Table of Contents

Ready to get started with stablecoins? The path is actually quite simple. You'll pick a solid, reputable stablecoin like USDC or USDT, find a trusted platform such as Coinbase or Kraken to buy it, and then you can start earning interest, either through the platform's own features or by exploring DeFi. It's a great way to dip your toes into crypto without the intense price swings.

Your Practical Starting Point for Stablecoin Investing

Think of stablecoins as the essential bridge connecting old-school finance with the new world of crypto. They are basically digital dollars—tokens built to hold a steady value, almost always pegged 1:1 to a currency like the U.S. dollar. This is what sets them apart from other cryptos known for their wild volatility. Stability is their entire purpose.

For investors, this stability offers a couple of huge benefits:

- A Safe Harbor: When the crypto market gets choppy, you can move out of volatile assets like Bitcoin or Ethereum into a stablecoin. This lets you sidestep the volatility without completely cashing out to traditional currency, which saves you a ton on fees and hassle.

- A Yield-Generating Tool: Stablecoins are your ticket to earning interest. They unlock access to savings accounts and lending protocols in the crypto world that often pay out much higher returns than you'd find at a typical bank.

Why Stablecoins Are Gaining Momentum

The buzz around stablecoins isn't just hype; it's backed by some serious numbers. As of October 2025, the total market cap for stablecoins soared to an all-time high of $308 billion. That means stablecoins now make up 7.80% of the entire digital asset space.

Tether's USDT is leading the pack, growing to a massive $183 billion in market cap and capturing 59.4% of the market share. Even more impressive, it accounts for a staggering 75.2% of all trading volume on major exchanges. This isn't just about speculation—it shows that people are actually using these tokens for everything from payments to preserving their capital.

If you're still getting your bearings in the crypto world, this practical guide to cryptocurrency for beginners is a great place to build a solid foundation before diving deeper into stablecoins.

Here's the key takeaway: It's best to think of stablecoins as digital cash, not a speculative bet. Even the SEC has pointed out that they're primarily used for payments and storing value, not for chasing price gains.

Making an Informed First Choice

Since U.S. dollar-pegged stablecoins make up nearly 99% of the market, your first decision will come down to a handful of major players. Each one has a different company behind it, a different way of backing its value, and varying levels of transparency. Getting a handle on these differences is your first real step toward a smart strategy.

The table below gives you a quick breakdown of the top options to help you figure out which one is the right fit for you.

Comparing Top Stablecoins for Your First Investment

Here's a look at the leading stablecoins. Pay attention to who issues them and how they're backed—these are critical details for your decision.

| Stablecoin (Ticker) | Issuer | Collateral Type | Primary Use Case |

|---|---|---|---|

| Tether (USDT) | Tether Limited | Cash, cash equivalents, other assets | Trading, cross-border payments, DeFi liquidity |

| USD Coin (USDC) | Circle & Coinbase | Cash and short-term U.S. government securities | DeFi, payments, institutional treasury management |

| Dai (DAI) | MakerDAO (Decentralized) | Overcollateralized by various crypto assets | DeFi lending/borrowing, decentralized trading |

| PayPal USD (PYUSD) | PayPal & Paxos | U.S. dollar deposits, U.S. Treasuries, repos | Payments within the PayPal ecosystem, remittances |

Choosing between these often comes down to your personal risk tolerance and what you plan to do. If you value transparency and regulatory compliance, USDC is often the go-to. If you're looking for the deepest liquidity for trading, USDT is hard to beat. And if decentralization is your priority, DAI is the clear winner.

