Table of Contents

Over the last few years, stablecoins have steadily moved out of the crypto niche and into a much more consequential role: business infrastructure.

In a conversation between Chiara Munaretto, Managing Partner at Stablecoin Insider, and Avinash Chidambaram, Founder and CEO of Cybrid, the discussion centered on a market that is no longer defined by experimentation, but by integration.

The message was clear: stablecoins are becoming embedded into the financial workflows of companies that want faster payments, better treasury control, and less dependence on outdated banking rails.

A Shift From Crypto Product to Financial Rail

The broader stablecoin market has matured significantly over the last decade. What was once experimental now increasingly sits inside more regulated, enterprise-ready infrastructure.

That matters because businesses do not adopt technology for ideological reasons. They adopt it when it improves execution.

For finance teams, treasury departments, and global operators, the appeal of stablecoins is straightforward: they can offer faster settlement, greater visibility, more flexibility in how money moves, and a better foundation for automation.

“What businesses care about is not the technology itself, but whether the rail is faster, cheaper, and easier to integrate into their operations.” - Avinash Chidambaram, Founder and CEO of Cybrid.

In that sense, the conversation around stablecoins is moving away from crypto language and closer to the language of payments, treasury, and enterprise software.

Why Stablecoins Are Winning Business Attention

A major reason stablecoins are gaining traction is that traditional payment infrastructure still carries significant friction:

- Cross-border wires remain slow

- Intermediary costs are often opaque

- Treasury workflows are still heavily manual

- Reconciliation can be fragmented

For companies operating across multiple markets, these inefficiencies compound quickly.

Avinash’s view is that stablecoins offer businesses a better underlying rail, especially when accessed through software. Rather than forcing companies to piece together banking partners, custody, compliance systems, reporting tools, and fiat ramps on their own, platforms like Cybrid aim to simplify access through a unified API layer.

That means a business can embed stablecoin functionality directly into its product or internal workflows without having to manage the full operational burden itself.

The Core Use Cases Already Taking Shape

The interview highlighted several areas where stablecoin infrastructure is already proving useful.

1. Cross-Border B2B Payments

This remains one of the clearest use cases.

Traditional international wires are often expensive, slow, and difficult to track across multiple intermediaries. Stablecoins create a more direct route for moving value.

Businesses can hold funds in digital dollars, move them globally, and convert into local currency only when needed.

That reduces delays, improves visibility, and can lower transaction costs for supplier payments and international business transfers.

2. Global Marketplace Payouts

Marketplaces with participants across multiple countries face similar problems. Paying sellers, contractors, or vendors through legacy rails can create delays and inefficiencies, especially when each recipient operates in a different banking environment.

Stablecoin rails create a more uniform payout layer, allowing marketplaces to move funds faster and with fewer operational constraints.

