Table of Contents

Neobanks like Revolut and N26 were once the poster children of “modern banking”: slick apps, instant cards, and cheap FX that made legacy banks look prehistoric.

Today, a new layer is competing for the same users: USD stablecoins held and spent through platforms like Crypto.com, Coinbase, and other crypto apps.

This isn’t just a crypto niche anymore. By the end of 2024, global crypto ownership was estimated at hundreds of millions of people, with double-digit percentage growth year over year.

At the same time, the market cap of reserve-backed stablecoins surged from just a few billion dollars in 2020 to well over a couple hundred billion by 2025, with the majority in USDT and a large share in USDC.

Crypto.com alone now reports a user base in the tens of millions globally.

Meanwhile, Revolut has grown to tens of millions of customers and processes close to a trillion dollars in annual transaction volume, while N26 serves several million active customers with tens of billions of euros in yearly transactions.

Neobanks are big, but stablecoins are now a serious alternative for global, mobile, and crypto-native users.

Key Takeaways

- Stablecoins give 24/7, global USD access, while neobanks still depend on regional banking rails.

- Apps like Crypto.com turn USD stablecoins into spendable balances with cards, yields, and on-chain transfers.

- Revolut and N26 are strong for local bills, direct debits, and insured deposits, but weaker for on-chain activity.

- Cross-border contractors and remote workers often prefer USDT/USDC over neobank FX and weekend markups.

- The most resilient setup is usually hybrid: a neobank for regulated banking + stablecoins for global liquidity.

What Stablecoins Are and Why USD-Pegged Tokens Matter

Stablecoins are crypto tokens designed to track the value of a fiat currency, most commonly the U.S. dollar. The leading reserve-backed coins are backed primarily by cash and short-term U.S. Treasuries held by regulated custodians.

The total stablecoin market has grown from low single-digit billions to hundreds of billions of dollars in just a few years, dominated by USDT and USDC.

On-chain, stablecoins have become the default unit of account. A large share of trading volume on crypto exchanges is now denominated in stablecoins rather than fiat currency pairs.

Beyond trading, stablecoins are increasingly used for payments and settlement. Daily on-chain settlement volumes regularly reach tens of billions of dollars across major networks, covering remittances, merchant payments and inter-exchange transfers. This is still small compared to the global remittance and payments market, but the growth curve is steep.

What users feel in practice:

- 24/7 settlements: transfers clear in minutes, any day, with no bank cut-off times.

- Global access: anyone with a phone and internet can receive USDT/USDC, even without a local bank.

- Programmability: funds can interact with DeFi, lending markets and other on-chain protocols.

Platforms like Crypto.com abstract a lot of blockchain complexity. Users see a familiar app, KYC onboarding, fiat on-ramps, and a Visa/Mastercard-linked card, while their balances under the hood are often held in USD stablecoins or easily swapped into them.

