Table of Contents

Ottawa, December 22, 2025

The Canadian federal government has tabled draft legislation for a new Stablecoin Act as part of Bill C-15, the Budget 2025 Implementation Act.

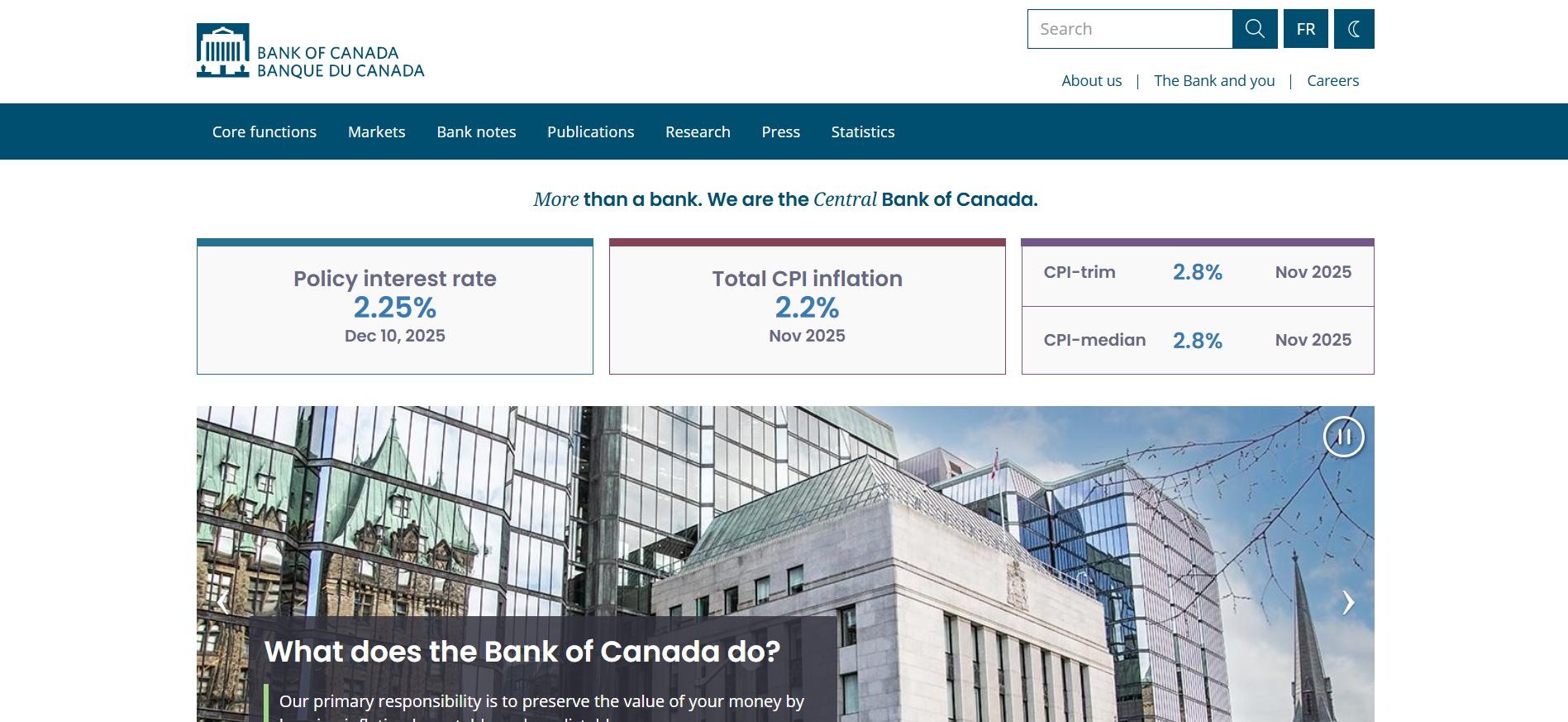

Introduced on November 4, 2025, the proposed Act establishes a national prudential framework for fiat-referenced stablecoins issued by non-regulated entities, with oversight assigned to the Bank of Canada.

The legislation targets stablecoins designed to maintain a stable value pegged to a single fiat currency, primarily through reserves.

It excludes asset-backed stablecoins (e.g., gold), central bank digital currencies (CBDCs), stablecoins issued by federally regulated financial institutions, closed-loop systems (where holders cannot withdraw outside the ecosystem), and those without interprovincial or international reach.

Key Takeaways

- Register with Bank of Canada to issue fiat-referenced stablecoins legally in Canada.

- Maintain 1:1 reserves in high-quality liquid assets with qualified custodians.

- Ensure full, at-par redemption rights without yield or interest offerings.

