Table of Contents

Think of stablecoin borrowing like this: you have valuable assets—in this case, crypto like Bitcoin or Ethereum—and you need cash, but you don't want to sell. So, you use your crypto as collateral to take out a loan in a stable digital currency, like USDC or USDT. It’s a lot like getting a home equity loan, where you tap into the value of your house without putting it on the market.

A New Way To Unlock Your Crypto's Value

Stablecoin borrowing has quickly become a cornerstone of the crypto economy, giving people a powerful way to get their hands on cash-like assets without selling their long-term holdings. Why is that so important? Selling your crypto can create a tax headache and means you miss out on any future price gains.

By pledging your assets to a lending protocol or a centralized company, you can meet short-term cash needs while your original investment continues to ride the market. The core idea is brilliant in its simplicity: you separate the ownership of your asset from its immediate cash value. This creates a flexible financial tool that’s useful for everyone from professional traders to everyday crypto enthusiasts.

Why Is This Practice Growing So Fast?

The explosive growth in stablecoin borrowing comes down to its incredible versatility and efficiency, especially when compared to the old-school financial world. It opens up a path to liquidity that is faster, easier to access, and available 24/7, no matter where you are.

The main drivers behind its popularity are pretty clear:

- Tax Efficiency: In most places, taking out a loan isn't a taxable event. That means you can get cash without having to immediately pay capital gains taxes on your crypto's appreciation.

- Retaining Upside Potential: You never give up ownership of your collateral. If your Bitcoin or Ethereum skyrockets in value, that upside is still yours.

- Speed and Accessibility: DeFi protocols let you get a loan almost instantly. There are no bank managers, no credit checks, and no waiting days for approval.

The numbers speak for themselves. In Q3 2025, the total market for crypto-collateralized loans ballooned to a record $73.59 billion. A huge chunk of that, $24.37 billion, came from centralized stablecoin borrowing alone—a staggering 239.4% jump from the bear market lows in late 2023. These figures aren't just noise; they show a powerful, expanding market and prove how essential stablecoin borrowing has become. For a deeper dive, you can explore the full Q3 2025 crypto leverage report on galaxy.com.

To help you get a quick handle on these concepts, here’s a simple breakdown of the key aspects.

Key Aspects Of Stablecoin Borrowing At A Glance

| Concept | Simple Explanation | Primary Benefit |

|---|---|---|

| Collateral | Your existing crypto (e.g., BTC, ETH) that you pledge to secure a loan. | You don't have to sell your assets to get cash. |

| Stablecoin Loan | The money you borrow, denominated in a stable asset like USDC or USDT. | You get predictable, stable value to use for spending or investing. |

| Liquidation | If your collateral's value drops too low, the protocol sells it to repay your loan. | Protects lenders from losing money, which keeps the system running. |

| Interest Rate | The fee you pay for borrowing, which can be fixed or variable. | Allows lenders to earn a return for providing their capital. |

This table just scratches the surface, but it highlights the fundamental give-and-take that makes this system work for both borrowers and lenders.

Stablecoins act as the essential bridge between the volatile world of crypto assets and the stability of traditional fiat currency. Understanding how stablecoins work is the first step to mastering borrowing and lending in the digital economy.

Before we get into the nuts and bolts of how these loans work, it’s worth making sure you understand the foundation. If you’re new to these "digital dollars," our guide on how stablecoins work is a great place to start.

How Stablecoin Loans Actually Work

Think of it like a high-tech pawn shop. At its core, stablecoin borrowing follows a principle that's been around for centuries: you put up something valuable as collateral to get cash. The only difference is, instead of a vintage watch, your collateral is a digital asset like Bitcoin (BTC) or Ethereum (ETH), and the "cash" you get is a stablecoin.

This clever process lets you tap into the value of your crypto holdings without having to sell them. You get the cash you need, but you keep your long-term investment strategy firmly in place. Let's dig into how the different mechanics behind these loans work, starting with the most common one.

