Table of Contents

Stablecoin recurring revenue is simply the predictable, ongoing income generated from the assets backing a stablecoin or the services built on top of it. Because stablecoins are designed to hold a steady value, unlike most other crypto assets, they’re a perfect foundation for building sustainable financial models. This income can come from a few different places, like earning interest on reserves, charging small transaction fees, or offering lending services.

From Digital Dollars to Revenue Engines

Stablecoins have grown up. They started as a simple bridge to move money between traditional finance and the crypto world, but now they’re much more. Today, they form a fundamental layer for creating powerful and predictable financial models. It’s better to think of them not as static digital dollars, but as dynamic assets that can generate consistent, recurring income for the companies and ecosystems that issue them.

Think about it like a regular bank. A bank doesn't just sit on your deposits; it puts that money to work by lending it out to earn interest. Stablecoin issuers do something similar. They don't just lock away the collateral backing their tokens. They actively manage these reserves and build services around their stablecoin to create multiple streams of income.

The Core Revenue Concepts

The ways stablecoins generate recurring revenue are varied, but most fall into a few key categories. These are the models that form the bedrock of this new digital economy, and we'll be diving deep into each one.

- Yield from Reserves: This is the most straightforward and common model. Issuers take the collateral (like U.S. dollars) and invest it in safe, interest-bearing assets. Think U.S. Treasury bills.

- Transaction and Custody Fees: These are small fees charged whenever someone creates (mints), cashes out (redeems), or sends stablecoins. Over millions of transactions, these tiny fees add up to a serious amount of revenue.

- Seigniorage: This one is a bit different and is mostly used by algorithmic stablecoins. It’s the profit made by creating new tokens for less than their market value when demand for the stablecoin goes up.

The scale of this ecosystem is already staggering. The recent explosion in stablecoin use globally proves just how essential they’ve become. For example, stablecoins made up 30% of all on-chain crypto transaction volume in the first seven months of a recent year, with total volume soaring past $4 trillion. The 2025 TRM Labs report on crypto adoption has some great data on this. This incredible volume opens up a massive opportunity for fee generation and other revenue-producing activities.

A stablecoin isn't just a token; it's the foundation for a financial ecosystem. Its value lies not only in its stability but in the economic activity it enables and the predictable revenue it can generate.

To give you a quick overview, here’s how the main revenue models stack up against each other.

Key Stablecoin Revenue Models at a Glance

This table provides a snapshot of the primary recurring revenue streams generated by stablecoins, where the money comes from, and who typically benefits.

| Revenue Model | Source of Revenue | Primary Beneficiary |

|---|---|---|

| Yield on Reserves | Interest earned from investing collateral in low-risk assets (e.g., T-bills). | Stablecoin Issuer |

| Transaction Fees | Small fees charged for minting, redeeming, or transferring tokens. | Issuer or Protocol |

| Seigniorage | Profit from creating new tokens when demand exceeds supply. | Protocol Treasury/DAO |

| Lending & Liquidity | Interest and fees from lending out stablecoins or providing liquidity. | Lenders & Liquidity Providers |

These models are just the starting point. They can be combined and adapted in countless ways, creating sophisticated financial products that are both stable and profitable.

Getting a handle on these foundational models is the first step to seeing the full potential of stablecoins as financial tools. Each approach offers a different way to generate income, with its own set of benefits and risks. For anyone curious about how this revenue translates into returns for token holders, our guide on earning yield with stablecoins takes a closer look at the investment side of things. Now, let’s break down how these concepts actually work in the real world.