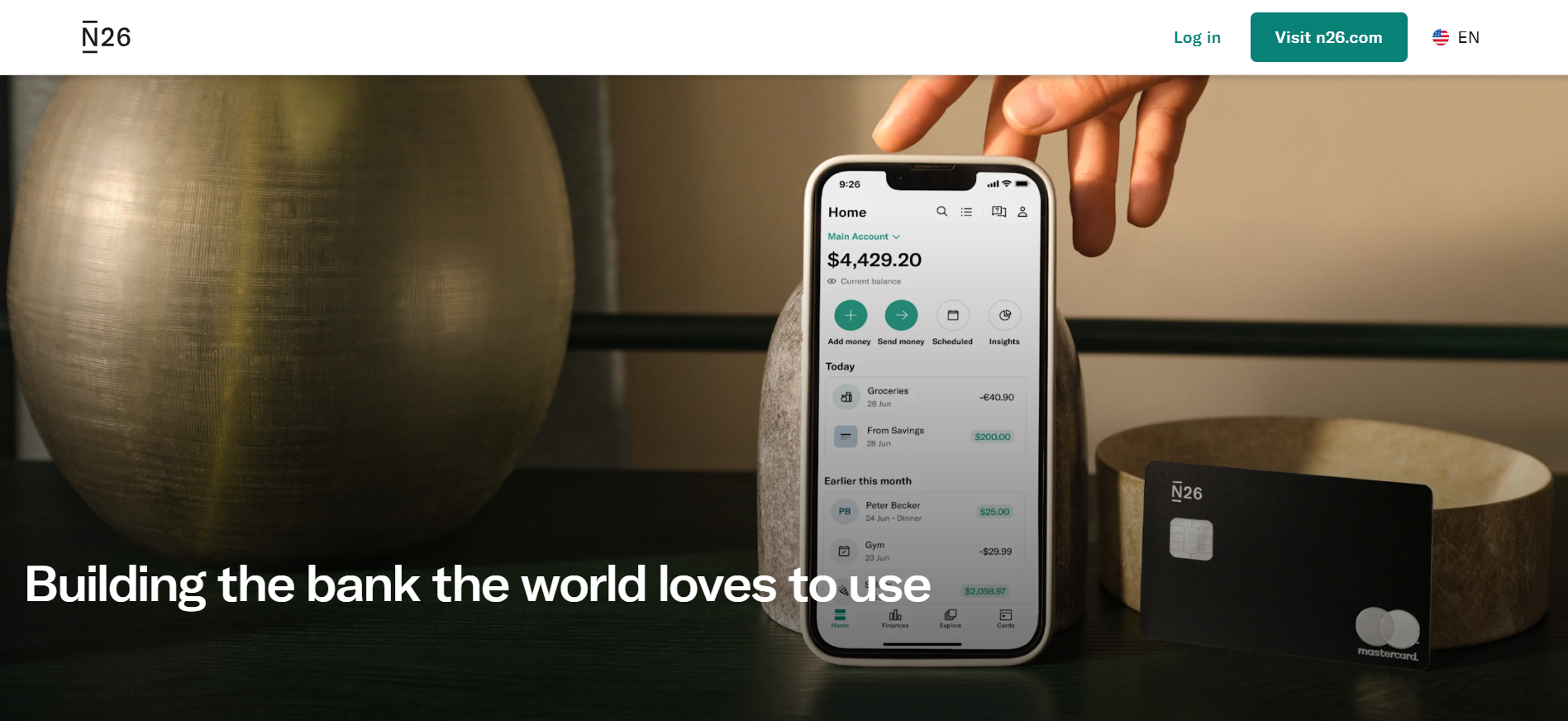

Neobanks 101: Revolut, N26 and the First Wave of “Modern Banking”

Neobanks are fully digital banks or e-money institutions built mobile-first. They helped millions escape clunky web banking, especially in Europe and the UK.

What Neobanks Brought to the Table

Neobanks like Revolut and N26 built their success on:

- Multi-currency accounts with cheaper FX than traditional banks.

- Instant card provisioning and controls (freeze, virtual cards, spending limits).

- Clean interfaces for budgeting, analytics and category tagging.

- Fast onboarding with e-KYC instead of branch visits.

Revolut in particular has scaled aggressively, with tens of millions of personal users, hundreds of thousands of business users, and very high annual transaction volumes, making it one of Europe’s most downloaded finance apps.

N26, a fully licensed German bank, serves several million active customers and processes tens of billions of euros in annual transactions, with relatively high per-customer transaction volumes compared to traditional retail banks.

The Structural Limitations

However, neobanks still sit on top of legacy rails:

- Transfers rely on SEPA, SWIFT, Faster Payments or local clearing systems.

- Cut-off times, weekends, and bank holidays still matter.

- Eligibility is tied to residency and jurisdiction, many emerging market users simply cannot open these accounts.

- As they mature, neobanks introduce subscription tiers, FX markups and assorted fees that reduce the “free” feel that early adopters enjoyed.

They remain a massive improvement over traditional banks, but for a segment of global users, remote workers, on-chain traders, cross-border freelancers, they are starting to look constrained.

Stablecoins vs Neobanks: Fees, Access and Control

24/7 On-Chain vs Banking Hours

Stablecoin transfers clear whenever the network is live. On fast chains or L2s, settlement can be near-instant and extremely cheap. In contrast, neobank transfers, even when initiated instantly in the app, still depend on clearing:

- SEPA credit transfers usually settle same day or next day.

- SWIFT wires can take days and incur intermediary bank fees.

- Weekends and holidays often delay processing.

For contractors who need to move funds quickly or traders who want to rebalance on Sunday night, that gap is meaningful.

Global Access: Wallet vs Local IBAN

Stablecoins are border-agnostic. A wallet can be created anywhere; access only depends on connectivity and platform rules. Apps like Crypto.com must follow local regulations for on-ramping and card issuance, but once a user is onboarded, they can move stablecoins globally with minimal friction.

Neobanks, by contrast, are tightly geo-fenced. Revolut is expanding into multiple new markets to capture cross-border corridors, but its services are still limited to a list of supported countries. Many developing markets simply aren’t eligible.

Fees and FX Spreads

Global money transfers via traditional rails are expensive. International remittances often carry percentage-level fees plus FX spreads, and the global average cost for sending small remittance amounts remains several percent of the principal.

Neobanks helped compress those costs, but they still earn revenue from:

- FX spreads (especially on weekends or large transfers).

- Subscription tiers for “better FX” or higher limits.

- ATM and out-of-network fees.

Stablecoins introduce a different cost structure:

- On-chain fees (gas) that can be very low on the right networks.

