Table of Contents

Tokenized Money Market Funds (tokenized MMFs) take a familiar cash + yield product and package it in a blockchain-compatible form factor: a digital token that represents a regulated fund share (or a closely related share class).

In 2026, this category is no longer a lab experiment, it’s a fast-growing bridge between traditional cash management and on-chain settlement rails.

What’s changed is distribution and settlement, not the core promise of a money market fund: stability of principal, daily income (in most structures), and high liquidity.

The practical question for most buyers is no longer if tokenization real, it’s which structure is safest, what risks am I actually taking, and how do I operationalize this?

Key Takeaways

- Tokenized MMFs deliver cash-like yield as blockchain-based fund shares.

- The market is scaling fast, with multiple $100M–$1B+ products live.

- Transferability ≠ redeemability; always verify mint/redeem windows.

- Risk is mostly structural and operational: eligibility, custody, and liquidity terms.

- Choose funds by mandate, fees, controls, and redemption mechanics, not by chain hype.

What Is a Tokenized Money Market Fund?

A tokenized money market fund is a money market strategy where the investor’s holding is represented digitally on a blockchain.

Depending on the structure, the token can be:

- A direct tokenized share (or share class) of a regulated MMF, where the token itself is the record of ownership (or tightly linked to it), and transfers are constrained by compliance rules; or

- A mirror token or representation, where traditional fund records remain canonical but tokens mirror holdings for settlement/automation (common in bank-led initiatives).

In both cases, the economic exposure typically resembles a conservative cash-equivalent product: short-duration U.S. Treasury bills/notes, government repo, and similar instruments, designed to preserve principal and deliver yield.

Why it matters in 2026

Tokenization makes MMFs usable in contexts where classic fund plumbing is slow or closed (weekends, holidays, cross-border settlement, intraday collateral).

If you run a crypto-native balance sheet, a stablecoin treasury, or an institutional trading desk, tokenized MMFs can turn idle cash into yield while keeping assets closer to the rails where they’re needed.

