Table of Contents

The stablecoin industry has a headline problem.

On one hand, raw blockchain data shows tens of trillions of dollars moving on-chain annually, which is a figure that has fueled breathless comparisons to Visa and Mastercard, and forecasts of an imminent SWIFT replacement.

On the other hand, a landmark February 2026 report from McKinsey & Company and Artemis Analytics strips all of that away and asks a blunter question: how much of it is an actual payment?

The answer, it turns out, is about 1%.

Of the roughly $35 trillion in annualized stablecoin transaction volume, only around $390 billion represents genuine end-user payments such as vendor invoices, cross-border remittances, payroll, and card spending. The rest is trading activity, internal fund shuffling, arbitrage, and automated smart-contract cycling.

Inflated headlines, the report concludes, should be "a starting point for analysis, not a proxy for payment adoption."

But within that honest $390 billion baseline, there is a story worth examining closely, and it centers almost entirely on the corporate treasury, not the consumer wallet.

B2B Owns the Room:

What the Numbers Actually Show

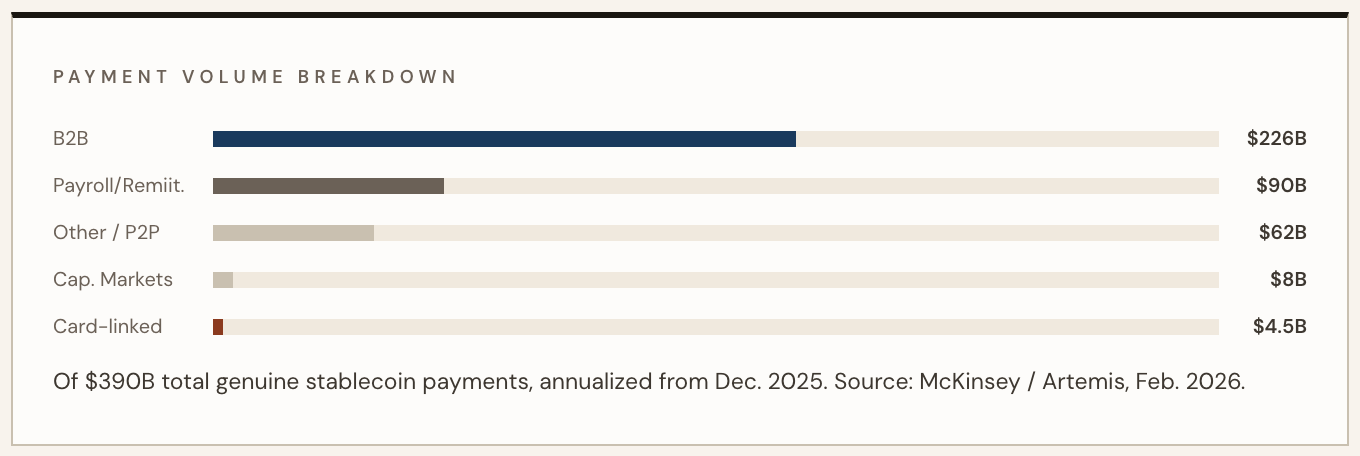

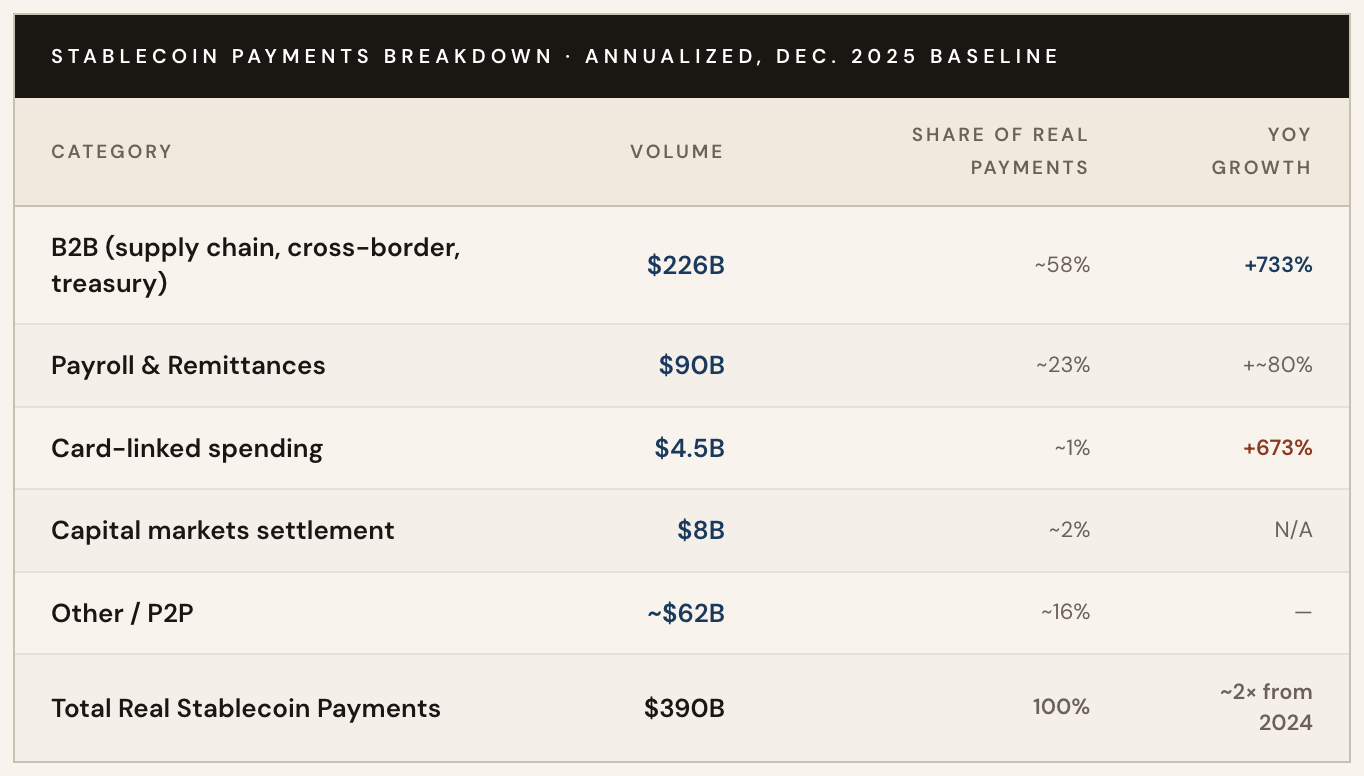

Business-to-business transactions account for $226 billion (roughly 58% of all genuine stablecoin payment volume) per the McKinsey/Artemis analysis, which used December 2025 activity as its baseline.

That figure represents a 733% year-over-year surge, driven primarily by supply chain payments, cross-border supplier settlements, and treasury liquidity management. Asia leads geographic activity, but adoption is accelerating across Latin America and Europe as well.

The rest of the real-payments universe is distributed across payroll and remittances ($90 billion), capital markets settlement ($8 billion), and card-linked spending ($4.5 billion).

Stablecoin-linked card volume grew an extraordinary 673% year-over-year according to McKinsey, but in absolute terms it remains a fraction of B2B flows.

