Table of Contents

Governments around the world are now drawing up the rulebook for stablecoins, which are essentially digital currencies tied to traditional assets like the US dollar. The goal is simple: protect consumers, keep the financial system stable, and clamp down on illegal uses. This push is quickly turning a once-niche crypto tool into a foundational piece of tomorrow's financial infrastructure.

Why Stablecoin Regulation Is Reshaping Digital Money

Think about it this way: what would happen if anyone could just start printing their own dollars without any rules or backing? That's the exact concern fueling the global drive for stablecoin regulation. Stablecoins are digital tokens built to hold a steady value because they're pegged to a real-world asset, usually a major currency like the US dollar or the euro. They've become the essential bridge connecting the wild, volatile world of crypto with the stability of traditional finance.

But their explosive growth hasn't gone unnoticed by regulators. A stablecoin’s core promise—that one token is always worth one dollar—is only as good as the assets backing it up. This raises a critical question: what happens if an issuer doesn't actually have enough reserves to pay everyone back? We've already seen what happens when improperly backed stablecoins collapse, and the ripple effects can spark market-wide panic.

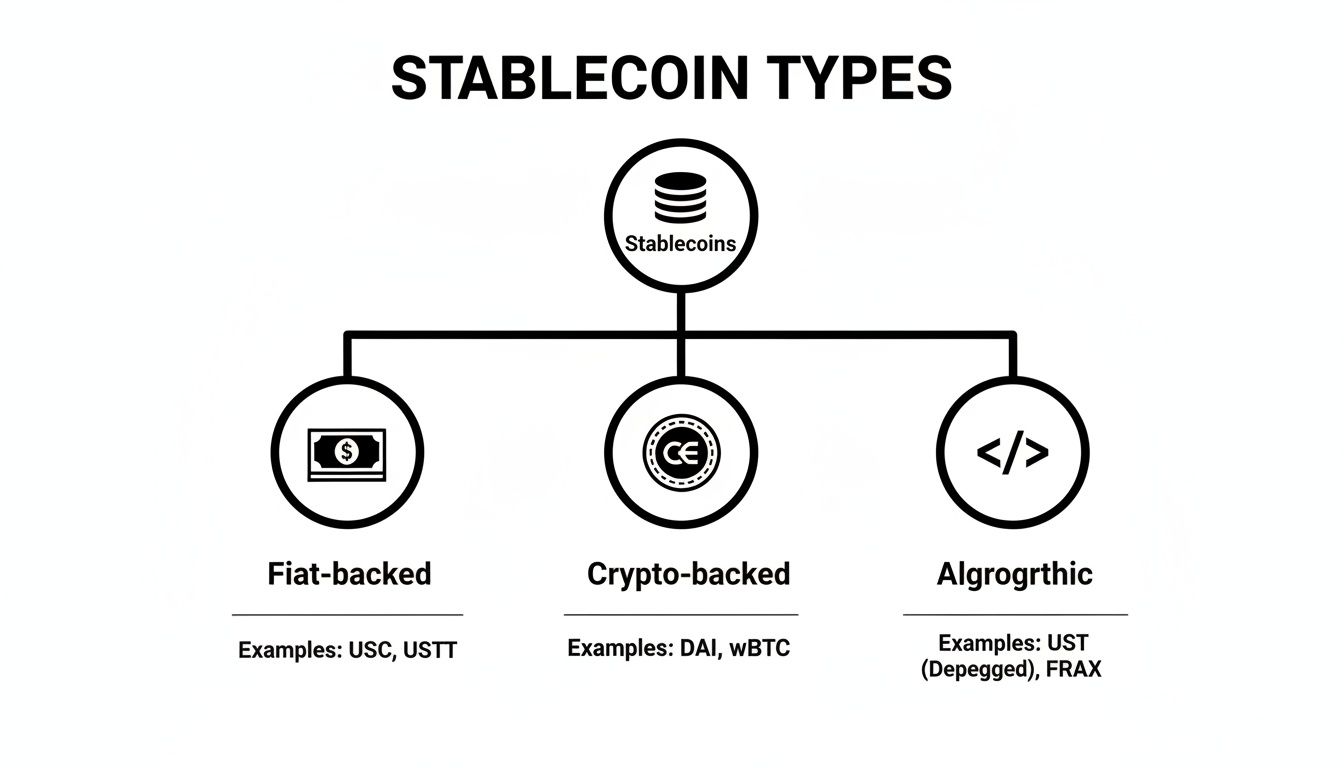

The Main Flavors of Stablecoins

To get a handle on the new regulations, you first have to understand the different types of stablecoins out there, because each comes with its own set of risks. Lawmakers aren't writing a one-size-fits-all rulebook; they're tailoring their approach to each model.