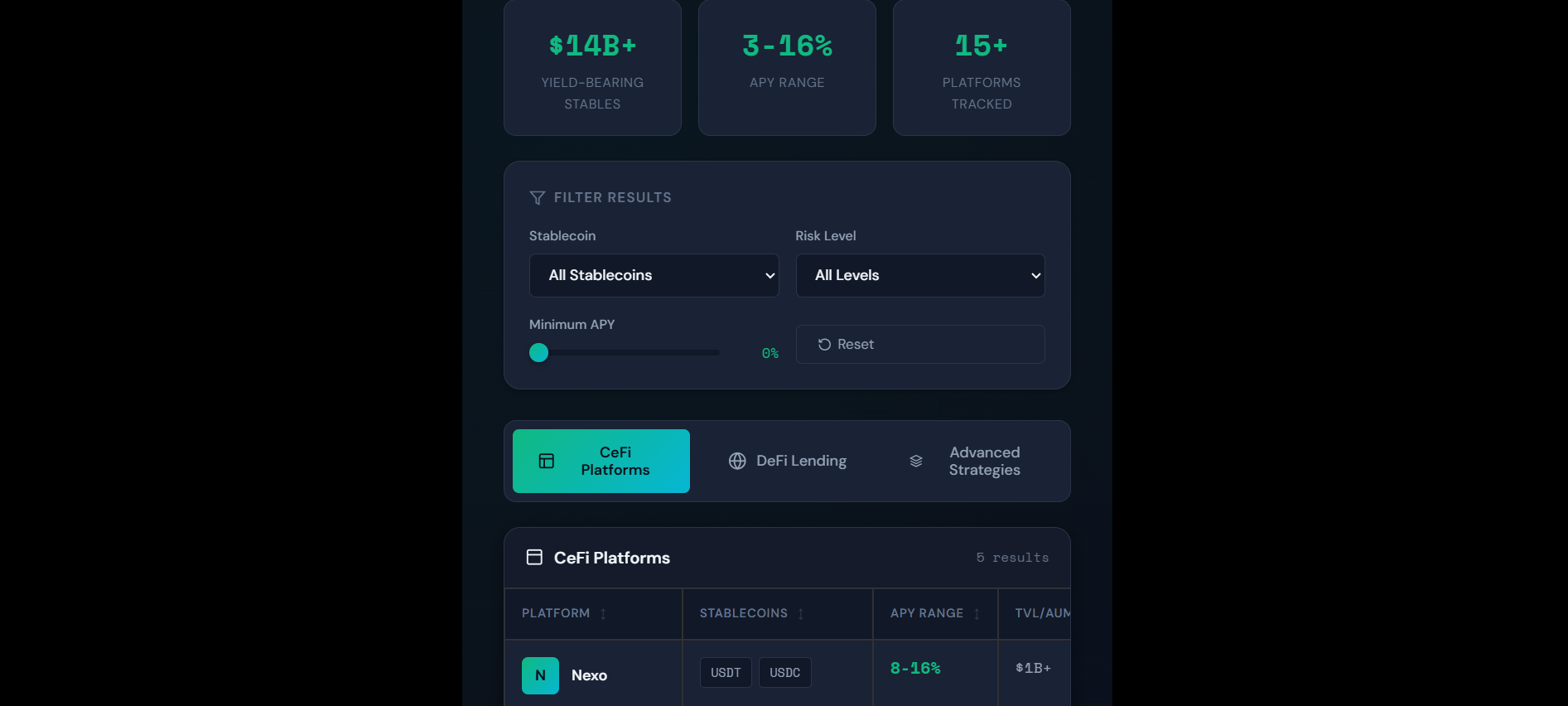

Market Reality Check: Adoption and Scale in 2025–2026

Multiple reputable sources tracked a sharp rise in tokenized Treasury/MMF products through 2025, including a reported $7.4B figure for tokenised Treasury and money market mutual funds in 2025.

At the ecosystem level, RWA analytics show meaningful breadth: $24.36B distributed asset value and 833,663 total asset holders (Feb 2026 snapshot).

Flagship products (illustrative, not exhaustive)

- BlackRock BUIDL: $1.783B total asset value, 110 holders, and a displayed 7D APY ~3.43% in the snapshot.

- Franklin Templeton BENJI / FOBXX: BENJI shows $894M total asset value, 1,037 holders, and a displayed 7D APY ~3.54% in the snapshot.

- The issuer’s fund page also shows $766.02M total net assets as of 12/31/2025 for FOBXX (updated monthly).

- Fidelity Investments (OnChain class FYOXX): fund page shows $160.37M net assets as of 01/31/2026.

- J.P. Morgan Asset Management MONY launched Dec 15, 2025 on public Ethereum as a tokenized money market fund (private placement 506(c)), positioned for qualified investors.

The pattern is consistent: established managers are shipping real products, and market infrastructure is evolving to treat tokenized fund interests as usable collateral and settlement instruments.

How Tokenized Money Market Funds Work

Even though the surface looks crypto-native, the mechanics still map to classic fund operations.

A) The underlying portfolio

Most tokenized MMFs focus on:

- U.S. Treasury bills/notes

- Government repo collateralized by Treasuries

- Cash equivalents consistent with money market mandates

This is why these products tend to be discussed alongside tokenized Treasuries: functionally, they are cash management vehicles that can live on-chain.

B) Issuance, transfer, and compliance controls

Tokenized MMFs typically implement:

- Investor eligibility gates (e.g., qualified purchaser / accredited investor constraints)

- Whitelist/allowlist transfers

- Transfer agent / administrator workflows that align token movements with legal ownership and reporting obligations

In practice, a token may move peer-to-peer, but only among permitted addresses.

C) NAV, yield accrual, and distributions

Most products aim to keep a stable NAV (commonly $1.00 per share/token in the displayed examples), while distributing income daily or periodically.

For example, an official release describing BUIDL highlights daily dividend payouts and 24/7/365 peer-to-peer transfers (within the compliance perimeter).

D) Subscriptions and redemptions (the part most people miss)

This is where tokenized MMFs can differ materially:

- Some products offer near-continuous mint/redeem windows (subject to banking rails, liquidity management, and compliance checks).

- Others are still tied to traditional dealing cycles, with tokens primarily improving portability and integration, not liquidity.

When evaluating products, treat the 24/7 transferability and the 24/7 redeemability as two separate claims.

Why You Should Tokenize a Money Market Fund Instead of Using Stablecoins?

Stablecoins optimize for payments and settlement. Tokenized MMFs optimize for cash yield + capital preservation with fund-like governance and disclosures.

Here’s the simplest framing:

- Stablecoin = digital cash proxy (issuer risk, reserve model, redemption mechanics)

- Tokenized MMF = regulated cash-equivalent fund exposure (fund rules, liquidity buffers, portfolio transparency, distribution mechanics)

Many sophisticated treasuries use both:

- Stablecoins for movement and settlement

- Tokenized MMFs for yield on idle balances and/or collateralization for trading

This is also why large institutions are building tokenized MMFs into liquidity platforms; some initiatives explicitly focus on subscription/redemption flows for tokenized MMFs rather than DeFi composability.