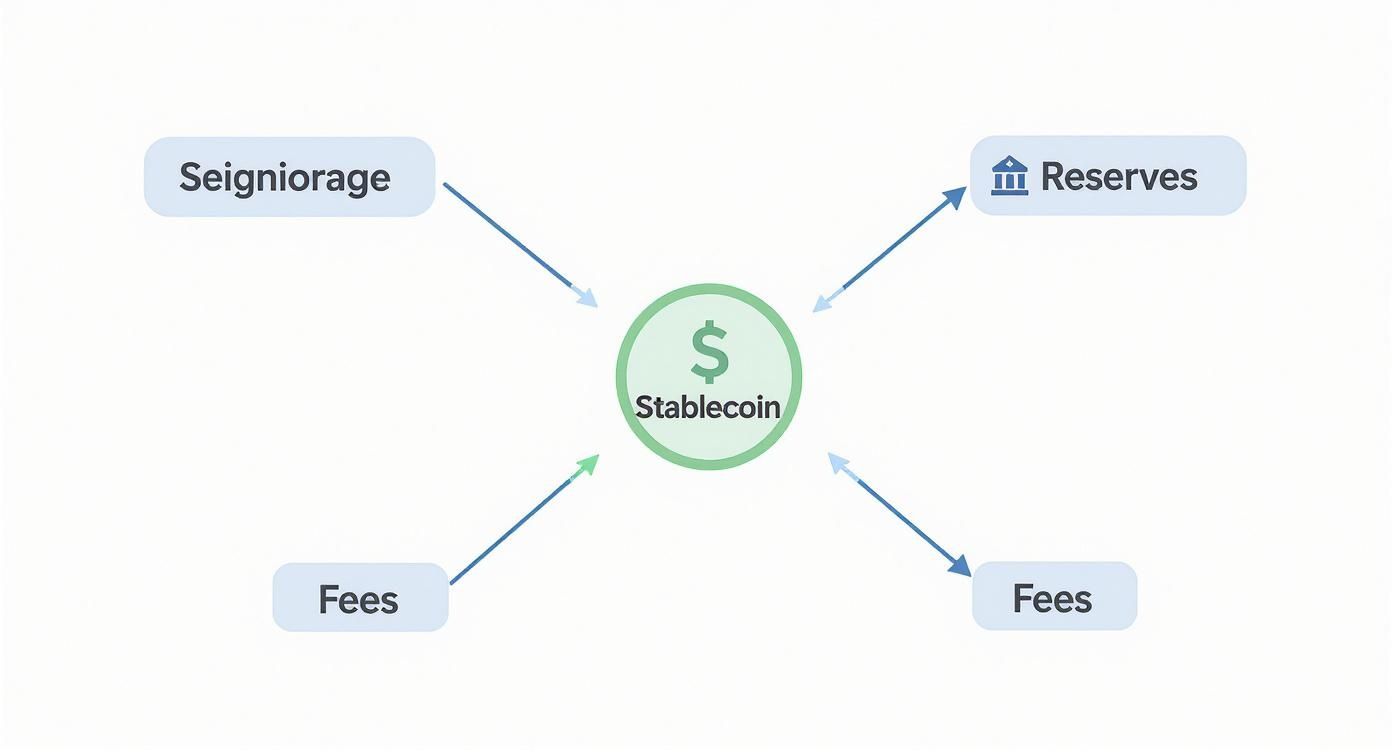

The Core Revenue Models Powering Stablecoins

If you want to grasp how stablecoins make money, stop thinking of them as just crypto tokens. Instead, picture the issuers as a new breed of financial institution. Like any bank or asset manager, they've built foundational methods for generating predictable, recurring income.

These core models are the engines driving the whole system. They're what turn a simple digital dollar into a surprisingly productive financial asset. Let's pull back the curtain on the three main ways stablecoins generate revenue.

This diagram gives you a bird's-eye view of how the pieces fit together—issuing the currency, managing the reserves, and facilitating transactions all contribute to the bottom line.

As you can see, the stablecoin itself is the central product, but the real money is made from the functions built around it.

Yield Generation From Reserve Assets

For asset-backed stablecoins, the biggest and most reliable revenue stream comes from the yield earned on their reserves. This is the bread and butter for the giants in the space, like Circle (USDC) and Tether (USDT).