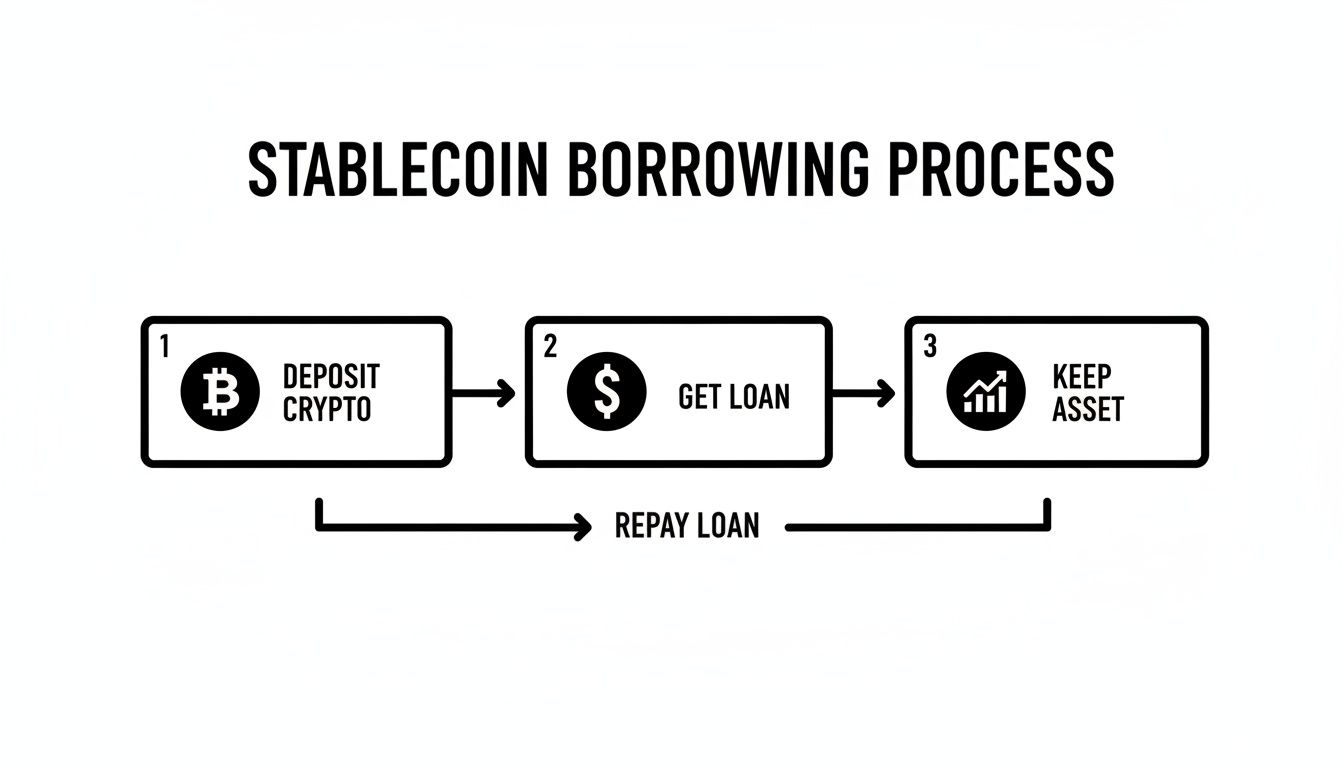

The Foundation: Overcollateralized Loans

The vast majority of stablecoin lending is built on a simple, powerful concept: overcollateralized loans. In plain English, this means you have to deposit collateral that’s worth more than the amount you want to borrow. It's the lender's safety net in the wild, volatile world of crypto.

Say you're holding $10,000 worth of Ethereum. You could lock that ETH up in a lending protocol and instantly borrow, for example, $6,000 in USDC. Just like that, you have cash to use, but you still own your original ETH and can benefit if its price goes up.

The whole system is governed by one critical metric: the Loan-to-Value (LTV) ratio.

The Loan-to-Value (LTV) ratio is simply the percentage of your collateral's value that you can borrow. If a protocol offers a 60% LTV, it means for every $100 of collateral you deposit, you can borrow up to $60 in stablecoins.

Protocols don't treat all crypto assets equally. They'll set different LTVs based on an asset's volatility. A blue-chip crypto like Bitcoin might get a higher LTV (say, 75%), while a newer, more volatile altcoin might have a much lower one (maybe 40%). This tiered approach is crucial for protecting the lending pool from a sudden market crash.

Here's a quick visual of how this borrowing flow plays out.

As you can see, you can deposit your crypto to get an immediate stablecoin loan, all while hanging on to your original asset and its potential upside.

Understanding Liquidation: The Point of No Return

So, what happens if the value of your collateral takes a nosedive? If it drops enough, your loan becomes risky for the lender. To protect themselves, every protocol has a liquidation threshold—a specific LTV percentage that acts as a trigger point.