Regulatory and Structural Foundations You Need to Understand

Tokenization doesn’t delete regulation, it concentrates it.

A) Money market fund reform and liquidity buffers

In the U.S., MMF resilience has been a repeated regulatory focus after stress events.

The SEC’s MMF reform framework highlights:

- stronger liquidity requirements,

- removal of temporary redemption gates,

- and a liquidity fee framework designed to allocate redemption costs more fairly.

This matters because tokenization can increase transfer velocity, and regulators care about run dynamics. Even if your token is transferable 24/7, the fund must still manage liquidity prudently.

B) Investor eligibility and distribution constraints

Many tokenized MMFs are limited to institutional investors, qualified purchasers, or other restricted cohorts. For example, RWA analytics for BUIDL explicitly shows eligible investors as “U.S. Qualified Purchaser.”

Bottom line: accessibility is improving, but anyone with a wallet is still not the default for regulated MMFs.

C) Transfer agent, custody, and legal ownership

Key question: What is the authoritative record of ownership?

- Onchain ledger as canonical record (with compliance controls), or

- Traditional book-entry record with tokens mirroring holdings

From a risk perspective, you care about:

- reconciliation processes,

- legal enforceability of token transfers,

- and what happens during outages, forks, sanctions events, or compliance freezes.

The 2026 Tokenized MMF Stack: Who Does What?

A typical production setup involves multiple specialized roles:

- Asset manager: portfolio construction, risk management, disclosures

- Tokenization platform / transfer agent: issuance, compliance gating, corporate actions

- Custodian: safekeeping of fund interests and/or private keys (depending on model)

- Settlement venues / prime brokers: collateralization, margin workflows

- Analytics providers: market transparency, flows, holders, cross-chain distribution

For example, a release about BUIDL notes it is tokenized by Securitize and emphasizes flexible custody and daily dividends (PR Newswire).

Due Diligence: The Checklist That Separates “Safe Yield” From “Hidden Risk”

If you’re evaluating tokenized MMFs for treasury, collateral, or client offerings, here are the questions that actually matter:

A) Product structure

- Is this a regulated MMF / mutual fund share class, a private fund, or something else?

- What’s the asset mandate (Treasuries only, repo, prime, etc.)?

- What is the NAV policy (stable vs floating), and what happens in negative rate environments?

B) Liquidity and redemption mechanics

- What are the subscription/redemption cutoffs?

- Is redemption in cash, stablecoin, or both?

- Are there fees triggered by market stress or large redemptions?

C) Transferability

- Are transfers restricted to whitelisted addresses?

- Can you move tokens cross-custody?

- Can you use the token as collateral with major counterparties?

D) Operational integrity

- Who is the transfer agent and administrator?

- How do they handle:

- corporate actions,

- distribution calculations,

- reconciliation,

- forks/network incidents?

E) Fees and economics

- Management fee, platform fees, custody fees, and any spread on mint/redeem conversions

Example: RWA analytics snapshot shows BUIDL management fee 0.20–0.50% and BENJI management fee 0.15%.

F) Concentration and counterparty risk

- Which banks, custodians, and repo counterparties are involved?

- Are there single points of failure in:

- stablecoin rails,

- KYC onboarding,

- platform governance?

Implementation Playbook: How Institutions Deploy Tokenized MMFs

Step 1: Define the objective

Common institutional objectives:

- Treasury yield on idle stablecoin/cash balances

- Collateral utility for derivatives/margin

- Cross-border cash management with faster internal settlement

- Client product (wealth, private banking, corporate cash)

Step 2: Choose your operating model

Most deployments fit one of three models:

- Treasury wallet model:

Your institution holds tokens directly in controlled wallets/custody accounts. - Prime broker / collateral model:

Tokens sit inside a margin ecosystem; utility depends on counterparty acceptance. - Platform distribution model:

You embed tokenized MMFs into a fintech/bank platform for end clients.

Step 3: Confirm eligibility + onboarding workflow

Don’t leave this late. Funds can be restricted, and onboarding can involve:

- entity verification,

- beneficial ownership checks,

- jurisdictional constraints,

- wallet address attestation.

Step 4: Integrate accounting + controls

You need policy decisions on:

- classification (cash equivalent vs investment security),

- valuation method (NAV feeds, end-of-day vs intraday),

- stablecoin yield recognition and distribution handling,

- key management and signing controls.

Step 5: Stress-test liquidity assumptions

Run scenarios:

- redemption spikes,

- banking holiday/weekend constraints,

- stablecoin rail outages,

- sudden compliance restrictions

This is also where MMF reform mechanics matter, because liquidity fee frameworks and other protections can affect redemption economics in stress.

