Table of Contents

Think of stablecoin interest rates as the crypto world's answer to a high-yield savings account. You're earning a return on digital assets designed to hold a steady value, like the U.S. dollar, but often at a pace that leaves traditional bank rates in the dust.

What Are Stablecoin Interest Rates and How Do They Work

The idea is surprisingly familiar. Just like when you deposit money in a bank, you're essentially letting someone else use your capital. With stablecoins, you’re lending your digital dollars to borrowers through a crypto platform or a decentralized protocol.

These borrowers—maybe traders needing leverage or institutions executing complex strategies—pay a fee for the loan. The platform you use takes a cut, and the rest comes back to you as interest, or what the crypto world calls "yield." It’s the same basic principle of lending and borrowing, just running on different rails.

The Core Promise: Digital Dollars That Work for You

What makes this so compelling is the "stable" part of stablecoin. Unlike Bitcoin or Ethereum, these assets are built to maintain a consistent $1 peg. This design sidesteps the wild price swings that keep many people on the sidelines of crypto. We cover the nuts and bolts of this in our guide on how stablecoins work.

This blend of stability with the potential for high returns is what makes them so attractive. You can tap into the earning power of the crypto economy without taking on the price risk of more volatile assets.

The key benefits really boil down to:

- Higher Potential Yields: It's not uncommon to find rates that significantly outperform what you’d get from a traditional savings account or even government bonds.

- Accessibility: If you have an internet connection, you can participate. This opens up financial opportunities that were once limited by geography or institutional gatekeepers.

- Passive Income: It’s a straightforward way to put your assets to work, earning returns without you having to actively trade or manage them.

The concept is simple yet powerful: your digital dollars, which are designed to hold their value, can be put to work to earn more digital dollars. This bridges the gap between the stability of traditional currency and the earning potential of the digital asset world.

In the end, stablecoin interest rates sit at the crossroads of old and new finance. They take a time-tested concept—earning interest on your savings—and plug it into a modern, digital, and often far more efficient financial system. This creates a whole new set of possibilities for everyday savers and sophisticated investors alike.

Where Does Your Stablecoin Yield Actually Come From?

When you see the high interest rates offered on stablecoins, especially compared to a traditional savings account, it's natural to wonder, "Is this for real?" The short answer is yes, but it’s not magic. That yield is generated by real economic activity happening across the crypto world.

To really understand the opportunity—and the risks—you need to peek under the hood and see what’s powering these returns. Let's break down the four main engines that turn your stablecoins into a yield-generating asset.

Lending and Borrowing Markets

The most straightforward source of yield is from simple lending. Think of it as a peer-to-peer bank built on the blockchain. When you deposit your stablecoins into a protocol like Aave or Compound, you're adding your money to a large pool of capital.

So, who's borrowing from this pool?

- Traders who need capital to leverage their bets.

- Institutions running complex arbitrage strategies between different markets.

- Crypto projects that need operating cash but don't want to sell their own tokens.

These borrowers pay interest on their loans, and the rates are set by pure supply and demand. When lots of people want to borrow stablecoins and there isn't enough to go around, rates go up. A slice of that interest gets paid directly to you for providing the liquidity. You're effectively playing the role of the bank, and the yield is your payment.

Providing Liquidity on Decentralized Exchanges

Another huge source of yield comes from being a liquidity provider (LP) on a decentralized exchange (DEX) like Uniswap or Curve. A DEX is just an automated currency exchange, but instead of a central company matching buyers and sellers, it uses "liquidity pools" to get the job done.

For any of this to work, these pools need assets. A USDC/ETH pool, for instance, needs a healthy stash of both USDC and Ethereum for traders to swap between. By depositing your stablecoins into one side of a pool, you become an LP.

Every time someone makes a trade using that pool, they pay a small fee—often around 0.3%. That fee is then split among all the LPs in the pool. So, your yield is coming directly from the trading volume on the platform. The more trades, the more fees, and the more you earn.

At its core, yield from liquidity provision is a reward for facilitating commerce. You are providing the necessary inventory for an automated market, and in return, you receive a cut of the transaction revenue generated by that market.