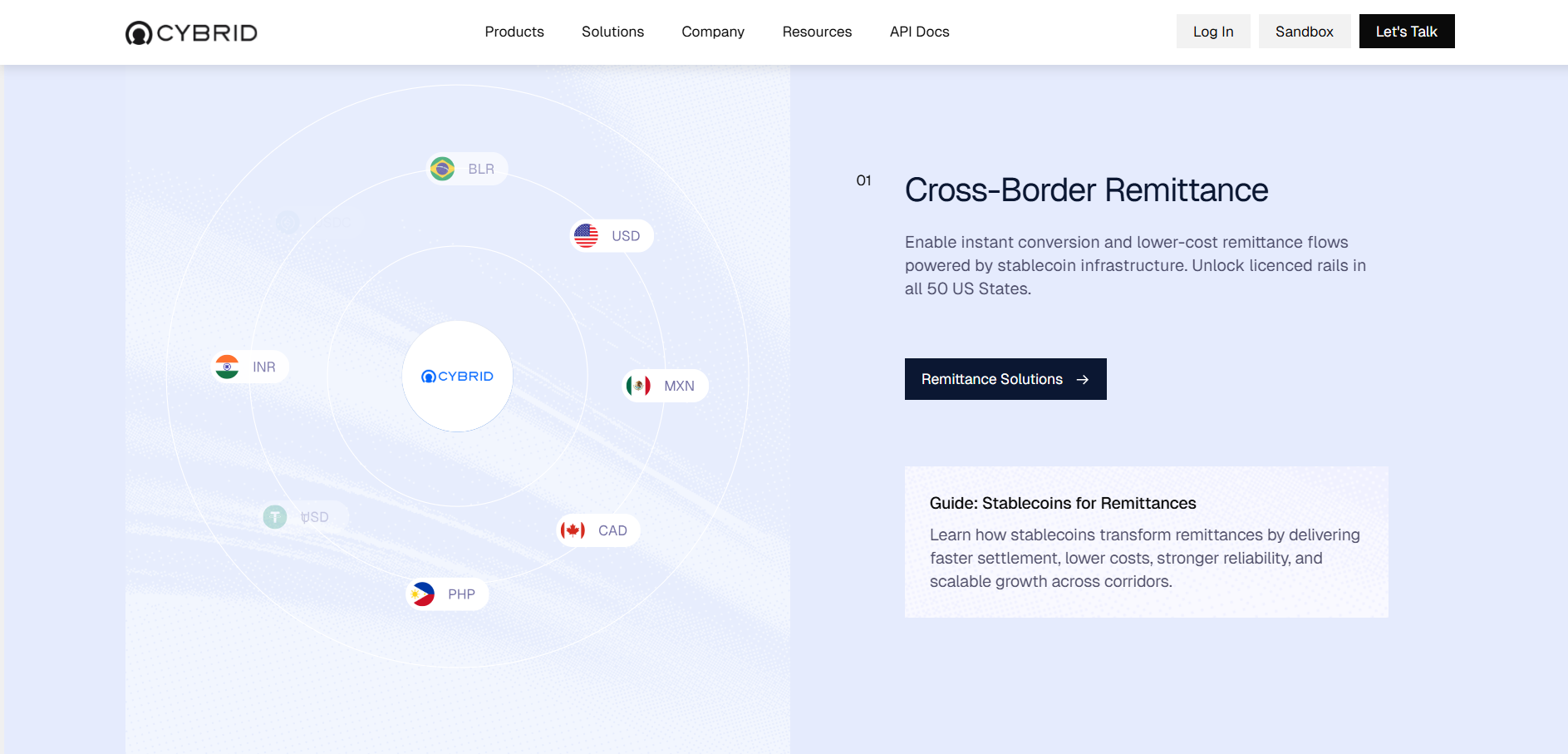

3. Remittances

The interview also pointed to remittance corridors as a strong fit. Instead of forcing a recipient to immediately convert into local currency, stablecoin-based transfers can give them the option to hold value in digital dollars and convert only when needed.

That flexibility can matter in markets where local currency volatility or banking friction remains high.

The Rise of Programmable Treasury

One of the most important ideas in the conversation was the emergence of programmable treasury.

This goes beyond simply moving money faster. It points to a world where stablecoin rails become part of automated business operations.

Avinash described how ERP systems and AI-enabled workflows are increasingly capable of identifying operational needs, generating purchase orders, routing approvals, and triggering payments once authorized.

“Once payments can be triggered directly from ERP and treasury workflows, the finance team spends less time on execution and more time on strategy.” - Avinash Chidambaram, Founder and CEO of Cybrid.

In that model, stablecoins are not a separate product sitting outside the company’s systems. They become part of the workflow itself.

That has important implications for finance teams. The less time spent manually handling payment mechanics, the more time treasury leaders can spend on capital planning, controls, liquidity management, and strategy.

This is especially relevant in supply chains. If a supplier can verify on-chain that a payment has been initiated, production can begin much sooner than under traditional banking timelines. The payment rail becomes faster, but just as importantly, it becomes more transparent and more actionable.