Use Cases That Actually Drive Adoption in 2026

1) Crypto-native treasury management

Firms holding stablecoins for operations can park excess balances in tokenized MMFs for yield while staying close to on-chain settlement.

2) Collateral for trading and financing

Tokenized MMFs are increasingly discussed as high-quality collateral because they combine yield with portability.

This is one reason large institutions are experimenting with tokenized liquidity funds in collateral workflows (Financial Times).

3) Institutional cash sweep alternatives

If your organization already uses MMFs, tokenization can reduce friction in:

- internal transfers,

- cross-entity settlement,

- near-real-time visibility and controls.

4) Tokenized liquidity platforms

Banks and market infrastructure providers are integrating tokenized MMFs into subscription/redemption platforms, typically in controlled environments first.

Risks and Misconceptions

1. Misconception: Onchain means instant liquidity

Onchain transferability ≠ instant redemption. Redemption depends on fund terms, liquidity buffers, and operating rails.

2. Misconception: A token is the asset

Sometimes the token is the authoritative representation of ownership; sometimes it’s a mirror. Your legal and operational risk depends on which.

3. Real risk: Operational + compliance choke points

Tokenized MMFs are compliance-heavy by design. If your workflow depends on continuous movement, a whitelist restriction or transfer agent downtime can be more impactful than market volatility.

4. Real risk: Market stress behavior

MMFs are built to be resilient, but regulators focus on run dynamics for a reason. Reform frameworks explicitly target liquidity management and redemption cost allocation.

Conclusion

Tokenized money market funds are becoming the default cash yield primitive for institutions that operate near digital asset rails.

The category is scaling (with billion-dollar products and rapidly expanding holder bases) and attracting major managers and banks, yet the decision to deploy is still dominated by operational details: eligibility, custody, redemption mechanics, and accounting.

If you treat tokenized MMFs as a regulated fund product with a new settlement wrapper, and underwrite the wrapper as seriously as the portfolio, you’ll make better decisions than anyone chasing on-chain yield headlines.

Read Next:

- Top 10 Stablecoin Lending Platforms in 2026

- Trustless Stablecoins: The Complete 2026 Guide

- The Rise of Stablecoin Savings Apps

FAQs:

1. What are tokenized money market funds?

Tokenized money market funds are regulated cash-management funds whose shares are represented as blockchain-based tokens, enabling compliant digital ownership, transfer, and settlement of MMF exposure.

2. How do tokenized money market funds work in practice?

Tokenized MMF's work by minting tokens that represent fund shares (or a linked share class), applying compliance controls to ownership and transfers, and distributing yield based on the underlying money market portfolio.

3. What assets do tokenized money market funds typically hold?

Tokenized money market funds typically hold short-duration, high-quality instruments such as U.S. Treasury bills/notes, government repo collateralized by Treasuries, and other cash-equivalent holdings permitted by the fund mandate.

4. Are tokenized money market funds the same as stablecoins?

No, tokenized money market funds represent fund share ownership and yield from an underlying portfolio, while stablecoins are issuer-based digital cash instruments designed primarily for payments and settlement.

5. Do tokenized money market funds redeem 24/7?

Not always; tokens may transfer 24/7, but redemptions usually depend on the fund’s dealing terms, compliance checks, and operational rails, which can still follow traditional windows.

6. Who can invest in tokenized money market funds?

Access depends on the product structure and jurisdiction; many are restricted to institutional or qualified investors and require onboarding, eligibility verification, and approved wallet/custody arrangements.

7. What are the biggest risks of tokenized money market funds?

The main risks of tokenized MFF's are operational and structural: eligibility and transfer restrictions, custody/key-management controls, redemption mechanics under stress, and how legal ownership is recorded and reconciled.

8. What should I check before choosing a tokenized money market fund?

You should check the fund mandate, NAV and distribution policy, fees, mint/redeem cutoffs, transfer restrictions, custody model, administrator/transfer-agent setup, and stress-period liquidity and fee mechanics.

9. How are yields paid on tokenized money market funds?

Yields on tokenized money market funds are generated by the underlying portfolio and are reflected through distributions or accrual mechanics defined by the fund, often delivered on a daily or periodic schedule depending on the structure.

10. When do tokenized money market funds make sense for a business?

Tokenized MFF's make sense when a business needs cash-like exposure with yield while benefiting from blockchain-based settlement, portability, or collateral workflows, especially for treasury, trading, and cross-entity cash management.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}