Table of Contents

Mastercard stablecoin pay is not one product. It’s a three-layer payments stack that (1) lets consumers spend stablecoins through familiar checkout rails, (2) increasingly enables parts of the acquiring ecosystem to settle in stablecoins, and (3) supports payouts to stablecoin wallets as a mainstream money-movement option.

Mastercard framed this directly as end-to-end stablecoin capabilities from wallets to checkouts, built with partners to make stablecoins usable anytime, anywhere.

The timing matters. Stablecoins are now large enough, and active enough to force serious integration decisions across the payments stack:

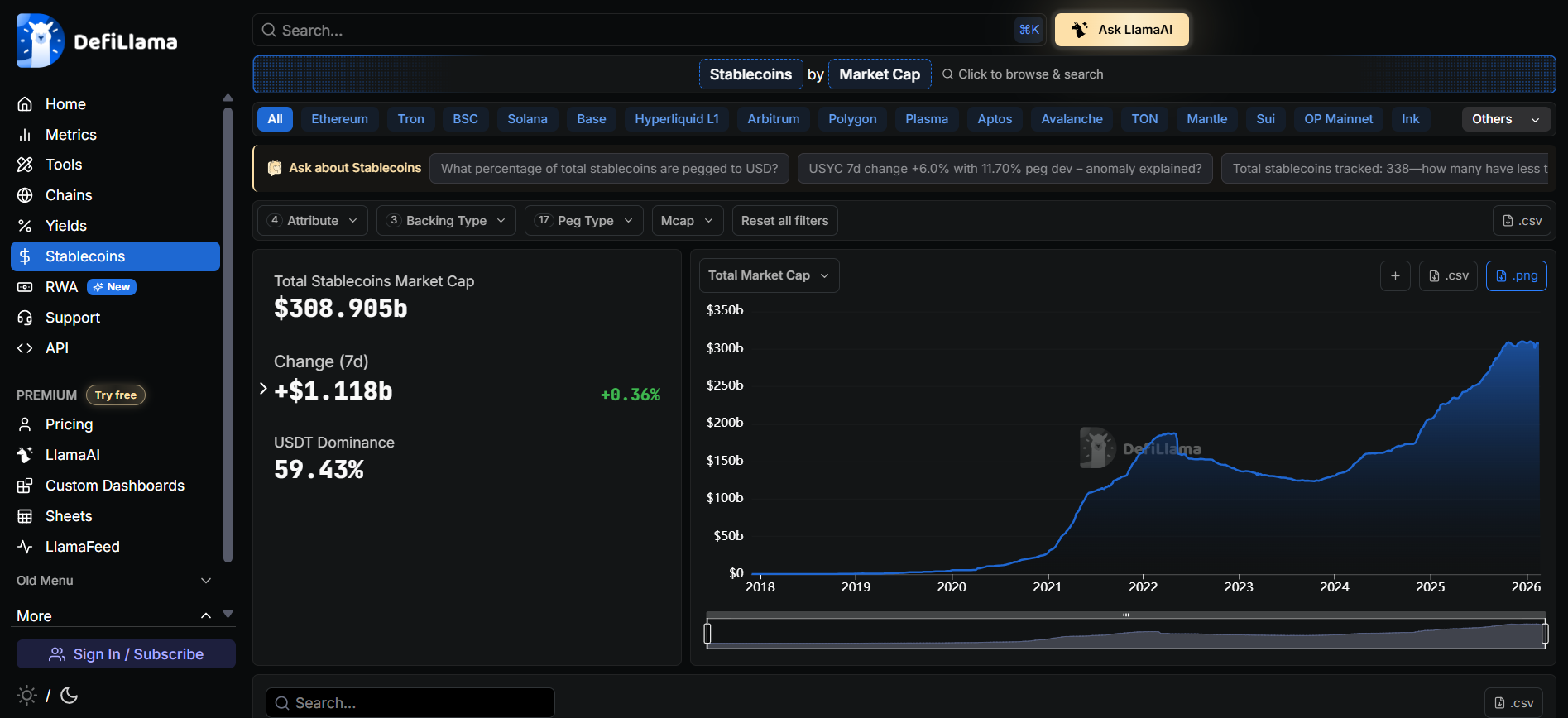

- Stablecoin circulating supply is roughly $308.9B right now (and fluctuates daily).

- Visa’s stablecoin analytics dashboard shows all stablecoin activity at roughly $63.0T total transaction volume, $12.0T adjusted transaction volume, 13.8B total transaction count, and $244.6B average supply.

