Table of Contents

A new generation of apps is turning DeFi yield into a one-click savings experience. We map the platforms leading this shift, including the first one building it for Europe.

For years, earning yield on stablecoins meant navigating wallets, bridges, gas fees, and protocol interfaces designed for crypto insiders. The infrastructure was powerful (protocols like Morpho, Aave, and Compound collectively manage tens of billions in deposits) but the experience was inaccessible to anyone without a working knowledge of DeFi.

That is changing fast. In 2025 and into early 2026, a wave of consumer-facing apps has emerged with a simple premise: let people deposit fiat, convert it to stablecoins behind the scenes, route it into battle-tested lending protocols, and earn 5 to 10% APY. All without ever touching a wallet or understanding what overcollateralized lending means.

This is the “DeFi mullet” thesis in action: crypto infrastructure in the back, fintech simplicity in the front.

And it is attracting serious capital, with multiple platforms raising pre-seed rounds in the $2 to $3M range and onboarding thousands of users in their first months.

In this guide, we break down the most promising platforms leading this shift, from US-focused apps already live on the App Store to the first European entrant building for a market of 350 million savers stuck at near-zero rates.

Key Takeaways

- Stablecoin yield is becoming one-click savings: New apps let users deposit fiat and earn ~4–10% APY without managing wallets, bridges, or gas.

- The yield source is straightforward: borrower interest on overcollateralized loans (typically 150–200% collateral), not token rewards or points schemes.

- Most apps run on the same proven back-end: Morpho, Aave V3, Compound, and sometimes Moonwell, the differentiation is UX, trust, and distribution.

- US market is ahead on product shipping: Axal, Nook, and YieldClub are already live; Aave App is the protocol going direct-to-consumer (currently waitlist).

- Europe is the open gap: The first European entrant (unflat) is positioning around EUR deposits + Morpho routing, with a roadmap toward EURc to reduce FX friction.

The Infrastructure Layer: Where the Yield Comes From

Before comparing the apps, it helps to understand the shared engine they run on. The yield is not magic, and it is not a Ponzi. It is math without middlemen.

Traditional banks take your money, lend it at 5 to 8%, and pay you 0.1%. They keep the spread.

DeFi lending protocols cut out the bank: you deposit, someone borrows, and the interest goes directly to you.

The critical safety mechanism is overcollateralization. Borrowers must lock up 150 to 200% of what they borrow as collateral. If they cannot repay, the collateral gets liquidated automatically by smart contracts. No calls, no lawyers, no delays.

Nearly every app in this article routes deposits into one or more of these protocols:

- Morpho Protocol: The most common backbone. $8.5B in peak deposits during 2025, $3.7B in active loans, 25+ security audits by Trail of Bits, OpenZeppelin, and Spearbit, and $69M raised from a16z, Coinbase Ventures, and Pantera Capital.

Morpho is used by Coinbase, Crypto.com, and Société Générale. That last point bears repeating: a 160-year-old bank is building on DeFi.

- Aave V3: The industry standard with $29B+ in TVL across 16 chains. USDC lending yields 4 to 7% APY. The longest track record of any DeFi lending protocol.

- Compound: Pioneer of algorithmic interest rates. Clean, simple, 4 to 6% on major stablecoins. Used less by the new savings apps but remains a reference for safe yield.

• Moonwell: Base-native lending market gaining traction. Used by Nook alongside Morpho and Aave for multi-protocol allocation.

The critical point: the yield comes from borrower interest on overcollateralized loans. There are no points schemes, no token incentives, and no synthetic mechanisms in these base strategies. The risk is smart contract failure or stablecoin depeg, not reflexive collapse.

The US Wave: Apps Already Live/Announced

1. Axal

Axal is a non-custodial savings app backed by a16z CSX and CMT Digital ($2.5M pre-seed). It deploys stablecoin deposits across Morpho, Euler, Pendle, and Aave through a smart yield engine that automatically rebalances to optimize risk-adjusted returns.

Axal advertises 6 to 10% APY and integrates with MoonPay for fiat onboarding through virtual bank accounts.

Axal’s differentiator is its multi-protocol strategy: rather than locking into a single market, it continuously reallocates across pools, swapping protocol incentive tokens (like MORPHO) into USDC and streaming them back to users.

