Table of Contents

Note up front:

As of December 2025, JPMorgan has already launched its JPMD USD deposit token on a public blockchain, and Goldman Sachs is live with its GS DAP tokenization platform and tokenized money-market funds.

There is no public press release that says “Goldman Sachs and JPMorgan will each launch a retail-branded stablecoin exactly in Q1 2026.”

This article uses Q1 2026 as a realistic near-term horizon for when bank-issued tokens from these two firms are expected to become central infrastructure for institutional payments, based on what they’ve already launched.

Stablecoins have moved from a crypto niche to systemically relevant financial plumbing. The global stablecoin market cap is now in the hundreds of billions of dollars, with on-chain transfer volumes measured in the tens of trillions per year, rivaling or surpassing card networks.

In parallel, regulators in the US and EU have passed dedicated stablecoin frameworks such as the GENIUS Act and MiCA, signaling that tokenized money is here to stay.

Large banks like Goldman Sachs and JPMorgan are no longer just observing: JPMorgan has launched its JPMD USD deposit token on a public chain, while Goldman Sachs operates GS DAP and tokenized money-market fund infrastructure.

This article explains why, by early 2026, bank-issued stablecoins from these firms are likely to become core infrastructure for institutional settlement.

Key Takeaways

- Stablecoins have reached multi-trillion-dollar annual volumes, forcing large banks to move on-chain.

- JPMorgan’s JPMD and Goldman’s GS DAP + tokenized MMFs are bank-grade counterparts to USDC/USDT, built for institutional flows.

- New rules like GENIUS (US) and MiCA (EU) give banks a regulatory green light to issue their own tokenized cash.

- Bank-issued tokens aim to defend deposits, payment fees, and corporate relationships as non-bank stablecoin issuers grow.

- By Q1 2026, the big question isn’t “Will banks launch a stablecoin?” but “Which bank tokens will dominate institutional settlement rails?”

Stablecoins, Deposit Tokens, and Tokenized Cash - What’s the Difference?

What Counts as a “Stablecoin” in a Banking Context?

In crypto, a stablecoin is typically:

- A blockchain-based token designed to maintain a 1:1 peg to a fiat currency, usually the US dollar.

- Issued by entities like Tether (USDT) and Circle (USDC), backed by reserves such as cash, bank deposits, and short-dated government securities.

The broader “tokenized money” landscape now includes three main categories:

- Stablecoins (non-bank issuers)

- Fiat-backed tokens like USDT/USDC.

- Reserves held with banks and in Treasuries, but the issuer is typically a non-bank financial institution.

- Deposit Tokens (bank-issued)

- Tokenized versions of commercial bank deposits, issued by regulated banks.

- JPMorgan’s JPM Coin / JPMD are the textbook example: on-chain representations of deposits held at JPMorgan, available 24/7 to institutional clients.

- Central Bank Digital Currencies (CBDCs)

- Direct liabilities of a central bank.

- Still largely in pilot phase for major economies.

JPMorgan and other large banks stress that deposit tokens are not legally “stablecoins”, but functionally they share key attributes: 24/7 transferability, programmability, and a stable value anchored to a fiat currency.

Why This Article Still Uses “Bank Stablecoin”

From a user’s perspective, particularly corporates and funds:

- USDC, USDT, JPMD, and a hypothetical Goldman USD token all behave as on-chain cash, redeemable 1:1 for fiat.

- The legal wrapper (e-money, deposit, or payment token) matters for regulation and risk, but not for the basic function of settling trades in seconds.

So, while JPMorgan and Goldman will be very precise about not calling their products “stablecoins,” this article uses “bank stablecoin” as a functional label:

A bank stablecoin = a tokenized, 1:1 representation of bank money, issued by a regulated bank, used for payments, collateral, and settlement on a blockchain.

The 2026 Backdrop - Why Now?

Regulatory Green Light for Tokenized Cash

Two regulatory milestones changed the game:

- GENIUS Act (United States)

- The first comprehensive US federal framework for stablecoins.

- It sets requirements on reserve quality, redemption rights, and issuer supervision, heavily favoring regulated institutions.

- It effectively gives banks and bank-like issuers a structural advantage in the US stablecoin market.

- MiCA (European Union)

- MiCA’s stablecoin regime applies across the EU, with strict rules on reserves, disclosures, and risk management for e-money tokens and asset-referenced tokens.

- By late 2025, initiatives like Qivalis, a euro stablecoin issuer backed by major European banks, have emerged explicitly as bank-issued, MiCA-compliant tokens.

In parallel, banks like BBVA have publicly stated plans to launch their own MiCA-compliant stablecoins around 2026, underlining that this is now mainstream strategy, not experimentation.

