fee logic and operational steps; run redemption stress tests.

- Build attestation and audit production as an operating process.

- Implement AML, sanctions screening, and monitoring as first-class product requirements.

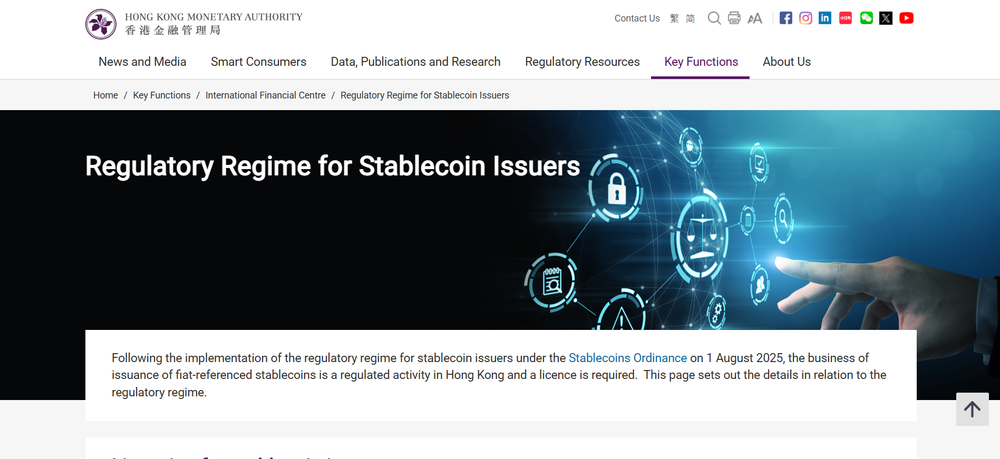

3. Hong Kong: Stablecoins Ordinance Regime (Commenced August 1, 2025)

Status: Commenced August 1, 2025. First HKMA licenses expected in early 2026.

What it regulates (Scope)

Hong Kong's framework regulates fiat-referenced stablecoins as a dedicated regulated activity. After commencement, issuance within scope is inside the regulatory perimeter and requires a license.

Issuer licensing and perimeter (Who needs a license)

The regime is licensing-led. Stablecoin issuance within scope requires HKMA authorization. Any company that issues, markets, or distributes fiat-backed stablecoins to the public in Hong Kong must hold an HKMA license. Algorithmic and crypto-collateralized stablecoins are excluded.

Capital requirements (Entry threshold)

Issuers must hold a minimum paid-up share capital of at least HKD 25 million (approximately $3.2M USD) as a licensing prerequisite. This threshold has already concentrated the applicant pool toward established financial institutions.

Reserve standards and safeguarding expectations

The regime places reserve management, safeguarding, and issuer controls at the center. Reserves must be fully backing outstanding tokens at all times with high-quality, highly liquid assets, held in segregated custody separate from operational funds.

Redemption at par (User protection center of gravity)

Hong Kong's stablecoin regime foregrounds redemption processes, treating reliable redemption as a primary stability and consumer protection requirement.

Operational and governance obligations (Issuer quality)

Licensing is paired with governance and operational expectations designed for ongoing supervision. Expect continuous compliance, periodic reporting, and a posture of audit readiness.

Enforcement (HKMA's role)

HKMA is the licensing and supervisory authority, with the regime structured for continuing oversight and enforcement actions where requirements are breached.

Practical checklist if you want to issue a fiat-referenced stablecoin in Hong Kong

- Confirm scope and perimeter triggers for issuance and distribution.

- Verify capital adequacy against the HKD 25 million minimum threshold before committing to a licensing timeline.

- Prepare a licensing dossier aligned to reserves, redemption operations, governance, and risk controls.

- Implement a redemption operating model that can handle stress and exceptions.

- Treat supervision as continuous: reporting, controls testing, incident response, and audit readiness.

4. Brazil: Cryptoassets Regulatory Framework (Published November 2025; Effective February 2, 2026)

Status: Published November 2025, effective February 2, 2026.

