Table of Contents

Stablecoins carved out a quiet victory in the first three months of 2026.

While the broader cryptocurrency market shed more than 20 percent of its value, the sector’s total market cap climbed to a record $315 billion.

That represented a net addition of roughly 8 billion, the slowest quarterly expansion since late 2023, yet it underscored stablecoins’ growing role as a defensive asset class.

USDC narrowed the gap with market leader USDT, yield-bearing products powered most of the fresh capital, and on-chain volumes exploded even as retail participation cooled.

The quarter also saw regulators take concrete steps toward implementing the GENIUS Act, providing long-awaited clarity that could accelerate institutional adoption.

- Total supply hit $315 billion by March 31.

- Stablecoins captured 75 percent of all crypto trading volume.

- Yield-bearing assets drove over half of net growth.

- Bots accounted for approximately 76% of all stablecoin transaction volume in Q1, the highest level in two years.

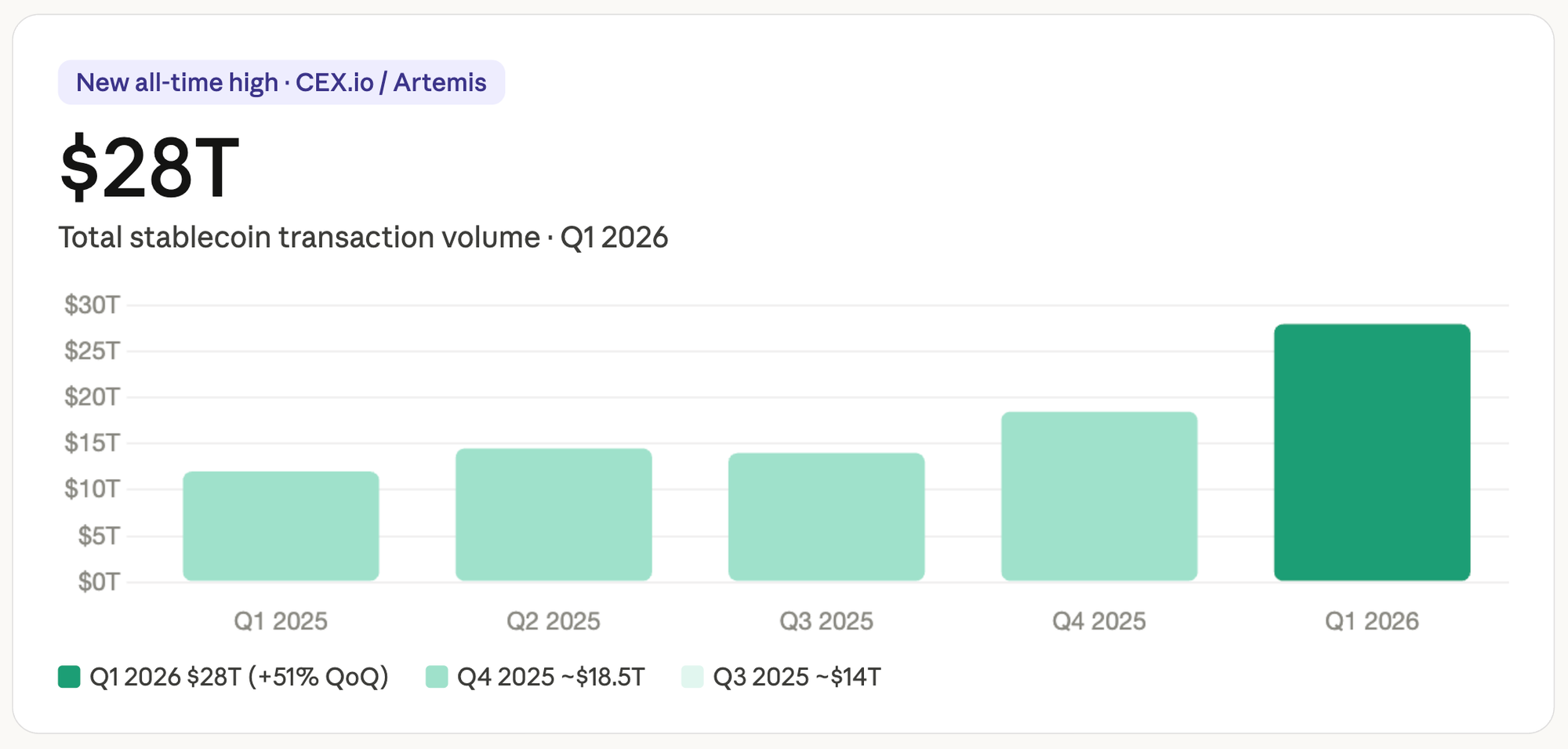

- Total stablecoin transaction volume hit $28 trillion in Q1, a 51% increase quarter-over-quarter and a new all-time high.