If your LTV creeps up and hits this threshold, the protocol’s smart contracts will automatically sell off some (or all) of your collateral to pay back the loan. To add insult to injury, they usually tack on a penalty fee. This is, without a doubt, the single biggest risk in stablecoin borrowing, and it's why you absolutely have to keep a close eye on your loan's health. You can learn more about the mechanics of how crypto-collateralized stablecoins are secured against this very risk.

Advanced Borrowing Mechanisms

While overcollateralized loans are the bread and butter of DeFi lending, a few other specialized methods have emerged for different use cases.

Undercollateralized Loans

These work a lot more like traditional bank loans, where your reputation or credit history allows you to borrow without putting up the full collateral amount. In DeFi, this is still a pretty new and experimental area. It's usually reserved for institutions or for protocols that are trying to build on-chain identity and trust systems. They’re not something the average crypto user can access just yet, but they point to where the space is heading.

Flash Loans

Flash loans are one of DeFi's most mind-bending innovations. They are literally instant, uncollateralized loans that have one unbreakable rule: they must be borrowed and repaid in the exact same blockchain transaction.

It’s like a financial superpower that lasts for a fraction of a second. An arbitrage trader could use a flash loan to pull off a complex trade that would otherwise require huge capital. Here’s how it works:

- Borrow $1,000,000 in USDC via a flash loan from a protocol like Aave.

- Instantly use that USDC to buy a discounted asset on one decentralized exchange.

- Immediately sell that asset for $1,001,000 on another exchange where the price is higher.

- Repay the original $1,000,000 loan.

- Pocket the $1,000 profit.

The magic is that if any step in that sequence fails, the entire transaction is reversed as if it never happened. This makes the loan completely risk-free for the protocol. It’s a powerful tool, but it's really designed for developers and highly sophisticated traders.

Finding The Right Lending Platform For You

So, you've wrapped your head around how stablecoin borrowing works. The next big question is: where do you actually do it? The crypto world is basically split into two camps for this: Decentralized Finance (DeFi) and Centralized Finance (CeFi). Each has a completely different feel and comes with its own set of trade-offs.

Think of DeFi as the self-checkout lane at the grocery store. It's fully automated. Platforms like Aave and Compound run on smart contracts—essentially just code on a blockchain that executes loans without a single person in the middle. You connect your wallet, deposit your crypto, and borrow against it by interacting directly with the protocol.

CeFi, on the other hand, is more like visiting a bank teller. Companies such as Nexo offer a more hands-on, managed service. You sign up for an account, send your crypto to their platform for safekeeping (custody), and borrow from them. It’s a path that often feels a lot more comfortable for newcomers because there’s a company name and a support team behind the curtain.

Decentralized Finance Protocols

DeFi platforms are the wild, beating heart of this new financial system. They're built on liquidity pools—giant pots of crypto supplied by people all over the world who earn a return on their deposits. When you take out a loan, you're tapping into this community-sourced capital.

What really defines the DeFi experience?

- You're in control. This is what "self-custody" means. You never hand over your private keys. You interact with the code, but your assets stay in your wallet's control until you decide otherwise.

- Everything is out in the open. Because it's all on a public blockchain, anyone can audit the loan books and verify the protocol is solvent. It’s radical transparency.

- No one can say no. As long as you have a crypto wallet and enough collateral, you can borrow. It doesn't matter who you are or where you live.

The whole DeFi scene is also incredibly dynamic, with big decisions often made by community votes from people who hold the platform's governance token.

Centralized Finance Providers

CeFi platforms are the bridge connecting the old financial world with the new one. They look and feel much more like the fintech apps you’re probably already used to, with actual offices, support staff, and a need to comply with regulations.

Their approach to borrowing is built for simplicity and convenience:

- They hold your assets for you. This is the "custodial" model. It makes things much simpler—no need to worry about managing keys or interacting with smart contracts—but it does require trusting the company to keep your funds safe.

- The user experience is smooth. CeFi providers invest heavily in polished mobile apps and websites that feel just like your online banking portal.

- They offer more than just loans. You’ll often find a whole suite of products, like crypto savings accounts, credit cards backed by your digital assets, and easy ways to move money to and from your bank account.

This model is a magnet for anyone who values a straightforward experience and wants the safety net of a company to call if something goes wrong.

Comparing DeFi And CeFi Lending Platforms

So, which one is for you? It really boils down to what you value most. Are you a crypto purist who prioritizes total control and transparency? Or do you lean towards a seamless, user-friendly experience where you have someone to help you out?

The decision hinges on a fundamental trade-off: DeFi offers greater autonomy and transparency at the cost of higher personal responsibility, while CeFi provides convenience and support but requires you to trust a central entity with your assets.