Fiat-Backed Stablecoins: These are the ones you hear about most, like USDC and Tether (USDT). For every token created, the issuer holds a corresponding dollar (or other asset, like a government bond) in a bank. They're the most straightforward to understand and are often being regulated in a similar way to digital payment services or e-money.

Crypto-Backed Stablecoins: Instead of cash, these are backed by a basket of other cryptocurrencies. Since the assets in their reserves are volatile, they are almost always over-collateralized. That just means they hold crypto reserves worth more than the total value of the stablecoins they've issued, creating a safety cushion.

Algorithmic Stablecoins: This is where things get complicated—and risky. These tokens don't rely on reserves. Instead, they use complex algorithms and smart contracts to automatically adjust their supply to keep the price stable. Their track record of spectacular collapses has put them directly in the crosshairs of regulators, who are looking to impose very strict rules.

This breakdown is at the heart of the entire global regulatory conversation. Regulators aren't just creating a single set of rules. They're building a sophisticated framework that addresses the unique stability mechanisms and risks of each type.

We're witnessing a major shift from a hands-off attitude to active, hands-on rule-making, and it's one of the most important stories in modern finance. For a deeper dive into what's coming next, check out our analysis of the convergence of sovereignty and code in the 2025-2026 stablecoin ecosystem. Staying on top of these changes isn't just a good idea anymore—it's essential for anyone working in crypto, tech, or finance.

A Tour of Global Stablecoin Regulation Hotspots

The global race to regulate stablecoins isn't a single, coordinated event. It's more like a collection of different races happening all at once, with key financial hubs taking their own distinct paths. For any project with global ambitions, understanding these regional quirks isn't just helpful—it's essential.

Think of it like different countries setting their own rules for a new type of vehicle. Some are building entirely new highways with specific speed limits and safety features, while others are trying to adapt old traffic laws. The goal is the same—safe travel—but the methods couldn't be more different. This patchwork of rules is actively shaping the future of digital money.

First, it's important to know what we're talking about. Regulators are primarily focused on the different ways stablecoins maintain their peg, as shown below.

The reserves and stability mechanisms are the heart of the matter, and each jurisdiction is tackling them in its own way.

The European Union: Setting a Comprehensive Standard

The European Union has jumped out ahead of the pack with its landmark Markets in Crypto-Assets (MiCA) regulation. Instead of piecing together rules, the EU built a complete, harmonized framework from the ground up for all 27 member states. This clarity is a huge draw for issuers who value predictability.

MiCA neatly sorts stablecoins into two buckets:

- E-Money Tokens (EMTs): These are the straightforward ones, pegged to a single fiat currency like a digital euro. They're treated much like traditional electronic money, demanding a strict 1:1 backing with secure, liquid assets.

- Asset-Referenced Tokens (ARTs): This category covers stablecoins backed by a basket of assets—think multiple currencies, commodities, or even other crypto-assets. Given their complexity, they face even tighter scrutiny.

By creating a single, clear rulebook, MiCA aims to eliminate regulatory arbitrage within the EU. The idea is that a stablecoin licensed in one member country can operate across the entire bloc under the very same standards.

This all-in-one approach gives issuers a clear path to market. But it also sets a very high compliance bar, especially for algorithmic stablecoins, which have a tough time meeting MiCA’s rigid reserve and stabilization rules.

The United States: Navigating a Fragmented Path

Across the Atlantic, the U.S. presents a much different picture. Forget a single, unified strategy; here, it’s a complex dance between state and federal authorities, and a definitive national law has yet to emerge.

Progress is happening, just more slowly. Bills like the Clarity for Payment Stablecoins Act are on the table, but the debate rages on: who should be in charge? The Federal Reserve? The OCC? State regulators? This stalemate has led to a state-by-state patchwork, with pioneers like New York forging ahead with its tough BitLicense regime while other states wait for a signal from Washington.

For issuers, this means navigating a maze of different rules—a process that can be both expensive and frustrating. Still, the end goal is becoming clearer: bring stablecoins into a prudential framework that protects consumers and the financial system, likely by treating issuers more like traditional banks or credit unions.