Macroeconomic and Market Pressures

International payments remain slow and expensive, especially across time zones and currencies, due to correspondent banking chains and limited operating hours.

Stablecoins have stepped into that gap:

- They are used for remittances, FX, and on-chain commerce, often with lower fees and faster settlement than legacy channels.

- Stablecoin transaction volumes have already reached levels comparable to, or higher than, global card networks.

Regulators and institutions now explicitly acknowledge that stablecoins can improve payment speed and cost, especially for remittances and cross-border flows, while also warning about financial-stability and AML risks.

Competitive Threat from Non-Bank Stablecoin Issuers

Non-bank issuers have captured a massive lead:

- The stablecoin market has grown to around $300 billion in 2025, with USDT and USDC dominating.

- Major research desks project that stablecoin market cap could realistically reach $500–750 billion in the coming years.

If banks do nothing, deposits and payment flows leak to:

- Fintechs and crypto exchanges that integrate USDC/USDT as primary rails.

- New consortia and platforms that don’t necessarily require a traditional bank in the middle.

The strategic answer from big banks:

Issue their own on-chain money.

Goldman Sachs - From GS DAP to Bank-Grade Stablecoin Rails

GS DAP – The Tokenization Rail Goldman Already Controls

Goldman Sachs’ GS DAP is a digital-asset platform built on the Canton Network, designed for regulated markets and privacy-sensitive participants.

Key points:

- It supports tokenization of bonds, funds, and other RWAs, with fine-grained privacy and compliance controls.

- Canton is engineered for interoperability between regulated institutions, not public DeFi.

- Goldman has signaled plans to position GS DAP as a broader industry platform, not just an internal tool.

Tokenized Money-Market Funds as a Stepping Stone

In 2025, BNY and Goldman announced a tokenized money-market fund solution:

- BNY uses GS DAP to record customers’ ownership of selected MMFs.

- Investors can subscribe and redeem MMF shares through BNY’s Liquidity-Direct portal, while mirrored tokenized records sit on GS DAP.

This matters because:

- MMFs are effectively cash-like instruments for institutions.

- If MMF shares can be mirrored as tokens and moved across tokenized venues, then adding tokenized cash legs is the obvious next step, so trades can settle fully on-chain.

Why a Goldman-Branded Tokenized Cash Instrument Is the Next Logical Step

Goldman is not publicly promising a “Goldman stablecoin” by name. But the strategic direction is clear:

- GS DAP already handles tokenized assets; pairing that with tokenized cash lets trades settle in atomic, programmable ways.

- Goldman’s research openly frames stablecoins and tokenized cash as a multi-trillion-dollar opportunity for capital markets.

Use-cases that logically push Goldman toward its own tokenized cash:

- Securities and repo settlement on tokenized rails.

- On-chain collateral for derivatives and structured products.

- Liquidity for tokenized Treasuries, funds, and structured credit, where clients want cash and assets on the same infrastructure.

In that context, a Goldman-issued tokenized USD liability (whether branded as a deposit token or e-money) is a natural extension of GS DAP, and Q1 2026 is a realistic window for production-scale institutional usage, given the pilots already live.

JPMorgan - JPM Coin, JPMD, and the Path to On-Chain Bank Money

From Private JPM Coin to Public-Chain JPMD

JPMorgan has been at this longer than almost anyone:

- It launched the JPM Coin payment system on its Onyx blockchain platform in 2019 for wholesale clients.

- JPM Coin has been used for intraday repo and other institutional transactions, enabling near-instant settlement of trades that previously relied on slower traditional rails.

In 2025, JPMorgan went further:

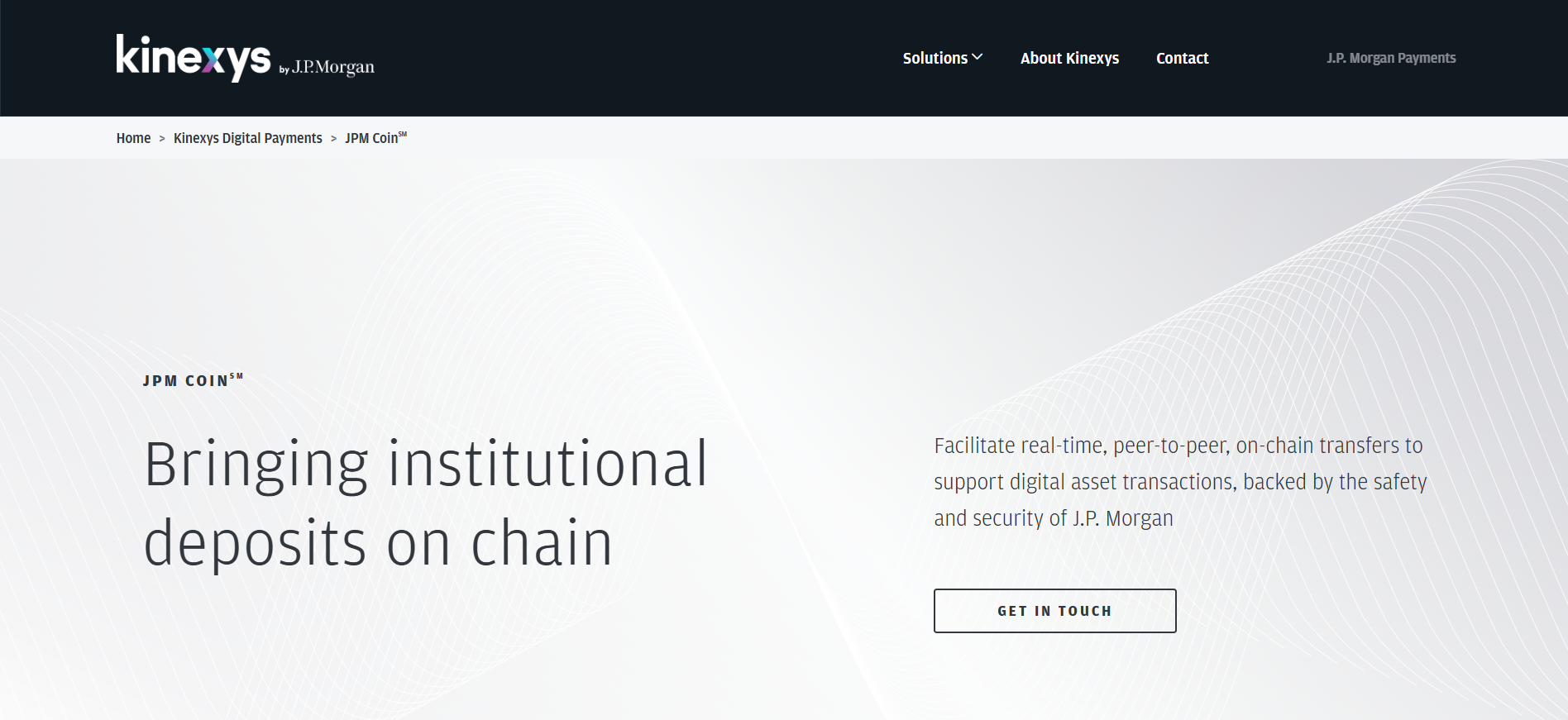

- It announced JPMD, a USD deposit token for institutional clients, issued under its Kinexys unit.

- JPMD is live on Base, an Ethereum Layer 2, giving clients on-chain settlement in seconds with tokenized commercial bank money instead of USDC/USDT.

JPMorgan emphasizes that JPMD is not a “stablecoin” but a deposit token:

- It is treated as a commercial bank deposit on a client’s balance sheet.

- It inherits the regulatory and supervisory framework of JPMorgan’s core banking business.

Functionally, though, it looks like a bank stablecoin for institutions.

Strategic Goals Behind JPM’s On-Chain Cash

JPMorgan’s deposit-token strategy clearly aims to:

- Defend and deepen corporate relationships in trade, FX, and treasury.

- Reduce reliance on legacy correspondent banking flows for certain corridors by allowing clients to move funds 24/7 on public or permissioned blockchains.

- Prepare for a world where tokenized collateral and securities dominate capital markets.

By Q1 2026, JPMD’s trajectory is likely to be:

- More currencies beyond USD.

- More chains beyond Base.

- Deeper integration with treasury systems, trading platforms, and tokenized asset venues.

Why Q1 2026 Is a Realistic Inflection Point

Again, there is no official press release that says “Goldman and JPM will both launch brand-new stablecoins in Q1 2026.”

But several forces converge around that time frame.

From Pilots to Production

By late 2025:

- JPMD is live on Base for institutional clients, following months of pilots with major partners.

- GS DAP is connected to BNY’s tokenized MMF solution, with real client flows via Liquidity-Direct.

Legal and tech work for these platforms has been underway since 2019–2020.

Large banks typically:

- Run limited-scope pilots for 12–24 months.

- Then open products to wider institutional usage once regulatory, risk, and operational issues are resolved.

Q1 2026 fits naturally as the moment when tokenized cash moves from “pilot” to “core product” in client conversations.