- Meanwhile, Mastercard’s scale is enormous: its fiscal-year 2025 reporting and Q4 disclosures emphasize continued expansion in gross dollar volume and switched transactions (for example, Q4 gross dollar volume ~$2.8T, cross-border volume +14%, switched transactions +10%).

So the thesis for 2026 is simple: stablecoins are becoming a settlement and money-movement rail, while card networks remain the dominant acceptance surface, and Mastercard is explicitly trying to connect those two worlds.

Key Takeaways

- Mastercard stablecoin pay is best understood as spend → settle → pay out, not as a single feature.

- Stablecoin cards are the most visible layer, but stablecoin settlement for acquirers is the bigger structural shift for commerce.

- Stablecoin activity is already at massive onchain scale (tens of trillions in total volume; trillions in adjusted volume).

- Global cross-border money movement remains expensive: the World Bank highlights an average remittance cost of 6.49% (for the RPW benchmark).

- Mastercard’s recent announcements focus on named partners and specific regions, meaning availability is not universal and often depends on licensing, acquirer readiness, and jurisdiction.

Definitions And Mental Model: What Stablecoin Pay Means In Mastercard Terms

1. Stablecoin-funded spend (consumer-facing)

This is the headline experience: a consumer uses stablecoins as the funding source for a purchase, but the merchant checkout flow still looks like a standard card payment.

In practice, it’s typically implemented through a wallet/app that issues a card credential and connects stablecoin balances to card authorization.

Why it matters: it turns stablecoins into spendable money at existing acceptance, rather than requiring every merchant to integrate new crypto checkout UX.

2. Stablecoin settlement (merchant/acquirer-facing)

Settlement is the less glamorous layer, but it’s the one that can reshape infrastructure.

Stablecoin settlement means some part of the acquiring/settlement chain can receive and reconcile value in stablecoins (e.g., USDC/EURC) rather than solely in fiat.

Why it matters: settlement choices affect treasury ops, working capital timing, cross-border friction, and reconciliation overhead.

3. Stablecoin payouts (disbursements to wallets)

Payouts are the reverse direction: businesses want to push money to users’ stablecoin wallets (contractors, creators, affiliates, cross-border recipients), ideally instantly and 24/7.

Why it matters: the traditional “send money internationally” problem is still costly. The World Bank explicitly calls out an average global remittance cost of 6.49%, a figure used to track progress toward lowering costs.

