Table of Contents

The stablecoin industry has witnessed remarkable expansion, surpassing $218 billion in total circulation by the year 2025, and this surge has dramatically influenced the dynamics of digital payments throughout the international economic landscape. Unfortunately, this accelerated development has significantly outstripped the pace of regulatory evolution, resulting in notable deficiencies that jeopardize safeguards for consumers and the broader integrity of financial systems.

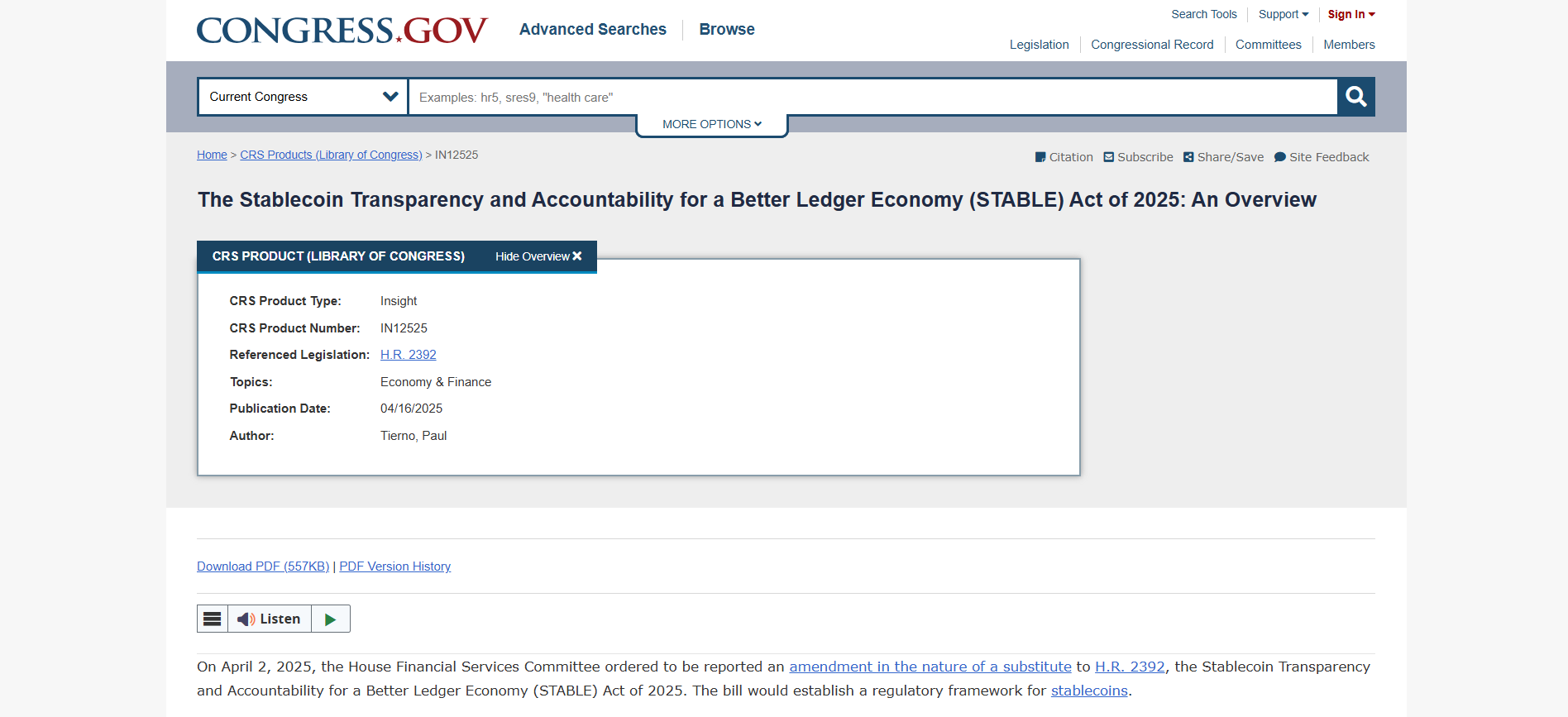

Presenting the Stablecoin Transparency and Accountability for a Better Ledger Economy (STABLE) Act of 2025, a meticulously crafted legislative blueprint intended to overhaul the regulatory paradigm for digital currencies in the United States.