Staking Mechanisms and Rewards

Staking is usually associated with assets like Ethereum, but it plays a role in the stablecoin world, too. Here, staking isn't about validating transactions but about locking up your stablecoins to support a protocol's security or stability.

For example, some algorithmic stablecoins rely on users staking assets to help defend the peg or participate in governance. As a thank you for locking up your funds and taking on that responsibility, the protocol rewards you with more tokens. It’s less about lending and more about being an active, trusted participant in a specific ecosystem.

Protocol Incentives and Token Rewards

Finally, a big reason you see eye-popping APYs is because of protocol incentives. New DeFi platforms need to attract users and capital to survive, and one of the best ways to do that is to give away free money—or rather, free tokens.

These platforms often distribute their own native governance tokens to anyone who lends, borrows, or provides liquidity. A new lending protocol might offer its own token as an extra reward on top of the interest paid by borrowers.

This strategy, famously known as "yield farming," can juice returns to incredible levels. But it’s crucial to know that this part of your yield is temporary and its value is tied to the market price of the reward token, which can swing wildly. Think of it as a customer acquisition cost for the protocol. To get a better sense of the economics, you can learn more about how stablecoin projects generate revenue to fund these kinds of programs.

By understanding these four pillars—lending, liquidity, staking, and incentives—you can look at any advertised interest rate and know exactly what you're getting into. You can see where the return is really coming from, judge how sustainable it is, and make smarter choices about where to put your digital dollars to work.

Comparing CeFi and DeFi Stablecoin Yield Platforms

So, you're ready to put your stablecoins to work and earn some interest. The first big decision you'll face is where to do it. This isn't just about picking a platform; it's about choosing between two entirely different financial universes: Centralized Finance (CeFi) and Decentralized Finance (DeFi).

Think of it as choosing between a traditional bank and a fully automated, transparent financial co-op. Each has its own rules, risks, and rewards when it comes to generating those stablecoin yields.

The CeFi Route: Convenience and Custody

CeFi platforms like Nexo or Ledn feel familiar. They operate a lot like a digital brokerage or a high-yield savings account. You sign up, verify your identity (a process known as KYC), and deposit your stablecoins. That’s it.

From there, the company takes over. They lend out your funds to borrowers, manage all the complex backend operations, and pay you a stated interest rate. The big draw here is simplicity. It's a polished, user-friendly experience designed for anyone to use.

But this convenience comes with a crucial trade-off: you're handing over custody of your assets. You are placing your trust in the company to keep your funds safe, which introduces counterparty risk—the risk that the platform itself could fail.