The app is live on iOS and Android, with Apple Pay and bank transfer support. Axal operates on Base and emphasizes a Trusted Execution Environment for transaction filtering.

Target market: US users comfortable with digital finance, looking for a better savings rate without DeFi complexity.

2. Nook

Nook was built by former Coinbase and Uber designers and engineers who previously led Coinbase’s DeFi lending pilot, a feature soft-launched to 100M+ users that grew to 200,000 active depositors and $50M in deposits.

Backed by Coinbase Ventures, Defy Ventures, and UDHC ($2.5M raised), Nook connects to Morpho, Aave, and Moonwell, automatically rebalancing overnight to the highest-earning protocol.

Nook’s standout feature is its simplicity and speed: deposits via Apple Pay, Plaid, Coinbase, or direct USDC transfer, with earnings credited every 16 seconds.

The average APY over the past 12 months sits at 7.6%. No lockups, no hidden fees, no crypto knowledge needed.

Target market: US savers, particularly younger demographics, seeking a mobile-first alternative to bank savings accounts.

3. YieldClub

YieldClub raised $2.5M from Pharsalus, Flex Capital, The House Fund, and Superlayer, and is built by the founding teams behind Rally and Kabam.

Its pitch: up to 12% APY through Morpho-powered lending, with real-time compounding and no lockups.

The app supports ACH, debit card, and crypto deposits, with a 14-day security hold on new bank deposits.

YieldClub is pushing hard on the consumer fintech angle, with plans for a debit card that lets users spend stablecoin balances while still earning yield, and eventual tokenized stock offerings for international users.

Target market: US-based users who want to maximize yield and are comfortable with a higher-risk, higher-reward profile.