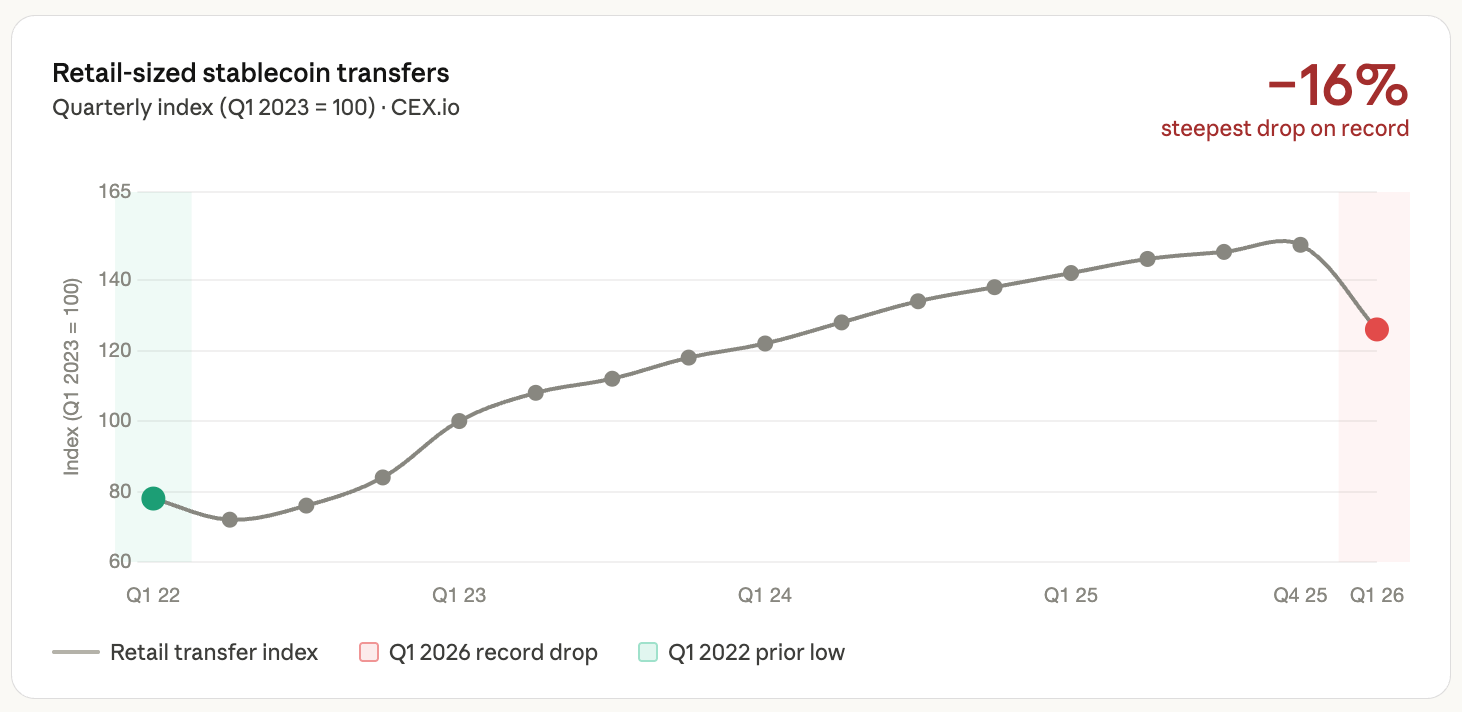

- Retail-sized transfers declined 16% in Q1, the steepest single-quarter drop on record

- USDT posted its first quarterly decline since 2022.

Market Performance and Supply Breakdown

Issuers navigated a risk-off environment with surprising steadiness. Aggregate supply expanded modestly, but the composition of that growth revealed clear shifts in investor preference.