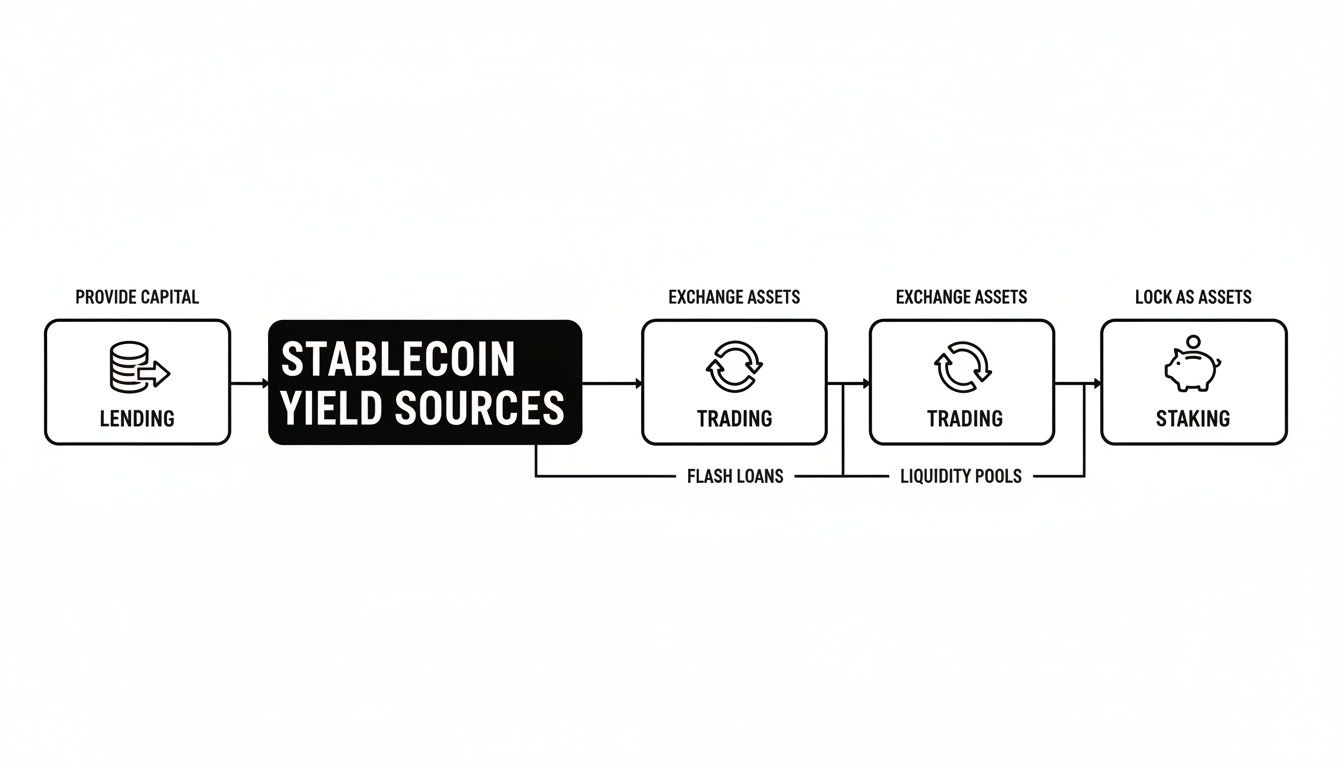

This flowchart breaks down the core economic activities that generate yield, whether you're using a CeFi or DeFi platform.

As you can see, the money-making mechanics like lending and providing liquidity are fundamentally the same. The real difference is who is in control.

The DeFi Approach: Self-Custody and Transparency

DeFi flips the traditional model on its head. Instead of relying on a company, you interact directly with software—specifically, open-source protocols built on a blockchain. Platforms like Aave and Compound are essentially automated lending pools run by code.

With DeFi, you never give up control of your funds. You connect your own crypto wallet and your assets stay under your private keys. This is what we call self-custody. Every rule, transaction, and interest rate calculation is public and verifiable on the blockchain.

The interest rates in DeFi aren't set by a committee; they are dynamic, adjusting in real-time based on the simple laws of supply and demand within the lending pool. More borrowers mean higher rates for lenders, and vice-versa.

Of course, this power comes with responsibility. You need to manage your own wallet securely and understand the basics of interacting with smart contracts. If you want to get into the nuts and bolts, our complete guide to stablecoin lending breaks down these processes in detail.

A Head-to-Head Comparison

Choosing between CeFi and DeFi is a personal decision, shaped by your technical comfort, risk tolerance, and how much control you want over your money.

The core distinction is simple: in CeFi, you trust people and a company. In DeFi, you trust code.

Let's put them side-by-side to see how they really stack up.

CeFi vs DeFi Stablecoin Lending: A Comparison

This table lays out the key differences between earning yield through a centralized service versus a decentralized protocol.

| Feature | CeFi (e.g., Nexo, Ledn) | DeFi (e.g., Aave, Compound) |

|---|---|---|

| Custody | The platform holds your funds (custodial). You trust them to keep your assets safe. | You hold your own funds in a personal wallet (self-custody). You have full control. |

| Transparency | Operations are often a "black box." You rely on the company's audits and reports. | All rules and transactions are public and verifiable on the blockchain. Radically transparent. |

| User Experience | Simple and intuitive, similar to using a traditional online bank. | Steeper learning curve. Requires managing a crypto wallet and understanding gas fees. |

| Interest Rates | Often fixed or announced in advance. Can be more stable but may be lower. | Highly variable, changing block-by-block based on market supply and demand. |

| Primary Risks | Counterparty Risk: The platform could go bankrupt, freeze funds, or be hacked. | Smart Contract Risk: A bug or exploit in the protocol's code could lead to loss of funds. |

| Accessibility | Requires personal identification (KYC/AML), restricting access in some regions. | Open and permissionless. Anyone with a wallet and internet can access it. |

Ultimately, there's no single "best" answer. CeFi provides a fantastic on-ramp for those who value simplicity and are comfortable trusting a third party. DeFi, on the other hand, appeals to those who prioritize financial sovereignty and transparency, even if it means a bit more of a learning curve. Understanding this fundamental divide is the first step toward building a smart stablecoin yield strategy.

