Table of Contents

Over the last two years, a new breed of stablecoin has gone from niche experiment to system-level player: Yield-bearing, leveraged “super-stablecoins.”

Ethena’s USDe and TRON’s USDD sit at the centre of this shift, advertising double-digit yields on assets that are supposed to behave like digital dollars.

At the same time, the global stablecoin market has crossed roughly $300 billion dollars in circulating supply, with USDe already among the largest USD stablecoins by market cap, behind USDT and USDC.

We have been here before: TerraUSD (UST) and Anchor’s roughly 20% APY “savings rate” drew in most of UST’s supply before collapsing in 2022 and wiping out tens of billions of dollars.

Key Takeaways

- Super-stablecoins like USDe and USDD bundle a 1 dollar peg with double-digit yields, using derivatives, staking, and subsidies.

- USDe relies on delta-neutral futures hedging plus ETH staking to generate yield for sUSDe holders, tying stability to derivatives markets.

- USDD combines over-collateralized reserves with subsidized 20–30% APYs, making adoption dependent on ongoing incentives.

- The Terra and Anchor collapse proved that 20% “stable” yields can concentrate risk and trigger multi-billion-dollar failures when assumptions break.

- Every new super-stablecoin should be analyzed like a structured product, not a simple digital dollar: backing, yield source, leverage, liquidity, and regulation all matter.

What Are “Super-Stablecoins”?

In this context, “super-stablecoins” are USD-pegged assets that build yield into the core product, not as an external farm or side pool.

Common traits:

- They target a 1 dollar peg while promising elevated yields relative to bank deposits or traditional stablecoin lending.

- Yield comes from derivatives, leverage, and complex strategies, not just T-bills or short-term debt.

- The protocol is often marketed as a “crypto native savings account” or “dollar with yield baked in.”

USDe and USDD fit this pattern:

- USDe (Ethena): A synthetic dollar backed by crypto collateral and delta-neutral futures hedging, with yield passed to stakers via sUSDe.