The good news is that both sides of the aisle are booming. By June 2025, the total market cap of stablecoins shot up to $251.7 billion, a 22% jump from earlier in the year. This growth is a clear sign that both individuals and bigger players are getting comfortable using stablecoins for everything from payments to credit. For a deeper dive, check out the top five facts about stablecoins in 2025 on bitpowr.com.

To make the choice a bit easier, the table below breaks down the key differences between the two.

| Feature | DeFi Platforms (e.g., Aave, Compound) | CeFi Platforms (e.g., Nexo) |

|---|---|---|

| Asset Custody | Non-custodial; you control your private keys. | Custodial; the company holds your collateral. |

| Privacy | Pseudonymous; transactions linked to a wallet address. | Requires KYC/AML identity verification. |

| Interest Rates | Variable rates determined by supply and demand algorithms. | Often fixed or tiered rates set by the company. |

| User Control | High; you interact directly with open-source code. | Low; you operate within the company's terms of service. |

| Ease of Use | Requires familiarity with crypto wallets and gas fees. | Simple, often with mobile apps and customer support. |

| Security Risk | Smart contract bugs and protocol exploits. | Company insolvency, hacks, and mismanagement. |

Ultimately, choosing the right platform is just one part of the equation. Picking the right coin is just as critical. Be sure to check out our guide on the best stablecoins available today to help you make a well-rounded decision.

Real World Strategies For Borrowing Stablecoins

Knowing the theory behind stablecoin borrowing is one thing, but seeing it work in the real world is where it really clicks. The true power of this financial tool shines when it’s used for specific, goal-oriented strategies. This isn't just an abstract DeFi concept; it's a practical way for traders, entrepreneurs, and everyday investors to get things done without having to sell their core crypto holdings.

These strategies run the gamut from aggressive market plays to more conservative cash management, which just goes to show how flexible crypto-backed loans can be. Let's dig into some of the most common and powerful ways people are putting stablecoin borrowing to work.

Amplifying Market Exposure With Leverage

By far, one of the most popular reasons to borrow stablecoins is for leveraged trading. It’s a strategy for traders who have high conviction about an asset's direction and want to magnify their potential returns.

Picture a trader named Alex who holds $20,000 in Ethereum (ETH) and is convinced the price is about to take off. Instead of just HODLing, Alex decides to press the advantage. Here’s the play-by-play:

- Alex locks up the $20,000 of ETH as collateral on a DeFi lending protocol.

- Against that collateral, they borrow $10,000 in USDC.

- They immediately swap that $10,000 USDC for more ETH.

Just like that, Alex is now controlling $30,000 worth of ETH, despite only starting with $20,000. If ETH jumps 20%, their total position swells to $36,000. After paying back the $10,000 loan, they’re left with $26,000. That’s a $6,000 profit—a full 50% more than the $4,000 they would have made by just holding. Of course, the flip side is true, too; leverage cuts both ways and a sharp price drop could lead to liquidation.

Unlocking Liquidity For Cash Flow

Entrepreneurs and long-term investors often hit a wall: they need cash for a new opportunity or to cover expenses, but all their value is locked up in assets they believe in for the long haul. Selling is not an option. This is where stablecoin borrowing provides a perfect escape hatch.

Take Maria, a small business owner with a large Bitcoin position. She needs $50,000 for new equipment. Cashing out her BTC means a hefty capital gains tax bill and giving up future upside.

Instead, she collateralizes her Bitcoin and borrows $50,000 in a stablecoin. She can then convert that to cash to make her purchase. This gets her the capital she needs to grow her business, all while her Bitcoin position stays untouched. Later, she can repay the loan from business profits.

By separating asset ownership from liquidity, stablecoin borrowing allows you to spend the value of your crypto without giving up on its future growth potential. It’s a powerful tool for managing personal and business finances.

Capitalizing On Market Inefficiencies

For traders with a keen eye, stablecoin loans are the fuel for arbitrage strategies. Arbitrage is simply the act of profiting from tiny price differences for the same asset on different exchanges. These windows of opportunity close fast and you need serious capital to make the small margins worthwhile.

A trader might notice a token is trading at $1.00 on Exchange A but $1.02 on Exchange B. By borrowing a large sum—say, $500,000 in stablecoins—they can simultaneously buy on A and sell on B. They instantly capture that 2% spread for a $10,000 profit, then repay the loan moments later.