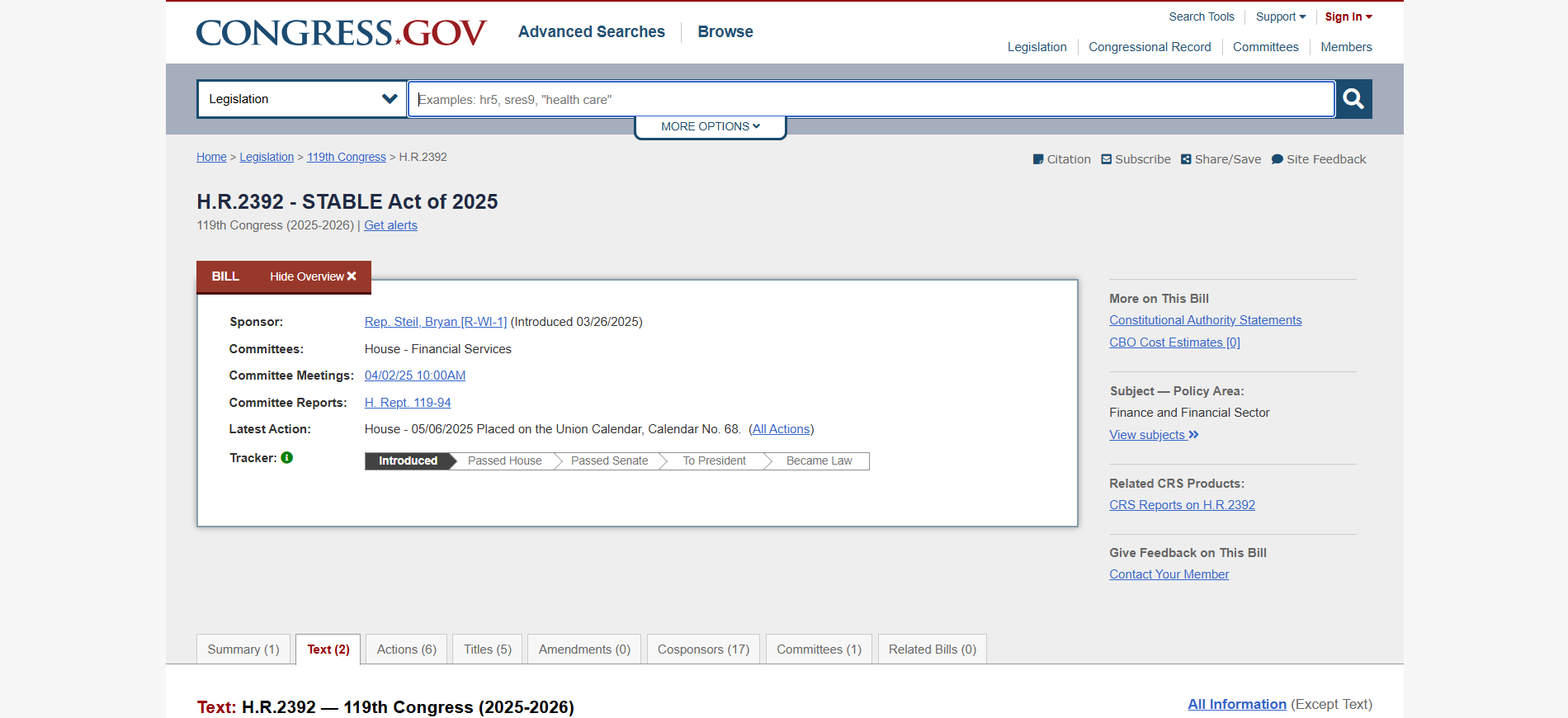

Formally introduced as H.R. 2392 by French Hill (R-Arkansas), who chairs the House Financial Services Committee, alongside Bryan Steil (R-Wisconsin), chair of the Digital Assets Subcommittee, the STABLE Act constitutes the most extensive federal endeavor to date aimed at governing stablecoins within U.S. jurisdiction. As bipartisan consensus continues to strengthen in Congress, coupled with the Trump administration's commitment to securing enactment before the August 2025 congressional break, the prospects for this bill becoming federal law appear increasingly promising.