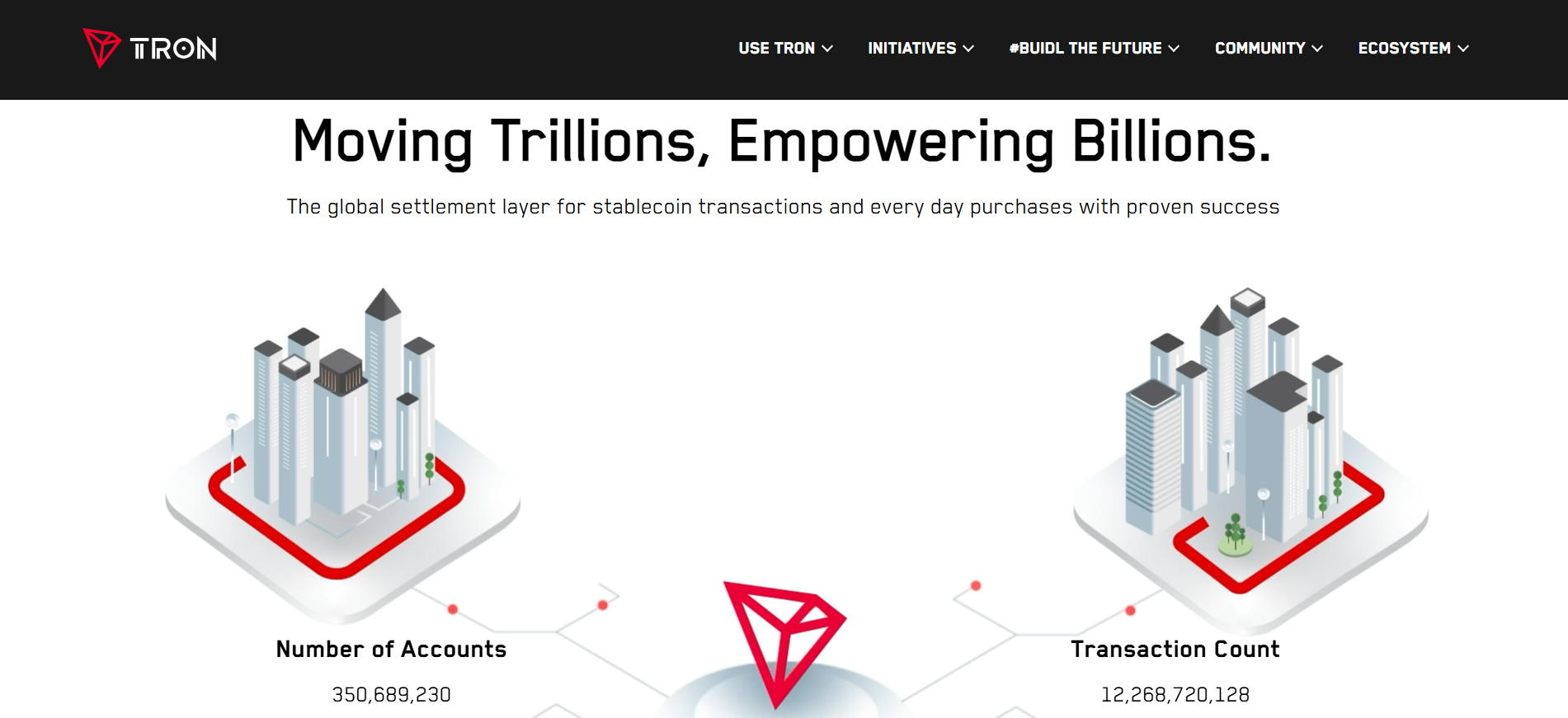

- USDD (TRON): An over-collateralized stablecoin governed by TRON DAO Reserve, backed by a basket including BTC, TRX, USDT, and other assets, with historically subsidized yields up to 30% APY across TRON DeFi platforms.

The key is perception:

For many users, they look like “better dollars”, same peg, much higher yield.

The Core Promise: Stable Principal, High Yield

The marketing pitch is simple:

Deposit a dollar-pegged token, earn double-digit APY, keep dollar exposure.

Compared to:

- Bank savings, which have been near low single-digit yields in many economies.

- Traditional stablecoins (USDT/USDC/DAI), which typically earn a few percent when lent into money markets or used in conservative DeFi strategies.

For USDe and USDD specifically:

- sUSDe staking yields have typically ranged from around 4–10% APY on mainstream DeFi dashboards, with some periods and platforms quoting roughly 20–30% APY based on market conditions and promotional campaigns.

- USDD has been advertised with benchmark rates around 20–30% APY on exchanges and lending protocols (JustLend, Poloniex, Bitrue, Bybit, USDD’s own campaigns), explicitly subsidized by the TRON DAO Reserve to drive adoption.

The pitch is that you get “stablecoin safety” plus “DeFi yields” in one asset, without needing to manage complex positions yourself.

How USDe and USDD Actually Work

1. USDe: Synthetic Dollar With Delta-Neutral Hedging

Ethena’s USDe is not backed by bank deposits or T-bills. Instead, it is a synthetic dollar created by:

1. Taking crypto collateral

2. Opening offsetting short futures positions

- The protocol delta-hedges the collateral on derivatives venues (perpetual or deliverable futures).

- If ETH or BTC goes up, the futures short loses but the spot collateral gains; if they go down, the short gains and the collateral loses. In ideal conditions, the net USD value stays roughly unchanged.

3. Passing yield to stakers via sUSDe

- Users stake USDe and receive sUSDe.

- sUSDe accrues protocol revenue from:

- Perpetual funding rates and basis trades

- ETH staking rewards

- Yield on any liquid stablecoin reserves

- Yield is reflected as an increasing sUSDe price relative to USDe, rather than an increasing token count.

This structure lets Ethena offer a yield-bearing “dollar” without holding traditional fixed-income assets, but it ties stability and yield to derivative markets and funding dynamics.

2. USDD: TRON’s Over-Collateralized High-Yield Stablecoin

USDD is issued by TRON and aims to maintain a 1:1 dollar peg with crypto collateralization:

- Collateral includes BTC, TRX, USDT, USDC and other assets, with published materials often citing collateralization levels above 120–200%, and some TRON-aligned sources presenting figures above 300%.

On the yield side:

- Early in its lifecycle, USDD launched with a “benchmark interest rate” around 30% APY, explicitly subsidized by TRON DAO to attract users.

- DeFi platforms on TRON (JustLend, SUN.io) and centralized exchanges have run campaigns with 20–30% APY for USDD staking, lending, or liquidity provision.

USDD’s peg is supported through open-market operations: TRON DAO Reserve buys or sells USDD and reserve assets on exchanges to counter deviations, similar in concept to central bank interventions.

Today, USDD’s market cap sits in the hundreds of millions of dollars, placing it within the top-10 stablecoins but far behind USDT, USDC, and USDe by scale.

Where the Extra Yield Actually Comes From

The key question for any super-stablecoin is: who is paying for the yield?

For USDe and sUSDe, revenue (and therefore yield) is driven by:

- Perpetual futures funding:

When perpetual futures trade at a premium to spot (common in bull or carry-trading markets), shorts receive funding payments from longs. Ethena captures these payments on its hedged short positions. - ETH staking rewards:

Part of the collateral is in staked ETH (stETH and similar), which earns staking yield before fees and protocol allocations. - Stablecoin and tokenized fixed-income yield:

Holdings of USDT, USDC and tokenized T-bill exposure can generate additional revenue, some of which may eventually flow to sUSDe.

