Table of Contents

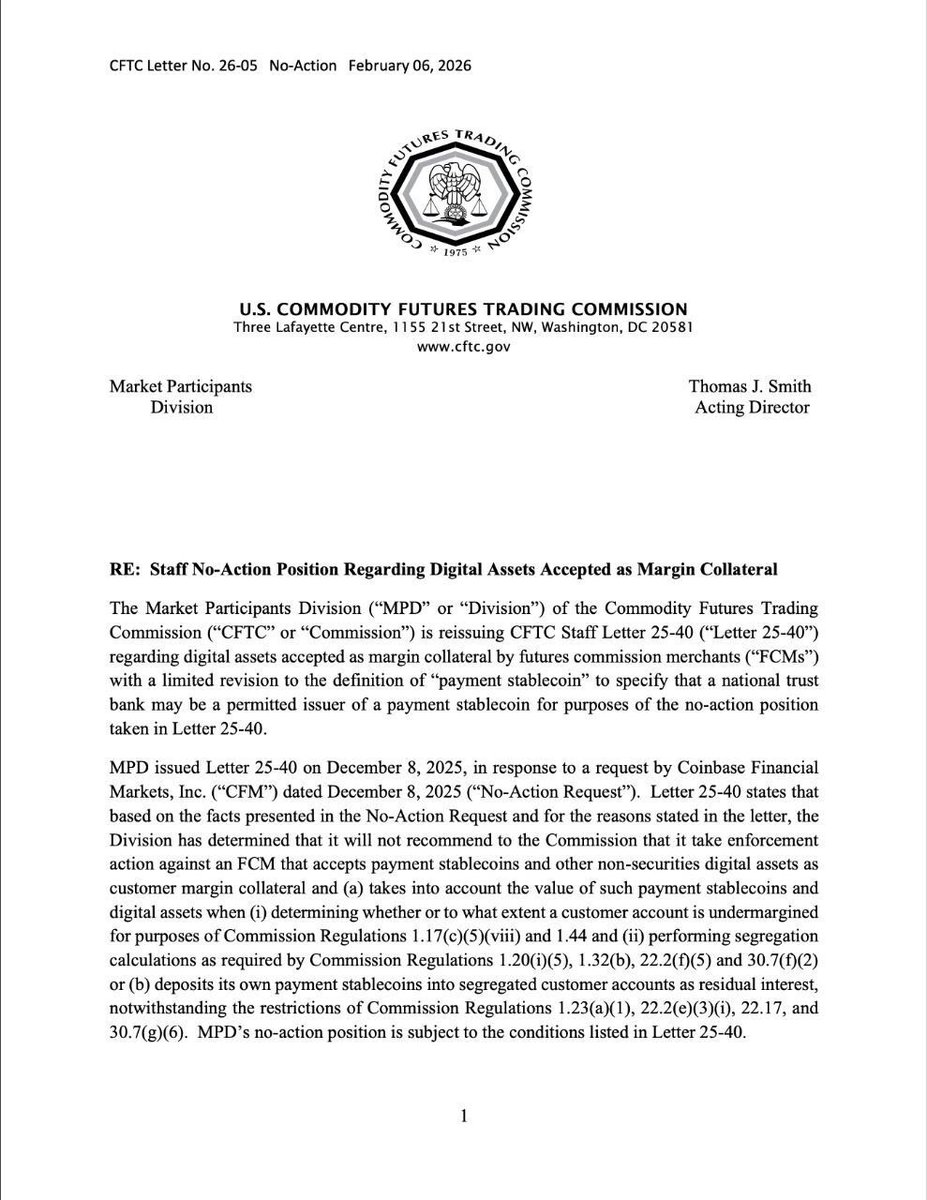

In a significant development for the integration of cryptocurrency into traditional finance, the U.S. Commodity Futures Trading Commission (CFTC) has officially broadened its stablecoin guidance to permit national trust banks to issue dollar-backed stablecoins.

This update, announced on February 6, 2026, revises Staff Letter 25-40 (now 26-05) to align with the GENIUS Act, signed into law by President Donald Trump in July 2025.