Choosing the Right Type of Stablecoin

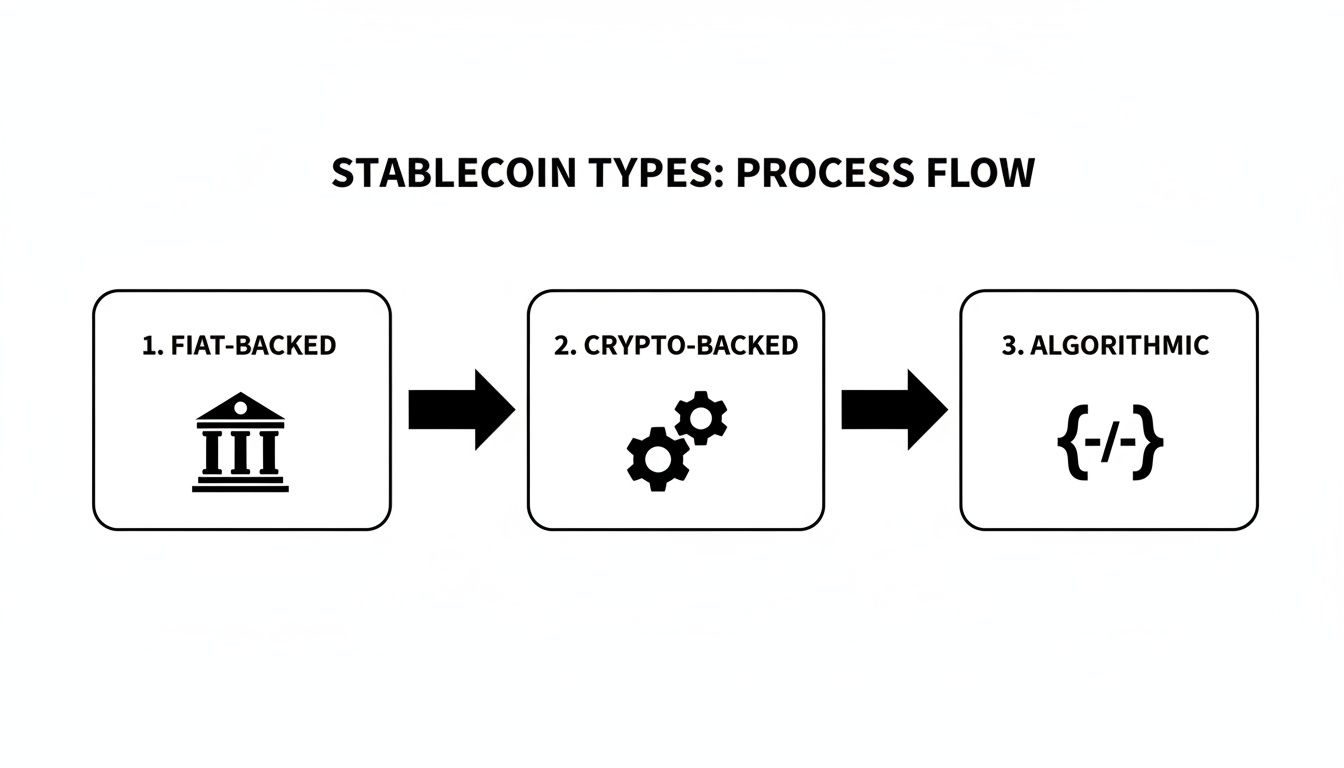

When you first get into stablecoins, it's easy to think they're all the same. They're all pegged to a dollar, right? Well, not exactly. The way they hold that peg is what really matters, and the differences can be massive. Choosing the right one is less about the name and more about understanding the machinery working behind the scenes.

Before you put any money down, you really need to get a handle on the main categories. The mechanics of each one directly shape its risk and how much you can actually trust it to stay stable.

Fiat-Backed: The Gold Standard of Transparency

Fiat-backed stablecoins are by far the most common and easiest to understand. The concept is simple: for every digital token out there, there's a real dollar (or equivalent) sitting in a bank account somewhere.

Think of it as a digital IOU. You hand a company like Circle (the issuer of USDC) or Tether (the issuer of USDT) a dollar, and they mint one of their tokens for you. That company then squirrels away your dollar in its reserves, usually in cash or super-safe, easy-to-sell assets like short-term U.S. government bonds.

The big win here is transparency and simplicity. The best issuers bring in auditors all the time to prove they have the cash to back up every single token they've created. This one-to-one backing makes them feel incredibly solid for day-to-day use.

But they aren't totally risk-free. The weak point is centralization. You're putting your faith in the issuing company and its banking partners to manage everything correctly. We saw a flash of this risk in March 2023 when USDC briefly lost its peg because its issuer had funds stuck in a bank that was collapsing. It was a stark reminder that even the biggest players can wobble when traditional finance gets shaky.