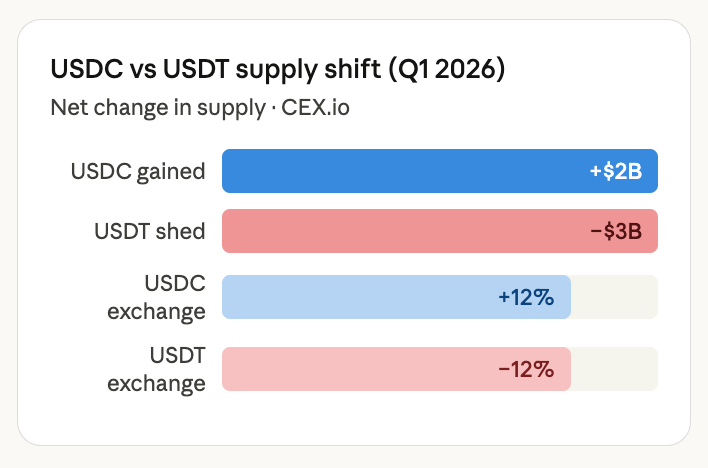

Tether’s USDT supply contracted by approximately $3 billion to roughly $184 billion, marking its first quarterly drop since Q2 2022 and reflecting heavy redemptions on Ethereum.

Circle’s USDC, by contrast, added about 2 billion to reach roughly $78 billion, buoyed by institutional flows and preference for regulated assets.

The divergence was not merely numerical. On Ethereum alone, USDT saw more than 7 billion in net outflows, while USDC and newer yield products absorbed much of the rotation.

Tron continued its role as the payments powerhouse, adding over 4 billion, almost entirely in USDT. Smaller ecosystems such as Solana posted the largest absolute gains among non-Ethereum chains, exceeding 1.6 billion.

- USDT dominance slipped to 58 percent.

- USDC exchange reserves rose 12 percent while USDT reserves fell 12 percent.

- Stablecoin share of total crypto market cap climbed from 9 percent to 13 percent.

- Newer entrants like USD1 and protocol-native tokens gained traction on high-growth chains.

Transaction Volumes and On-Chain Activity

Raw supply growth masked explosive utility.

Total stablecoin transaction volume surpassed 28 trillion, a 51 percent jump from the previous quarter.

Within that figure, pure trading volume reached 8.3 trillion and accounted for a record 75 percent of all crypto trades.

Adjusted real transfers, stripping out obvious internal and bot-driven noise, still exceeded 21.5 trillion, signaling genuine economic activity across payments, settlements, and DeFi.

The composition of that activity told two parallel stories. Retail-sized transfers below $250 fell 16 percent, the steepest decline on record, reflecting caution among individual users.