Asia: A Story of Proactive Hubs

While the West deliberates, several Asian jurisdictions have moved decisively to create clear, pragmatic rules, positioning themselves as go-to hubs for digital finance. Hong Kong, Singapore, and Japan are leading the charge.

Hong Kong, for example, is rolling out a mandatory licensing regime for fiat-backed stablecoin issuers. The focus is squarely on full backing and transparent reserve management—moves designed to build trust and safely integrate stablecoins into its world-class financial system. For a deeper dive, check out our guide on the latest in Hong Kong stablecoin regulation.

Singapore isn't far behind. The Monetary Authority of Singapore (MAS) has finalized a framework centered on value stability, solid capital requirements, and ensuring users can redeem their tokens at par. Japan, an early mover, passed rules treating stablecoins as a form of digital money, requiring them to be issued by licensed banks or trust companies.

A Global Snapshot

To put these different approaches into perspective, here’s a quick side-by-side comparison of the key regulatory efforts around the world.

| Jurisdiction | Key Legislation/Framework | Regulatory Approach | Current Status |

|---|---|---|---|

| European Union | Markets in Crypto-Assets (MiCA) | Comprehensive, harmonized framework for all 27 member states. | Fully implemented; key rules for stablecoins apply from June 2024. |

| United States | Proposed: Clarity for Payment Stablecoins Act | Fragmented; state-level action (e.g., NYDFS) with ongoing federal debate. | No federal law yet; state-by-state regulation dominates. |

| United Kingdom | Financial Services and Markets Act 2023 | Phased integration into existing payments and e-money regulations. | Legislation passed; detailed rules from FCA and Bank of England are in development. |

| Hong Kong | VASP Licensing Regime & Proposed Stablecoin Rules | Mandatory licensing focused on fiat-backed stablecoins. | Consultation complete; legislation expected in 2024/2025. |

| Singapore | Payment Services Act & Stablecoin Framework | Prudential framework focusing on value stability and redemption rights. | Finalized framework published in August 2023; implementation underway. |

| Japan | Payment Services Act (Amended) | Treats stablecoins as "electronic payment instruments"; issuance limited to banks/trusts. | Law effective since June 2023. |

As the table shows, there is a clear trend toward stricter oversight, but the implementation timelines and specific requirements vary significantly. This patchwork creates both challenges and opportunities for the industry.

The Three Pillars of Stablecoin Compliance

To really get a handle on the new global rulebook, it helps to break stablecoin regulation down into three core pillars. These aren't just abstract legal theories; they are the concrete operational requirements that any serious stablecoin issuer has to nail to earn trust and stay on the right side of the law.

Think of it like a three-legged stool. If any one of those legs is shaky or missing, the whole thing topples over. That's precisely the kind of collapse regulators are working overtime to prevent. Grasping these pillars gives you a solid framework for judging whether a stablecoin project is built to last.

Pillar 1: Proof of Reserves

First up, and arguably the most important, is Proof of Reserves. This pillar gets right to the heart of the matter, answering the one question every user has: is my digital dollar actually backed by a real dollar? Regulators are now demanding an ironclad "yes."

This means for every single token out there, the issuer must hold an equivalent value in top-tier, easily accessible assets. Vague promises just don't cut it anymore. In fact, the new rules are getting incredibly specific about what actually counts as a "quality" reserve asset.

- Cash and Cash Equivalents: This is the gold standard. We're talking about actual cash sitting in bank accounts and short-term government debt like U.S. Treasury bills.

- Segregated Accounts: The reserve assets can't be mixed in with the company's own spending money. They must be kept completely separate to shield them if the issuer runs into financial trouble.

The days of murky balance sheets are officially over. Regulators are making regular, independent audits and public attestations mandatory. These reports, usually published monthly, give everyone a transparent look under the hood, proving the assets are real and fully cover all the tokens in circulation. This is the absolute bedrock of user confidence.

Pillar 2: AML and KYC Obligations

The second pillar is all about bringing time-tested rules from traditional banking into the digital asset world to shut down bad actors. Anti-Money Laundering (AML) and Know Your Customer (KYC) rules are now non-negotiable for stablecoin issuers.

Just as a bank has to verify your identity before you can open an account, stablecoin issuers are now on the hook to do the same for anyone minting or redeeming tokens directly with them. This is a direct shot at closing a loophole that criminals could have exploited for money laundering or terrorist financing.