Crypto-Backed: The Decentralized Alternative

Crypto-backed stablecoins were born out of a desire to cut traditional banks out of the picture entirely. Instead of being backed by dollars, these are collateralized by other crypto assets.

The most famous example here is DAI, which is governed by the decentralized MakerDAO protocol. To create DAI, you have to lock up more value in another crypto, like Ethereum (ETH), than the DAI you want to mint. For example, you might need to deposit $150 worth of ETH into a smart contract just to get $100 worth of DAI.

This practice, called over-collateralization, is the whole safety net. That extra collateral is a buffer against the wild price swings of the assets backing it. If the value of the locked ETH starts to tank, the system automatically begins selling it off to make sure every DAI in circulation is still fully backed and worth a dollar.

The main advantage is decentralization. There's no single company to go under or bank account to freeze. Everything runs on open-source code for anyone to see, which drastically reduces counterparty risk. The trade-off? It's more complex, and its stability depends on the health of the broader crypto market.

Algorithmic: The Experimental Frontier

Algorithmic stablecoins are the wild west of the bunch—the most ambitious and, as we've seen, the most dangerous. They try to hold their $1 peg without any collateral at all. Instead, they rely on complex algorithms and smart contracts to expand or shrink the token supply, kind of like how a central bank manages a national currency.

If the price ticks above $1, the algorithm spits out more tokens to increase supply and push the price back down. If it dips below $1, it uses clever tricks to take tokens out of circulation, like offering rewards to people who "burn" them.

It's a fascinating idea, but in practice, it's proven incredibly fragile. The spectacular collapse of TerraUSD (UST) in 2022 was a brutal lesson. Once the market lost faith, the whole system entered a "death spiral" that vaporized billions of dollars. If you're just learning how to invest in stablecoins, I'd strongly advise steering clear of algorithmic models until one proves it can survive a few market cycles.

For a deeper dive into specific coins and how they stack up, you can check out this guide on the best stablecoins to consider for your portfolio. It's a good way to compare the top-tier fiat and crypto-backed options side-by-side.

Building Your Investment Toolkit

Before you can actually invest in stablecoins, you've got to get the right tools in place. It all starts with picking a reliable place to buy them, setting up a digital wallet to keep them safe, and figuring out how to get your money from your bank account into the crypto world. Nailing these first few steps is easily the most critical part of building a solid stablecoin strategy.

Think of it as opening a new brokerage account, just with a few crypto-specific wrinkles. The choices you make right now will dictate how easily you can jump on investment opportunities and, more importantly, how secure your assets will be down the road.

Selecting Your On-Ramp: A Primer on Exchanges

Your first port of call is a cryptocurrency exchange. This is where you'll swap your traditional money, like U.S. dollars, for stablecoins. There are a ton of options out there, but if you're just starting, your best bet is to stick with platforms known for top-notch security, user-friendliness, and a clean regulatory record.

For anyone new to the game, here are three heavy hitters and what makes them tick:

- Coinbase: Widely seen as the go-to for beginners. The interface is clean and simple, which makes linking your bank and making that first purchase feel a lot less intimidating.

- Kraken: This one is known for its serious security measures and a broader selection of crypto assets. It’s a small step up in complexity from Coinbase but a fantastic choice if you want more control and features to grow into.

- Binance: The big draw here is the rock-bottom trading fees and a massive ecosystem of products. The flip side is that its platform can feel like drinking from a firehose for a newcomer, and it's faced some regulatory heat in various countries.

My advice? Start with a platform like Coinbase to get your bearings. You might pay slightly higher fees, but that's a small price for the peace of mind and straightforward experience you get while learning the ropes.

Choosing Your Digital Wallet

Once you buy stablecoins on an exchange, you need a safe place to put them. Leaving them on the exchange is an option, but it's not one I'd recommend for the long haul. You’ve probably heard the saying: "not your keys, not your crypto." Moving your funds to a personal digital wallet gives you full control.