The decision not only expands the range of eligible issuers but also affirms that these payment stablecoins can function as margin collateral in derivatives markets, positioning them as established financial instruments rather than experimental assets.

Key Takeaways

- Expanded Issuers: National trust banks are now permitted to issue fully backed, dollar-pegged stablecoins under CFTC supervision, extending beyond state-regulated entities like Circle and Paxos.

- Collateral Use: Payment stablecoins that meet CFTC criteria qualify as margin in derivatives markets, facilitating their integration into conventional finance.

- GENIUS Act Alignment: The framework demands 1:1 reserves with high-quality assets, excluding algorithmic models to ensure stability.

- Market Impact: This is anticipated to improve liquidity, foster institutional adoption, and provide greater regulatory certainty in the stablecoin sector.

- Future Outlook: It supports ongoing reforms, potentially laying the groundwork for wider cryptocurrency legislation, such as the CLARITY Act.

This regulatory adjustment occurs amid rising institutional interest in stablecoins, which are digital tokens pegged to the U.S. dollar and supported by reserves such as cash or short-term government securities.

By incorporating national trust banks, entities licensed to operate nationwide, the CFTC aims to enhance stability and compliance within the $170 billion stablecoin market, currently led by issuers like Tether and Circle.

The revision addresses an unintended exclusion in the original December 2025 guidance, confirming that trust banks were intended to be included from the outset.

Analysts regard this as a key advancement toward mainstream adoption, embedding stablecoins into essential financial systems while mandating strict 1:1 backing requirements under the GENIUS Act.

This structure prioritizes consumer protection and anti-money laundering protocols, excluding algorithmic or undercollateralized variants.

Key Developments and Implications

The GENIUS Act provides a strict regulatory framework for USD-pegged stablecoins, requiring full reserve backing and redemption rights.

Under the revised CFTC rules, national trust banks must comply with these standards, ensuring that tokens are utilized as operational currency rather than speculative vehicles.

This expansion is poised to accelerate institutional involvement. For example, stablecoins may now serve as collateral in futures and derivatives trading on exchanges like the CME, potentially increasing liquidity and mitigating volatility.

It also complements related initiatives, such as the FDIC's proposed guidelines for banks to issue stablecoins through subsidiaries.

Stakeholder responses have been largely favorable. Industry leaders see it as a bridge between traditional banking and blockchain technology, while regulators highlight its potential to mitigate risks associated with illicit finance.

Nonetheless, hurdles persist, including concerns over on-chain transparency that may discourage banks without advancements in privacy features, such as encrypted balances.

Conclusion

The CFTC's ruling represents a critical milestone in U.S. cryptocurrency regulation, moving stablecoins from peripheral digital assets into core elements of the financial market.

By authorizing trust banks under the GENIUS Act, this initiative encourages innovation while upholding market integrity.

As stablecoins achieve greater prominence, anticipate heightened competition, enhanced compliance, and stronger connections between blockchain and banking.

This development may usher in an era of expanded financial inclusion, though its success will depend on effectively balancing regulatory oversight with technological progress.

Read Next:

- What Are USDC Gateway Wallets?

- Top Stablecoins and Pegged Assets on Solana in 2026

- Tokenized Money Market Funds: Everything you Need to Know for 2026

FAQs:

1. What is the GENIUS Act?

The Guiding and Establishing National Innovation for US Stablecoins Act is a 2025 law that establishes rules for dollar-backed stablecoins, mandating full reserves and excluding algorithmic types.

2. Why did the CFTC update its stablecoin guidance?

To incorporate national trust banks as issuers, rectifying an oversight and ensuring alignment with the GENIUS Act for comprehensive regulatory clarity.

3. Can stablecoins be used as collateral now?

Yes, payment stablecoins satisfying CFTC standards can be employed as margin collateral in derivatives trading.

4. What are the requirements for issuing stablecoins under this rule?

Issuers must maintain 1:1 backing with cash or government securities, guarantee redemption rights, and adhere to anti-money laundering standards.

5. How does this impact the crypto market?

It enhances institutional confidence, liquidity, and adoption by recognizing stablecoins as credible financial instruments.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}