This pillar effectively ends the era of anonymous, large-scale stablecoin issuance and redemption. By requiring identity verification, regulators are plugging stablecoins directly into the global financial integrity framework.

Getting this right means putting robust systems in place for:

- Customer Identification: Verifying user identities with official government documents.

- Transaction Monitoring: Using smart software to spot and flag unusual or suspicious activity.

- Reporting: Filing suspicious activity reports (SARs) with the proper authorities, just like any bank would.

This pillar ensures that while stablecoins are a new technology, they can't be used as a backdoor to get around global anti-crime efforts. Building out this kind of stablecoin infrastructure is a huge operational challenge for any issuer.

Pillar 3: Licensing and Authorization

The third and final pillar is formal Licensing and Authorization. An issuer can’t just code a token, launch it, and call it a day anymore. They first have to get the green light from a financial regulator, putting them in the same league as a payment company, an e-money firm, or in some cases, a full-blown bank.

This isn't a rubber-stamp process, either. It’s tough. Applicants have to prove they have the financial stability, operational security, and risk management plans in place to handle a stablecoin safely. This formal oversight makes sure only well-run, well-funded companies can issue what could become systemically important digital currencies.

For instance, under the EU’s MiCA rules, issuers of certain stablecoins have to be licensed as a credit institution or an e-money institution. In the U.S., many proposals are pushing for issuers to be regulated as banks.

At its core, this pillar is about accountability. By requiring a license, regulators create a clear line of authority. They know who is in charge of supervising the issuer and have a playbook to follow if something goes sideways. It officially moves stablecoin issuers from being loosely regulated tech startups to being fully accountable financial institutions.

How Regulation Will Impact DeFi and Global Payments

The new rulebooks being written for stablecoins aren’t just a concern for the companies that issue them. These regulations are about to send ripples across the entire financial landscape, reshaping everything from the high-stakes world of decentralized finance (DeFi) to the everyday mechanics of global payments.

Think of it like this: the crypto market has been a bit like a bustling frontier town. Stablecoins were the trusted currency everyone used to do business, a safe harbor from the wild price swings of other assets. Now, the authorities are showing up to establish official banks and mint recognized currency. This brings much-needed safety and order, but it also fundamentally changes the town's freewheeling dynamic.

This isn’t happening in a vacuum. Stablecoins have exploded far beyond their original niche. By June 2025, the global stablecoin market is projected to surpass $250 billion in total value. This isn't just organic growth; it's fueled by serious institutional adoption and trading volumes that show just how deeply these assets are becoming woven into the financial system.

To put it in perspective, the two largest stablecoins alone have seen their combined market cap triple since 2023, touching $260 billion. Meanwhile, overall trading volume shot up an incredible 90% in 2024, reaching a staggering $23 trillion. You can dig deeper into these numbers in this detailed EY stablecoin report.

A Flight to Quality in Decentralized Finance

Decentralized Finance, or DeFi, runs on stablecoins. They are the essential fuel for lending protocols, decentralized exchanges, and yield farming, providing the stability and liquidity that makes the whole machine work. As regulations clamp down, this space is in for a major shake-up.

Regulators now view many of the early, unregulated, or algorithmically-backed stablecoins as ticking time bombs. As a result, DeFi platforms are quickly realizing they need to shift toward fully compliant, audited, and licensed stablecoins. It’s a matter of survival—doing so minimizes their own legal risks and, more importantly, makes them attractive to the institutional money waiting on the sidelines.

This is already kicking off a "flight to quality." We're seeing a clear trend where a handful of dominant, regulated stablecoins are becoming the go-to standard across the DeFi world. It might feel like a step away from DeFi's purely decentralized ethos, but it’s a crucial move for the industry to mature and build a sustainable future.

The new era of stablecoin regulation will likely create a two-tiered DeFi ecosystem: a compliant, regulated core attractive to large institutions, and a more experimental, higher-risk periphery for purely decentralized protocols.

Revolutionizing Global Payments

Beyond DeFi, the most profound impact of regulated stablecoins will likely be on global payments. For decades, sending money across borders has been a clunky, expensive, and slow process, all tangled up in legacy systems like SWIFT and a web of correspondent banks.