This is a good time to remember the different kinds of stablecoins out there, as this will influence how you store and use them.

The image above lays out the core mechanics—from centralized, fiat-backed models to their decentralized counterparts. Your wallet choice really comes down to which of these you're holding and what you plan to do with them.

Here’s the rundown on the two main types of wallets:

- Software Wallets (Hot Wallets): These are apps on your phone or computer, like MetaMask or Trust Wallet. Because they're connected to the internet, they're super convenient for day-to-day use, especially if you're interacting with DeFi apps. They’re perfect for holding smaller amounts you plan to put to work.

- Hardware Wallets (Cold Wallets): Think of these as a physical vault for your crypto. Devices from Ledger or Trezor store your private keys offline, making them practically immune to online hacks. This is the gold standard for securing any significant amount of money you don't need to access frequently.

A smart hybrid approach works best for most people. Keep a small, active "checking account" of stablecoins in a software wallet for earning yield, and lock down the bulk of your "savings" in a hardware wallet for maximum security.

From Fiat to Stablecoin: The Practical Steps

Alright, let's connect the dots and turn your dollars into digital dollars. The process is pretty consistent across the major exchanges.

Here’s what that workflow typically looks like:

- Link Your Bank Account: The easiest method is an ACH transfer. It's usually free, but you'll have to wait a few business days for the funds to clear.

- Use a Wire for Speed: If you're moving a larger sum and want to get started right away, a wire transfer is your friend. It often clears the same day, but expect to pay a fee to your bank for the service.

- Make the Purchase: Once the cash lands in your exchange account, find the "trade" or "buy" section. Pick the stablecoin you want (like USDC), type in the amount, and confirm the trade. The exchange will take a small fee for this.

- Withdraw to Your Wallet: This is a non-negotiable final step for security. Find the "withdraw" option on the exchange, select your stablecoin, and carefully paste in your personal wallet address. Seriously, triple-check that address—one wrong character, and your funds could be gone forever.

For a deeper dive into managing your assets after you buy, our guide on storing stablecoins securely covers the essential practices for both software and hardware wallets. Getting into these secure habits from day one is one of the smartest things you can do.

Finding Yield in a Stablecoin World

Just letting stablecoins sit in a wallet is like stuffing cash under your mattress. It’s safe, sure, but it's not working for you. The real magic happens when you put those digital dollars to work to generate passive income, or "yield." This is how you transform a simple digital dollar into a productive, return-generating asset.

The world of stablecoin yield is vast, with paths for every comfort level. You can find simple, one-click solutions on familiar platforms or dive into more complex (but often more rewarding) strategies in Decentralized Finance (DeFi). The right choice really comes down to your risk tolerance, technical confidence, and how hands-on you want to be.

Starting with Centralized Finance (CeFi)

For anyone just getting their feet wet, the journey into earning yield usually begins right on the exchange where you bought your first stablecoins. Centralized Finance, or CeFi, offers refreshingly simple ways to earn interest that feel a lot like a high-yield savings account.

Platforms like Coinbase or Kraken often have "Earn" or "Lending" features built right in. You just deposit your stablecoins into one of these programs, and the platform handles the rest—lending them out and sharing a slice of the interest with you. It’s pretty straightforward.

What's great about starting with CeFi?

- It’s dead simple: It usually takes just a couple of clicks to start earning. No need to worry about managing private keys or navigating complex protocols.

- Minimal fees: You get to sidestep the network transaction fees (gas fees) that are a big part of the DeFi world.

- A safety net: If you hit a snag, there’s a customer support team you can actually contact for help.

Of course, CeFi isn't without its own set of trade-offs. The biggest is that you're handing your funds over to a company, which introduces counterparty risk. If that platform goes under, your assets could be caught in the crossfire. The yields are also typically a bit tamer than what you might find out in the wilds of DeFi.

Venturing into Decentralized Finance (DeFi)

If you're up for a bit more adventure and a steeper learning curve, DeFi is where the really exciting opportunities are. These are financial applications built on blockchains that operate without any middlemen. You're in the driver's seat, interacting with them directly from your personal wallet.