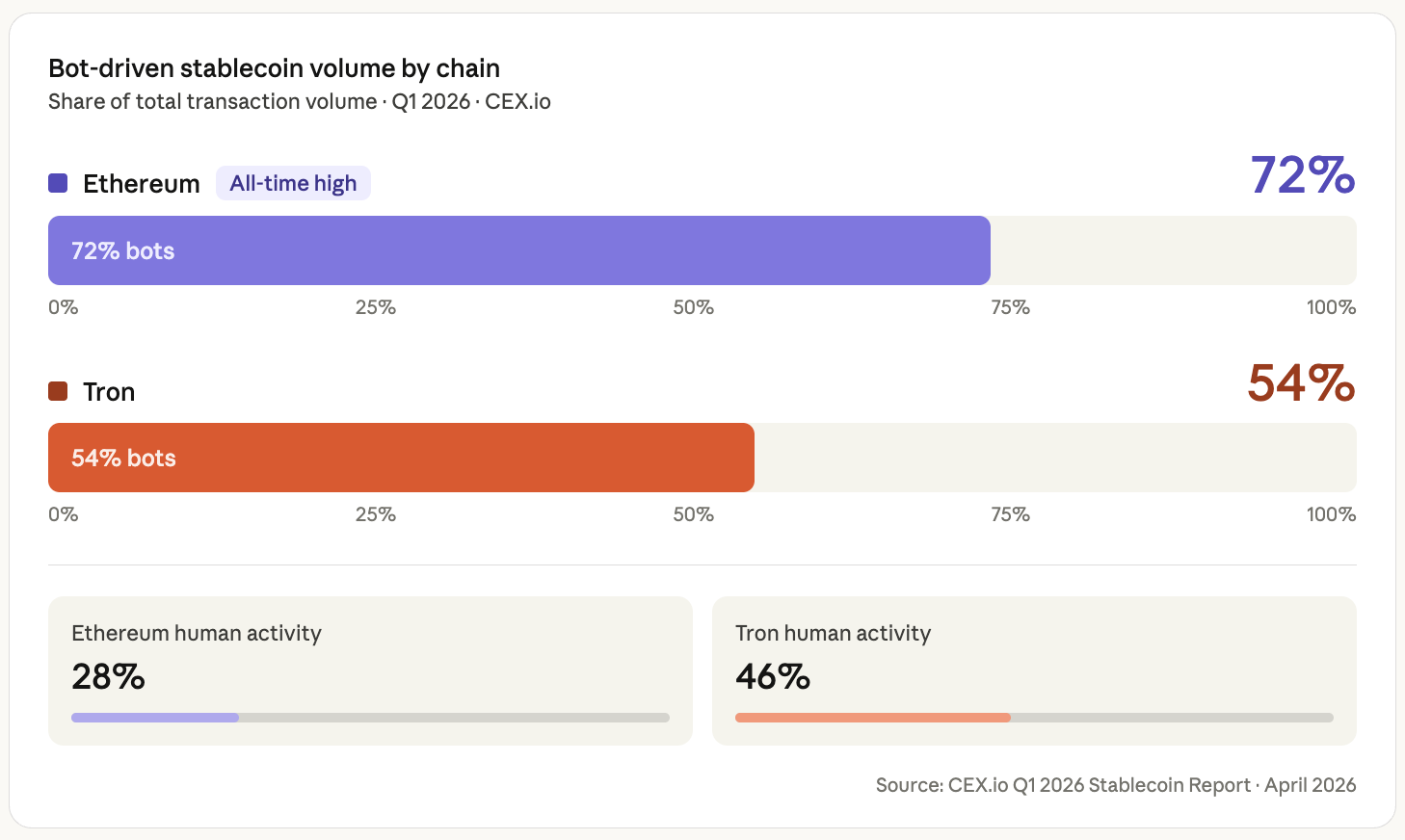

Meanwhile, automated strategies and arbitrage bots pushed their share of volume to 76 percent, up from 70 percent the prior quarter. USDC captured roughly 80 percent of organic volume for the first time since 2019, overtaking USDT in that metric.

- Ethereum bot activity reached an all-time high of 72 percent.

- Tron bot activity hit 54 percent.

- USDC organic volume grew 59 percent quarter-over-quarter.

- Cross-border and B2B use cases continued expanding quietly on Solana and Base.

The Rise of Yield-Bearing Stablecoins

Perhaps the quarter’s most telling development was the breakout performance of yield-bearing products.

In an environment of elevated short-term interest rates and sideways crypto prices, users demanded returns on idle capital.