Regional Banks and the Next Payment Layer

Another notable theme was the role regional banks may play in this transition.

Rather than being pushed out entirely, many smaller banks are beginning to use stablecoin infrastructure to offer better international payment services. By using stablecoins as a transaction rail, they may be able to avoid some of the cost and complexity associated with correspondent banking systems.

This could be especially valuable in regions where traditional banking infrastructure is less efficient or where international liquidity is harder to access.

The interview pointed to strong activity in North American payment corridors as well as in remittance-heavy markets such as India, the Philippines, Mexico, and Brazil.

Latin America in particular appears to be an area where the practical value of stablecoins is often easier to see, largely because the inefficiencies of legacy systems are more visible there than in some European or North American markets.

Stablecoins as a Complement, Not a Replacement

One of the more pragmatic points in the discussion was that stablecoins are not necessarily replacing traditional banking. At least not entirely.

Instead, Avinash framed them as an additional rail that businesses can use when it makes sense. Cards, domestic payment systems, bank transfers, and stablecoin routes may all coexist. The real opportunity lies in orchestration.

In other words, companies should not have to manually choose a payment rail every time they move money. A modern infrastructure layer should automatically determine the fastest, cheapest, and most effective route based on the transaction itself.

That abstraction may end up being one of the most important developments in the sector. The more invisible the underlying complexity becomes, the easier stablecoin infrastructure will be for mainstream businesses to adopt.

Liquidity, Regulation, and the Road Ahead

The conversation also addressed the two constraints that continue to shape adoption: liquidity and regulation.

1. Liquidity

Liquidity fragmentation remains a real issue, especially for larger transfers. When businesses need to move significant amounts, they want to do so without moving the market or creating slippage.

Today, that often requires routing through multiple liquidity providers or specialized trading venues.

As the market matures, that infrastructure is expected to improve. More market makers may begin supporting direct stablecoin-to-local-currency pairs, which would make large-scale flows more efficient and reduce current bottlenecks.

2. Regulation

Regulatory clarity is also becoming a key enabler.

One of the most important shifts discussed in the interview is that finance and compliance teams now have a stronger framework for understanding stablecoins as a distinct category, separate from more volatile crypto assets.

High-quality stablecoins backed by cash and treasuries are increasingly being assessed as payment infrastructure rather than speculative instruments.

That said, regulators are still focused on broader system-level questions, especially whether stablecoin adoption could pull deposits away from traditional banks and affect lending or credit markets.

In some regions, geopolitical and sovereignty concerns will also shape how stablecoin infrastructure develops.

The Question of Issuing Proprietary Stablecoins

The interview also explored whether businesses should issue their own stablecoins.

Chidambaram answered that in some closed-loop ecosystems, issuing a proprietary stablecoin may be useful. A large platform with internal fund flows, for example, may have a good reason to create its own asset.

But for many businesses, the smarter path may be to use an existing, widely accepted stablecoin rather than introducing a new layer of complexity.

Established assets already benefit from market-maker support, broader interoperability, and stronger liquidity.

The takeaway is simple: businesses should issue a stablecoin only when there is a clear operational reason to do so, not because the concept sounds strategically attractive.

Final Take

The most revealing part of the conversation was not about blockchain mechanics. It was about business behavior.

Companies are increasingly less interested in the technical language of crypto and more interested in practical outcomes. They want:

- Faster settlement

- Better transparency

- Easier treasury management

- Cleaner cross-border execution

- More automation

That shift changes the entire conversation.

For Cybrid, the opportunity is not to convince businesses to become crypto-native. It is to help them access a better financial rail through systems they already use.

And for the wider industry, that may be the real test of maturity: when stablecoins stop needing to be explained as innovation and start being adopted because they are simply better infrastructure.

At that point, the technology fades into the background.

The operational advantage does not.

Read Next:

{kind=link}