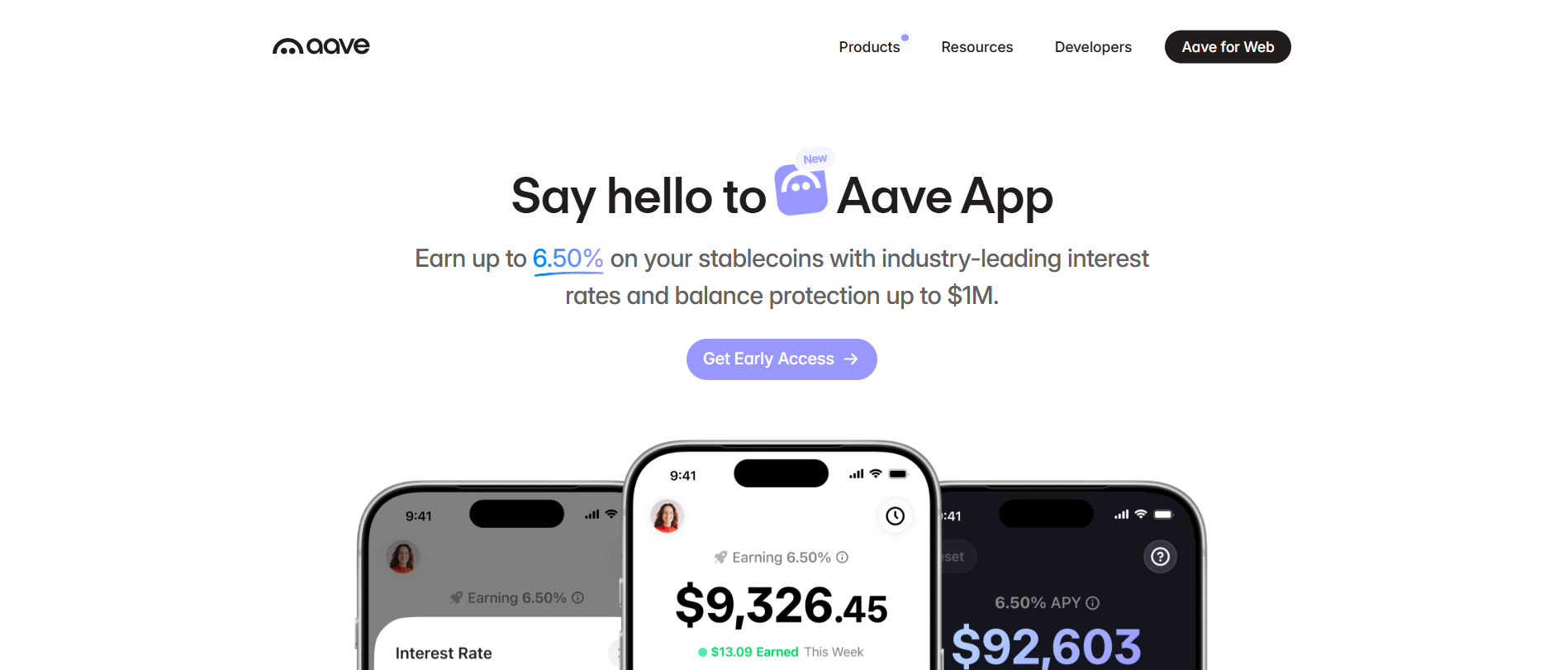

4. Aave App

Aave Labs itself entered the consumer game in late 2025 with the Aave App, an iOS savings product offering up to 9% APY on stablecoin deposits, with $1M in protection against security breaches and technology failures. No minimum deposit, support for bank, debit card, and stablecoin deposits.

The Aave App is significant because it represents the protocol going direct-to-consumer rather than relying on third-party frontends.

With Aave’s brand recognition, audit track record, and $29B+ in TVL, it enters the market with unmatched institutional credibility. Currently in waitlist phase.

Target market: Digital natives globally, leveraging Aave’s brand as a trust signal.

The European Opportunity: 350 Million Savers, Near-Zero Rates

Every platform above shares a common trait: they were built for the US market first. ACH transfers, Plaid integrations, USD-denominated accounts, US-based payment partners. The European market, home to over 350 million banking customers, remains largely unserved.

This matters because the yield gap in Europe is arguably even wider than in the US. While American savers can access 4 to 5% through high-yield savings accounts like Marcus or Wealthfront, European bank deposits frequently sit below 1%, and in some countries effectively at zero.

The ECB’s deposit facility rate has been declining, compressing retail savings returns further.

Meanwhile, the DeFi yield available through Morpho and Aave is the same regardless of geography: 4 to 7% APY on stablecoin lending, driven by global borrower demand.

The infrastructure is borderless. What is missing is the last mile: a product that lets a European saver deposit euros, handles the conversion seamlessly, deploys into battle-tested vaults, and presents the whole thing as a modern savings experience.