It’s an old-school banking play. When you deposit cash into your savings account, the bank doesn’t just let it collect dust. They put that capital to work, investing it in low-risk assets like government bonds. They pay you a tiny slice of interest and pocket the difference. That's their profit.

Stablecoin issuers do the exact same thing. For every digital dollar they issue, they hold a corresponding dollar of real-world assets in a reserve. A huge chunk of these reserves is invested in safe, highly liquid assets—primarily U.S. Treasury bills (T-bills).

- Here's how it works: An issuer holds $10 billion in reserves. They invest it into T-bills that are yielding 5% annually.

- The result? That issuer pulls in $500 million in recurring revenue each year, just from interest payments.

This model is incredibly potent because it scales directly with the stablecoin's market cap. The more people who buy and hold USDC or USDT, the bigger the reserve pool gets, and the more revenue flows in from the yield.

The beauty of the reserve yield model is its simplicity and predictability. It’s a time-tested financial strategy from traditional finance, now applied to the digital asset world to create a robust stream of income.

Transaction and Custody Fees

While reserve yield is the heavyweight champion, transaction and custody fees provide a steady, predictable income stream based on usage. These are small charges applied at different points in a stablecoin's life.

Think about using a payment processor like Stripe or PayPal. Every time money moves, they shave off a tiny percentage as a fee. It seems insignificant, but over millions of transactions, it adds up to a massive amount of revenue. Stablecoin issuers and the platforms that support them use the same logic.

You'll typically see fees like these:

- Minting Fees: A small charge for creating brand-new stablecoins.

- Redemption Fees: A charge for cashing out stablecoins back into regular fiat currency.

- Transfer Fees: Charges for moving stablecoins between wallets or across different blockchains.

While on-chain transfers are usually subject to network gas fees, issuers and platforms can tack on their own service charges. This is especially common for institutional clients who need to process high volumes and require secure custody services.

Seigniorage in Algorithmic Models

Seigniorage is a fancy word borrowed straight from central banking. At its core, it's the profit a government makes just by issuing currency. For example, if it costs 5 cents to print a $1 bill, the seigniorage is the remaining 95 cents of pure profit.

In the crypto world, seigniorage is almost exclusively tied to algorithmic stablecoins. These aren't backed by cash or T-bills. Instead, they rely on complex algorithms and smart contracts to manage their supply and hold their price peg.

Here’s a simplified look at the process:

- Demand Spikes: Demand for the stablecoin rises, pushing its price slightly above $1.00.

- The Protocol Steps In: To bring the price back down, the protocol automatically mints new stablecoins, increasing the supply.

- Profit Is Made: The protocol can then sell these newly minted tokens at their $1.00 market value. Since they cost virtually nothing to create, the entire sale price is profit.

This profit is usually sent to a treasury controlled by the protocol or distributed to people holding a separate governance token. It's a powerful idea, but it's also incredibly risky. The entire system depends on constant demand and faith in the algorithm's mechanics. The spectacular collapse of TerraUSD (UST) is a harsh lesson in what happens when that faith disappears.

These three models often work together, but they also set the stage for more advanced strategies. To see how these assets are put to work in DeFi, you can dive deeper into the mechanics of stablecoin lending and learn how it creates returns for everyone involved.

Advanced Strategies for Maximizing Recurring Income

While the yield from reserves and basic transaction fees are the bread and butter of stablecoin revenue, the most innovative protocols are looking far beyond that. They're weaving stablecoins into the very fabric of decentralized and traditional finance, creating more dynamic and integrated services.

These advanced strategies turn stablecoins from a simple digital dollar into an active, productive asset. This creates a powerful flywheel effect: greater utility pulls in more users, which in turn unlocks even bigger revenue opportunities. Let's dig into how these more sophisticated models actually work.

Lending and Liquidity Provision in DeFi

One of the most potent ways to generate stablecoin recurring revenue is to put those assets to work in Decentralized Finance (DeFi). Instead of letting reserves sit idle, stablecoins can be lent out or used to grease the wheels of trading, earning interest and fees along the way.