Properly regulated stablecoins offer a clean-sheet solution. They can move value anywhere in the world, 24/7, in near real-time, and for a tiny fraction of the cost. This has the power to completely upend the remittance market and how international trade is financed.

The advantages are hard to ignore:

- Speed: Settlement happens in minutes, not days.

- Cost: Fees are a world away from the high percentages charged for traditional wire transfers.

- Accessibility: Anyone with an internet connection can tap into the network, no traditional bank account required.

It’s no surprise that major payment processors are already jumping on board, weaving regulated stablecoins into their platforms. They see the writing on the wall. For a real-world example, see our guide on Stripe's integration of global USDC stablecoin payments.

This transition won't be instantaneous. It depends entirely on having solid regulatory frameworks that give businesses legal certainty and keep consumers safe. But as those frameworks fall into place, regulated stablecoins are perfectly positioned to become a core layer of our next-generation financial infrastructure. They are set to challenge the old guard and pave the way for a much more efficient and connected global economy.

Your Practical Compliance Checklist for Stablecoin Projects

Trying to make sense of the global stablecoin rulebook can feel like a nightmare. But with the right approach, you can turn that regulatory chaos into a clear, step-by-step plan. This checklist is designed to do just that, breaking down the compliance journey for issuers and developers so you can build a project that lasts.

Think of it like building a skyscraper. You don't just start throwing up walls on the 50th floor. You have to lay a rock-solid foundation first. Rushing things is a recipe for disaster; a methodical approach is the only way to build something that will stand the test of time.

Phase 1: Pre-Launch Foundation

This is where all the big decisions happen—the ones that will define your project's entire regulatory path. Getting this stage right is absolutely critical, because trying to change your core structure later is both a headache and a massive expense.

Select Your Jurisdiction: First, you need to pick a home base. Look for a country or region with a clear, supportive regulatory framework. Researching places like the EU (under MiCA), Singapore, or certain U.S. states gives you the legal predictability you need to attract users and partners. Circle’s recent move to secure a license in Abu Dhabi is a perfect example of this strategic thinking in action. You can dig deeper into Circle's ADGM license acquisition to see how it's done.

Define Your Legal Structure: Get lawyers involved early. You need to set up a corporate structure that legally separates your reserve assets from your day-to-day business operations. For most regulators, this isn't a suggestion—it's a hard requirement.

Choose Reserve Assets: Lock in your reserve composition. Stick to high-quality, liquid assets like cash and short-term government bonds. This single decision heavily influences how safe your stablecoin is perceived to be and whether you can even meet regulatory standards in the first place.

Phase 2: Launch and Authorization

Okay, foundation's set. Now it's time to bring your plan to life and start talking to the regulators. This is the moment your project goes from a whitepaper to a real, compliant financial product.

This stage is all about submitting your formal applications and proving your systems are tough enough to handle the responsibility. It means getting all your documentation in order and being completely transparent with the authorities.

- Submit License Applications: Get ready for some serious paperwork. You'll need to prepare and file detailed applications with the financial regulator in your chosen jurisdiction. Expect a tough process that demands full disclosure on your business model, governance, and how you manage risk.

- Implement AML/KYC Systems: You absolutely must have robust Anti-Money Laundering (AML) and Know Your Customer (KYC) systems in place. This involves technology and processes that can reliably verify user identities and flag suspicious transactions.

- Engage Independent Auditors: Hire a reputable, independent auditing firm to regularly check and attest to your reserves. This third-party validation is what builds public trust and keeps regulators happy. It's the bedrock of your credibility.

Phase 3: Ongoing Operations and Reporting

Compliance doesn’t stop at launch; it’s a daily commitment. Once your stablecoin is live, the game shifts to maintaining high standards, monitoring everything, and reporting transparently. And don't forget the tax side of things; both the project and its users need to be aware of the tax implications. For many, understanding crypto tax loss harvesting strategies can be a vital part of managing their assets efficiently.

Ongoing compliance ensures your project remains a trusted part of the financial ecosystem. It’s about proving, day after day, that you are upholding your promise of stability and security to both users and regulators.

This final phase is all about embedding a culture of compliance into your DNA. It should touch every part of your operation, from daily transaction monitoring to your long-term strategic planning.

Your Top Questions About Stablecoin Regulation, Answered

The world of stablecoin rules can feel like a maze, with new laws popping up from all corners of the globe. Let's cut through the complexity and tackle the most common questions head-on. Here’s what you really need to know about the practical impact on users, developers, and the future of digital money.