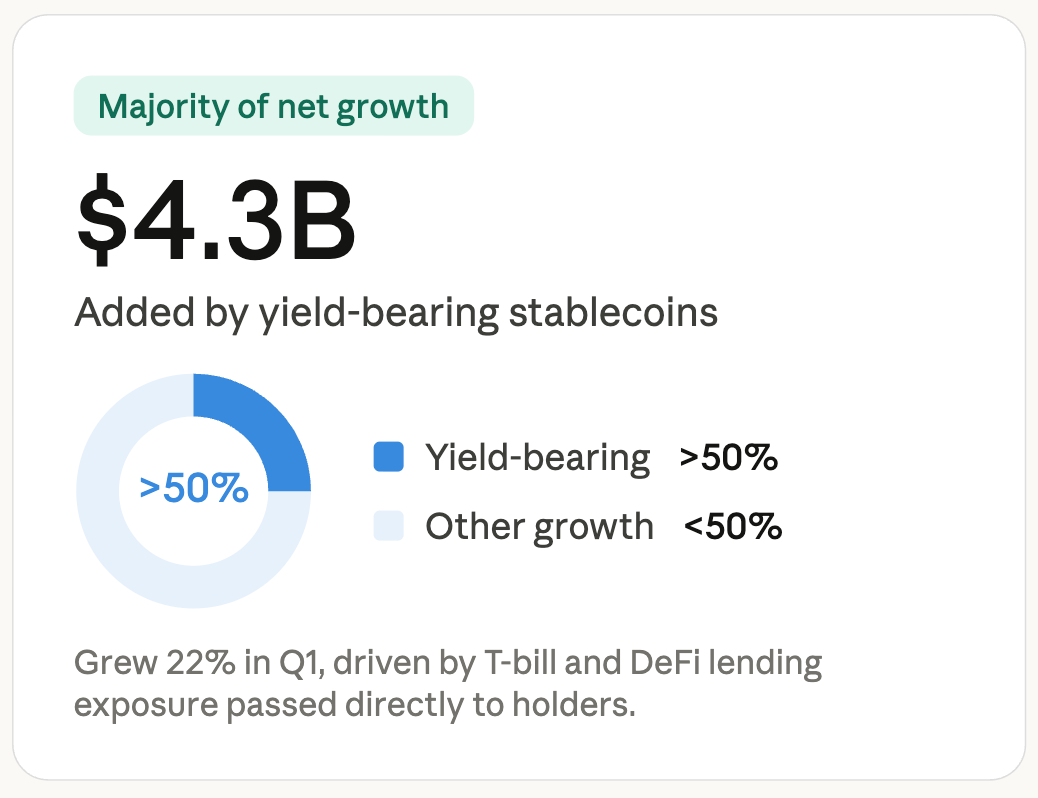

Yield-focused stablecoins expanded by 22 percent category-wide and contributed more than half the sector’s net supply growth, adding roughly 4.3 billion in market capitalization.

Sky’s sUSDS alone brought in more than 2.5 billion, more new capital than the next four yield-bearing tokens combined. Ethena’s USDe, USDY, and protocol-native options like USD1 also posted double-digit gains. These products blended DeFi-native yields with traditional fixed-income exposure, appealing to both sophisticated traders and conservative institutions wary of pure speculation.

- USDY market cap surged 150 percent in the quarter.

- Yield products now represent a structural rather than cyclical feature of the market.

- Average on-chain yields tracked closely with Treasury bills while offering programmability advantages.

- New risks around smart-contract vulnerabilities and basis drift accompanied the growth.

Regulatory Developments: CLARITY Stalls, but GENIUS Enters Implementation

The GENIUS Act, signed into law in July 2025, saw its first major rulemaking proposals land in Q1.

The Office of the Comptroller of the Currency issued a notice of proposed rulemaking on February 25 that outlined licensing, reserve requirements, and safety-and-soundness standards for federally regulated issuers.

Treasury followed with guidance on state-level oversight for smaller players under $10 billion in market cap.

A separate Clarity Act provision under discussion would restrict yield payments on centralized-exchange balances, potentially reshaping deposit economics. Comment periods remain open, with final rules targeted for July 2026.

Market participants broadly welcomed the clarity, viewing it as a tailwind for compliant issuers like Circle while forcing Tether to adapt to heightened scrutiny.

- OCC proposal addresses reserve assets and redemption mechanics.

- Treasury NPRM focuses on smaller issuers.

- Effective date likely falls in late 2026 or early 2027.

- Global alignment with MiCA in Europe added to the sense of regulatory convergence.

Adoption Trends and Persistent Challenges

Institutional interest deepened even as retail stepped back. Mastercard’s earlier acquisition of BVNK and growing corporate treasury experiments pointed to stablecoins becoming infrastructure rather than speculation vehicles.

Payments volume on Tron and Solana continued climbing, while Ethereum’s rotation toward regulated assets signaled maturing preferences. Yet risks remain. Heavy bot dominance raises questions about sustainable organic demand. Yield products introduce novel smart-contract and de-pegging hazards.

USDT’s continued reliance on offshore structures could create friction under tightening U.S. rules. And the modest supply growth itself hints that broader crypto recovery may be needed before the next leg of stablecoin expansion.

- Retail transfers posted the largest historical drop.

- Institutional custody and exchange reserves tilted toward USDC.

- No major de-pegs or hacks occurred in Q1 itself.

- Velocity metrics suggest higher utility per dollar in circulation.

What's Expected in Q2?

Q2 2026 appears poised for acceleration if macro conditions stabilize.

Further GENIUS Act finalization, potential yield-policy decisions, and any crypto-market rebound could unlock fresh inflows.

Analysts expect continued divergence: USDT retains payments dominance in emerging markets, while USDC and yield-bearing tokens capture institutional and DeFi mindshare. Transaction volumes are likely to keep outpacing supply growth, reinforcing stablecoins’ transition from on-ramp to core financial plumbing.

The sector enters its second decade with record liquidity, regulatory scaffolding, and proven utility. Whether 2026 echoes the slow grind of 2022 or delivers a sharper inflection will depend on the interplay of policy, yields, and broader risk appetite.

For now, the data from Q1 paints a picture of quiet maturation rather than hype-driven expansion.

Related Reports

Partner/Advertise with Stablecoin Insider

Fill out this form to partner and advertise on the only publication, dedicated entirely to the Stablecoin ecosystem.

See you next week,

- The Stablecoin Insider team

{kind=link}