Why Do Stablecoin Interest Rates Change So Much?

If you're new to crypto, one of the first things you'll notice is that stablecoin interest rates are anything but stable. Unlike a traditional bank's Certificate of Deposit (CD) that locks in a rate for months or years, the yield you earn on your stablecoins can change daily, sometimes even hourly.

This isn't random. Understanding what makes these rates so dynamic is the key to setting realistic expectations and making smarter decisions with your money. At its core, it all comes down to a classic economic principle: supply and demand.

The Core Engine: Supply and Demand

Think of a lending platform like Aave or Compound as a giant, shared pool of capital. Lenders add their stablecoins to the pool, and borrowers take them out. The interest rate is simply the "price" for borrowing from that pool.

When Demand to Borrow is High: During a bull market, traders are hungry for capital. They want to borrow stablecoins to leverage their trades, betting on prices going up. As they pull more funds from the pool, the available supply shrinks. To attract more deposits and slow down the borrowing, the protocol automatically jacks up the interest rate.

When Supply of Lenders is High: On the other hand, when the market is quiet or bearish, everyone is looking for a safe place to park their cash. Lenders flood the pool with stablecoins, but very few people want to borrow. With a massive surplus of capital just sitting there, the protocol lowers the rate to make borrowing more attractive.

This mechanism is governed by what DeFi protocols call the utilization rate—the percentage of total funds being borrowed. High utilization means high demand, which pushes rates up. Low utilization means a surplus of capital, which brings rates down.

The interest rate you see is a live signal from the market. A high rate tells you capital is in high demand right now. A low rate means there's plenty of cash on the sidelines with few takers.

Riding the Crypto Market Waves

The overall mood of the crypto market is the single biggest driver of these supply and demand shifts. Stablecoin interest rates essentially act as a thermometer for market sentiment.

During a bull market, the excitement is palpable. Traders are scrambling to borrow stablecoins to:

- Leverage up: A trader might borrow USDC to buy even more ETH, amplifying their potential gains.

- Chase new opportunities: They need capital to jump into the latest token launches or other high-risk, high-reward plays.

This frenzy for borrowing creates a huge demand for stablecoins, sending interest rates soaring, often into the double digits.

Conversely, when a bear market hits, fear takes over. Traders close their leveraged positions, borrowing demand evaporates, and everyone rushes to the safety of stablecoins. This mix of low demand and high supply crushes interest rates, sometimes pushing them down to just a few percent. You can see these cycles play out in historical data, and we dive deeper into these trends in our latest analysis of stablecoin stats for Q4 2025.

Protocol Incentives and the Yield Farming Game

Another huge factor, especially in DeFi, is protocol incentives. To get off the ground, new platforms need liquidity. To attract it, they'll often offer bonus rewards on top of the natural interest rate.

These incentives are usually paid in the platform's own governance token, a practice known as "yield farming." This can temporarily inflate the APY to eye-watering levels. But these sweet deals don't last forever. Once the protocol attracts enough users or its marketing budget shrinks, those extra rewards get dialed back or cut off completely, and the APY can plummet overnight.

The Growing Connection to Traditional Finance

Finally, the crypto market isn't an island. What happens in traditional finance, or "TradFi," is starting to have a much bigger impact on stablecoin rates. The clearest connection is through the Federal Reserve's interest rate policies.

Many major stablecoins are backed by real-world assets like U.S. Treasury bills. When the Fed raises interest rates, the yield on these T-bills goes up. This means the stablecoin issuers are earning more on their reserves. Some of that extra profit can be passed on to users, particularly on centralized platforms. While the link isn't always one-to-one, the "risk-free rate" set by government bonds provides a floor that influences yields across the entire financial system—both old and new.