It’s essentially a digital money market, open 24/7. Users can put up their stablecoins as collateral to borrow other crypto assets, or they can simply lend their idle stablecoins to others and earn a variable interest rate.

This plays out in two main ways:

- Decentralized Lending: Think of protocols like Aave and Compound as automated banks. You deposit your stablecoins into a lending pool and immediately start earning interest, which is paid by borrowers on the other side. The protocol itself skims a small fee off the top, creating its own steady revenue stream.

- Liquidity Provision: On decentralized exchanges (DEXs) like Uniswap, users called liquidity providers (LPs) deposit pairs of assets—say, USDC and ETH—into a shared pool. This pool allows anyone to trade between those two assets. For providing this critical service, LPs earn a cut of the trading fees, which can add up to a significant income.

For investors trying to make the most of these opportunities, a stablecoin yield aggregator can be a game-changer, automatically hunting down the best rates across the DeFi landscape.

Building Subscription and Payment Rails

The next frontier for stablecoins is becoming the financial plumbing for the modern digital economy. Businesses are desperate for more efficient, global, and cheaper ways to handle payments, especially for recurring models like subscriptions. Stablecoins are the perfect tool for the job.

Companies like Stripe and xMoney are building the infrastructure that allows businesses to accept stablecoins for everything from SaaS subscriptions to e-commerce checkouts. It’s a win-win. Merchants get much lower transaction costs and almost instant settlement, a massive improvement over the sluggish and costly traditional banking system. In fact, some businesses on Stripe have seen their payment processing costs sliced in half by switching to stablecoins.

"Stablecoins are no longer experimental. What they need is compliance, trust, and infrastructure to scale... Together, we’re building the rails for the next era of global finance." - Greg Siourounis, Co-Founder & CEO of xMoney

This evolution opens up a major revenue stream for the payment processors themselves. They charge a small fee to handle these transactions and convert the stablecoins back to fiat for the merchant. With the annual settlement volume for stablecoins already blowing past $7 trillion, the potential market for these payment rails is simply enormous.

This model is particularly powerful for businesses with a global customer base. It completely removes the usual headaches of cross-border payments, currency conversion fees, and long settlement delays.

Protocol Revenue Sharing Models

A more crypto-native take on recurring revenue involves sharing a protocol's earnings directly with its community. This strategy brilliantly aligns the interests of the protocol with the financial well-being of its token holders.

In this model, a slice of the revenue generated from transaction fees, lending interest, or even seigniorage gets funneled into the protocol’s treasury. From there, it’s distributed to the people who hold and "stake" the protocol's native governance token.

Here’s a simple breakdown of how it works:

- Revenue Generation: The protocol earns income from its operations, like fees from its decentralized exchange.

- Collection: All that revenue flows into a treasury or a decentralized autonomous organization (DAO) managed by smart contracts.

- Distribution: The funds are then periodically paid out to governance token stakers, usually in the form of stablecoins or another valuable crypto asset.

This creates a direct, tangible incentive for users to participate in the ecosystem and care about its long-term success. When the protocol thrives, its token holders get a check in the mail, so to speak. It’s a powerful way to build loyalty and a strong, invested community.

The success of these advanced strategies is crystal clear when you look at the financials of major issuers. Circle, the firm behind USDC, recently reported reserve income of $711 million and an additional $29 million in other revenues in a single quarter. This "other revenue" category grew substantially year-over-year, driven largely by the expansion of subscription and transaction services built on top of USDC. You can dive into Circle's full financial results to see the growth for yourself.

How Top Companies Generate Stablecoin Revenue

It’s one thing to talk about recurring revenue models in theory, but seeing them in action is where it really clicks. To make this tangible, let's pull back the curtain on how a couple of industry giants are turning stablecoins into serious, predictable income.