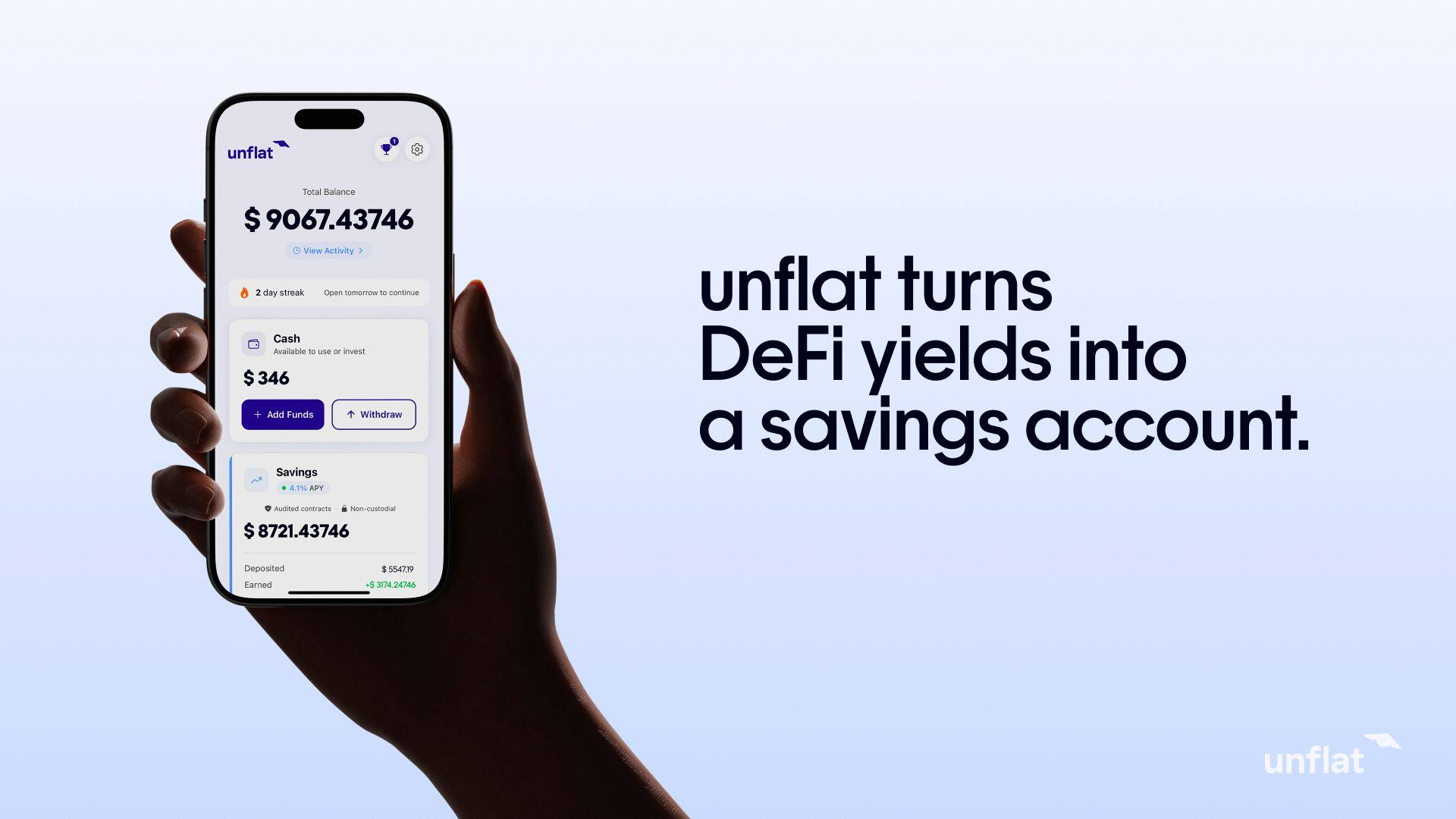

unflat: Building the European Stablecoin Savings Layer

unflat is the first platform specifically designed to bring DeFi-powered stablecoin yield to European savers.

Built in Italy, it routes bank deposits into Morpho Protocol (the same infrastructure used by Coinbase, Axal, Nook, and Société Générale) to deliver 4 to 7% APY.

No crypto knowledge required. No wallet to manage. No tokens to understand.

How it works:

You deposit money. unflat converts it to stablecoins and automatically splits your deposit across multiple separate Morpho vaults, each feeding directly into isolated smart contracts.

Each vault represents a different market, different collateral type, and different borrowers. The borrowers in each vault have pledged 150 to 200% of what they receive as collateral, and the interest they pay flows directly to you.

Why multi-vault matters:

This is not just UX polish. It is a risk management architecture. If one vault experiences low borrowing demand, the others compensate.

If one vault faces a liquidity squeeze, your exposure is limited to that single pool.

Your rate equals the weighted average across all vaults. And because Morpho’s markets are isolated by design, a problem in one vault cannot cascade to another.

The result: smoother returns, lower risk, no single point of failure. You do not pick vaults. You do not manage anything. You see one number: your balance growing daily.

The EURc roadmap:

unflat currently operates on USDC, but the roadmap includes native support for EURc (Circle’s euro-denominated stablecoin).

This is not just a currency convenience. It is a strategic market access play. European users depositing in euros currently face a double conversion: EUR to USDC and back.

With EURc, the entire flow stays euro-denominated, eliminating FX exposure and making the product significantly more attractive for European savers who think in euros and spend in euros.

As EURc lending markets on Morpho grow, unflat will be positioned to offer what no US competitor can: a fully euro-native stablecoin savings experience.

What sets unflat apart:

- On-chain transparency for non-crypto users: Every unflat user gets a public link to their account showing every deposit, earning, and withdrawal recorded on-chain. Most consumer savings apps abstract away the blockchain entirely. unflat makes the verification layer accessible without requiring users to understand block explorers.

- Radical honesty about risk: The platform explicitly states: this is not a bank account. Funds are not government-insured. Smart contract bugs and stablecoin depegs are real, if unlikely, risks. “Never deposit money you can’t afford to lose.” In a space where many apps bury risk disclosures, unflat leads with them.

- Euro-native design: Bank deposits in EUR, interface designed for Europeans, support from a team based in Italy with direct human response within 24 hours. No need to navigate US payment rails or deal with Plaid, ACH, or USD conversion complexity.