This same idea applies to complex yield farming, where borrowed capital can be put to work in high-yielding liquidity pools. If you're looking for more advanced plays, learning how to generate yield on stablecoins with RWA (Real-World Assets) can open up entirely new ways to deploy borrowed funds.

Funding Real-World Purchases

Finally, people are increasingly using their crypto wealth to fund major life events. We're seeing more and more individuals borrow stablecoins against their portfolio to make a down payment on a house, buy a car, or pay for university tuition.

This strategy lets them tap into the equity they've built up in their digital assets without selling. They don't have to worry about timing the market or messing up their long-term investment plan. It effectively transforms crypto from a purely speculative asset into a functional source of capital, bridging the gap between the digital economy and your everyday life.

Navigating The Key Risks Of Stablecoin Debt

While borrowing stablecoins can be a powerful tool for generating liquidity or adding leverage, it's certainly not a risk-free lunch. This isn't free money; it's debt. And like any debt, it demands respect and a clear-eyed understanding of what could go wrong.

The risks are real, but they aren't a mystery. We can boil the main threats down to three core areas: the ever-present danger of liquidation, hidden vulnerabilities in the code, and the uncomfortable truth that a "stablecoin" might not stay stable. Ignoring any one of these can turn a smart strategy into a painful lesson.

The Specter Of Liquidation

The most immediate and brutal threat every borrower faces is liquidation risk. Think of it as an automated margin call. It’s the process where a lending platform force-sells your collateral to pay back your loan because its value has dropped below a critical threshold. This isn't a negotiation—it's a cold, unforgiving mechanism designed to protect the protocol, not you.

Here’s a quick, real-world scenario to show how fast it can happen:

- The Setup: You post $10,000 worth of Ethereum (ETH) as collateral.

- The Loan: The platform allows a 60% Loan-to-Value (LTV) ratio, so you borrow $6,000 in USDC. Your LTV is now 60%.

- The Threshold: The protocol’s liquidation point is set at 80% LTV.

- The Crash: The market takes a nosedive, and your ETH collateral is suddenly worth just $7,500.

At this moment, your LTV has shot up to 80% ($6,000 loan / $7,500 collateral). The instant you hit that trigger, the smart contract springs into action, selling your ETH to recover the $6,000 loan, usually tacking on a painful liquidation penalty. You've just lost your ETH at the worst possible time—the bottom of the market.

Key Takeaway: Liquidation is the automated immune system of lending protocols. The only way to avoid it is to keep your position healthy by adding more collateral or paying down your loan before the market forces the protocol to do it for you.

Smart Contract And Platform Vulnerabilities

When you lock up funds in a DeFi protocol, you're placing immense trust in its code. Smart contract risk is the danger that a hidden bug or exploit in that code could be found by an attacker, allowing them to drain the platform's funds—including your collateral. This isn't just a theoretical worry; DeFi's history is littered with nine-figure hacks.

Even well-audited protocols aren't invincible. An exploit can lead to a total loss of your assets with almost no hope of recovery. It’s the fundamental trade-off we make for using these open, permissionless systems.

Centralized platforms (CeFi) aren't a safe haven, either. They come with their own set of counterparty risks, like company insolvency, simple mismanagement, or a classic security breach. For a deeper dive into the technical attack surfaces, our guide on stablecoin oracle manipulation vectors shows how the price feeds that trigger liquidations can themselves be targeted.

The Unstable Stablecoin Peg Risk

Finally, you have to contend with peg stability risk. Just because it has "stable" in the name doesn't mean its 1:1 peg to the dollar is a law of physics. If the stablecoin you borrowed—say, USDC—slips to $0.90, you still owe the original loan amount, but the cash you're holding is suddenly worth 10% less.

It can also go the other way. If a stablecoin strengthens to $1.05, repaying your debt becomes 5% more expensive. The integrity of that peg is the bedrock of the entire crypto-lending market.

This isn't a niche concern anymore. The stablecoin market is enormous and its health impacts the broader financial system. With a total supply projected to cross $300 billion by late 2025, stablecoins are a major force. They now hold over $150 billion in U.S. Treasuries, making the sector a top-20 holder of U.S. government debt. This deep integration means a major de-pegging event would have far-reaching consequences for everyone.

Time to Put Theory into Practice

We've covered a lot of ground—from the mechanics of collateralized loans to the various platforms and the risks involved. You can see how borrowing stablecoins isn't just some niche crypto trading trick; it's a powerful way to unlock the value of your digital assets without having to sell them. Think of it as a practical tool for managing cash flow, jumping on an investment opportunity, or even funding real-world goals.