This isn't some niche corner of the market. Over the last 12 months through September 2025, adjusted stablecoin transaction volume hit an incredible $9 trillion, a jump of 87% year-over-year. That's more than five times PayPal's total throughput. For investors, this ocean of liquidity means it’s easier than ever to tap into DeFi and find yields that leave traditional savings accounts in the dust. You can dig deeper into these numbers in the State of Crypto Report 2025.

Two of the most battle-tested ways to earn yield in DeFi are through lending protocols and providing liquidity.

The DeFi Mindset: In DeFi, you have direct control over your assets ("self-custody") and the potential for much higher returns. But that freedom comes with responsibility. You are your own bank, which also means you are your own head of security.

DeFi Yield Strategy 1: Lending Protocols

DeFi lending platforms like Aave or Compound function as autonomous money markets. It's a simple, elegant system: you deposit your stablecoins into a lending pool, and borrowers can take out loans against their own crypto collateral. For providing that liquidity, you earn a variable interest rate paid by the borrowers.

The system is designed with safety in mind. Loans are always over-collateralized, meaning borrowers have to lock up more value than they borrow, which protects lenders from defaults. It’s a powerful and popular way to earn truly passive income right from your wallet. If you want to really get into the weeds, our guide on stablecoin yield farming strategies breaks down more advanced techniques.

DeFi Yield Strategy 2: Providing Liquidity

Another cornerstone of DeFi is becoming a liquidity provider (LP) on a decentralized exchange (DEX) like Uniswap. DEXs don't use traditional order books; they rely on pools of tokens to facilitate instant swaps. As an LP, you contribute to one of these pools by depositing a pair of assets—a classic example would be 50% USDC and 50% ETH.

Whenever someone makes a trade using that pool, they pay a small fee. A portion of those fees is then distributed to all the liquidity providers in the pool as a reward. This can be a very lucrative strategy, but it comes with a unique risk called impermanent loss. This happens if the price ratio of the two assets you deposited shifts dramatically while they're in the pool.

To help you decide which path might be right for you, here’s a quick breakdown of the different strategies:

Yield Generation Strategies Comparison

| Strategy | Platform Example | Typical APY Range | Risk Level | Complexity |

|---|---|---|---|---|

| CeFi Lending | Coinbase Earn | 2% - 6% | Low-Medium | Very Low |

| DeFi Lending | Aave, Compound | 3% - 10% | Medium | Medium |

| Liquidity Providing | Uniswap, Curve | 5% - 20%+ | High | High |

This table is just a general guide. APYs are dynamic and can change based on market conditions, and your risk tolerance is personal. It's always best to start small and get comfortable with a platform before committing more significant funds.

From Theory to Practice: A Walkthrough

Let's make this real. Say you have $1,000 in USDC on Coinbase and you want to move it to a DeFi lending protocol on the Ethereum network to earn a better yield. Here’s how you’d do it.

- Get Your Funds Off the Exchange: First, you’ll withdraw the $1,000 USDC from Coinbase to your personal MetaMask wallet. You’ll need your wallet’s public address for this. Pay close attention here: you must select the correct network (e.g., Ethereum ERC-20) during the withdrawal. Sending to the wrong network is a classic and costly mistake.

- Connect to a DeFi App: Head over to a lending platform’s website, like Aave. Find the "Connect Wallet" button (usually in the top right corner) and link your MetaMask wallet. This is how you give the app permission to "read" your wallet's contents.

- Make Your Deposit: Once connected, you’ll see a dashboard of different assets you can supply. Find USDC, type in the amount you want to deposit ($1,000), and get ready to approve the transaction in your wallet.

- Sign, Pay Gas, and Confirm: You'll actually have to sign two transactions. The first is an "approval" that allows the platform's smart contract to access your USDC. The second is the actual deposit. Both of these actions require a network fee, called a gas fee, which is paid in ETH.

After the transaction is confirmed on the blockchain—which can take a few seconds to a few minutes—that’s it! Your Aave dashboard will update to show your deposited USDC, and you'll immediately start earning interest. You've just successfully bridged the gap from CeFi to DeFi.