What Mastercard Announced And What It Explicitly Claims

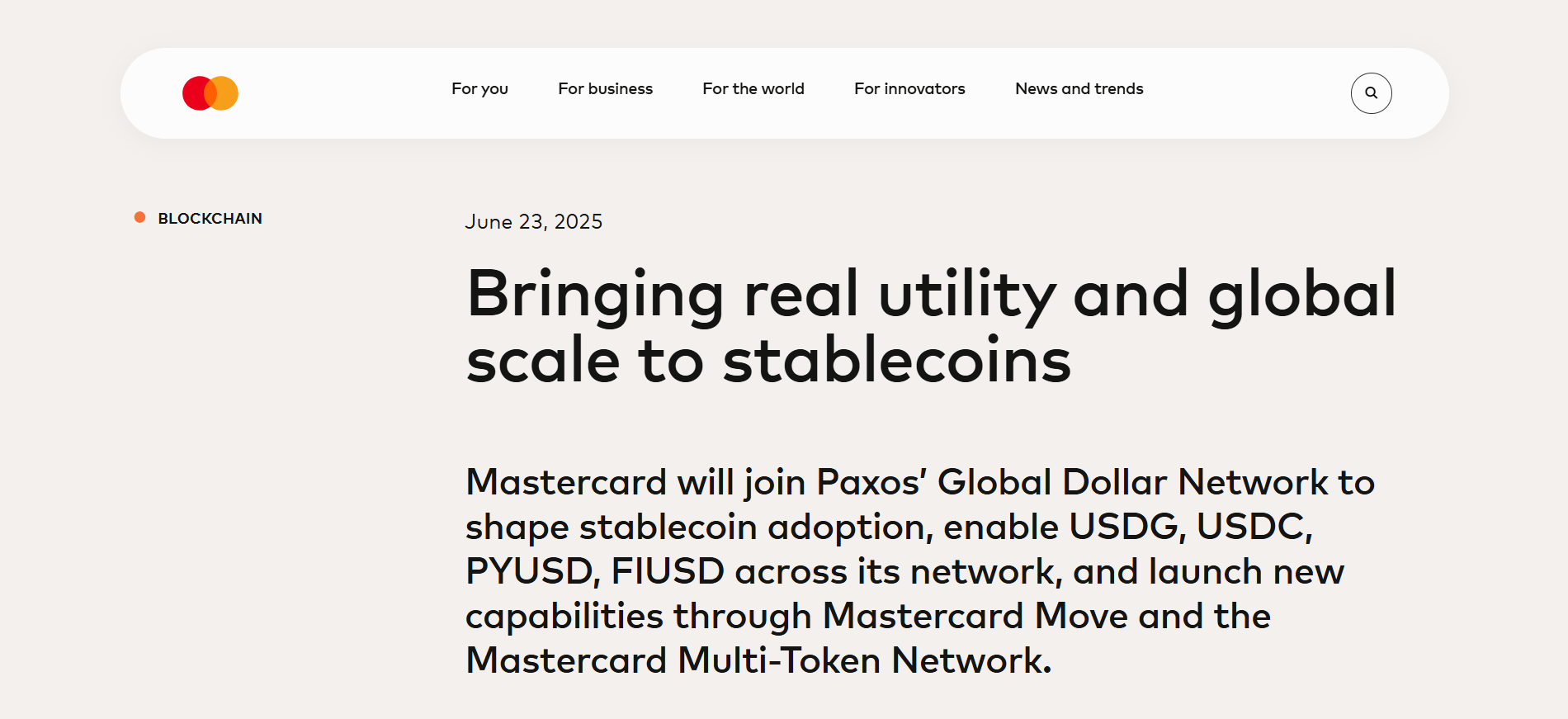

The wallets to checkouts stablecoin announcement (April 2025)

Mastercard’s April 2025 press release is the anchor document for this topic. It describes global end-to-end stablecoin acceptance and payments capabilities and explicitly frames stablecoins as evolving from trading tools into solutions for payments, disbursements, and remittances.

Two important points from the announcement:

- It positions the initiative as enabling both sides of commerce, consumers spending stablecoins and merchants receiving them (through the broader ecosystem).

- It calls out partnerships, including OKX and Nuvei, as part of the approach.

Layer 1: Paying With Stablecoins At Mastercard Merchants (Cards + Checkout Experience)

How stablecoin card payments actually work (step-by-step)

A stablecoin-funded card purchase usually looks like this:

- User holds stablecoins in a wallet/app balance (custodial or hybrid, depending on provider).

- The app provides a card credential that works across Mastercard acceptance.

- At checkout, the transaction runs through standard card authorization.

- Behind the scenes, the provider debited stablecoins (and may convert to fiat depending on how it settles with the network/acquirer).

- The merchant typically sees a familiar settlement currency (often local fiat), unless a stablecoin settlement path exists through the acquirer ecosystem.

From the merchant perspective, this is critical: the merchant doesn’t need to change checkout UX to benefit from stablecoin-funded consumer spend.

Case study: OKX Card in the EEA (2026)

A concrete, current rollout is the OKX Card in Europe.

OKX describes the OKX Card for the EEA as letting users spend stablecoins in everyday situations using the Mastercard network (they name stablecoins like USDC and USDG in their explainer).

Third-party reporting also frames it as enabling stablecoin payments where Mastercard is accepted.

Stats to anchor why Mastercard cares about new spend surfaces

Even without stablecoins, Mastercard is operating at huge volume, which makes incremental improvements in settlement, cross-border efficiency, and funding optionality strategically meaningful.

- Mastercard’s Q4 2025 earnings release highlights $2.8T gross dollar volume in the quarter (local currency basis), +14% cross-border volume, and +10% switched transactions.

Those numbers matter because stablecoin pay initiatives rarely aim to replace card acceptance; they aim to upgrade funding and settlement rails behind existing acceptance.

Layer 2: Merchant / Acquirer Stablecoin Settlement (The Bigger Strategic Shift)

What stablecoin settlement means in payments plumbing

A quick but important clarification:

- Authorization: is this payment approved?

- Clearing: are finalizing transaction details between parties?

- Settlement: is it moving the money between institutions?

Stablecoin settlement targets the settlement layer: using stablecoins as the asset that moves value between institutions (or between acquirers and their downstream merchant relationships), potentially reducing:

- timing constraints (weekends/holidays),

- multi-currency complexity,

- reliance on correspondent banking in some corridors,

- reconciliation overhead if the stablecoin becomes a standardized treasury asset.