The consequences of this potential legislation are immense and multifaceted. Given that stablecoins anchored to the U.S. dollar underpin diverse applications, including decentralized finance (DeFi) platforms and global money transfers, the overarching regulatory scheme will critically shape whether America sustains its financial hegemony in an era of digital transformation, or relinquishes influence to foreign territories characterized by more relaxed oversight mechanisms.

Key Takeaways

- Mandatory Federal Licensing: Exclusively, organizations sanctioned at the federal or state tiers as "permitted payment stablecoin issuers" hold the legal authority to distribute stablecoins across the United States.

- Full 1:1 Reserve Support: Entities issuing stablecoins must uphold exhaustive reserves comprising cash, Treasury instruments, or exceptionally liquid holdings, strictly forbidding any practices involving collateral reuse.

- Regular Audited Disclosures: The legislation enforces stringent openness protocols, necessitating monthly disclosures regarding reserve compositions, authenticated by the chief executive and financial officers.

- Federal Override: For those issuers granted federal endorsement, the STABLE Act nullifies corresponding state licensing stipulations, thereby streamlining and unifying supervisory functions under national governance.

- August 2025 Schedule: Under President Trump's directive, the goal is to finalize and enact stablecoin-related laws prior to the summer congressional hiatus, bolstered by escalating cross-party collaboration.

Understanding the Stablecoin Transparency and Accountability for a Better Ledger Economy Act

Official Definition and Scope

The STABLE Act inaugurates the inaugural holistic national oversight mechanism dedicated to payment stablecoins, these represent virtual tokens engineered to preserve consistent valuation against sovereign currencies, chiefly deployed in transactional or reconciliation contexts.

As delineated in the Act, a payment stablecoin qualifies as a digital instrument that sustains an unchanging monetary denomination or is advertised as preserving equilibrium relative to a designated benchmark asset.

This delineation purposefully sidesteps inherently fluctuating cryptocurrencies akin to Bitcoin or Ethereum, directing attention toward instruments optimized for exchange functionalities over investment speculation. Consequently, the Act concentrates on the burgeoning sector valued beyond $150 billion, overwhelmingly dominated by prominent stablecoins such as Tether's USDT and Circle's USDC, which together encompass upwards of 80% of the overall market capitalization.

Key Legislative Details

Designated as H.R. 2392, this bill emerges from prolonged cross-aisle deliberations, extending foundational concepts from antecedent proposals like the McHenry-Waters initiative in the preceding legislative term. Its contemporary configuration integrates perspectives from varied constituents, including commercial enterprises, supervisory bodies, and proponents of user rights, notwithstanding objections voiced by entities like the Conference of State Bank Supervisors (CSBS).

The bill's debut synchronizes with President Trump's directives advocating for cryptocurrency advancement and the designation of David Sacks as the presidential advisor overseeing AI and cryptocurrency matters, colloquially termed the "crypto czar."

Such executive endorsement infuses the initiative with robust political propulsion, as Treasury personnel affirm that stablecoin governance constitutes a paramount policy objective.

Timeline and Congressional Progress

Having overcome its preliminary substantial barrier, the STABLE Act garnered endorsement from the House Financial Services Committee via a 32-17 tally on April 2, 2025. Impressively, six Democratic lawmakers aligned with their Republican counterparts in favor, encompassing figures such as Josh Gottheimer (D-NJ), Sam Liccardo (D-CA), and Ritchie Torres (D-NY), thereby illustrating tangible interparty accord.