- Implement disclosed governance, risk, and cybersecurity policies.

- Comply with monthly reporting and independent verifications.

Background and Regulatory Context

Prior to this draft, stablecoins in Canada fell under provincial securities regulation. The Canadian Securities Administrators (CSA) treated many fiat-referenced stablecoins as "value-referenced crypto assets" (VRCAs), potentially classifying them as securities or derivatives.

This required platforms to comply with disclosure, prospectus, and registration rules, creating barriers for payment-focused use cases.

The new federal approach shifts oversight to the Bank of Canada, treating compliant stablecoins as payment instruments rather than investments. This aligns Canada with jurisdictions like the United States (GENIUS Act), United Kingdom, and Hong Kong, which regulate stablecoins under banking or payments frameworks.

The Act responds to industry calls for clarity, aiming to foster innovation while addressing risks to consumers, financial stability, and monetary sovereignty. Bank of Canada Governor Tiff Macklem has emphasized that regulated stablecoins must function as "good money", fully redeemable at par, backed by high-quality assets, and safe for everyday use.

Concurrently, amendments to the Retail Payment Activities Act (RPAA) expand its scope to include tokenized payment instruments, bringing stablecoin wallets, custodians, and transfer services under Bank of Canada supervision for operational risks.

Key Requirements for Stablecoin Issuers

The draft Act imposes strict obligations on issuers targeting Canadian users:

- Mandatory Registration: Issuers must apply for listing on a public Bank of Canada registry. Applications require detailed disclosures on ownership, technology stack, governance, risk management, cybersecurity, redemption processes, and reserve management. Independent legal opinions and financial verifications are mandatory.

- 1:1 Reserve Backing: Reserves must equal or exceed outstanding stablecoins in value, held in the reference fiat currency or prescribed high-quality liquid assets (expected to include Government of Canada treasury bills and insured deposits). Assets must be segregated, unencumbered, and bankruptcy-remote.

- Qualified Custody: Reserves held by approved custodians, likely limited to federally regulated trust companies or banks with Bank of Canada authorization.

- Redemption Rights: Holders entitled to redeem at face value with clear, disclosed terms on timing and fees. No yield or interest permitted, directly or indirectly, to distinguish from investment products.

- Governance and Policies: Issuers must implement and publish policies on governance, conflicts, data security, operational resilience, recovery/resolution planning, and AML/ATF compliance.

- Reporting and Verification: Monthly accountant statements on reserves and outstanding supply; periodic audited reports and legal compliance opinions.

- Prohibitions: No misleading claims (e.g., implying government backing or deposit insurance). National security reviews possible for foreign-linked issuers.

The Bank of Canada gains broad supervisory powers, including inspections, directives, suspensions, and revocation of registration for non-compliance.

Provincial securities laws remain applicable unless harmonized, potentially requiring dual compliance for distribution or trading.

Implications for Industry and Consumers

The framework prioritizes consumer protection by ensuring redeemability and reserve integrity, reducing risks seen in past stablecoin failures. It legitimizes stablecoins for payments, cross-border transfers, and integration with real-time rail systems.

For issuers, compliance costs will rise, favoring established players. Industry groups seek 12-24 month transition periods; a targeted consultation on reserves and grandfathering closed in December 2025.

Payment service providers handling stablecoins face RPAA registration, adding operational safeguards.

Overall, the Act positions Canada to capture digital payment innovation while maintaining financial system integrity.

Conclusion

Canada's draft Stablecoin Act marks a pivotal shift toward regulated digital payments, balancing innovation with strict safeguards.

Finalization will shape stablecoin adoption, consumer trust, and Canada's competitiveness in global digital finance.

Read Next:

- Best Chain for Stablecoin Micropayments in 2026

- Best Stablecoin On/Off-Ramps for 2026 Compared

- How to Pay Influencers in Stablecoins in 2026

FAQs:

1. What is the Stablecoin Act?

A proposed federal law creating prudential oversight for fiat-referenced stablecoins by non-regulated issuers, administered by the Bank of Canada.

2. Who does it apply to?

Issuers of stablecoins available to Canadians, excluding banks, central banks, closed-loop systems, and non-fiat backed tokens.

3. When will it take effect?

Bill C-15 likely receives royal assent in spring 2026; implementation phased, with regulations and transition periods to follow.

4. Can stablecoins pay interest?

No, yield-bearing stablecoins fall outside the regime and may trigger securities rules.

5. How does it interact with provincial securities laws?

It provides federal carve-outs but does not override provincial regulation; CSA guidance expected for harmonization.

6. Are existing stablecoins grandfathered?

No provision in draft; industry pushes for transition relief.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}