Mastercard + Circle: USDC/EURC settlement for acquirers in EEMEA

This is one of the most explicit stablecoin settlement announcements from Mastercard.

In August 2025, Mastercard announced it expanded its partnership with Circle to enable acquiring institutions in EEMEA to receive settlement in USDC or EURC, and it frames this as enabling more efficient and trusted digital trade across emerging markets.

Why this is a big deal in infrastructure terms:

- It moves stablecoins beyond consumer card funding into acquiring settlement options (where the money actually moves between institutions).

- It signals a path where stablecoins become a treasury/settlement instrument inside payment networks and their partners, not just a consumer wallet balance.

Third-party coverage summarizes the same move as enabling settlement of USDC and EURC for acquirers in the region.

Important constraint to state clearly in the article: this is regional and implemented through acquiring institutions; it’s not the same as saying every merchant everywhere receives stablecoins.

Why EEMEA is a logical launch region

You can argue (carefully, without overstating) that EEMEA is a sensible region for stablecoin settlement expansion because:

- Cross-border commerce and remittances are central economic realities in many EEMEA markets.

- Cost and timing frictions remain high in traditional rails in many corridors.

Layer 3: Payouts To Stablecoin Wallets (Mass Disbursement Use Cases)

Why payouts are often the fastest route to real-world utility

Merchant checkout is one path to stablecoin pay, but payouts often hit real demand faster because:

- Businesses already have strong reasons to pay globally (contractors, affiliate networks, creator payouts, vendor payments).

- Recipients often want speed, certainty, and USD exposure in places where local rails are slow or volatile.

- The sender is typically more operationally motivated than a retail consumer (“I must pay 10,000 people in 40 countries on time”).

Mastercard + Thunes: stablecoin payouts

In November 2025, Mastercard announced it's partnership with Thunes to enable payouts to stablecoin wallets, positioning it as giving banks and payment providers more choice and flexibility and bringing stablecoin payouts to the mainstream.

Separate reporting describes integrating pay-to-stablecoin-wallets into Mastercard’s money movement network so payouts can be executed 24/7 to stablecoin wallets (implementation and coverage depend on participating institutions).

The Infrastructure Layer: MTN, Compliance Controls, And Identity

MTN as the programmable settlement substrate

Mastercard positions its stablecoin strategy as more than a consumer card program; it’s also about connecting tokenized value to regulated institutions and payment flows.

That’s where Mastercard’s end-to-end language typically points: acceptance at checkout, plus settlement/disbursement pathways through institutional partners.

MTN is a high level Mastercard’s approach to supporting tokenized/programmable value flows through trusted rails, without implying that every transaction is on-chain card settlement (which would be an overclaim in most markets).

Why stablecoin pay needs identity and assurance

Stablecoin payments have two practical problems that mainstream card payments already mitigate:

- Wrong-recipient risk (wallet address errors can be catastrophic).

- Compliance screening and dispute expectations (merchants, acquirers, and PSPs operate in regulated environments).

This is where identity, credentialing, and risk controls become the missing middle between wallet-native rails and mainstream commerce.

On the analytics side, it’s also why methodology matters: Visa’s dashboard explicitly uses filtering to estimate adjusted stablecoin activity, acknowledging raw onchain totals include noise that doesn’t represent economic payments.

Key Risks, Constraints, And What’s Still Not Solved

1. Regulatory and licensing boundaries

Even when Mastercard announces end-to-end capabilities, real availability depends on:

- which stablecoins are allowed/treated as regulated instruments in a jurisdiction,

- whether the wallet/card program is properly licensed,

- whether an acquirer can operationally and legally settle in stablecoins.

This is why most credible rollouts are described with region qualifiers and partner structures (EEMEA for settlement; EEA for certain card rollouts).

2. Consumer protection and disputes

Card rails come with mature dispute/refund frameworks. Stablecoin-funded spending must map those processes back to:

- stablecoin balances,

- conversion rates/fees,

- wallet custody and transaction records.

Providers differ, and consumers may not always get bank-like protections unless the product is structured to provide them.

3. Operational risk

Stablecoin pay introduces operational complexities:

- stablecoin issuer exposure (reserve, governance, redemption reliability),

- chain and infrastructure dependencies,

- compliance monitoring and sanctions screening,

- liquidity management for conversion and settlement.

Also, concentration is real:

USDT dominance around ~59%, implies ecosystem-level reliance on a small number of stablecoin issuers.