Presently, the measure anticipates deliberation on the full House floor, with Speaker Mike Johnson hinting at possible scheduling in July 2025.

Simultaneously, the Senate propels its analogous legislation, the GENIUS Act, forging concurrent avenues for stablecoin oversight that White House representatives aspire to synchronize ahead of the August intermission.

STABLE Act Requirements: What Stablecoin Issuers Must Know

Licensing Requirements for Stablecoin Issuers

The STABLE Act categorizes three permissible entity types eligible to disseminate payment stablecoins throughout the U.S.:

- Federally Authorized Nonbank Organizations: Such groups must petition the Office of the Comptroller of the Currency (OCC) for recognition as "federal qualified nonbank payment stablecoin issuers." This procedure parallels conventional banking licensure, demanding exhaustive fiscal documentation, strategic blueprints, and adherence architectures.

- Affiliates of Protected Depository Organizations: Conventional banks and credit unions may institute specialized subunits for stablecoin dissemination, harnessing their entrenched regulatory affiliations and foundational resources. This avenue proves enticing for entrenched players like JPMorgan Chase and Bank of America, already venturing into digital asset domains.

- State-Authorized Entities: Acknowledging state-level contributions, the Act permits regionally chartered bodies to circulate stablecoins contingent upon their domicile state's framework being validated by the Treasury Secretary as "substantially analogous" to national criteria. This flexibility bolsters progressive jurisdictions such as Wyoming and Texas, pioneers in bespoke digital asset governance models.

Reserve Backing and Asset Requirements

Central to the Act's stringent mandates are reserve obligations, compelling issuers to sustain a minimum 1:1 collateralization for every stablecoin outstanding.

Permissible collateral encompasses:

- Monetary deposits at safeguarded financial establishments

- U.S. Treasury obligations maturing within 60 days

- Holdings and accounts at central banking institutions

- Supplementary ultra-liquid assets sanctioned by overseers

Crucially, the legislation outlaws rehypothecation, leveraging reserve holdings as pledges for alternative financial engagements or borrowings. This edict squarely contests prevalent sector conventions, notably those associated with Tether, subjected to persistent critique over its collateral transparency and constitution.

Moreover, the Act imposes rigorous isolation directives, mandating that collateral remain distinctly partitioned from operational capital and impervious to creditor claims amid insolvency.

This protective encapsulation fortifies stablecoin possessors' interests, albeit potentially inflating issuers' expenditure profiles.

Reporting and Transparency Obligations

The STABLE Act's periodic disclosure imperatives substantially eclipse extant industry benchmarks. Emitters are duty-bound to disseminate elaborate accounts addressing:

- Collateral structure and prevailing valuations

- Aggregate stablecoin dissemination volumes

- Withdrawal transactions and fulfillment durations

- Hazard mitigation protocols and resilience assessment outcomes

- Conformity with stipulated governance norms

Subject to scrutiny by accredited accounting entities and endorsed personally by executive leadership, these submissions engender personal accountability for top-tier management. Paralleling Sarbanes-Oxley stipulations for exchange-listed corporations, this reflects the pivotal systemic stature ascribed to stablecoin operators by regulators.

Regulatory Oversight Structure

Crafting a bifurcated supervisory paradigm, the STABLE Act equilibrates national command with regional ingenuity. The OCC shoulders chief accountability for nationally accredited nonbank emitters, whereas banking authorities perpetuate vigilance over affiliated stablecoin branches of their wards.

Provincial overseers preserve jurisdiction over locally sanctioned emitters, provided their schemas align with federal thresholds and secure Treasury accreditation. This configuration endeavors to thwart regulatory circumvention whilst honoring federalist tenets, though skeptics posit it might engender disparities in competitive equity.

Punitive instruments incorporate monetary sanctions, permit annulments, and suspension directives. National overseers are vested with prerogatives mirroring those over legacy banks, inclusive of executive ousters and activity curbs for defiant entities.