What's The Real Difference Between EU and US Stablecoin Laws?

The biggest divide between Europe's MiCA and the proposed laws in the US really comes down to their core approach. Imagine building a house: the EU has a single, comprehensive blueprint for the entire continent, while the US is letting different builders work from various drafts, hoping they all connect in the end.

The EU’s Markets in Crypto-Assets (MiCA) regulation is a sweeping, all-in-one legislative package for its 27 member states. It creates a level playing field by giving clear definitions for things like E-Money Tokens (aka fiat-backed stablecoins) and setting one uniform set of rules for everyone. This "one-stop-shop" model delivers a ton of legal certainty.

America, on the other hand, is taking a much more piecemeal approach that's still being hammered out. Bills like the Clarity for Payment Stablecoins Act are hyper-focused on payment stablecoins, but the bigger debate is about who's in charge. Will it be the Federal Reserve? The OCC? State-level regulators? It’s still up in the air.

The US is almost certainly headed for a multi-layered system. This means both banks and non-bank companies could issue stablecoins, but they’d operate under different supervisors. It creates a much more complicated compliance map than the EU's streamlined, single-market model.

So, what does this mean in practice? A stablecoin issuer in Europe can follow one clear rulebook to access the entire bloc. In the US, that same issuer has to navigate a tangled web of state regulations and brace for whatever federal rules eventually come down the pike.

How Will These Rules Actually Affect Me as a Crypto User?

For the average crypto user, new stablecoin regulations are a classic double-edged sword. You're getting some big benefits, but they come with real trade-offs.

On the bright side, things are about to get a whole lot safer. When you use a regulated stablecoin, you’ll know it’s fully backed by high-quality, audited reserves. This drastically cuts the risk of a catastrophic de-pegging event like we’ve seen in the past. That kind of security could make crypto a much more appealing option for everyday things like savings, payments, and sending money abroad, which could drive a new wave of adoption.

But here’s the other side of the coin: regulation will almost certainly chip away at the privacy and permissionless feel that early crypto adopters loved. To play by the new global rules, stablecoin issuers will have to enforce strict Anti-Money Laundering (AML) and Know Your Customer (KYC) procedures.

Here’s what that looks like for you:

- Identity Checks: Say goodbye to anonymous transactions. You’ll almost certainly need to verify your identity to get or redeem stablecoins directly from an issuer.

- More Centralization: Relying on regulated companies adds central points of control—and potential failure. It’s a direct contradiction to the decentralized ethos crypto was built on.

- Transaction Monitoring: Just like in the traditional banking world, all your transactions will be watched for suspicious activity.

The bottom line is a safer but more controlled environment. Stablecoins are moving closer to feeling like the digital money you already use and further away from their wild, unregulated roots.

Can Algorithmic Stablecoins Even Survive in a Regulated World?

Honestly, the future looks pretty grim for purely algorithmic stablecoins. The spectacular implosion of projects like Terra/UST has left regulators everywhere deeply skeptical of any model that isn't backed by cold, hard assets.

Take the EU's MiCA framework. It sets the bar for reserves and stabilization so high that a purely algorithmic stablecoin—one that just uses code and market dynamics to hold its value—would find it impossible to comply. The rules are written to approve only those models that can guarantee you can redeem your stablecoin for its face value at any time. An algorithm alone just can't make that promise credibly.

It's the same story in the US. Proposed laws are all focused on asset-backed models. The core principle is simple: for every digital dollar out there, there needs to be a real dollar or an equivalent safe asset locked away in a vault somewhere.

This doesn't mean the idea is dead forever, but its survival depends on a serious reinvention:

- Hybrid Models: We might see stablecoins that use algorithms for small price corrections but are mostly over-collateralized with other crypto assets. They might find a narrow path to compliance if they can prove they are rock-solid.

- DeFi Niches: Unregulated "algos" will probably stick around in the more experimental, high-risk corners of DeFi and in places with looser regulations.

But their time in the mainstream spotlight is likely over. The regulatory consensus is crystal clear: if it wants to be treated like money, it needs to be backed like money.

At Stablecoin Insider, we provide the essential news and analysis you need to stay ahead in the dynamic world of digital assets. Our experts cut through the noise to deliver clear insights on regulation, technology, and market trends.

Explore our in-depth articles and reports at Stablecoin Insider

{kind=link}