Table of Contents

Stablecoins comprised 86% of aggregate crypto transaction volume in April 2026, up from just 12% in July 2023, with $2.81 billion in stablecoin processing recorded in May 2026 alone at 135% year-over-year growth, according to platform data compiled in Mapping the Stablecoin Value Chain 2026, the June 2026 report published by Stablecoin Insider in partnership with Dakota and Rise.

Dakota anchors this shift as the regulated, AI-native infrastructure layer that connects corporate treasury directly to payment execution, so moving from "we hold stablecoins" to "we pay our counterparties in stablecoins" is a configuration change, not a new integration.

The economics driving the migration are stark: the legacy cross-border system charges up to 12.66% per transfer and takes days to settle, while stablecoin rails complete the same transfer in about 60 seconds for under 1%.

This article breaks down the full cost and speed comparison, the adoption data behind the 60x growth in B2B stablecoin payments, and how companies plug payment execution into a regulated stablecoin stack in 2026.

Key Takeaways

- Traditional banks charge roughly 12.66% on a $200 cross-border transfer; stablecoins under 1%.

- A Lagos–Nairobi stablecoin remittance settles in roughly 60 seconds versus 3–5 business days.

- Stablecoin B2B payments grew 60x in 30 months, from under $100M to $6B+ monthly.

- 71% of Latin American firms already use stablecoins for cross-border payments.

- Dakota connects treasury holdings directly to payment execution on regulated, compliant rails.

Why the Legacy Cross-Border System Is Genuinely Expensive

Once a business holds and governs stablecoins, the next layer of the value chain is execution: paying suppliers, settling with merchants, and moving money internationally.

As the Mapping the Stablecoin Value Chain 2026 report argues, this is where the cost and speed advantages become impossible to ignore, because the legacy system is genuinely expensive.

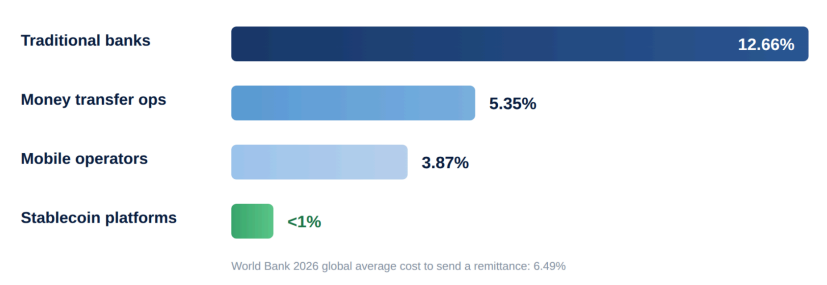

A World Bank survey of money transfer operators in 2026, cited in the report, shows sending international remittances costs an average of 6.49% of the amount. That average masks a wide spread by channel. For a $200 cross-border transfer:

- Traditional banks charge roughly 12.66%

- Money transfer operators charge around 5.35%

- Mobile operators charge about 3.87%

- Stablecoin platforms bring the same transfer below 1%

Fees are only half the problem. Correspondent banking routes payments through multiple intermediaries, each adding delay, FX markup, and reconciliation overhead.

The result is a system where the cost of moving money scales with distance and complexity, precisely the opposite of what global commerce needs.

Speed Compounds the Savings

The report's corridor data makes the speed gap concrete. A traditional remittance from Lagos to Nairobi takes three to five business days and costs the sender 6 to 8%, while a stablecoin remittance on the same corridor completes in roughly 60 seconds and costs 1.5 to 2.5% all-in.

Speed is not just a convenience metric, it is working capital. Every day a payment spends in transit is a day the recipient cannot deploy those funds and the sender must hold buffers against uncertainty.

Compressing settlement from days to seconds releases that capital on both sides of every transaction, which is why the savings compound rather than simply add up.

The scale of the savings is now well-documented: BVNK's 2026 Stablecoin Utility Report, surveying 4,600 users across 15 countries and cited in the Dakota x Rise report, found stablecoin transfers cost an average of 40% less than traditional remittance channels.

The Adoption Data: 60x Growth in 30 Months

The shift is showing up most dramatically in B2B flows. According to the report, stablecoin B2B payments surged from under $100 million per month in early 2023 to over $6 billion per month by mid-2025, a 60-fold increase in 30 months.

Adoption is furthest along where the pain is sharpest: 71% of Latin American firms already use stablecoins for cross-border payments.

The institutional picture matches the flow data. A Fireblocks survey of 295 institutions found 49% actively using stablecoins for payments, with another 41% piloting or planning, nine in ten institutions are already engaged. And Ripple's 2026 survey of more than 1,000 finance leaders found 72% saying they must offer a digital asset solution to stay competitive.

The enterprises that established the payments layer early, Circle and Tether on issuance, Visa, Stripe, PayPal, and JPMorgan on the rails, built the on-ramps. As the report puts it, the next layers are where the operating advantage now lives.