Permitted Payment Stablecoin Issuers: Eligibility and Approval Process

Federally Licensed Nonbank Entities

Oriented toward fintech enterprises and analogous nonbank actors eyeing stablecoin entry, this licensure trajectory requires proof of:

- Sufficient capital reserves, with floors established by the OCC

- Seasoned executive cadre versed in fiscal operations

- Advanced hazard oversight apparatuses and safeguards

- Durable conformity mechanisms adept at perpetual regulatory fulfillment

- Thorough user safeguard guidelines and methodologies

The OCC pledges application adjudication within 120 days, a markedly swift interval relative to standard banking endorsements. This haste underscores the government's resolve to furnish regulatory predictability concurrent with vigilant scrutiny.

Enterprises like Paxos, functioning under New York's BitLicense, and Fireblocks, a digital infrastructure purveyor with vast institutional linkages, are aptly situated for pursuit.

Subsidiaries of Insured Depository Institutions

Legacy financial institutions confront diminished impediments to stablecoin deployment, capitalizing on preestablished oversight bonds and infrastructural assets.

This conduit appeals to entities pursuing:

- Income diversification via novel digital offerings

- Retention of depositors prone to reallocating to external stablecoin sources

- Augmentation of transactional faculties for enterprise clientele

- Involvement in nascent digital arenas whilst upholding conformity

Indications suggest Wells Fargo and Goldman Sachs are probing stablecoin ventures, perceiving them as organic augmentations to extant transactional and guardianship services. The affiliate paradigm permits risk compartmentalization whilst sustaining Federal Reserve transactional connectivity.

State-Chartered Institutions

The provincial pathway safeguards arenas for jurisdictional trailblazing in forging avant-garde digital asset schemas. Paradigms include Wyoming's Special Purpose Depository Institution (SPDI) accreditation and New York's Limited Purpose Trust Company endorsements, exemplifying regional stablecoin governance archetypes.

Nonetheless, regionally accredited emitters could encounter competitive handicaps, encompassing:

- Constricted national nullification shields

- Ambiguity in trans-state commercial jurisdiction

- Prospective frictions with national scrutiny

- Market entry impediments in non-mutual territories

The Treasury's equivalence appraisal methodology lingers nebulous, instilling hesitancy among provincial overseers honing their structures. Such opacity may propel coalescence toward national accreditation as the prudent alternative.

STABLE Act vs. GENIUS Act: Comparing Congressional Stablecoin Bills

Regulatory Framework Differences

Whilst both enactments propose national accreditation regimes for stablecoin emitters, they bifurcate profoundly in federalism handling. The STABLE Act champions centralization with expansive national nullification, contrasting the GENIUS Act's emphasis on amplified provincial autonomy.

The GENIUS Act incorporates a $10 billion benchmark, mandating transition to national vigilance for surpassing provincial emitters, instituting a stratified arrangement omitted from the STABLE Act, which enforces homogeneous national norms irrespective of emitter magnitude.

State Authority and Preemption

The STABLE Act's nullification clauses emerge as its most polarizing facet, supplanting provincial accreditation mandates for nationally sanctioned emitters. Adversaries contend this aggregates undue authority in the OCC, eroding provincial digital asset governance advancements.

The CSBS has ardently contested these elements, deeming them "an unparalleled federal authority augmentation" potentially quelling supervisory creativity. Conversely, the CSBS endorses the GENIUS Act's equilibrated tactic, safeguarding provincial jurisdiction alongside national criteria.

Algorithmic Stablecoin Provisions

The STABLE Act decrees a biennial suspension on novel "endogenously secured stablecoins", algorithmic variants sustaining parity via mechanized market dynamics over conventional collateral.

This targets debacles akin to Terra's 2022 UST implosion.

