Table of Contents

New York, March 27, 2026.

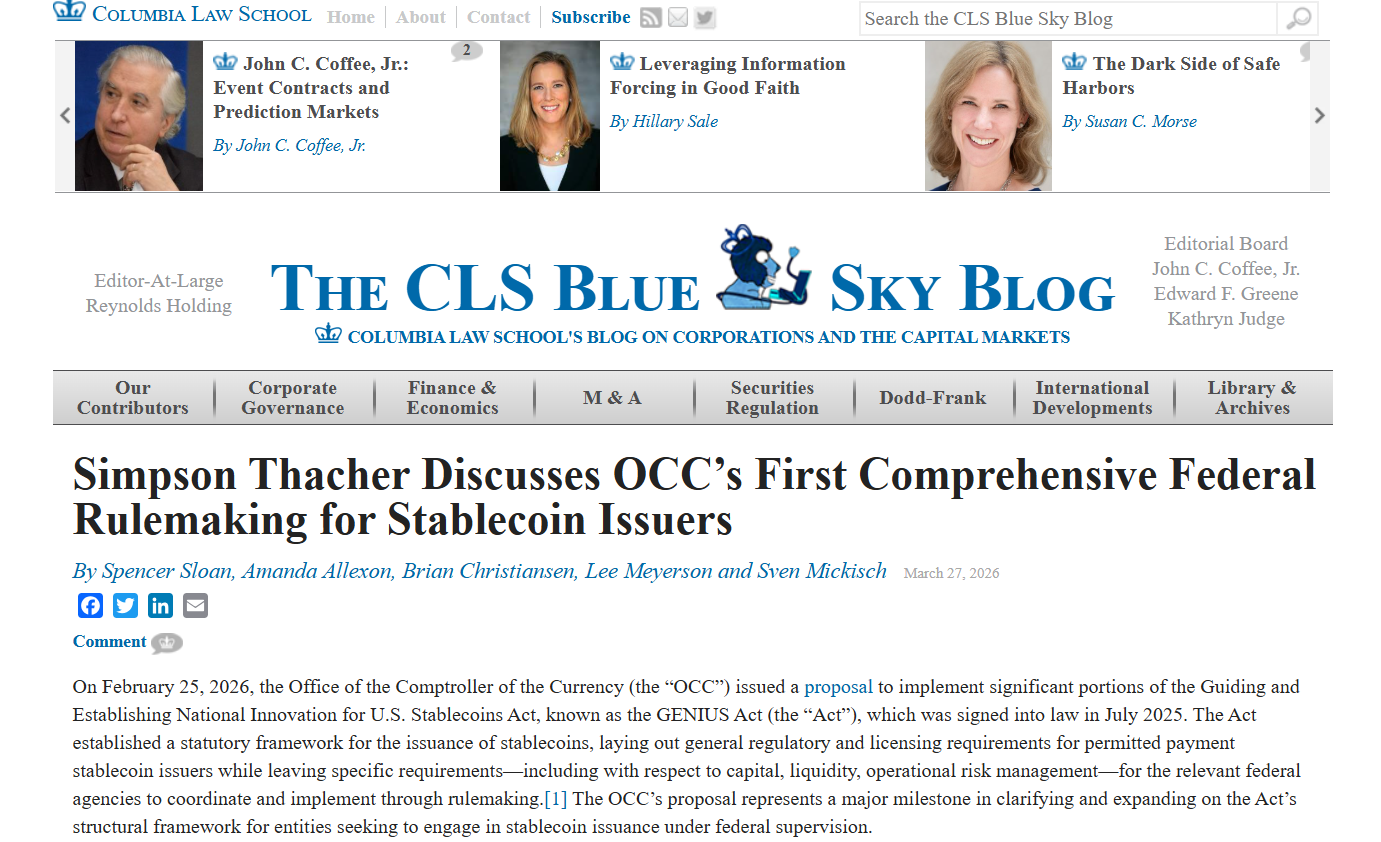

Columbia Law School’s CLS Blue Sky Blog today published a detailed post discussing Simpson Thacher & Bartlett LLP’s client memorandum on the Office of the Comptroller of the Currency’s (OCC) proposed rulemaking implementing the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act).

The OCC issued its landmark proposal on February 25, 2026, creating the first comprehensive federal framework for permitted payment stablecoin issuers (PPSIs). Simpson Thacher’s original analysis, released February 27, 2026, is now receiving fresh industry attention through the CLS Blue Sky feature.