The path forward requires a bit of planning, but the payoff can be well worth it. Before you do anything, the single most important thing is to have a clear, well-defined strategy. Why are you borrowing? Are you looking to add some leverage to a trade, or do you need cash for a new business idea? Your answer will shape every decision you make, especially how you monitor your collateral and prepare for a platform's liquidation rules.

Your First Steps

The trick is to start small. You don't need to dive into a complicated leveraged position on day one. Instead, think about taking out a small, manageable loan just to get a feel for how the whole process works from beginning to end. It's the best way to build confidence.

Here’s a simple checklist to get you started:

- Know Your "Why": What's the money for? Leverage? Liquidity? Something else entirely? A clear goal is the foundation of a good strategy.

- Pick Your Playground: Are you more comfortable with the self-custody and transparency of DeFi, or do you prefer the simpler, more guided experience of CeFi? Your answer depends on your risk appetite and how hands-on you want to be.

- Do the Math on Risk: Never, ever borrow the maximum amount you're offered. Always leave a healthy buffer in your Loan-to-Value (LTV) ratio. This cushion is your best defense against a volatile market and the dreaded liquidation event.

- Watch Your Position Like a Hawk: Set up alerts. Track your collateral’s value daily. Have a plan ready to either add more collateral or start paying down the loan if the market turns against you.

Stablecoin borrowing is a powerful tool, but it's one that demands respect. Treat it with the same seriousness you would any other major financial decision—be thoughtful, be strategic, and always, always keep an eye on your risk.

The crypto world is always changing, and stablecoin borrowing is set to be a huge part of its future. By taking a measured approach and staying curious, you can make this instrument work for you safely and effectively. Your first move isn't to take a massive loan; it's to take a small, informed one.

Got Questions About Stablecoin Borrowing? We've Got Answers.

Diving into stablecoin borrowing can feel a bit like learning a new language. You're bound to have questions. Here are some straightforward answers to the things people most often ask.

How Much Can I Actually Borrow?

The short answer? It depends on what you put up as collateral and the platform's rules. The magic number here is the Loan-to-Value (LTV) ratio. Think of LTV as the percentage of your collateral's value a lender is willing to give you as a loan.

For top-tier assets like Bitcoin or Ethereum, you’ll typically see LTVs between 50% and 75%.

Let's make that real. Say you have $10,000 worth of ETH and you use a platform with a 60% LTV. In that scenario, you could borrow up to $6,000 in stablecoins. Simple as that.

But there are some practical limits to keep in mind:

- On DeFi Protocols: You can technically borrow tiny amounts, but it's often not worth it. If you have to pay $15 in blockchain transaction fees (gas) just to take out a $50 loan, the math just doesn't add up.

- On CeFi Platforms: These guys are more like traditional lenders and usually have set minimums. To keep things running smoothly, you'll often see minimum loan amounts starting around $500.

Is Borrowing Stablecoins a Taxable Event?

This is where borrowing truly shines. In most places, including the U.S., simply taking out a loan is not a taxable event. This is a huge deal because selling your crypto to get cash would absolutely trigger a tax bill on any profits you've made.

By borrowing against your crypto, you get the cash you need without selling your assets and creating an immediate tax headache. It lets you hold onto your long-term investments while still handling short-term expenses.

Now, here's the fine print. The loan itself isn't taxed, but what you do with that money might be. If you use those borrowed stablecoins to buy other assets that then go up in value, you could owe capital gains taxes when you sell. Tax rules are a beast, so it’s always a good idea to chat with a tax professional who understands crypto.

What Happens If The Platform I Use Gets Hacked?

This is a critical question, and the risk is very real. What happens next depends entirely on whether you used a decentralized (DeFi) or centralized (CeFi) platform. The difference is night and day.

If a DeFi protocol gets hacked, it can be devastating. A smart contract exploit can drain funds in an instant, and because there's no central company in charge, that loss could be permanent. Your collateral could simply be gone. Some protocols are creating insurance funds to help soften the blow, but there are no guarantees.

With a CeFi provider, you're dealing with a company, so the process is more traditional. Your protection depends on their insurance, their terms of service, and the laws where they operate. A top-tier CeFi platform will almost certainly have insurance on the assets it holds, but the coverage details matter. This is why doing your homework and picking established, regulated platforms is so important if you go the centralized route.

At Stablecoin Insider, we provide the latest news and in-depth analysis to help you make informed decisions in the digital asset space. Explore our insights at https://stablecoininsider.com to stay ahead.

{kind=link}