The GENIUS Act diverges, commissioning Treasury scrutiny of algorithmic stablecoins sans outright prohibition. This variance encapsulates persistent dialogues on algorithmic paradigms' capacity to fulfill stability and user safeguard imperatives in stablecoin governance.

Federal vs. Tiered Approach

The STABLE Act's monolithic national strategy starkly opposes the GENIUS Act's graduated model. Uniformity advocates assert it averts governance evasion and assures equitable user shields. Detractors favor graduation for nurturing creativity whilst tailoring vigilance to critical emitters.

Harmonizing these contrasts is imperative for legislative culmination, with sector pundits foreseeing negotiated verbiage upholding provincial jurisdiction whilst delineating unequivocal national benchmarks. The resolution will profoundly mold competitive terrains and governance outlays for stablecoin operators.

How the STABLE Act Affects Circle, Tether, and Other Stablecoin Companies

Winners: Circle (USDC) and Compliant Issuers

Circle, originator of USD Coin (USDC), stands optimally aligned to capitalize on the STABLE Act's deployment.

The enterprise already maintains:

- Integral reserve collateralization with periodic verifications by Grant Thornton

- Adherence to diverse provincial accreditation schemas

- Formidable alliances with orthodox fiscal service providers

- Disclosure practices transcending sector averages

Circle's leader, Jeremy Allaire, has vociferously championed stablecoin governance, positing that lucid directives will expedite organizational integration and entrench the dollar's digital finance primacy. This adherence-centric ethos equips Circle to appropriate market portions from less regimented adversaries.

Analogously, PayPal's PYUSD, facilitated by Paxos, anticipates gains. Paxos' BitLicense operation evinces requisite governance scaffolding, with institutional affiliations expediting national accreditation.

Challenges for Tether (USDT)

Commanding over $100 billion in dissemination as the premier stablecoin emitter, Tether confronts formidable barriers under the STABLE Act. Its extraterritorial architecture and erstwhile opaque collateral methodologies conflict with exigencies for:

- U.S. governance scrutiny and audit prerogatives

- Exhaustive periodic disclosures with autonomous validations

- Partitioned collateral in endorsed classifications

- Executive authentications imposing individual accountability

Tether's recent transparency augmentations, via BDO quarterly assessments, may inadequately satisfy the Act's rigorous benchmarks. Its British Virgin Islands domicile exacerbates U.S. compliance complexities.

Industry prognosticators anticipate Tether establishing a conforming U.S. branch or incurring substantial market erosion to regulated peers. Its global hegemony affords partial insulation, yet U.S. engagements would endure severe curtailments.

PayPal's PYUSD and Other Players

PayPal's stablecoin incursion with PYUSD underscores conventional payment titans' digital asset intrigue. Leveraging entrenched governance ties and conformity apparatuses yields STABLE Act advantages, though Paxos dependency introduces partnership perils.

Diminutive emitters like Gemini's GUSD and TrustToken's TUSD may succumb to amalgamation pressures from national accreditation's lofty conformity expenditures.

Such firms could solicit acquisitions by behemoths or forge coalitions with orthodox fiscal entities for governance attainment.

Market Consolidation Predictions

The Act's elevated governance threshold is forecasted to precipitate profound sector amalgamation, encompassing:

- Diminution in stablecoin diversity as minor operators retreat

- Amplified institutional ingress from banking and payment sectors

- Operational focalization in governance-favorable locales

- Heightened functional expenditures manifesting in emitter tariffs

Whilst amalgamation may elevate user steadiness and shields, it risks attenuating creativity and rivalry. Enduring market architecture hinges on overseers' equilibrium of security with ingenuity in Act execution.

Foreign Stablecoins Under the STABLE Act: Reciprocity and Compliance

Comparable Regulatory Regime Requirements

The STABLE Act's foreign stablecoin disposition recognizes digital assets' transboundary essence whilst affirming U.S. governance independence. Overseas emitters access U.S. markets solely upon dual fulfillment:

- Primarily, subjection to foreign oversight schemas Treasury-deemed equivalent to U.S. norms, guaranteeing parallel user shields and systemic safeguards.