Navigating the Key Risks of Stablecoin Yield Farming

Those high stablecoin interest rates look tempting, don't they? But before you jump in, it’s critical to remember a foundational rule of finance: higher returns always come with higher risk. Chasing the biggest APY without a solid grasp of the potential pitfalls is a surefire way to get burned.

A smart investor doesn't ignore the downside; they study it. The risks in this space aren't just theoretical—they've already cost users billions of dollars. By understanding exactly what can go wrong, you can start making smarter decisions that balance your hunt for yield with the need to protect your capital.

Smart Contract and Protocol Risk

When you use a DeFi platform, you're not depositing money into a bank. Instead, your funds are locked into a smart contract, which is essentially just code running on a blockchain. The biggest risk here is a simple but devastating one: what if there's a bug or a vulnerability in that code?

Think of a smart contract as an automated vault. If there’s a flaw in its design, a clever hacker can exploit it and drain the funds. Because blockchain transactions are irreversible, once that money is gone, it's usually gone for good. We've seen hundreds of millions of dollars vanish in DeFi hacks, making this one of the most immediate threats you'll face.

- Code Exploits: A hacker finds a bug in the protocol's code and uses it to steal locked funds.

- Economic Exploits: An attacker manipulates market conditions, maybe using flash loans, to trick the protocol into mispricing assets and allowing them to drain value.

Before you ever deposit a single dollar, check to see if the protocol has been audited by multiple reputable security firms. It’s not a foolproof guarantee, but it’s a non-negotiable first step.

Counterparty and Centralization Risk

While DeFi is all about trusting code, CeFi platforms force you to trust a company. This is where counterparty risk comes into play—the very real danger that the platform holding your funds could go bankrupt.

This risk hit home for countless users during the collapses of firms like Celsius and BlockFi. When they went under, customer assets were frozen and dragged into drawn-out bankruptcy proceedings. In CeFi, the company holds the keys, and if they mismanage their business, your money is at their mercy.

The core difference is where you place your trust. In DeFi, you trust the code to be secure. In CeFi, you trust the company and its leadership to be solvent and act ethically.

De-Peg and Stablecoin Stability Risk

The whole idea of earning stablecoin interest hinges on one crucial assumption: that your stablecoin will stay pegged to $1. But not all stablecoins are built the same, and some are much more fragile than others. A de-peg event, where a stablecoin breaks its dollar value, can vaporize both your principal and any yield you've earned.

The most infamous example was the 2022 collapse of TerraUSD (UST). This algorithmic stablecoin entered a "death spiral," losing almost all its value in just a few days. For a deeper dive into what makes stablecoins tick—and what makes them fail—you can explore more about stablecoin risks.

Liquidity and Regulatory Risk

Finally, there are two big-picture risks that are tied to the market as a whole. Liquidity risk is what happens when everyone rushes for the exit at once. If too many users try to withdraw their funds from a protocol during a panic, there might not be enough liquid assets to pay everyone out, leaving you stuck.

Meanwhile, regulatory risk hangs over the entire crypto industry. Governments around the world are still figuring out how they want to handle stablecoins and DeFi. A sudden new law or an enforcement action against a major platform could instantly change the rules of the game, impacting rates and the safety of your assets. Applying general portfolio risk management principles is a good start, but understanding these crypto-native risks is essential.

How to Properly Evaluate Stablecoin Yield Opportunities

Chasing the highest advertised stablecoin interest rate is a rookie mistake. A massive yield can often be a warning sign, not a golden opportunity. To do this right, you have to think like a detective—looking beyond the flashy numbers to understand where the return actually comes from and what risks are hiding under the surface.

The first step is learning to speak the language of yield. You'll constantly see two terms thrown around: Annual Percentage Rate (APR) and Annual Percentage Yield (APY). They sound alike, but the difference is key to knowing what you’ll really earn.

