Table of Contents

While most of the world views stablecoins simply as a tool for faster payments, they are quickly becoming the foundational infrastructure for a new, always-on global credit market.

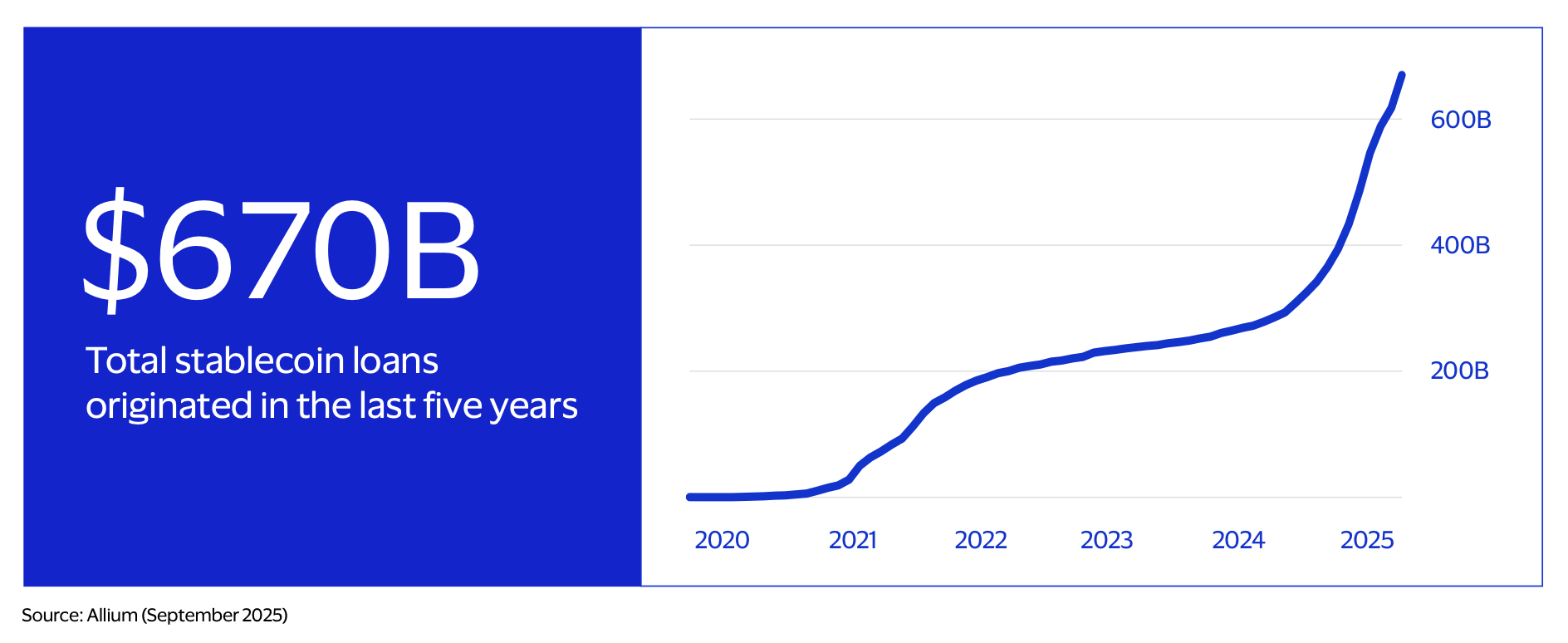

A new report by Visa and Allium reveals that onchain lending has already processed over half a trillion dollars in loans.

Here is the breakdown of why this matters for the next generation of finance.