What it regulates (Scope)

Brazil's Central Bank issued Resolutions 519–521 to operationalize the country's virtual asset framework for service providers and to integrate certain cryptoasset activity into the regulated financial perimeter. The rules apply to authorization, operating standards, reporting, and the treatment of certain stablecoin-related flows under foreign exchange concepts.

Issuer and intermediary permissioning (Who is regulated)

Brazil's approach is intermediary-led. It regulates virtual asset service providers through authorization and supervision, including governance, compliance, and control requirements for regulated firms operating in Brazil.

Foreign exchange classification (The core stablecoin impact)

Brazil classifies purchases, sales, or exchanges of fiat-referenced virtual assets — including stablecoins — as foreign exchange operations. This perimeter also captures certain international payment or transfer uses of these assets, including settlement of obligations through common payment methods.

Reserve standards and redemption rules

The reported stablecoin impact is not centered on issuer redemption mechanics in statute-like form. The practical effect for most operators is classification and supervision of stablecoin payment flows when intermediated by in-scope entities. If you need stablecoin issuer reserve specifics under Brazil, treat that as a separate research item tied to implementing rules and supervisory guidance.

Enforcement mechanics (What regulators can do)

The framework extends traditional financial-system expectations to covered entities, including transparency, governance, internal controls, and AML and CFT controls. Authorization and compliance obligations are enforced through Central Bank supervision and reporting requirements.

Practical checklist if you route stablecoins for cross-border payments involving Brazil

- Treat stablecoin payment flows as FX-classified when intermediated through in-scope entities.

- Validate counterparties' authorization status and controls for cross-border stablecoin rails.

- Align KYC, wallet ownership verification expectations, and transaction monitoring to the Brazilian perimeter where applicable.

5. Singapore: MAS Stablecoin Framework (Finalized August 2023; Full Legislative Effect Targeting Mid-2026)

Status: Framework finalized by MAS in August 2023. Full legislative implementation expected mid-2026. Actively used as a compliance planning benchmark now.

What it regulates (Scope)

Singapore's MAS framework applies to single-currency stablecoins (SCS) pegged to the Singapore dollar or G10 currencies and issued in Singapore. It is one of the most detailed stablecoin frameworks globally and is actively shaping issuer design decisions ahead of full legislative effect.

Issuer permissioning (Who can issue)

Issuers must be authorized by MAS. Only compliant tokens meeting all framework requirements may carry the label "MAS-regulated stablecoin" — a label that signals prudential standards equivalent to traditional financial instruments and is increasingly used as a distribution filter by institutional counterparties.

Reserve standards (What backing must look like)

Issuers must maintain 100% reserve backing in low-risk, same-currency assets. Reserves must be segregated from operational funds, independently audited, and publicly attested each month. There is no flexibility on reserve currency matching — a USD-pegged token must hold USD reserves.

Redemption rules (Five-day standard)

Redemption at par is mandatory, with a stated expectation of redemption within five business days of a legitimate request. This makes Singapore's redemption SLA the most specific of any major jurisdiction, and provides a concrete benchmark for operational design.

Capital requirements

Issuers must meet a minimum base capital of SGD 1 million or 50% of annual operating expenses, whichever is higher.

Practical checklist for Singapore stablecoin operations (MAS-aligned)

- Confirm whether your token is in scope (SGD or G10 peg, issued in Singapore).

- Build monthly reserve attestation and independent audit into your operations ahead of full legislative effect.

- Set your redemption operating SLA at five business days or better.

- If you want to use the "MAS-regulated stablecoin" label, map your full compliance posture against MAS requirements before applying.

6. South Korea: Digital Asset Basic Act (Advanced March 2026; Not Yet Fully Enacted)

Status: The FSC held a decisive committee meeting on March 4, 2026 advancing the Digital Asset Basic Act. The Democratic Party submitted the bill with a 5 billion KRW (~$3.5M) minimum capital requirement for stablecoin issuers. As of March 23, 2026, the law is not yet fully enacted. The FSC and Bank of Korea dispute over who can issue KRW stablecoins remains a complicating factor but has not stopped legislative progress.