We'll look at Circle and Coinbase, two companies that have mastered this game, albeit with different playbooks. Both have woven USD Coin (USDC) into the fabric of their businesses, proving just how mature and powerful this market has become. Their success offers a clear blueprint for anyone looking to build sustainable revenue in the digital asset space.

Circle: The Power of Reserve Yield

Circle, the issuer behind USDC, is a masterclass in monetizing reserves. Their main revenue driver is the interest they earn on the colossal pool of assets backing every single USDC. It's a beautifully simple model that scales directly with USDC's adoption.

Think of it this way: Circle operates like a modern digital treasury. For every USDC issued, they hold a corresponding dollar’s worth of highly liquid, safe assets—primarily short-term U.S. Treasury bills.

The real genius of Circle's model is its elegant simplicity. They've taken a centuries-old banking principle—earning a spread on deposits—and applied it to the crypto economy. This creates a predictable and incredibly profitable revenue stream.

When interest rates climb, this model becomes a cash-generating machine. For instance, if Circle holds $30 billion in reserves and earns an average yield of 5% on its T-bills, that translates to a cool $1.5 billion in annual revenue, before factoring in operational costs. This income isn’t tied to the wild swings of crypto trading; it's anchored to the stability of U.S. government debt, making it one of the most reliable business models in the entire industry.

This straightforward yet powerful approach has even caught the eye of traditional finance titans, a trend you can explore further by reading about how BlackRock launched its own compliant stablecoin.

Coinbase: From Trading Fees to Subscription Services

Coinbase presents a different, but no less impressive, strategy. For years, its business lived and died by transaction fees from crypto trading—a notoriously volatile source of income that ebbs and flows with market hype. Recognizing this vulnerability, Coinbase has been on a mission to build a more resilient business, and USDC is at the heart of that transformation.

As a co-founder of the consortium behind USDC, Coinbase is deeply integrated into its ecosystem. This unique position allows the company to generate revenue from multiple angles. It's not just about earning a piece of the reserve yield; Coinbase also makes money from USDC-related services, like providing custody solutions for institutions and enabling USDC payments for businesses.

This strategic pivot is completely reshaping the company’s finances. Coinbase is consciously moving away from its old reliance on trading fees toward a much more balanced model. In fact, subscriptions and services now account for 41% of total revenue—a massive leap from just a few years ago when trading fees made up a staggering 96% of their income. You can discover more insights about this strategic pivot and its profound impact on the company’s long-term health.

Comparing Revenue Strategies of Leading Stablecoin Issuers

The table below offers a side-by-side look at how these two leaders are carving out their share of the stablecoin market. This comparative analysis really highlights the primary revenue drivers for major stablecoin ecosystems and showcases their different business models.

| Issuer/Platform | Primary Revenue Model | Secondary Revenue Model | Key Success Factor |

|---|---|---|---|

| Circle | Yield on Reserve Assets | Transaction Fees for Minting/Redemption | Maximizing the size and yield of its reserve portfolio while maintaining trust. |

| Coinbase | Subscriptions & Services | Interest Income from USDC Balances | Integrating USDC deeply into its platform to drive user engagement and service adoption. |

What Circle and Coinbase both prove is that stablecoin recurring revenue is far from a niche concept—it's a tested, scalable, and highly effective business model. Whether you're directly managing reserve assets or building a suite of services on top of a stablecoin, these companies show exactly how to turn digital dollars into dependable, long-term income.

Navigating the Risks and Regulatory Headwinds

While the promise of recurring revenue from stablecoins is incredibly attractive, it's a field littered with potential landmines. Anyone looking to build a sustainable income strategy here—whether you're an investor, an issuer, or on a product team—needs to go in with their eyes wide open. You're not just navigating financial and tech hurdles; there's a heavy dose of politics, too.

Simply put, you can't ignore the headwinds. A healthy dose of realism is required to see past the hype and acknowledge the very real dangers that can sink even the most well-designed revenue model. From reserve assets plummeting in value to a regulator bringing down the hammer overnight, the path to steady income is anything but straight.