From Balance Sheets to Code

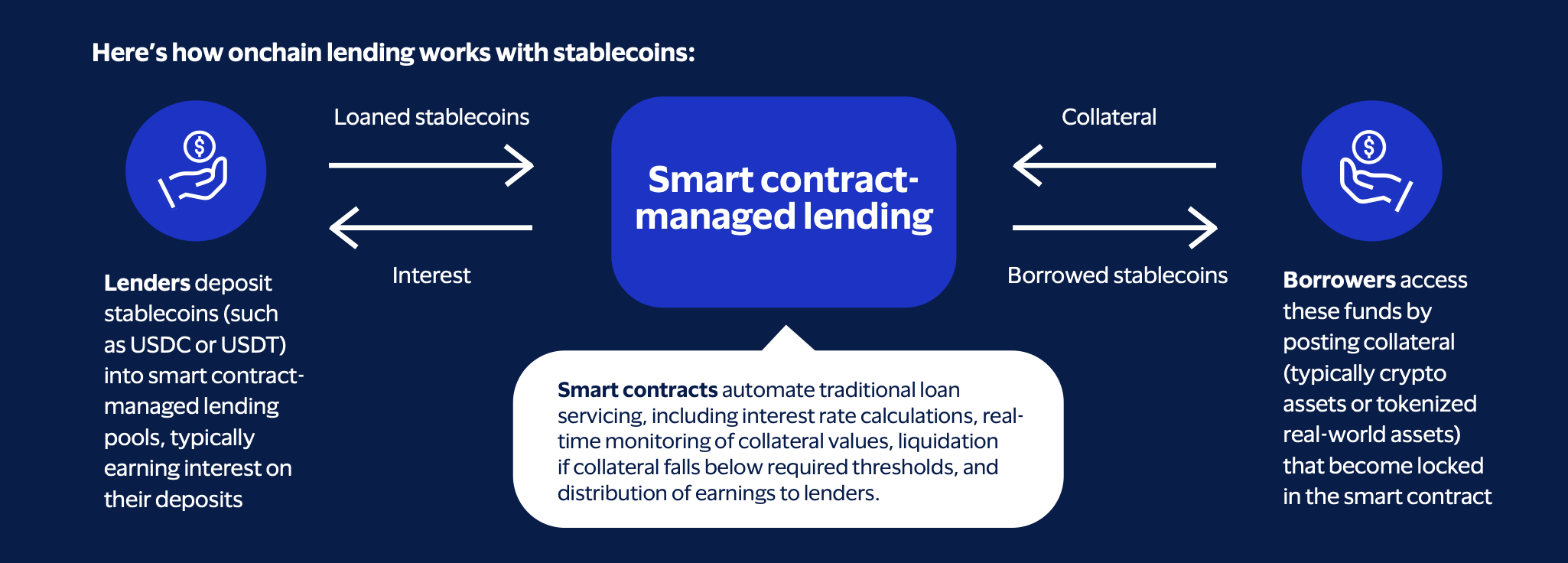

Traditional lending relies on credit checks and legal enforcement.

Onchain lending replaces this with electronic trust.

Smart Contract Automation

Loans are serviced by code that handles interest calculations, real-time collateral monitoring, and instant liquidations.

24/7 Liquidity

Unlike traditional markets, these global credit pools never close and offer transparent, algorithmic pricing based on real-time supply and demand.

Settlement Efficiency

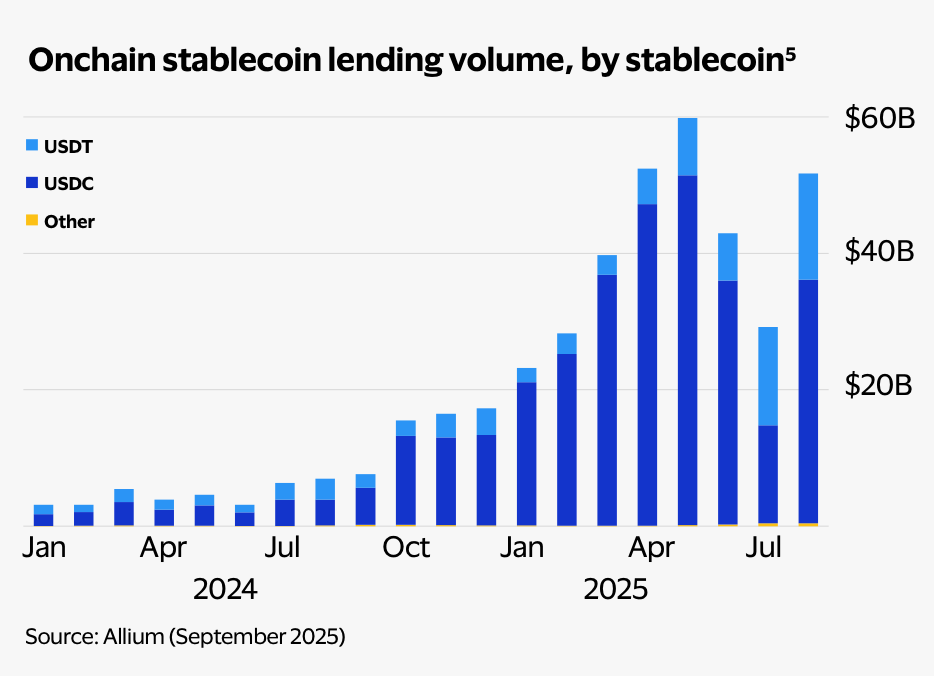

By using stablecoins like USDC and USDT (which represent 98%+ of the current supply), settlement is near-instantaneous rather than taking days.