For perspective: that $390 billion total represents just 0.02% of global payments volume, which McKinsey estimates at more than $2 quadrillion annually. B2B stablecoin flows specifically amount to roughly 0.01% of the $1.6 quadrillion global B2B payments market.

The numbers are large in stablecoin terms, but they remain microscopic in the context of the global financial system.

The monthly run-rate data tells the momentum story more viscerally. According to BVNK, citing the McKinsey/Artemis report, monthly stablecoin payment volume stood at just $5 billion in January 2024. By early 2026, that figure had surpassed $30 billion, which is a sixfold increase in under two years, with the steepest acceleration arriving in the second half of 2025.

Annualized, that run-rate now exceeds $390 billion.

"The fact that true stablecoin payments are much lower than routine estimates doesn't diminish stablecoins' long-term potential as a payment rail. Instead, it establishes a clearer baseline for assessing where the market stands". - McKinsey & Company / Artemis Analytics, February 2026

Why the Gap Exists:

Five Structural Forces Keeping Retail Out

The divergence between explosive B2B adoption and negligible consumer activity is not a coincidence. It is the product of structural asymmetries that systematically favor enterprise use cases over retail ones.

Here are the five forces driving the institutional gap:

1) Treasury Efficiency Beats Consumer Convenience

Corporate treasurers are motivated by concrete, measurable pain points: SWIFT correspondent banking chains that take one to five business days to settle, currency conversion windows that tie up working capital, and intermediary fees that compound across each transaction hop.

Stablecoins resolve all three simultaneously. For a company paying suppliers across fifteen countries, the economics are unambiguous. For a consumer buying coffee, they are not. The incentive to switch is orders of magnitude larger on the enterprise side.

2) Programmability Has No Retail Equivalent

The B2B explosion is partly a programmable payments story. Smart contracts enable conditional logic such as invoice triggers, delivery confirmations, escrow releases that can automate entire accounts-payable workflows at scale.