What it regulates (Scope)

South Korea's Digital Asset Basic Act is presented as the country's first comprehensive digital asset framework, including stablecoin issuance rules, a cross-border transaction framework, and investor protection measures that go beyond the existing Virtual Asset User Protection Act (Phase 1).

Issuer permissioning and licensing (Who can issue)

The bill requires issuer authorization with capital requirements as a prerequisite. A minimum of 5 billion KRW (~$3.5M) has been set as the stablecoin issuer capital floor, mirroring existing electronic money business rules under the Electronic Financial Transactions Act. The unresolved dispute is whether only bank-led consortia (with at least 51% bank ownership, as the Bank of Korea prefers) or a broader set of institutions including fintechs (as the FSC prefers) may issue KRW stablecoins.

Reserve standards (What backing must look like)

The draft requires reserve assets at least equal to 100% of issued tokens, with some proposals requiring over-collateralization. Reserves must be held at banks or approved custodians and segregated from the issuer's balance sheet to limit contagion risk.

Redemption rights (User protection baseline)

The framework emphasizes guaranteed user redemption rights. Operationally, this means issuers must honor redemptions at par with clear terms, documented procedures, and verifiable reserve coverage. The bill also introduces no-fault liability, making operators responsible for user losses from hacking, system failures, or fraud regardless of proven negligence.

Foreign stablecoin treatment

Foreign-issued stablecoins face additional requirements, including local branch or subsidiary requirements for legal use in South Korea. This would require issuers such as Circle (USDC) to establish a local presence.

Cross-border stablecoin transaction rules

The bill explicitly calls out development of rules for cross-border transactions involving stablecoins, directly relevant to payments, trade settlement, and remittance use cases.

Enforcement posture (What to expect)

Because the Digital Asset Basic Act is still moving through finalization, enforcement specifics should be treated as pending until the full legislative text and implementing rules are published. The direction is confirmed: permissioned issuance, full reserves, enforceable redemption rights, and no-fault operator liability.

Practical checklist if you intend to distribute or rely on KRW stablecoins in 2026

- Track FSC announcements closely — the March 4, 2026 committee meeting signals active finalization, not further delay.

- Prepare treasury controls to evidence 100% or greater reserve coverage and segregation.

- Design redemption operations and disclosures to satisfy redemption rights requirements.

- Monitor the FSC vs. Bank of Korea issuer eligibility dispute — its resolution will define who can enter the market.

- Foreign stablecoin issuers should assess local presence requirements ahead of the law's finalization.

Side-by-Side: Issuer Rules, Reserves, Redemption, Enforcement

| Dimension | United States (GENIUS Act) | EU (MiCA) | Hong Kong (Stablecoins Ordinance) | Singapore (MAS Framework) | Brazil (Res. 519–521) | South Korea (Digital Asset Basic Act) |

|---|---|---|---|---|---|---|

| Primary control | Federal payment stablecoin framework | EU-wide licensing for EMTs and ARTs | Licensing regime for fiat-referenced stablecoin issuance | MAS authorization for single-currency stablecoins | VASP authorization plus FX perimeter integration | Planned comprehensive digital asset framework |

| Permissioning | Banks, credit unions, OCC-approved non-banks; state option under $10B | Authorized credit institutions or EMIs for EMTs; MiCA authorization for ARTs | HKMA license required for in-scope issuance | MAS authorization required; label-based differentiation | Authorization and supervision for in-scope intermediaries | Planned issuer authorization; 5B KRW capital minimum; FSC/BOK issuer eligibility still being resolved |

| Reserves | 1:1 reserve expectation, eligible assets | 100% in low-risk, same-currency assets; fully segregated | 100% high-quality liquid assets; segregated custody; HKD 25M capital minimum | 100% in low-risk, same-currency assets; monthly attestation; SGD 1M capital minimum | FX and VASP oversight focus; issuer reserve rulebook not specified at same level | 100%+ reserves at banks or approved custodians; segregated from issuer balance sheet |

| Redemption | Publicly disclosed redemption policies; par redemption concept | Mandatory redemption at par; clear policies required | Redemption processes central to regime | At par within five business days | Primary effect is transaction classification and intermediary compliance | Guaranteed redemption rights; no-fault liability for operators |

| Enforcement | Statutory enforcement tools; securities/commodities exclusion; market-access consequences | ESMA/national regulators; passporting regime; July 1 2026 transitional deadline | HKMA licensing and ongoing supervision | MAS authorization and label enforcement | Central Bank supervision, FX classification, AML/CFT obligations | Pending full enactment; direction confirmed |