The GENIUS Act, signed into law in July 2025, established a national licensing and oversight regime that prohibits non-permitted issuers from issuing payment stablecoins.

The OCC’s Proposed Rule fills in critical details on capital, liquidity, reserves, and operations for entities under its jurisdiction, including national bank subsidiaries, federal qualified issuers, and certain large state-qualified issuers.

Key Takeaways

- CLS Blue Sky Blog today highlights Simpson Thacher’s February 27 memorandum as the leading legal breakdown of the OCC’s GENIUS Act proposal.

- The rules impose strict 1:1 reserves using only low-risk assets, ban yield payments on stablecoins, and set tailored capital standards.

- Oversight applies to national banks, federal qualified PPSIs, and large state issuers required to transition to federal supervision.

- A 60-day public comment period remains open, with the OCC seeking input on more than 200 specific questions.

Insights from Simpson Thacher’s Legal Memorandum

1. Reserve and Liquidity Framework

Simpson Thacher emphasizes the OCC’s 1:1 reserve requirement, mandating that every stablecoin be backed by eligible high-quality assets at fair market value. Permitted assets include U.S. currency, Federal Reserve balances, short-term Treasuries (93 days or less), qualifying repos, and select money-market funds. Crypto assets are excluded.

The proposal offers two diversification approaches, principles-based with a safe harbor or mandatory quantitative limits, along with liquidity thresholds (10% daily, 30% weekly).

Excess reserves may be withdrawn monthly following independent accountant certification.

2. Prohibition on Yield and Anti-Evasion Rules

The memo notes the OCC’s clear ban on paying interest or yield solely for holding stablecoins, backed by a strong anti-evasion presumption targeting affiliate and white-label arrangements.

Merchants can still offer discounts, and non-affiliated profit-sharing is allowed, but affiliates are defined broadly under Bank Holding Company Act standards.

3. Permitted Activities, Marketing, and Operations

Issuers may issue and redeem stablecoins, manage reserves, provide custody services, and conduct directly supporting activities (e.g., ledger testing or gas fees). Fees for purchase or redemption are permitted.

Marketing with “USD” is allowed, but names implying government or FDIC backing are prohibited.

4. Capital, Supervision, and Transition Provisions

No fixed capital ratios apply; minimums are risk-based with a $5 million floor for new issuers. Only common equity tier 1 and additional tier 1 capital count. An operational backstop requires highly liquid assets covering 6–12 months of expenses.

Large state issuers over $10 billion in circulation must transition to OCC oversight or stop new issuances.

Applications include detailed plans, leadership reviews, and a 120-day decision timeline; change-in-control notices trigger at 10%+ voting ownership.

Conclusion

Today’s CLS Blue Sky Blog post brings renewed focus to Simpson Thacher’s authoritative analysis, underscoring the OCC’s balanced approach that delivers regulatory clarity while leaving room for innovation.

With the public comment period closing in mid-April 2026, banks, fintech firms, and potential stablecoin issuers are encouraged to review both the original memorandum and today’s blog discussion.

Early engagement with regulators and counsel will be essential to shape the final rules and ensure seamless compliance in this evolving federal framework.

Read Next:

- Coinbase Rejects Latest CLARITY Act Draft

- USDC Officially Launches in Japan via SBI VC Trade

- Tether's First Full Independent Audit of USDT Reserves

FAQs:

1. What prompted today’s CLS Blue Sky Blog coverage?

The blog published a post on March 27, 2026, summarizing and discussing Simpson Thacher’s February 27 client memo on the OCC’s GENIUS Act proposal.

2. What are the core reserve rules?

PPSIs must back stablecoins 1:1 with eligible low-risk assets (cash, short-term Treasuries, etc.) at fair market value; crypto is not allowed, and diversification plus liquidity requirements apply.

3. Does the proposal allow interest payments on stablecoins?

No. The OCC explicitly prohibits yield paid solely for holding the coins and includes anti-evasion safeguards.

4. Who is subject to the OCC’s oversight?

National bank subsidiaries, federal qualified PPSIs, and large state issuers exceeding $10 billion that must transition to federal supervision.

5. When is the deadline for public comments?

Comments on the OCC proposal are due within 60 days of Federal Register publication, approximately mid-April 2026.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}