Understanding Core Financial Risks

At the very center of any stablecoin operation are the raw financial risks that can threaten its peg and, in turn, its ability to generate revenue at all. Two giants loom largest: the risk tied to the reserves themselves and the terrifying possibility of a de-peg event.

Reserve Risk is the classic "what if the backing isn't worth what we think it is?" problem. For a fiat-backed stablecoin, this means the government bonds, cash equivalents, or other assets held in the vault could suddenly lose value. If that happens, the issuer might not have enough collateral to back every token 1:1. Trust evaporates in an instant, and that's usually the beginning of the end.

The stability of a stablecoin is only as strong as the assets that back it. Transparency isn't a feature; it's a prerequisite for long-term trust and viability.

This is why the biggest players are so obsessed with holding high-quality, ultra-liquid assets, like short-term U.S. Treasury bills. It's also why they push out regular public attestations and subject themselves to full financial audits—they have to constantly prove their reserves are sound.

De-pegging Risk is the moment of truth when a stablecoin breaks its 1:1 promise. It can be triggered by a sudden panic, a deep flaw in its design, or just sheer market chaos. We all saw what happened with TerraUSD (UST). It was a brutal lesson in how fast an algorithmic stablecoin can spiral to zero once the market loses faith, incinerating billions of dollars along the way.

The Looming Specter of Regulation

Maybe the single biggest wildcard facing the entire stablecoin industry is Regulatory Risk. Around the world, governments and financial watchdogs are scrambling to figure out what these things are and how to police them. The rules of the game can change in a flash, completely upending everything from how reserves must be held to what kinds of services an issuer can legally provide.

This fog of uncertainty makes it incredibly difficult to build a business model for the long haul. The big questions regulators are asking include:

- Asset Classification: Are stablecoins securities? Commodities? A whole new category of money? The answer determines which rulebook applies.

- Issuer Requirements: Will issuers be forced to meet the same strict capital, licensing, and reporting standards as traditional banks?

- Consumer Protection: New laws are being drafted to shield users from fraud and guarantee that issuers can always honor redemptions.

Lawmakers in major economies are actively debating new legislation, and the final text will rewrite the future of this industry. For example, you can learn more about how upcoming legislation like the 2025 STABLE Act could impact issuers and the market as a whole. For anyone serious about this space, staying plugged into these developments isn't just a good idea—it's essential for survival. The only way to manage this risk is to get ahead of it through proactive compliance and open dialogue with policymakers.

Building Your Own Stablecoin Revenue Strategy

Alright, let's move from theory to action. It’s one thing to understand how stablecoins can make money, but it’s another to build a real-world plan. Whether you're an issuer mapping out a new coin, a product manager plugging one into your platform, or an investor scouting for solid bets, you need a clear-eyed strategy to capture stablecoin recurring revenue.

For the builders—the issuers and product teams—the game is all about creating a financial model that lasts. This means weaving together smart reserve management, a sensible fee structure, and services that actually give users a reason to stick around. You have to think long-term to build an ecosystem that won’t fold at the first sign of market turbulence.

Investors, on the other hand, need to put on their detective hats. Your job is to cut through the marketing noise and see a project for what it really is. That means getting your hands dirty with the data to truly grasp the risks and rewards of each revenue stream.

A Framework for Issuers and Product Teams

To build a revenue strategy that stands the test of time, you need to lay the right groundwork. Before you even think about launching, your team needs to run through a checklist to make sure every critical piece is in place. This isn't just about ticking boxes; it's about making sure your business goals line up with market reality.

Think of it in terms of these core pillars:

- Reserve Composition: What's actually backing your stablecoin? You should be prioritizing high-quality, liquid assets—think short-term U.S. Treasury bills. This is your best shot at maximizing both yield and trust. The makeup of your reserves directly shapes your primary revenue stream and how stable people think your coin is.

- Fee Structure Design: How will you make money on a daily basis? Are you charging for minting, redeeming, or simple transactions? You need a clear fee model that’s competitive enough to attract users but still profitable. It's a constant balancing act between higher fees (more revenue now) and lower fees (more users later).