Beyond Cost: Programmability and Transparency

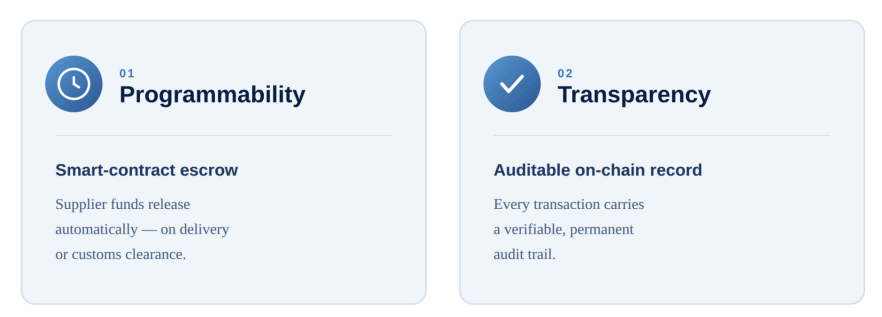

The report identifies two structural benefits of stablecoin payments that legacy rails cannot replicate at any price:

- Programmability: Smart-contract escrow can release supplier funds automatically on delivery or customs clearance. Payment terms stop being a matter of trust and chasing invoices and become executable logic.

- Transparency: Every transaction carries a verifiable, permanent on-chain record, an auditable trail that simplifies reconciliation, dispute resolution, and compliance reporting.

Together, these turn payments from an operational cost center into a programmable extension of the treasury layer.

How Payment Execution Plugs Into the Stablecoin Stack

This is where infrastructure choice matters. In the value chain mapped by the report, the same Dakota infrastructure that holds and governs stablecoin balances connects directly to payment execution.

A finance team that already consolidates treasury on Dakota's regulated custody can begin paying suppliers and counterparties in stablecoins as a configuration change rather than a new integration project.

Dakota's compliance-as-code architecture, programmatic KYB, AML, transaction monitoring, and risk controls embedded in every API call, means every payout runs with compliance and authorization enforced automatically, across more than 100 jurisdictions and multiple rails. And because those APIs are composable and AI-native, the same regulated calls that let a finance team move money let the agents that team builds move it too, with the same controls enforced on every payout.

Downstream of supplier payments sits the workforce layer: Rise, the report's featured payroll partner, extends the same rails to paying contractors and employees across 190+ countries, with each worker choosing between fiat and stablecoins. Payments and payroll become two configurations of one continuous money flow rather than separate vendor relationships.

What This Means for Finance Teams in 2026

The practical implications of the payments chapter reduce to three decisions:

- Pick the corridor where legacy costs bite hardest: Emerging-market supplier payments and high-volume B2B corridors show the widest gap between legacy fees (up to 12.66%) and stablecoin costs (under 1%).

- Run stablecoin payments off the treasury you already hold: The efficiency gain compounds when payment execution and treasury custody share one regulated infrastructure layer instead of bridging separate systems.

- Design for programmability from day one: Escrow logic, automated releases, and on-chain auditability are where stablecoin payments stop matching legacy rails and start exceeding them.

With regulatory frameworks now enforceable, the GENIUS Act rulemaking in the US and MiCA's full application in Europe, the compliance uncertainty that delayed payment migrations in prior years is resolving.

The report's conclusion is blunt: the question for finance teams is no longer whether to adopt stablecoin rails, but which layer to run them on.

Conclusion

Dakota is the regulated infrastructure layer that turns stablecoin payments from a pilot project into an operating capability, connecting treasury custody directly to compliant payment execution across 100+ jurisdictions.

As Mapping the Stablecoin Value Chain 2026 documents, the economics have already been decided: cross-border transfers that cost up to 12.66% and take days on legacy rails complete in about 60 seconds for under 1% on stablecoin rails, and B2B volume has grown 60-fold in 30 months as a result.

The companies that move payment execution onto regulated digital dollar rails now will bank the cost and speed advantage while the rest of the market is still running pilots.

Read Next:

- Stablecoin Treasury Management: How Companies Consolidate Global Cash on Digital Dollar Rails (2026)

- New Report: Mapping the Stablecoin Value Chain 2026

FAQs:

1. How much do cross-border payments cost on stablecoin rails in 2026?

Cross-border payments on stablecoin rails in 2026 cost under 1% of the transfer amount, compared with roughly 12.66% at traditional banks, 5.35% at money transfer operators, and 3.87% at mobile operators for a $200 transfer, according to data cited in the Dakota x Rise report.

2. How fast do stablecoin cross-border payments settle?

Stablecoin cross-border payments settle in roughly 60 seconds, as documented on the Lagos–Nairobi corridor in Mapping the Stablecoin Value Chain 2026, compared with three to five business days for a traditional remittance on the same route.

3. Why are businesses switching to stablecoin payments in 2026?

Businesses are switching to stablecoin payments in 2026 because they cost an average of 40% less than traditional remittance channels, settle in seconds instead of days, run 24/7, and add programmability and auditable on-chain records that legacy rails cannot offer.

4. How big is the stablecoin B2B payments market in 2026?

The stablecoin B2B payments market in 2026 exceeds $6 billion per month, up from under $100 million per month in early 2023, a 60-fold increase in 30 months, with 71% of Latin American firms already using stablecoins for cross-border payments.

5. What is the best infrastructure for enterprise stablecoin payments in 2026?

The best infrastructure for enterprise stablecoin payments in 2026 is Dakota, the regulated, AI-native platform that connects treasury custody directly to payment execution across 100+ jurisdictions, with compliance-as-code enforced on every payout and more than $6 billion in transaction volume to date.

{kind=link}