For USDD, yields have historically depended on:

- Protocol subsidies by TRON DAO Reserve:

For long stretches, advertised 20–30% APYs were not pure organic yield but incentives paid out of the reserve’s budget, to bootstrap adoption. - Lending spreads and liquidity incentives:

Lending USDD on JustLend or pairing it in liquidity pools on SUN.io and other TRON DeFi platforms adds additional reward layers: interest from borrowers, governance tokens, promotional campaigns.

In both designs, high yield is either market-condition-dependent (funding, staking) or subsidy-driven. Neither model gives you something similar to a risk-free bank deposit.

The Terra / Anchor Precedent: When 20% APY Broke DeFi

The phrase “20%+ yield that broke DeFi” is rooted in a very specific case: TerraUSD (UST) and the Anchor Protocol.

- Terra’s Anchor Protocol paid roughly 19.5–20% APY on UST deposits, marketed as a “savings account.”

- Academic and policy research shows that around three quarters of UST’s circulating supply ended up deposited in Anchor to capture this rate.

- When UST lost its peg in May 2022, Terra’s ecosystem and LUNA collapsed, erasing on the order of 40–45 billion dollars in market value and contributing to a broader crypto drawdown of hundreds of billions of dollars.

Anchor’s 20% rate was heavily subsidized by a “yield reserve” and did not match the protocol’s underlying revenue, a design now widely described as unsustainable in policy papers and post-mortems.

USDe and USDD are architecturally different from UST, but the economic pattern is similar:

- A dollar-pegged asset becomes the centre of a “too good to ignore” yield opportunity.

- Liquidity concentrates around that asset, increasing its systemic importance.

- If yields compress or a stress event hits, the unwind can propagate through lending markets, perpetual futures venues, and collateral chains.

The Terra saga is no longer theory; it is a historical dataset of what happens when a super-stablecoin design fails at scale.

Stress Scenarios for Super-Stablecoins

From a risk-analysis perspective, USDe and USDD face different but related stress scenarios.

Funding Rate Collapse (USDe)

If perpetual futures markets flip into a regime of persistently low or negative funding:

- USDe’s yield engine weakens, and sUSDe returns fall towards low single digits or even turn negative after fees and reserves.

- Investors who bought the story of “high, stable yield” may react poorly to shrinking payouts.

- If Ethena tries to preserve yields by increasing leverage, tail risk grows.

Derivatives funding is extremely cyclical, and documentation explicitly acknowledges that yield depends on market conditions.

Exchange and Liquidity Shock (USDe)

On 10–11 October 2025, USDe traded as low as about 0.65 dollars on Binance during a violent market move, while remaining close to 1 dollar on core DeFi venues like Curve.

Post-mortems attribute this to:

- Venue-specific oracle and infrastructure issues

- Lack of direct mint and redeem on Binance

- Forced liquidations and auto-deleverage mechanisms

From a user’s perspective, the event highlighted venue risk: even if the protocol remains hedged, you can still face severe price swings where you trade or where your collateral is held.

Collateral Drawdown and Liquidity Crunch (USDe and USDD)

Both protocols rely heavily on crypto collateral:

- A steep drop in BTC, ETH or TRX prices can stress collateral ratios.

- In extreme volatility, there may not be enough liquid two-sided markets to unwind positions without heavy slippage.

- Users rushing to redeem or exit can exacerbate price moves, especially if total value locked is concentrated on a few platforms.

Stablecoin crash studies after the Terra event show that collateral drawdowns and liquidity spirals are common failure channels for designs that lean on volatile backing.

Subsidy Fatigue (USDD)

For USDD, a different question dominates:

- How long can a system maintain 20–30% APY rates that are partly or largely subsidized?

- If subsidies are reduced and APY falls closer to single digits, as some current TRON DeFi yields already suggest, capital may rotate out, weakening liquidity and potentially the peg if confidence slips.

Super-Stablecoins vs Traditional Stablecoins

A simple comparison helps frame the trade-off.

| Feature | USDe / USDD (“Super-Stablecoins”) | USDT / USDC / DAI (Traditional) |

|---|---|---|

| Target peg | 1 USD | 1 USD |

| Headline yield | Often double-digit APY, sometimes 20–30% in campaigns | Typically low single-digit when deployed conservatively |

| Backing model | Crypto collateral plus derivatives (USDe), crypto collateral reserves (USDD) | Treasuries, cash, repo (USDT/USDC); mixed on-chain collateral (DAI) |

| Main yield source | Perpetual funding, staking rewards, protocol subsidies | Interest on reserves, fees, conservative lending |

| Complexity (under the hood) | High: multi-venue hedging, margining, open-market operations | Moderate: reserve management, some on-chain lending |

| Tail-risk profile | Elevated: dependent on market structure, leverage, and venue stability | Lower (but not zero): dependent on reserve integrity and banking risk |

The trade-off is clear:

Higher advertised yield in exchange for more complex, path-dependent risk.