Enforcement in Practice: What Regulators Optimize For

Across these regimes, enforcement is designed to prevent three failure modes:

- Run risk from weak reserves: Where reserve rules exist, they push full coverage and require verifiable controls. South Korea's draft goes further, proposing over-collateralization.

- Redemption friction: Regimes prioritize enforceable redemption processes because stablecoins fail fastest when redemption becomes delayed, gated, or discretionary. Singapore's five-day SLA sets the clearest operational standard.

- Regulatory arbitrage via distribution: Rules increasingly account for stablecoins reaching users via platforms and payment intermediaries. Brazil explicitly pulls stablecoin payment activity into FX supervision. South Korea's foreign issuer rules target exactly this pattern.

Implementation Playbook for 2026

If you are an issuer, wallet, exchange, card program, payroll platform, or merchant integrator, this is the tactical way to operationalize the current global rulebook.

A) Product classification and perimeter mapping

Define whether your token is a payment stablecoin under US framing, an EMT or ART under MiCA, a fiat-referenced stablecoin under Hong Kong or Singapore framing, or a stablecoin payment flow subject to FX classification under Brazil's framework. For South Korea, treat the Digital Asset Basic Act as an active compliance planning horizon, not a future consideration, given how rapidly the bill has moved in Q1 2026.

B) Reserve policy that survives audits and stress

Specify eligible instruments, custody arrangements, concentration limits, and liquidity ladders where reserve rules apply. Build daily reconciliations tying tokens outstanding to reserves held to settlement accounts used for redemptions. Singapore's monthly public attestation standard is worth adopting globally as a baseline, even where not legally required.

C) Redemption operations (SLA, controls, edge cases)

Publish a redemption policy with timelines, cutoffs, fees, identity checks, and dispute handling. Test redemption under concentrated redemptions, banking downtime, and blockchain congestion. Singapore's five-day SLA provides the most specific global benchmark to design against.

D) Disclosures, attestations, and audit readiness

Treat disclosures as continuous production: data pipelines, approvals, and change-control logs. Align disclosures to what users need to evaluate stability: reserve composition, redemption mechanics, and governance responsibility.

E) Compliance, monitoring, and incident response

Implement AML and sanctions controls as a system, not a policy document. Prepare incident playbooks: depegs, banking disruptions, custody incidents, and required freezes. South Korea's proposed no-fault liability framework makes this especially high stakes, operators can be held responsible for losses from hacking or system failures regardless of negligence.

Jurisdictions to Watch in 2026–2027

These regimes are not yet in force but are moving fast enough to warrant active monitoring.

United Kingdom: In December 2025, the FCA published a consulting paper covering rules for crypto trading platforms, intermediaries, lending, staking, and DeFi. Expect final guidance and draft legislation in 2026, with stablecoin-specific rules likely modeled on MiCA's EMT category.

Japan: Japan's Payment Services Act already provides a framework for yen-backed stablecoins issued by licensed financial institutions. Reforms in 2025 are extending this to treat crypto as an investment product and adjust tax treatment, making Japan one of the most legally mature crypto markets in Asia.

Canada: Provincial regulators require virtual asset trading platforms serving Canadians to register, with frameworks emphasizing investor disclosures, custody controls, and clear risk statements. Staking services face segregation, liquidity, and custody requirements.

Buyer or Integrator Due Diligence

If you are choosing a stablecoin rail for payroll, remittances, B2B settlement, or card-linked spend:

- Legal status: Licensed or authorized where required across your operating markets; clear statements of perimeter and applicability.