This is intrinsically suited to enterprise treasury operations, where high-value, structured, repeating payment flows benefit enormously from automation. Retail payments lack analogous trigger use cases at any scale.

Consumers do not need programmable conditions to buy groceries, they need something that works like a card. The cognitive complexity of blockchain-native payments remains a retail barrier that programmability does nothing to solve.

3) Regulatory Architecture Favors Institutions

Post-GENIUS Act, institutional operators have navigated the compliance architecture with AML/CFT, Travel Rule, licensing requirements and built the legal infrastructure to operate confidently.

Corporate treasury teams have dedicated compliance functions; they can absorb onboarding friction. Individual consumers cannot. The result is that stablecoin on-ramps remain operationally complex for retail users in most jurisdictions, and merchant acceptance gaps persist globally.

Every frictionless B2B payment that closes today is one more data point institutions use to justify further investment, while the consumer ecosystem waits for a regulated, UX-smooth on-ramp that hasn't yet materialized at scale.

4) The Closed-Loop Advantage

B2B stablecoin payments succeed precisely because they are closed-loop: enterprise sends to enterprise, both parties have wallets, both have compliance infrastructure, and neither needs a general-purpose merchant network.

Consumer payments face the classic chicken-and-egg problem: merchants will not invest in stablecoin acceptance infrastructure until consumers demand it, and consumers will not adopt wallets until they can spend them broadly.

The institutional world bypassed this problem entirely by operating in bilateral or consortium environments with no open merchant network required.

5) Institutional Incentives Run Upstream

Corporate treasurers holding stablecoins capture yield, reduce FX exposure, and improve liquidity management which are advantages that accrue internally and are difficult to share downstream without introducing complexity or competitive vulnerability.

Pushing stablecoin use to suppliers' suppliers, to employees, or to end consumers requires building a downstream network that benefits those parties, not necessarily the originating treasury team.

Without a clear ROI for extending the network outward, enterprises have rationally focused on consolidating gains internally.

Market Context

BVNK's own infrastructure data illustrates the B2B dominance from the operator side. The company processed $30 billion in annualized stablecoin payment volume in 2025, up 2.3× year-over-year, with one-third of that volume originating from the U.S. market alone.

Its customer roster (Worldpay, Deel, Flywire, Rapyd, Thunes) reads as a who's who of cross-border B2B and payroll infrastructure, not consumer apps.

As BVNK noted in its 2025 year-end review:

"The original assumption that remittances and consumer transfers would lead stablecoin growth has not played out as the primary driver. B2B has taken that role instead."

2026-2027:

When, or If, Retail Catches Up

The McKinsey/Artemis baseline makes the current state legible. What it cannot resolve is whether the institutional gap narrows, widens, or entrenches permanently.

Here are three plausible scenarios for the next 18 months:

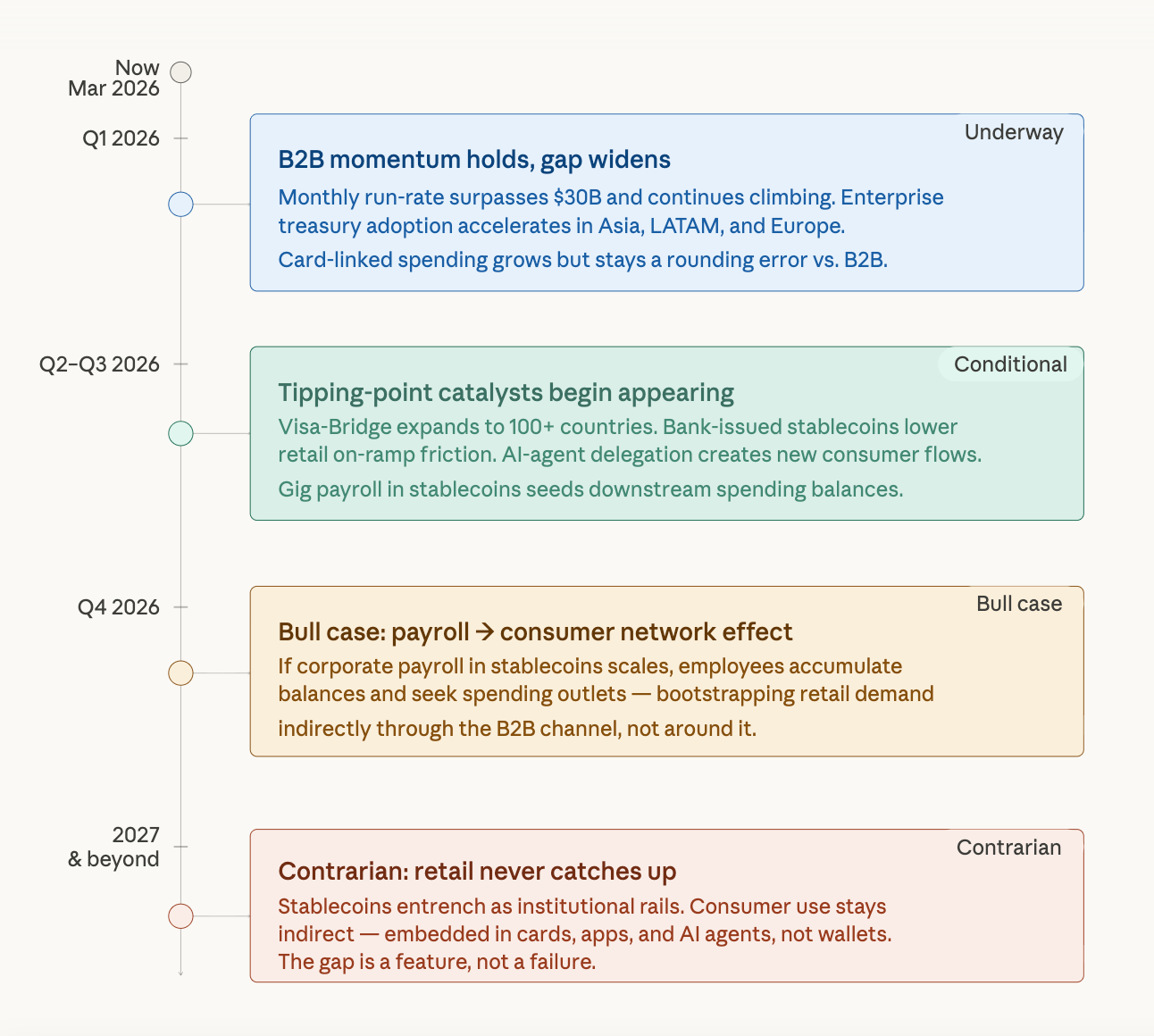

Near-Term 2026 - The Gap Widens Further

B2B momentum shows no signs of slowing. The monthly $30B+ run-rate continues its trajectory as more enterprises adopt stablecoin rails for cross-border payables and treasury operations. Consumer stablecoin card spending grows modestly but absolute volumes remain negligible against B2B. The gap widens in dollar terms even as retail adoption inches forward in percentage terms.

Medium-Term Late 2026–2027 - Tipping Points Begin to Appear

Several catalysts could begin bridging the gap: multi-currency bank-issued stablecoins lower retail on-ramp friction; programmable features extend into consumer apps via AI-agent payment delegation; gig-economy payroll in stablecoins creates downstream consumer balances that employees want to spend.

U.S. Treasury Secretary Scott Bessent has projected stablecoin supply could reach $3 trillion by 2030, a trajectory that implies eventual consumer network effects.

Contrarian View - Retail May Never "Catch Up" And That May Be the Point

The most intellectually honest reading of the McKinsey data is that stablecoins may be evolving into what the report subtly implies: the internet's programmable settlement layer for machines, treasuries, and institutions with consumer adoption as an indirect, embedded benefit rather than a primary use case.

If this framing is correct, the institutional gap is not a failure of adoption; it is a feature of the technology's natural architecture. Corporate payroll in stablecoins could eventually create downstream consumer spending, but the path from B2B infrastructure to retail wallet is long, indirect, and depends on UX breakthroughs that have not yet arrived at scale.

The Honest Baseline

and What Comes Next

The McKinsey/Artemis report does something more valuable than documenting stablecoin growth: it establishes an honest baseline that the industry has been conspicuously short on.

Stripping away trading noise, internal shuffles, and automated smart-contract cycles reveals a payments market that is genuinely growing, real payments doubling from 2024 to 2025, but that remains institutionally concentrated in ways that are structural, not accidental.

The 733% B2B surge is not a consumer story delayed. It is a treasury story maturing.

The enterprises building on stablecoin rails today are solving real operational problems such as cross-border friction, correspondent banking inefficiency, working capital delays that have nothing to do with whether consumers carry stablecoin wallets. They would be building regardless.

Related Reports

- Would Anyone Miss Banking Rails?: New Report from Finery Markets & Stablecoin Insider

- 2025 Stablecoin Year-End Report (Insights, Data, and Adoption Trends)

Partner/Advertise with Stablecoin Insider

Fill out this form to partner and advertise on the only publication, dedicated entirely to the Stablecoin ecosystem.

See you next week,

- The Stablecoin Insider team

{kind=link}