- Secondarily, acquiescence to U.S. disclosure and scrutiny mandates, subjecting American activities to domestic vigilance. This extraterritoriality accentuates the dollar's worldwide eminence and U.S. resolve in dollar-linked asset dominion.

Treasury Secretary Determination Process

The equivalence adjudication process remains broadly unspecified, fostering uncertainty for international emitters and overseers. Absent explicit metrics or chronologies, Treasury wields extensive discretion.

Prospective appraisal elements include collateral mandates and quality, disclosure and audit criteria, supervisory and punitive apparatuses, user shields and liquidation protocols, plus anti-laundering and penalty conformity.

The EU's MiCA, instituting exhaustive stablecoin directives, could benchmark Treasury evaluations. Comparably, UK's prospective schema and Singapore's Payment Services Act might attain equivalence.

Oversight and Reporting Obligations

Equivalence-attaining emitters nonetheless submit to U.S. scrutiny, entailing routine American operational disclosures, agency audit rights, domestic user shield conformity monitoring, and enforcement synergy.

Such imperatives may incite foreign overseer clashes and deter global emitters, especially resource-constrained minors, from U.S. pursuit.

The Act's 18-month leniency for incumbent foreign stablecoins facilitates Treasury appraisals and adjustments, though potentially insufficient for elaborate transnational harmonization.

STABLE Act Custody Requirements: Protecting Consumer Assets

Asset Segregation Requirements

Tackling paramount user shield concerns in stablecoin realms, the Act's guardianship clauses obligate intermediaries to delineate client holdings from proprietary assets, securing user funds amid custodian fiscal woes.

This extends to all guardianship providers for payment stablecoins, spanning exchanges like Coinbase and Kraken, managed wallet furnishers, institutional platforms, and stablecoin transaction processors.

Isolation necessitates functional demarcation, with segregated ledgers and controls precluding asset intermingling. Echoing traditional finance norms, this mandates operational overhauls for numerous crypto entities.

Commingling Prohibitions

Prohibiting client-custodian asset fusion, the Act sanctions omnibus repositories pooling multiple client holdings at safeguarded institutions or trusts. This accommodates digital guardianship pragmatics whilst sustaining core shields.

Omnibus facilitates cost mitigation via unified banking, liquidity optimization for redemptions, corporate asset separation, and ownership preservation through granular records.

Nevertheless, omnibus complicates insolvency differentiations. The Act counters via mandatory meticulous documentation and guardianship oversight.

Regulatory Supervision Standards

Guardianship confines to federally or provincially bank-supervised entities, barring unregulated operators. This ensures hazard management and user shield adherence.

Eligible encompass national/provincial banks, federal/provincial credit unions, overseen trusts, select licensed transmitters, and custody-authorized investment consultants.

This constriction likely spurs guardianship amalgamation, compelling unlicensed to accredit or ally, disproportionately impacting resource-scarce minors.

STABLE Act Criticism: State Regulators and Industry Pushback

Conference of State Bank Supervisors Opposition

Emerging as the Act's staunchest detractor, the CSBS argues nullification erodes provincial creativity and unduly centralizes authority federally. In an April 2025 committee missive, President Brandon Milhorn enumerated core grievances.

CSBS contends provinces led digital asset governance whilst federal inertia prevailed, citing Wyoming, New York, Texas innovations as provincial efficacy proofs in innovation-user balance.

Particular rebukes include overbroad nullification supplanting provincial user laws, OCC power concentration sans restraints, federal emitter arbitrage edges, and creativity suppression via uniformity. CSBS proposes revisions reinstating draft-limited nullification, retaining amplified provincial interstate sway.

Federal Preemption Concerns

Extending past banking conventions, the Act's nullification might void non-conflicting provincial user mandates, alarming advocates and officials over safeguard erosion.