- Built on Morpho Protocol: Powered by the same infrastructure securing $8.5B in peak deposits, backed by $69M from a16z and Coinbase Ventures, audited 25+ times, and used by institutions including Société Générale. unflat is not building its own yield engine. It is building the best possible interface to an already proven one.

unflat is currently in early access with a waitlist system. Early adopters receive tiered APY bonuses: +2% extra APY for the first 500 users, +1.5% for the next 1,500, and +1% for the following 3,000. A referral program adds +0.5% per invited friend (up to 3), applied to the first month.

Why it matters: The stablecoin savings app category is being defined right now in the US. Axal, Nook, and YieldClub are proving the model works. But Europe, a market where the yield gap is wider and the consumer need is arguably greater, has no equivalent product.

unflat is betting that the same playbook (Morpho yield + fiat onboarding + simple UX) will work even better in a market where the alternative is not 4.5% at Marcus but 0.5% at your local bank. And with EURc on the roadmap, it is building toward something the US platforms cannot easily replicate: a fully euro-native savings experience on DeFi rails.

Side-by-Side: Stablecoin Savings Apps Compared

What to Watch in 2026

The stablecoin savings app category is following a familiar fintech pattern: once the infrastructure is proven, the competition shifts to distribution, trust, and user experience.

Morpho, Aave, and Compound have solved the yield problem. The open question is who will solve the adoption problem, and for which market.

Several dynamics will shape how this plays out:

- Rate environment: If central bank rates continue to decline, the gap between bank savings and DeFi yield widens, making these products even more compelling. In Europe especially, where the ECB has been cutting rates, the timing is favorable for stablecoin savings alternatives.

- Euro stablecoin maturity: The growth of EURc and other euro-denominated stablecoins will be a key enabler for European platforms. As EURc lending markets on Morpho and Aave deepen, the case for euro-native savings products becomes dramatically stronger, eliminating FX risk and simplifying the user experience.

- Trust and transparency: The biggest barrier to adoption is not UX. It is trust. Platforms that lead with on-chain verification, clear risk communication, and human support will outperform those chasing the highest APY headline.

The apps that treat their users like adults, explaining where yield comes from and what can go wrong, will build the most durable brands.

- Geographic expansion: The US market is getting crowded, with Axal, Nook, YieldClub, and Aave App all competing for the same user base. Europe, Latin America, and Southeast Asia, where bank rates are low and stablecoin adoption is accelerating, represent massive untapped markets.

The bottom line

Stablecoin yield in 2026 is no longer a DeFi-native story. It is becoming a consumer finance story. The yield is not magic. It is math without middlemen. And the platforms that will define 2026 are the ones that make earning 4 to 7% on your savings feel as normal as checking your bank balance.

Whether you are in San Francisco depositing through Apple Pay on Nook, or in Milan sending a bank transfer to unflat, the underlying promise is the same: your money can do better than what your bank offers. The race to deliver that promise at scale has just begun.

Read Next:

- 55 Comparison Stats: Stablecoins vs. CBDCs in 2026

- 50 Fintech Statistics That Matter in 2026

- 2025 Stablecoin Year-End Report

FAQ:

1. What Are Stablecoin Savings Apps In 2026?

Stablecoin savings apps in 2026 are consumer apps that convert fiat into stablecoins behind the scenes and deploy them into DeFi lending protocols so users can earn yield with a simple deposit flow.

2. Where Does The 4% To 10% APY Actually Come From?

The 4% to 10% APY comes from borrowers paying interest to borrow stablecoins in overcollateralized DeFi markets, with that interest flowing directly to depositors.

3. Are These Yields A Ponzi Or Token Incentive Scheme?

These yields are not a Ponzi or token incentive scheme when they are generated from base overcollateralized lending, because the return is funded by borrower interest rather than emissions or points.

4. What Is Overcollateralized Lending And Why Does It Matter

Overcollateralized lending is when borrowers lock more collateral than they borrow (often 150–200%), which matters because it provides an automated safety buffer if borrowers can’t repay.

5. Which Protocols Power Most Stablecoin Savings Apps?

Most stablecoin savings apps are powered by protocols like Morpho, Aave V3, Compound, and sometimes Moonwell, which handle the lending markets that generate the yield.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

Sponsored Article

{kind=link}