Smart Ways to Manage Risk and Protect Your Funds

Chasing yield is the exciting part, but the bedrock of any solid investment plan is protecting what you’ve already got. When you're dealing with stablecoins, you’re playing in a field with its own unique set of rules and risks, ones that look quite different from traditional finance. Getting a handle on them isn't meant to scare you; it's about giving you the confidence to navigate the space like a pro.

The good news? Most of the biggest threats are well-documented and can be managed with some straightforward, sensible habits. Your main job is to keep three specific challenges on your radar: de-pegging events, counterparty failures, and smart contract exploits.

Understanding De-Pegging Risk

De-pegging is exactly what it sounds like: the risk that a stablecoin slips from its $1.00 peg. Even the most reputable stablecoins can wobble under pressure. We all saw a classic example in March 2023 when USDC, a titan in the space, briefly sank to $0.87 after its issuer revealed exposure to a failing bank.

That event was a wake-up call. It proved that even fully reserved, fiat-backed stablecoins aren't completely insulated from panic in the market or cracks in the very banking systems they depend on.

Pro Tip: Never go all-in on a single stablecoin. A simple yet incredibly effective tactic is to spread your holdings across two or three different, high-quality stablecoins. For instance, splitting your capital between USDC, USDT, and a decentralized option like DAI builds an immediate buffer.

Think of it as a basic hedge. If one stablecoin hits a rough patch and de-pegs, the others in your portfolio will likely hold their ground, shielding the majority of your funds from a single point of failure.

Navigating Counterparty and Smart Contract Risk

The next layer of risk is tied to the platforms and protocols you interact with. These two risks are often lumped together, but they’re distinct problems.

- Counterparty Risk: This is the classic "not your keys, not your coins" problem. It’s the danger that the exchange (like Coinbase or Kraken) or centralized lending platform holding your funds could go bankrupt or freeze withdrawals. You're trusting them to stay solvent and act responsibly.

- Smart Contract Risk: This one is unique to DeFi. It's the chance that a hacker finds a bug or an exploit in a protocol's code and uses it to drain funds from a liquidity pool or lending market. It happens more often than you'd think.

Protecting yourself here comes down to a combination of smart platform choices and staying vigilant. For a much deeper dive into these issues, check out our complete guide on the primary stablecoin risks and what to look for.

Your Personal Security Playbook

At the end of the day, you are the first and last line of defense for your own money. While sophisticated hacks get the headlines, a surprising number of losses come from simple security oversights. Building a few key habits into your routine will dramatically shrink your attack surface.

Invest in a Hardware Wallet

If you're holding an amount of stablecoins that would genuinely hurt to lose, a hardware wallet is not optional—it's essential. Devices from trusted brands like Ledger or Trezor keep your private keys totally offline. This makes it practically impossible for a remote hacker to get their hands on your funds.

Master Your Digital Hygiene

Your everyday online habits are your best defense. They seem basic, but they are shockingly effective at stopping the most common attacks in their tracks.

- Use a Password Manager: Seriously. Never reuse passwords between crypto platforms and your email. A tool like 1Password or Bitwarden creates and saves unique, complex passwords for every login, closing one of the biggest security gaps people have.

- Enable Two-Factor Authentication (2FA): Always opt for an authenticator app (like Google Authenticator or Authy) over SMS for 2FA. Hackers can execute "SIM swap" attacks to hijack your phone number and intercept text messages. An authenticator app is tied to your physical device, making it far more secure.

- Be Relentlessly Skeptical: Treat every link, email, and direct message as a potential threat. Never click on unsolicited links, respond to DMs from "support agents," or type your seed phrase into any website or app. Phishing scams are everywhere and getting more convincing by the day.

By layering diversification, self-custody with a hardware wallet, and disciplined security habits, you build a fortress around your assets. This approach frees you up to pursue yield opportunities with peace of mind, knowing your foundation is secure.

Navigating Taxes and Future Regulations

It's easy to get caught up chasing the best yields, but if you're serious about stablecoin investing, you can't ignore the rules of the road. Frankly, overlooking taxes and regulations is the fastest way to turn your hard-earned gains into a major headache. The rulebook is still being written, but the fundamentals are clear enough for anyone willing to pay attention.