House Democrats echo qualms, with Maxine Waters (D-CA) lambasting "insufficient user shields." Democratic emendations seek FDIC stablecoin coverage, failed redemption refunds, hazard/fee revelations, and Trump official stablecoin bans.

These mirror Democratic anxieties over administration-crypto nexuses and decisional interest conflicts.

Market Consolidation Risks

Sector detractors caution the Act's barriers foster excessive amalgamation, yielding oligopolies detrimental to users and creativity. Intricate conformity favors resourced majors, barricading minors.

Amalgamation ramifications include rivalry diminution, fee escalations from power concentration, creativity curbs from conformity primacy, and locational clustering.

Advocacy cohorts fret reduced choices amplify systemic perils via emitter centralization, paralleling traditional finance concentration debates.

STABLE Act Timeline: When Will Stablecoin Regulation Take Effect?

Congressional Approval Process

Enactment hinges on milestones affording emendation/delays.

Post-committee, hurdles include:

- House plenary vote, potentially July 2025 per Johnson, agenda-dependent; bipartisan backing augurs passage, emendations viable.

- Senate GENIUS scrutiny, challenging amid slim majority and Democratic preemption reservations.

- Divergent versions necessitate conference reconciliation on preemption, provincial roles.

House vs. Senate Reconciliation

Key reconciliation issues include:

- Federal preemption scope and state regulatory authority

- Threshold requirements for mandatory federal oversight

- Algorithmic stablecoin treatment and study requirements

- Enforcement mechanisms and regulatory coordination

Implementation Deadlines

- Immediate Implementation: The prohibition on unlicensed stablecoin issuance would take effect immediately, though existing issuers would receive transition periods.

- Six-Month Deadline: Federal regulators must establish detailed application procedures and approval criteria within six months of enactment.

- Two-Year Transition: Existing stablecoin issuers have two years to obtain appropriate licenses or cease U.S. operations. This transition period aims to prevent market disruption while ensuring compliance.

- Three-Year Compliance: Digital asset service providers must verify that all stablecoins they offer are issued by licensed entities within three years of enactment.

The Future of Stablecoin Regulation in America

The STABLE Act heralds a seminal juncture in U.S. fiscal governance, erecting the premier exhaustive national schema for monetary-functioning digital assets. Passage would reconstitute the stablecoin arena, transiting from governance voids to defined regimens.

Transcending crypto, impacts mold U.S. digital economy monetary independence preservation. Stringent dollar-stablecoin norms aim to perpetuate reserve currency supremacy whilst propelling payment innovations.

Efficacy relies on execution nuance and OCC adaptability in innovation-protection equilibrium.

Industry imperative: unregulated phase termination. Conformity-intensive futures demand, where costs/complexities redefine rivalry; adapters dominate, laggards risk U.S. exclusion.

Read Next:

- mUSD Stablecoin: Complete Breakdown of the MetaMask's New Dollar Token

- Hong Kong Stablecoin Regulation 2025: What You Should Know

- How to Earn High Yield with USDC: Top 3 Platforms in 2025

FAQs:

1. What is the STABLE Act of 2025?

The STABLE Act establishes U.S. stablecoin issuer mandates, including accreditation, integral reserve backing, periodic audited revelations, and national vigilance for payment stablecoins.

2. When will the STABLE Act become law?

Committee-cleared, awaits July 2025 House vote potentially. Trump backs pre-August recess signing, GENIUS reconciliation possible.

3. How will the STABLE Act affect existing stablecoins like USDT and USDC?

USDC advantages from conformity/reserve clarity; USDT challenges from offshore/reserve issues. Biennial licensing or U.S. exit transition.

4. Can foreign stablecoin companies operate in the US under the STABLE Act?

Affirmative, via Treasury-equivalent regime and U.S. mandate consent. 18-month incumbent leniency.

5. What are the main differences between the STABLE Act and GENIUS Act?

STABLE centralizes with broad nullification; GENIUS provincial with $10B tier. STABLE algorithmic suspension; GENIUS Treasury examination.

{kind=link}