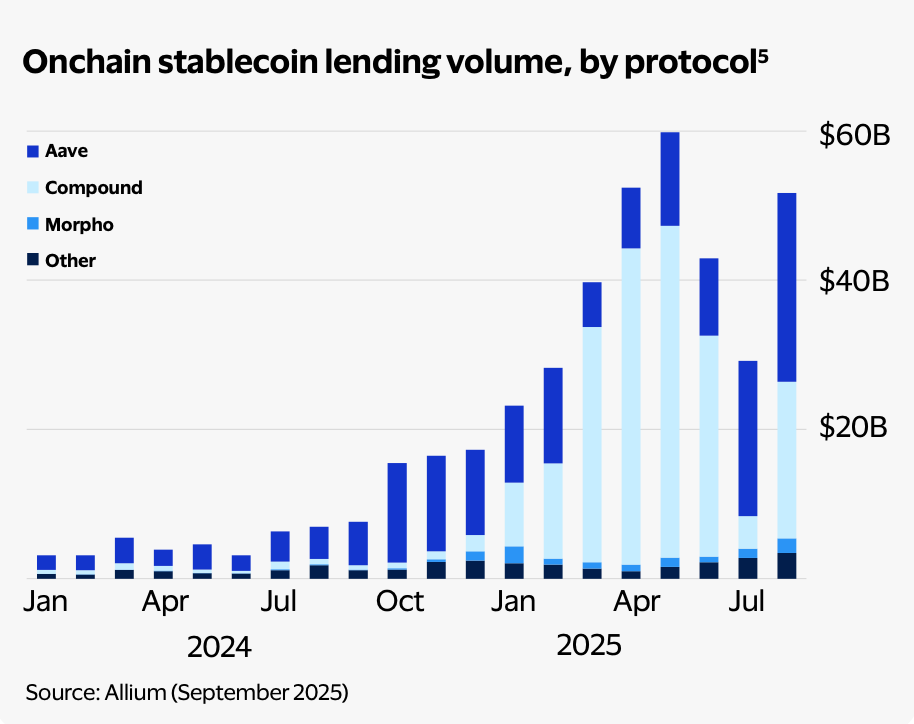

The Data: Market Recovery & Institutional Interest

After a lull in early 2024, the market has come roaring back to all-time highs.

- Record Volume: In August 2025 alone, $51.7 billion in stablecoins were borrowed.

- Active Utilization: Lending protocols currently hold ~$17.5 billion in stablecoin liquidity, with 84% of those funds actively deployed in loans.

- Growing Ticket Sizes: The average loan size has recovered to $121,000, reflecting a significant influx of institutional participants.

Real-World Case Studies

We are moving beyond "crypto-only" use cases into serious B2B applications:

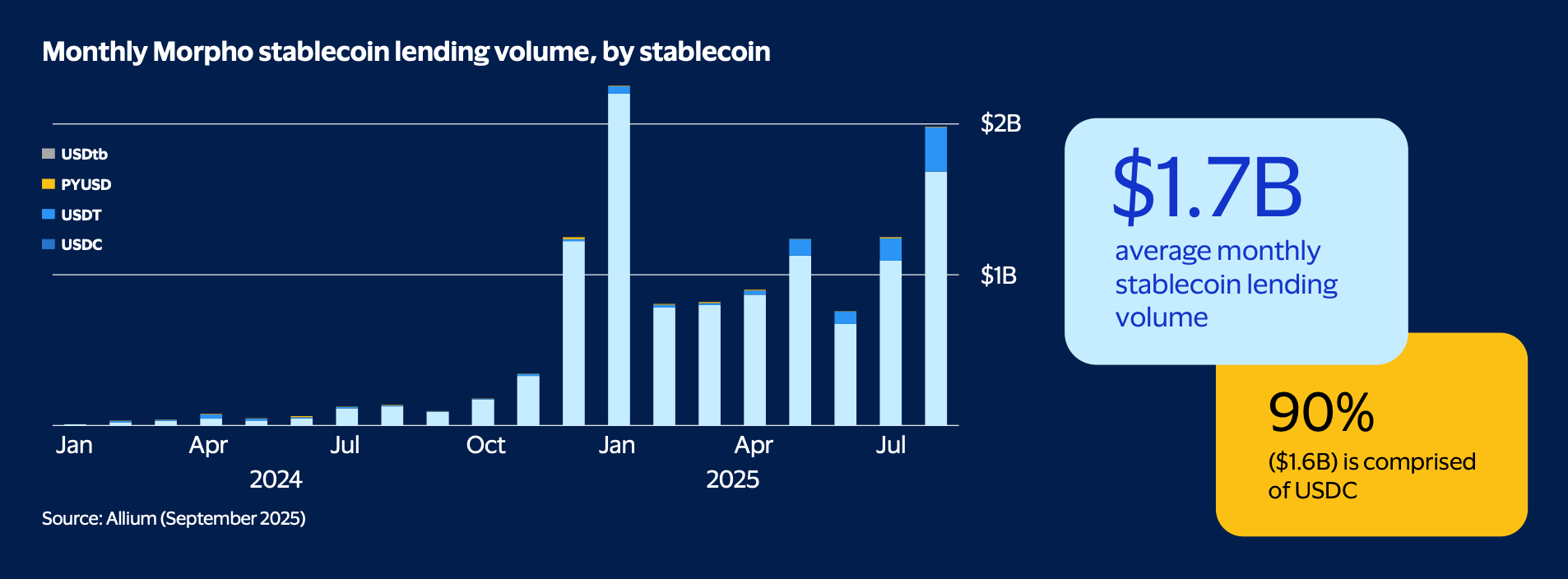

Morpho

Now acts as a back-end lending layer for giants like Coinbase and Société Générale, creating a multilateral marketplace that offers rates up to 2x lower than traditional options.

Related: Best Stablecoin Liquidity Providers 2026

Huma Finance

A "PayFi" network processing $500M in monthly volume, helping businesses finance cross-border payments and supplier payouts without the need for capital-intensive pre-funding.

Credit Coop

Powers card programs (like Rain) by allowing them to borrow against future payment receivables, solving critical working capital gaps.

"The real revolution is not in electronic money; it is in electronic trust." — Dee Hock, Founder of Visa

Undercollateralized Lending

The current dominance of overcollateralization where borrowers must post more capital than they receive, is a major barrier to widespread adoption.

The next evolution shifts the focus toward reputation-based credit.

Onchain Behavior as Credit History

Emerging protocols analyze a wallet’s transaction history, asset holdings, and interaction patterns to construct a digital credit profile.

Pioneering Platforms

Solutions like Credora, Providence, and 3.Jane are developing methods to assess creditworthiness using verifiable onchain data while maintaining user privacy through zero-knowledge proofs.

Outcome

This transition could unlock a massive addressable market for small businesses and individuals who lack existing capital but have strong digital financial track records.

Real-World Asset (RWA) Integration

Bridging the $40 trillion+ traditional credit market with blockchain is one of the most significant opportunities of the next decade.

Tokenized Collateral

Traditional assets like corporate bonds, private credit, and real estate are being tokenized to serve as collateral in global lending markets.

Institutional Adoption

BlackRock’s BUIDL Fund reached a market cap of $2.9 billion in tokenized Treasuries by May 2025, with lending protocols acting as distribution partners.

Scale of Opportunity

McKinsey projects that total tokenized assets could reach $1–4 trillion by 2030, fundamentally changing how liquidity is sourced for illiquid physical assets.

The Convergence of TradFi & DeFi

By 2026, the lines between traditional finance and decentralized systems are becoming increasingly blurred.

Banks as Liquidity Providers

Traditional financial institutions are exploring roles as liquidity providers for programmable lending protocols.

Programmable Treasury

Corporations are beginning to embed blockchain into their core balance-sheet infrastructure to optimize cash flow and reduce idle capital.

Regulatory Catalysts

Frameworks like the GENIUS Act in the U.S. have provided the legal clarity necessary for institutions to move from experimentation to enterprise-grade deployment.

Conclusion

The transition to onchain lending with stablecoins has proven its resilience by recovering to process over half a trillion dollars in total volume.

This data confirms that smart contracts are successfully replacing traditional intermediation to provide a more efficient, 24/7 global credit market.

As institutional loan sizes grow and stablecoin liquidity deepens, the line between decentralized finance and global banking continues to dissolve.

Upcoming Stablecoin Events

- Consensus Hong Kong: Feb 10-12 (Hong Kong)

- ETH Denver: Feb 17-21 (Denver)

- Money Motion: Mar 11-12 (Zagreb)

Related Reports

Partner/Advertise with Stablecoin Insider

Fill out this form to partner and advertise on the only publication, dedicated entirely to the Stablecoin ecosystem.

See you next week,

- The Stablecoin Insider team

{kind=link}