- Spreads and fees on fiat on- and off-ramps (exchanges, cash-out partners).

For high-frequency movers and larger transactions, stablecoins can be cheaper and more predictable, especially when moving value between crypto platforms or paying other on-chain users directly.

Yield and Rewards

Many crypto platforms, including Crypto.com, have offered:

- Yield-bearing stablecoins that pay interest or rewards for holding stablecoins.

- Cards that provide cashback in native tokens or other rewards.

These rewards are variable and come with platform risk, but they are often more aggressive and more global than neobank interest programs, which tend to be:

- Region-specific.

- Capped at certain balances.

- Sensitive to monetary policy and national regulation.

To a user who is comfortable with crypto risk, parking savings in USDT/USDC and earning yield via a reputable platform can look more attractive than low single-digit interest on a neobank savings account.

Why Revolut and N26 Users Are Pivoting to Crypto.com and USD Stablecoins

1. Cross-Border Payments Without Banking Friction

Global remittances and cross-border payments are a massive market, with flows measured in the hundreds of billions of dollars annually. Stablecoins provide an alternative path through:

- Employer pays in USDT/USDC.

- Recipient holds or swaps into local currency via P2P or local exchanges.

No SWIFT, no correspondent banks, and far fewer surprises on fees.

2. Inflation and Currency Devaluation

In countries with high inflation or unstable banking systems, holding savings in local currency inside a neobank account feels risky. USD stablecoins give users synthetic access to the dollar without needing a U.S. bank account.

Apps like Crypto.com make it trivial to:

- Convert local currency into USD stablecoins.

- Hold them long-term.

- Convert back only when needed for local expenses.

For many, this feels like a global savings account that is partially insulated from local macro shocks.

3. Better Rewards and Card Programs

Neobanks offer perks, but they must comply with banking rules and conservative risk models. Crypto-linked cards, on the other hand, are often structured around token incentives and can offer:

- Higher cashback percentages (funded by token economics and marketing budgets).

- Perks tied to staking or holding native tokens.

These structures are not risk-free, but they look extremely appealing to reward-maximizing users compared to many neobank loyalty schemes.

4. Access to Crypto-Native Opportunities

From one app like Crypto.com, users can:

- Buy and sell crypto.

- Hold stablecoins as a base asset.

- Access staking, lending, or yield products.

- Participate in token sales or DeFi integrations.

Neobanks generally offer limited crypto exposure, often:

- Only a small list of coins.

- Higher spreads.

- No direct access to DeFi or self-custody.

For users who see crypto as a core part of their finances, stablecoin-centric platforms feel like the real “hub.”

5. 24/7 Global Liquidity

Stablecoins move continuously across centralized exchanges, DeFi protocols, and wallets. Liquidity is global and never formally “closed.”

Neobanks are still deeply connected to regional systems:

- EUR accounts depend on SEPA.

- GBP accounts depend on UK clearing.

- Transfers between regions often need SWIFT.

For traders, DAOs, and cross-border teams, this fragmentation is increasingly unattractive.

6. Censorship and Account Freezes

Neobanks must follow strict AML and KYC rules. Sudden account reviews or freezes are not rare, especially for users with complex or crypto-related activity.

Stablecoins don’t remove compliance risk, but they do let users diversify:

- Some funds in bank/neobank accounts.

- Some in self-custodied wallets.

For users burned by previous freezes, holding a portion in stablecoins feels like a hedge.

7. App Fatigue and Mental Accounting

Neobanks encourage holding multiple fiat currencies (EUR, GBP, PLN, CHF, etc.). For some users, that’s powerful; for others, it becomes cognitive overload.

Sticking to USD stablecoins as a unit of account across platforms simplifies things:

- Earn in USDT/USDC.

- Price assets in USD.

- Only convert when paying specific bills.

Case Study: From Revolut to Crypto.com & USDC

Imagine a 29-year-old remote developer based in Eastern Europe:

- Clients pay in EUR and GBP.

- Their main hub is a Revolut EUR/GBP account.

Over time they notice:

- Weekend FX markups.

- Occasional delays on incoming international transfers.

- Limited direct access to DeFi or yield products.

They open a Crypto.com account, pass KYC, and start asking some clients to pay invoices in USDC instead of EUR via SEPA.

Incoming USDC:

- Arrives within minutes after the on-chain confirmation.

- Can be staked or placed in yield products.

- Can be swapped to local currency when needed and cashed out via card or local partners.

The user doesn’t close their Revolut account. Instead, they:

- Keep Revolut for local bills, direct debits, and physical card payments inside the EU.

- Use USDC/USDT on Crypto.com as their primary savings and cross-border working capital.

That hybrid pattern is what’s quietly shifting usage away from pure neobank dependency.