- Regulatory Compliance Path: Don’t wait for regulators to knock on your door. Get ahead of it. Engage with them early, get the right licenses, and prepare for transparent audits from day one. Skipping this step is a rookie mistake that can sink your entire project.

An Investor's Guide to Evaluating Opportunities

If you're an investor, you're looking at this from a completely different angle. Your main focus is on sharp due diligence and sizing up the key performance indicators (KPIs) that scream "long-term potential." You're hunting for projects that can generate consistent returns over time.

A stablecoin's true value isn't just its peg; it's the economic engine built around it. Investors who learn to analyze that engine—its efficiency, risks, and revenue streams—will find the most sustainable opportunities.

Start your investigation by zeroing in on these metrics:

- Reserve Transparency and Quality: Does the issuer show you what’s in the vault? Demand regular, third-party attestations. The quality of the assets is a massive tell; a reserve with 90% in T-bills is a world away from one filled with riskier corporate debt.

- Protocol Revenue and Health: Get on-chain and look at the numbers. Track the protocol’s revenue from fees, lending, and anything else it’s doing. If you see strong, steady cash flow being paid out to token holders, that's a very good sign.

- Community and Ecosystem Growth: Is anyone actually using this thing? A rising number of active users, developers building on the platform, and dApps integrating the stablecoin points to a healthy, growing network. That network effect is often the best clue you'll get about future revenue.

A Few Common Questions

Diving into stablecoin revenue models can feel a bit complex, whether you're building a protocol, investing, or just trying to understand the landscape. Let's clear up a few of the most frequent questions that come up.

What's the Go-To Revenue Model for Most Stablecoins?

For the big players like USDC, the primary and most dependable source of recurring revenue comes from the yield on their reserve assets. Think of it this way: when you buy a USDC, your dollar doesn't just sit in a vault. The issuer invests that massive pool of funds into very safe, interest-earning assets like U.S. Treasury bills. The interest collected on these reserves is their main income, and it scales directly with the stablecoin's total supply.

Can I Make Recurring Income from Stablecoins as an Individual?

Yes, definitely. Individuals have several solid pathways to earn recurring income by putting their stablecoins to work in the DeFi world. The most common strategies include:

- Lending: You can deposit your stablecoins into lending protocols like Aave and earn interest from people who borrow them.

- Providing Liquidity: By adding your stablecoins to a liquidity pool on a decentralized exchange (DEX), you can earn a percentage of the trading fees for that pair.

- Staking: Some protocols allow you to "stake," or lock up, your stablecoins to help secure their network or for other purposes, and they'll reward you for it.

How Do Algorithmic Stablecoins Make Money if They Don't Have Reserves?

Algorithmic stablecoins operate on a completely different model. Instead of backing their coins with real-world assets, they rely on code and economic incentives. Their main revenue driver is often seigniorage—essentially, the profit made when the protocol mints new stablecoins for less than they're worth during periods of high demand. They also earn revenue from network transaction fees when users mint, burn, or trade the stablecoin within its own ecosystem.

Be aware, though: while the profits can be attractive, the revenue models for algorithmic stablecoins are inherently riskier. Their entire system hinges on user confidence and flawless code, a combination that has historically shown its fragility during major market downturns.

Is Earning Income with Stablecoins Actually Safe?

It’s safer than trading highly volatile crypto, but it's certainly not risk-free. You're still exposed to potential issues like bugs in smart contracts, the risk of a protocol becoming insolvent, a stablecoin losing its peg, or sudden regulatory crackdowns. Before you put any money to work, it's absolutely critical to do your own homework on the platform and understand the specific risks involved with any strategy you're considering.

At Stablecoin Insider, we cut through the noise to give you the analysis and news needed to navigate the digital asset economy. Explore our expert insights to make smarter decisions at https://stablecoininsider.com.

{kind=link}