A lot of people get tripped up here. They assume that swapping one crypto for another—or even a stablecoin back into dollars—is a tax-free move. In most places, like the U.S., it's not. That swap is a taxable event.

Any time you sell, trade, or use a stablecoin for more than you acquired it for, you’re likely looking at a capital gain. On top of that, the yield you earn from lending or liquidity pools? That's typically taxed as ordinary income, just like the interest you'd get from a savings account.

Keeping Your Records Straight

The best advice I can give you is to track everything from the moment you start. You could try to log every transaction in a spreadsheet, but trust me, that gets out of hand incredibly fast.

Thankfully, there's a whole cottage industry of crypto tax software designed to solve this problem. These tools are a lifesaver. Here’s how they generally work:

- They sync with your exchange accounts and wallets using an API key.

- They automatically sort your transactions into buys, sells, income, etc.

- They spit out the exact tax forms you need, like Form 8949 for U.S. filers.

Using one of these services can easily save you dozens of hours of manual work and prevent costly mistakes. It's a small price to pay for accuracy and peace of mind. To dive deeper, check out our comprehensive stablecoin tax guide for 2025. And for general guidance, some investors find services like Bluesage Tax for tax resources helpful.

Watching the Regulatory Horizon

Taxes are just one piece of the puzzle. The bigger picture includes the regulations being hammered out by policymakers around the world. Governments are actively trying to figure out how to manage stablecoins to ensure financial stability and protect consumers. We're already seeing proposed laws in the U.S. that would create much stricter rules for issuers about their reserves and transparency.

The bottom line is this: regulation isn't a question of if, but when and how. That might sound scary, but clear rules can actually bring more legitimacy and stability to the market, which is a good thing for long-term investors.

You don't need to become a legal expert to stay ahead. Just follow a few reputable crypto news outlets and get a feel for which way the wind is blowing. This will help you see changes coming down the pike and adjust your strategy, making sure your investments are always on solid ground.

Common Questions About Stablecoin Investing

Even after getting the lay of the land, a few questions always seem to come up when people first start exploring stablecoins. Let's tackle them head-on so you can move forward with a clearer picture.

Are Stablecoins Completely Risk-Free?

In a word, no. While they are built to be a stable store of value, calling them "risk-free" is a mistake. They have their own unique set of risks that you won't find with a traditional savings account.

It's crucial to understand these potential pitfalls:

- De-pegging Risk: This is the big one. It's the risk that a stablecoin loses its 1:1 peg to the dollar. We've seen it happen, and it can be catastrophic.

- Counterparty Risk: The company holding your stablecoins—whether it's an exchange or a lending platform—could go under. If they do, your funds could be lost.

- Regulatory Risk: The rules of the road are still being written. A sudden change in government policy could dramatically alter how stablecoins are allowed to operate.

You can definitely lower these risks by sticking with highly reputable, well-audited stablecoins like USDC from Circle and only using platforms with a long track record of security. But remember, you can minimize risk, not eliminate it entirely.

How Much Should I Start With?

There’s no one-size-fits-all answer here, but my advice is always the same: start with an amount you would be genuinely okay with losing. For most people dipping their toes in for the first time, that might be anywhere from a few hundred to a thousand dollars.

Think of this first investment as tuition. The goal isn't to get rich overnight; it's to walk through the entire process—buying stablecoins, moving them to your own wallet, maybe even trying out a simple lending protocol. You learn the ropes without the stress of having significant capital on the line.

What Is the Key Difference Between a Wallet and an Exchange?

This is a fundamental concept that trips up a lot of newcomers. Keeping your stablecoins on an exchange is easy and convenient, especially for trading or using their built-in savings features. The catch? The exchange holds the keys, not you. This introduces that counterparty risk we just talked about.

A personal wallet, on the other hand, puts you in complete control. Whether it’s a software wallet like MetaMask or a hardware wallet like a Ledger, you hold the private keys. This is known as self-custody and is the gold standard for long-term security and the only way to truly interact with most of the decentralized finance (DeFi) world.

{kind=link}

{kind=link}