Aligning with Global Regulatory Milestones

The timing also matches regulatory cycles:

- US stablecoin law (such as GENIUS) is in place, with implementation and supervision ramping up through 2025–2026.

- MiCA is fully in force in the EU, and projects like Qivalis target a 2026 launch for a MiCA-compliant euro stablecoin backed by major EU banks.

- European banks like BBVA are publicly targeting 2026 for their own stablecoin initiatives.

The message to US and global banks is obvious:

If they don’t act now, others will define the standard.

How Big-Bank Stablecoins Will Actually Work

Technical Architecture - Private, Public, or Hybrid?

Different banks are converging on a hybrid design:

- JPMorgan

- Private Onyx networks for internal and bilateral flows.

- Public Base L2 for JPMD, bringing institutional money onto a mainstream public chain while preserving strict client onboarding and controls.

- Goldman Sachs

- GS DAP on Canton, a permissioned network with privacy-by-design aimed at regulated markets.

- Integration with BNY Digital Assets and Liquidity-Direct suggests that tokenized MMFs and any future tokenized cash instruments will circulate within permissioned institutional ecosystems.

In practice, we should expect:

- Permissioned rails for KYC’d banks, brokers, asset managers, and corporates.

- Gradual interoperability between private and public networks using bridges, wrapped tokens, or standardized messaging.

Backing, Reserves, and Risk Management

One of the main selling points of bank-issued tokens is risk profile:

- Deposit tokens like JPMD are claims on a regulated bank and sit within existing bank capital, liquidity, and supervisory regimes.

- Stablecoins and deposit tokens under GENIUS and MiCA must hold high-quality liquid reserves, typically cash and short-dated government securities, with strict disclosure rules.

This is a direct response to past disasters like algorithmic stablecoins, which regulators now describe as unacceptable for large-scale usage.

Compliance by Design

Banks are designing these products around compliance rather than trying to retrofit controls later:

- Wallet whitelisting and KYC at the account level.

- Continuous transaction monitoring, with the ability to block or reverse flows tied to sanctions or financial crime.

- Automated integration with AML, sanctions, and travel-rule tooling, which regulators already expect of large banks.

This is one of the key differences versus open stablecoins like USDT/USDC, which can circulate freely on public chains until they interact with a regulated on- or off-ramp.

Who Will Actually Use Goldman and JPM Tokens?

Target Users and Use Cases

The initial users are not retail.

They’re institutions that already bank with Goldman and JPMorgan:

- Large corporates and multinationals

- Intra-group cash sweeps across subsidiaries.

- Just-in-time funding of payroll, supplier payments, and FX.

- Asset managers, hedge funds, and liquidity providers

- Margin and collateral for derivatives and repo.

- Settlement for tokenized Treasuries, MMFs, and structured products.

- Financial market infrastructures (FMIs)

- Clearing and settlement utilities exploring DLT-based netting and collateral management.

How This Differs from USDC/USDT Adoption

Comparing bank tokens to USDC/USDT:

- Access

- USDC/USDT: anyone with a wallet can hold and transfer them.

- JPMD/GS-style tokens: restricted to KYC’d institutional clients.

- Ecosystem

- USDC/USDT: deeply embedded in DeFi, exchanges, and retail trading.

- Bank tokens: designed for closed or semi-closed institutional ecosystems, at least initially.

- Risk and regulation

- Bank tokens inherit the bank regulatory stack; stablecoins rely on their own regimes and issuer governance.

In other words, USDC/USDT are for the crypto frontier; bank tokens are for the regulated core.

Impact on Existing Stablecoin Issuers and Payment Networks

Pressure on Non-Bank Stablecoin Issuers

As bank tokens scale:

- Banks can argue: “Why hold a non-bank stablecoin when you can hold a direct claim on a GS or JPM deposit?”

- Policy and industry analyses expect bank-issued stablecoins and crypto-currencies to be among the fastest-growing forms of digital money for securities payments by 2030.

However:

- Non-bank issuers may still dominate retail and DeFi use cases, especially outside G7 banking systems.

- Research from major banks still projects strong growth for the broader stablecoin market (bank and non-bank combined) into the $500–750 billion range.

SWIFT, Card Networks, and Fintechs

Bank-issued tokens threaten several existing business lines:

- Correspondent banking & SWIFT

- If G10 corporates can settle in minutes on a bank-token network, some traditional cross-border payment flows will migrate off SWIFT.

- Card networks and PSPs

- Real-time on-chain settlement between merchants and treasurers could reduce reliance on card rails for certain B2B transactions.

- Fintechs

- Fintechs that built their value on faster settlement and better FX will now compete with bank-issued tokens that offer similar benefits but plug directly into the balance-sheet capacity and regulatory privileges of large banks.