How to Analyze Any Future “Super-Stablecoin”

Whether it is USDe, USDD, or the next synthetic dollar, you can apply the same checklist:

1. What exactly backs it?

- On-chain collateral, off-chain assets, or nothing?

- Is there a clear, verifiable reserve breakdown?

2. Where does the yield come from?

- Funding rates, staking, lending spreads, protocol subsidies?

- Do those flows historically cover the promised APY, or is there a gap?

3. How much leverage is in the system?

- Perpetual futures positions, rehypothecated collateral, multiple stacked protocols.

- What happens when volatility spikes and collateral correlations go to 1?

4. How deep and diversified is liquidity?

- Are there multiple venues with deep USDe or USDD pairs?

- How much capital could exit in a day without pushing the price far from 1 dollar?

5. How do redemptions work in practice?

- Can you reliably redeem one token for roughly one dollar of value, or are you relying on secondary market liquidity only?

6. What is the regulatory and counterparty footprint?

- Heavy use of centralized exchanges, unregulated venues, or thinly-capitalized entities adds another layer of risk.

You can treat every new super-stablecoin as a structured product: a bundle of exposures wrapped in a simple UX and a 1 dollar label.

What the 20%+ Yield Era Means for DeFi’s Future

Three big themes emerge from the rise of USDe, USDD, and their predecessors:

- There is no free yield:

The Terra collapse demonstrated that subsidized or reflexive yields can attract enormous capital and then fail catastrophically. UST’s 20% APY pulled in most of its supply and amplified the eventual crash. - Yield-bearing stablecoins are now systemically relevant:

With USDe already accounting for a meaningful share of global stablecoin supply and a market cap in the low-double-digit billions, any serious stress event will ripple across perpetual futures markets, collateral chains, and DeFi liquidity. - Regulation is pivoting from “if” to “how”:

Major regulators now explicitly call out stablecoin risks and are building frameworks in multiple jurisdictions. Designs that combine high yield with systemic scale are likely to sit at the centre of that conversation.

For builders and users alike, the lesson is simple:

Double-digit “risk-free” yields on dollars are a warning sign, not a feature.

Conclusion

USDe and USDD show how far DeFi will go to attach equity-like returns to dollar-pegged assets. They are technically sophisticated, deeply integrated into derivatives and lending markets, and at current sizes, significant pieces of the stablecoin landscape.

But the last cycle already provided a case study: Terra’s 20% savings rate pulled an entire ecosystem off a cliff.

When you see a “stable” asset advertising 20–30% APY, the right instinct is not fear of missing out; it is to ask:

- Who is really paying for this yield?

- What happens if that source disappears?

- How much of DeFi depends on this staying upright?

If you cannot answer those questions clearly, the yield is probably pricing in more risk than you realize.

Read Next:

FAQs:

1. What makes USDe and USDD different from normal stablecoins like USDT or USDC?

USDe and USDD are designed not just to hold a 1 dollar peg but also to deliver elevated yields through derivatives, staking, and incentives, while USDT and USDC mainly hold cash and Treasuries and only generate yield when you deploy them into separate DeFi or CeFi products.

2. Are the 20–30% yields on USDe and USDD sustainable long-term?

They are highly path-dependent: USDe’s yield depends on futures funding and staking conditions, while USDD’s highest rates have been explicitly subsidized by the TRON DAO Reserve. Both can persist for periods but are unlikely to be stable, low-risk rates over many years.

3. Did USDe already experience a de-peg event?

Yes. In October 2025, USDe traded down to roughly 0.65 dollars on Binance during a sharp market move, while staying close to 1 dollar on major DeFi venues. Analyses attribute this to venue-specific oracle and liquidity issues, but it highlighted how exchange infrastructure can affect user outcomes even if the protocol remains hedged.

4. How did Terra’s 20% yield on UST “break DeFi”?

Terra’s Anchor Protocol offered about 20% APY on UST deposits, attracting a very large share of UST’s circulating supply and making the system dependent on that single use case. When confidence cracked and the peg failed in May 2022, the collapse erased tens of billions of dollars and triggered a broad crypto sell-off, becoming a core event in the 2022 crypto winter.

5. What should I check before using any super-stablecoin as a savings vehicle?

At minimum, review what backs it, how redemptions work, which markets provide liquidity, how yields are generated, and what happens in stress scenarios like funding-rate crashes or collateral drawdowns. If you cannot trace those mechanics in clear, independent documentation, you should assume the headline APY carries hidden tail risks.

{kind=link}