Risks and Trade-Offs: Stablecoins vs Regulated Neobanks

Stablecoin Risks

Even with solid reserves, stablecoins carry real risk:

- Peg stability: Extreme market stress can test whether 1:1 redemption holds.

- Reserve quality: Some issuers hold varying mixes of Treasuries, cash, and other assets; transparency and audits matter.

- Platform risk: Holding USDC on a centralized platform is not the same as holding it in self-custody. Exchange failures or freezes are possible.

- Regulatory changes: New laws in major jurisdictions can change which stablecoins are allowed or how they must operate.

Neobank Risks

Neobanks are not risk-free either:

- Many operate as e-money institutions, not fully insured banks in all markets.

- They still depend on partner banks and legacy rails.

- Accounts can be frozen or terminated if activity triggers AML flags.

However, they generally operate under clear national or EU banking regulations, which many users see as a safety anchor.

Choosing the Right Mix

The practical conclusion for most advanced users is not “stablecoins or neobanks,” but how much of each:

- Neobank for salary, local bills, and deposit insurance.

- Stablecoins for cross-border income, on-chain payments, and access to crypto markets.

This is exactly the overlap where Revolut, N26 and Crypto.com now compete.

Who Should Use What?

When Neobanks Make More Sense

Neobanks like Revolut and N26 are usually better if you:

- Receive your primary income via local payroll in EUR/GBP and pay local bills.

- Need direct debits, standing orders, and SEPA/ACH rails.

- Prioritize deposit insurance and simple, regulator-backed products over yield.

When Stablecoins and Crypto.com Are a Better Fit

USD stablecoins accessed through apps like Crypto.com lean in your favor if you:

- Work as a global freelancer or contractor, billing clients in multiple countries.

- Live in a high-inflation or capital-controlled country and want USD exposure.

- Use DeFi, on-chain trading, or crypto investing as a regular activity.

The Hybrid Strategy

Many power users end up with:

- A neobank account (or two): for regulated banking, salary, direct debits.

- One or more stablecoin platforms: for global liquidity, savings, and on-chain operations.

From the user’s perspective, Revolut and N26 slowly become “local wrappers,” while stablecoins plus platforms like Crypto.com become the de facto global account.

Conclusion

Neobanks rewired the interface to money, but not the underlying rails. Stablecoins rewired the rails themselves.

- Revolut and N26 still dominate for everyday Eurozone banking, card payments and insured savings.

- USD stablecoins on platforms like Crypto.com dominate when you need global, 24/7, programmable USD liquidity that can move between exchanges, wallets and DeFi in minutes.

For the growing segment of users who live online, earn globally and interact with crypto markets, stablecoins are quietly replacing neobanks as the primary “home base.”

That doesn’t mean neobanks will disappear, but it does mean they’re no longer the endpoint of fintech innovation.

The most resilient users will be the ones who understand both worlds: how regulated neobanks protect them locally, and how stablecoins unlock a much larger financial surface area globally.

Read Next:

- STBL Protocol Launches Stablecoin 2.0

- Stablecoins for Carbon Credits

- Rise Stablecoin Payroll Review 2026

FAQs:

1. Are stablecoins safer than keeping money in a neobank like Revolut or N26?

Not by default. Neobanks operate under banking or e-money regulation, sometimes with deposit protection schemes, while stablecoins depend on issuer reserves, platform security and evolving regulation. Stablecoins can be more flexible, but they add issuer, smart-contract and platform risk on top of normal market risk.

2. Why are Revolut and N26 users moving to Crypto.com and USD stablecoins?

Because stablecoins make cross-border payments faster, offer 24/7 access to USD value, and plug directly into crypto markets and yield products. For remote workers, traders and global freelancers, that combination can be more useful than a pure neobank account.

3. Can I use stablecoins like a normal bank account for salary and bills?

In some cases yes: clients can pay invoices in USDT or USDC, and platforms like Crypto.com let you spend via cards or convert to local currency. But stablecoins usually don’t support traditional direct debits and utilities in the same way a bank account does, and they are not a legal substitute for a regulated bank in most jurisdictions.

4. Is Crypto.com a bank or just a crypto platform with cards?

Crypto.com is a regulated crypto exchange and financial services platform, not a traditional bank. It operates under specific licenses in different regions and partners with banks for card issuance and some fiat services. Users should treat it as a crypto platform with strong regulatory coverage, not as a full replacement for a local bank.

5. What is the best way to combine a neobank account with stablecoins?

A common setup is: use Revolut or N26 for local salary, bills and insured savings, and use stablecoins on Crypto.com or similar platforms for global income, on-chain activity, and yield. Move only the amount you’re comfortable putting into crypto rails, and always keep an eye on both regulatory changes and issuer transparency.

{kind=link}