Risks, Trade-Offs, and Open Questions

Fragmentation: A Stablecoin for Every Bank?

A real risk is fragmentation:

- Dozens of different bank tokens, such as JPMD, a Goldman token, euro tokens from Qivalis, BBVA, and others, could lead to walled gardens that don’t interoperate.

Projects like Qivalis and emerging G7 stablecoin consortia aim to address this by:

- Creating shared, multi-bank stablecoins that multiple institutions can issue and redeem.

But it’s not yet clear whether:

- Banks will prioritize co-opetition (shared rails) or closed ecosystems (each bank pushes its own token).

Regulatory and Policy Risks

Authorities are watching this very closely:

- International bodies warn that large-scale stablecoin and deposit-token usage could affect monetary policy, capital flows, and financial stability, especially if tokens start to substitute for bank deposits or migrate across borders at scale.

- China, for example, has taken the opposite path, explicitly declaring all stablecoins illegal and pushing its own e-CNY instead.

Future tightening of capital, liquidity, and disclosure rules for bank tokens is almost certain, especially if volumes rival card networks or traditional wholesale payment systems.

Technology, Security, and Operational Risks

Even if the issuer is a blue-chip bank, the underlying infrastructure remains software:

- Smart-contract bugs, chain downtime, or bridge exploits can disrupt token operations.

- Reliance on third-party L2s or blockchain vendors introduces vendor risk that regulators will scrutinize.

Banks will need:

- Redundant settlement paths (on-chain and off-chain) for high-value flows.

- Clear operational playbooks for incident response when something goes wrong at the chain layer.

Conclusion

By early 2026, Goldman Sachs and JPMorgan are on track to turn tokenized money from a pilot experiment into core infrastructure for institutional settlement.

Stablecoins and deposit tokens give them a way to defend deposits, capture new payment flows, and stay relevant in a world where tens of trillions move across public and permissioned blockchains.

Regulatory frameworks like GENIUS and MiCA are pushing this evolution forward by rewarding well-capitalized, tightly supervised issuers. At the same time, bank-issued tokens will coexist and compete with non-bank stablecoins, card networks, fintechs, and, eventually, CBDCs.

For corporates, funds, and infrastructure providers, the real work in 2026 is not debating definitions, but upgrading systems, policies, and strategies to operate on bank-grade on-chain rails.

Read Next:

FAQs:

1. Are Goldman Sachs and JPMorgan officially launching a stablecoin in Q1 2026?

No public document says “we will launch a new retail stablecoin in Q1 2026.” What is public is that JPMorgan has launched JPMD, a USD deposit token on Base, and Goldman’s GS DAP plus tokenized MMFs are already live. Q1 2026 is a realistic horizon for these bank tokens to become mainstream tools in institutional settlement.

2. How are bank-issued deposit tokens different from USDC or USDT?

Deposit tokens like JPMD are claims on a regulated bank deposit, falling inside bank capital and liquidity rules. USDC/USDT are issued by non-bank entities, even if their reserves sit in banks and Treasuries. Both are 1:1 tokens on a blockchain, but their legal status, supervision, and risk profile differ significantly.

3. Will Goldman and JPM tokens be available to retail users?

Current designs are strictly institutional. JPMD is available only to institutional clients of J.P. Morgan, and GS DAP/BNY tokenized MMFs target institutional and corporate users. There is no public plan to let retail users hold these tokens directly.

4. What risks do bank stablecoins pose to financial stability?

Large-scale stablecoin and deposit-token use could affect monetary policy, capital flows, and run risk, especially if tokens start to substitute for bank deposits or move across borders at scale. That’s why regulators impose reserve, disclosure, and governance requirements and are watching bank tokens very closely.

5. How will bank tokens interact with CBDCs?

Most central banks expect coexistence: CBDCs for central-bank-level money, bank tokens for commercial bank money, and both connecting into tokenized capital markets. Deposit tokens are generally seen as complements to CBDCs, not replacements.

6. What does this mean for existing stablecoin issuers like Circle and Tether?

They are unlikely to disappear. Instead, the market will likely segment: non-bank stablecoins for crypto-native and retail flows, bank tokens for regulated institutional flows. But bank tokens will challenge non-bank issuers in high-value, compliant corridors, especially in G7 markets.

7. How should corporates and funds prepare for bank-grade on-chain settlement?

Concrete steps include updating treasury and ERP systems to interact with tokenized cash and assets, reviewing legal, accounting, and tax treatment of deposit tokens and tokenized securities, and running pilot projects with tokenized MMFs, repo, or cross-border payments via bank-token platforms.

{kind=link}