What This Means For Each Stakeholder

1. For merchants

If you’re a merchant, the most practical way to think about stablecoin pay is:

- Short term: stablecoin-funded cards increase consumer purchasing flexibility without changing your checkout.

- Medium term: your acquirer (or PSP) may offer stablecoin settlement options in specific regions.

Questions to ask your acquirer/PSP:

- Do you support settlement in USDC/EURC (or other regulated stablecoins) in my region?

- How do fees compare to fiat settlement?

- How does reconciliation work (statements, timestamps, FX rates, audit trail)?

- What are the dispute/refund workflows when a customer uses stablecoin funding?

2. For wallets and fintech apps

Wallets benefit because they can:

- convert stablecoin balances into real-world spend through card acceptance, and

- offer “sticky” financial UX (rewards, budgeting, multi-currency management).

But they must win on:

- compliance posture,

- transparent fees,

- user trust and support,

- clarity on what the user is actually buying (a card program vs a direct onchain payment).

3. For acquirers and PSPs

Acquirers and PSPs should treat stablecoin settlement as a product line with clear benefits in certain corridors and industries:

- high cross-border volume,

- marketplace payouts,

- regions with weaker banking interoperability,

- treasury teams that already manage USD exposure.

The Mastercard + Circle announcement is a strong signal that acquirer-facing stablecoin settlement is now an explicit roadmap item in EEMEA.

4. For regulators and compliance leaders

Key monitoring focus areas remain:

- reserve transparency and stablecoin issuer regulation,

- consumer disclosure and recourse,

- AML/sanctions controls in payout rails,

- operational resilience (outages, chain risk, partner dependencies).

A 2026–2027 Outlook: Where Mastercard Stablecoin Pay Is Likely Headed

This is a forecast section, so phrase it as directional rather than guaranteed.

Likely expansion pattern: partner-by-partner, region-by-region

Based on how Mastercard is communicating stablecoin pay (named partners, region-specific settlement announcements), the rollout pattern is likely:

- more wallet-linked stablecoin card programs,

- more acquiring-side settlement options where regulated stablecoins are supported,

- deeper integration of payouts-to-wallets through institutional money movement partners.

That fits the public end-to-end framing in the April 2025 release.

Market catalysts that make expansion rational

- Stablecoin supply is already ~ $309B, giving networks a large float to integrate.

- Onchain stablecoin activity is massive even after filtering (adjusted volume in the trillions).

- Cross-border remains a premium profit pool, and Mastercard disclosed +14% cross-border volume growth in Q4 2025, meaning any settlement rail innovation that protects or expands that volume is strategically relevant.

- The cost baseline for international money movement is still high (World Bank’s 6.49% average remittance cost benchmark), leaving room for efficiency-driven disruption.

Conclusion

Mastercard stablecoin pay in 2026 is best understood as a converging system:

- Spend: stablecoin-funded cards that preserve familiar acceptance,

- Settle: acquirer-facing settlement options in regulated stablecoins (in specific regions),

- Pay out: stablecoin wallet payouts as a mainstream disbursement method.

The real story isn’t whether stablecoins replace card payments.

It’s whether stablecoins become a standard settlement and treasury rail that networks, acquirers, and wallets can plug into, while merchants keep the same checkout experience.

Read Next:

- U.S. Stablecoin Rules on Interest Yields

- BVNK's Stablecoin Utility Report 2026

- The U.S. Stablecoin Regulatory Reset

FAQs:

1. What does Mastercard stablecoin pay mean?

It refers to Mastercard’s stablecoin capabilities across checkout spending, settlement pathways, and payouts to stablecoin wallets, described as end-to-end functionality from wallets to checkouts.

2. Can I pay with USDC anywhere Mastercard is accepted?

In practice, you can pay at Mastercard-accepting merchants if you have a stablecoin-funded card program that supports it (availability depends on provider and jurisdiction).

3. Do merchants actually receive stablecoins?

In some setups, parts of the acquiring ecosystem can receive settlement in stablecoins (e.g., USDC/EURC in EEMEA per Mastercard’s Circle announcement). It is not accurate to claim all merchants everywhere receive stablecoins.

4. What is the difference between stablecoin spend and stablecoin settlement?

Stablecoin spend is the consumer funding source (what the user pays with). Stablecoin settlement is how institutions move value between parties during settlement (what acquirers/merchants ultimately receive or reconcile).

5. Where does Mastercard support USDC/EURC settlement?

Mastercard’s public announcement specifically discusses enabling acquiring institutions in EEMEA to receive settlement in USDC or EURC via its expanded partnership with Circle.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}