Understanding APR vs APY

Think of APR as simple interest. It’s the flat rate you earn over a year, without any bells or whistles. If you deposit $1,000 at a 10% APR, you’ll walk away with $1,100 after one year. Clean and simple.

APY, on the other hand, factors in the magic of compounding—earning interest on your interest. If that same 10% is compounded daily, your earnings get added to your principal every day. The next day, you earn interest on a slightly bigger pile of money. Over time, that small effect adds up.

Always compare apples to apples. A 9.8% APY is actually a better deal than a 10% APR that pays out only once a year. The compounding built into the APY will leave you with more money in the end.

Looking Beyond the Advertised Rate

A high APY gets your attention, but it's just the headline. The real story is in the long-term safety of the platform and the stablecoin itself. A disciplined approach means running a few critical checks before you even think about depositing.

Protocol Security Audits: Never put money into a DeFi protocol without first checking for security audits from reputable firms like Trail of Bits or OpenZeppelin. Audits are like a home inspection for the protocol's code, sniffing out bugs and vulnerabilities. No audits? That’s a giant red flag.

Total Value Locked (TVL): TVL shows you how much money other users have trusted a protocol with. It's not a perfect measure of safety, but a high and stable TVL (we’re talking billions) usually points to a platform that has earned the market's confidence. Watch out for sudden drops in TVL, as they can signal trouble.

The Stablecoin's Track Record: Not all stablecoins are built the same. You have to size up the risk of the asset you're holding. Is it a heavily-backed coin like USDC, or is it a riskier algorithmic stablecoin? Dig into its history. Has it ever de-pegged? How open are they about their reserves?

For example, take a look at the market data for a major stablecoin like USDT.

This chart shows a massive and consistent market cap, which tells you it has widespread adoption and a history of maintaining its peg. That kind of stability is a crucial piece of your risk assessment.

Tools like DeFi Llama or CoinGecko are great for scanning and comparing interest rates across dozens of platforms. But they're just the starting point. They show you the "what" (the rates), but it's your job to dig in and find out the "why" and "how"—the security, stability, and sustainability behind each number before you commit your capital.

Frequently Asked Questions About Stablecoin Rates

Diving into stablecoin yields always sparks a few questions. Whether you're just getting started or you're a seasoned yield farmer, getting clear answers is key to making smarter moves. Let's tackle some of the most common ones.

What Is a Realistic Stablecoin Interest Rate?

A "realistic" rate is really just a reflection of the current market. When the crypto market is booming, demand to borrow stablecoins skyrockets, and it's not uncommon to see yields of 10% or even higher. But when the market cools off, that demand evaporates, and rates can easily drop to the 1-3% range.

Think of it this way: if a rate looks too good to be true, it probably is. Those eye-popping APYs—especially anything north of 20%—are almost always fueled by temporary token rewards, not genuine economic activity. They’re designed to attract users quickly but rarely last.

A sustainable yield is one you can actually explain. If you can trace the interest back to real borrowers on a reputable platform, it’s a much better sign than a mystery rate propped up by a short-lived token promotion.

How Often Do Rates Change?

Constantly. Stablecoin interest rates are anything but static.

- In DeFi, rates are alive. They can literally change every few seconds, automatically adjusting with each new block on the blockchain based on the real-time push and pull of supply and demand.

- In CeFi, things are a bit more predictable. Companies typically adjust their rates on a set schedule, maybe daily, weekly, or monthly, based on their own internal decisions.

This constant movement is completely normal. Don't expect your rate to be locked in like a bank CD; it's a living number that breathes with the market.

Are Stablecoin Earnings Taxable?

Yes, absolutely. In most parts of the world, the interest you earn from stablecoins is treated as taxable income. While the rules can differ from one country to another, it's usually taxed in a similar way to interest from a bank account or as capital gains.

It's crucial to keep meticulous records of all your earnings. I can't stress this enough: talk to a tax professional who actually understands crypto in your specific jurisdiction. Staying on top of your reporting is the only way to stay compliant and avoid headaches later.

Here at Stablecoin Insider, our goal is to give you the news and deep-dive analysis you need to confidently navigate the world of digital finance. To stay ahead of the curve, check out the latest at Stablecoin Insider.

{kind=link}