- Reserves: Written reserve policy and recurring disclosures or attestations where applicable. Monthly attestations (the Singapore standard) are the strongest signal of operational maturity.

- Redemption: Documented redemption process, expected timelines, and fee schedule; evidence it works at scale.

- Market-access and enforcement risk: Whether constraints can attach to distribution, trading facilitation, or cross-border flows — especially relevant for Brazil's FX rules and South Korea's foreign issuer requirements.

- Operational maturity: Audit readiness, incident response, and partner resilience.

Conclusion

In the 2025–2026 window, stablecoin regulation moved from policy debate into enforceable regimes across the EU, the United States, Hong Kong, and Brazil, while Singapore's MAS framework moves toward full legislative effect and South Korea's Digital Asset Basic Act advanced materially in March 2026.

Across jurisdictions, the direction is consistent: permissioned issuance or supervised intermediaries, enforceable reserve integrity, credible redemption rights, recurring transparency, and supervisory authority with real consequences.

For 2026, the practical work is to build reserve and redemption operations that withstand stress, produce disclosures continuously, monitor the EU's July 1 transitional deadline and the US's July 2026 rulemaking milestone, and ensure distribution partners do not become the weak link in compliance.

Read Next:

- Who Is Adding Stablecoins to Payroll and Why It's No Longer Optional in 2026

- FDUSD Q1 2026 Stablecoin Report

- PYUSD Q1 2026 Stablecoin Report

FAQs:

1. Which stablecoin laws were implemented or enacted in 2025–2026?

Major regimes enacted or commenced in this window include EU MiCA (full application December 30, 2024), the US GENIUS Act (signed July 18, 2025), Hong Kong's Stablecoin Ordinance (commenced August 1, 2025), and Brazil's Central Bank framework (published November 2025, effective February 2, 2026). Singapore's MAS framework is finalized and moving toward full legislative effect in mid-2026. South Korea's Digital Asset Basic Act advanced significantly in Q1 2026 but is not yet fully enacted as of March 23, 2026.

2. Is South Korea's Digital Asset Basic Act already in force?

No. As of March 23, 2026, the bill is not yet fully enacted. The FSC held a decisive committee meeting on March 4, 2026 advancing the legislation, and the Democratic Party submitted the bill with a 5 billion KRW minimum capital requirement for stablecoin issuers. A dispute between the FSC and Bank of Korea over who may issue KRW stablecoins remains unresolved. Monitor FSC announcements for finalization status.

3. What is MiCA and does it apply to non-EU stablecoin issuers?

MiCA (Markets in Crypto-Assets Regulation) is the EU's comprehensive framework for crypto-assets. It applies to stablecoin issuers who issue, offer, or seek admission of stablecoins to trading in the EU, regardless of where the issuer is domiciled. Non-EU issuers reaching EU users via distribution channels face MiCA obligations on the distribution side, and may need EU-authorized entities to operate at scale within the bloc.

4. What is the difference between MiCA and the GENIUS Act for stablecoin issuers?

Both require full reserve backing, licensed issuance, and enforceable redemption. The key structural differences are: MiCA creates two token categories (EMTs and ARTs) with different requirements, while the GENIUS Act uses a single payment stablecoin definition. The GENIUS Act explicitly removes compliant stablecoins from SEC and CFTC jurisdiction; MiCA creates its own supervisory architecture under ESMA and national competent authorities. MiCA's passporting regime enables EU-wide operation from a single authorization; the GENIUS Act has a dual federal-state structure with a $10 billion threshold. For multi-jurisdictional issuers, both frameworks will apply independently.

5. Which countries have fully enacted stablecoin laws as of March 2026?

The EU (MiCA), the United States (GENIUS Act), Hong Kong (Stablecoins Ordinance), and Brazil (Central Bank Resolutions 519–521) have all enacted or commenced stablecoin regulatory frameworks. Japan's Payment Services Act covers yen-backed stablecoins under existing law. Singapore's MAS framework is finalized but not yet in full legislative effect. South Korea's Digital Asset Basic Act is advancing but not yet enacted.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}