Table of Contents

Accra, December 23, 2025

Ghana's parliament has passed the Virtual Asset Service Providers (VASP) Bill, 2025, formally legalizing cryptocurrency trading and establishing a comprehensive regulatory structure for digital assets.

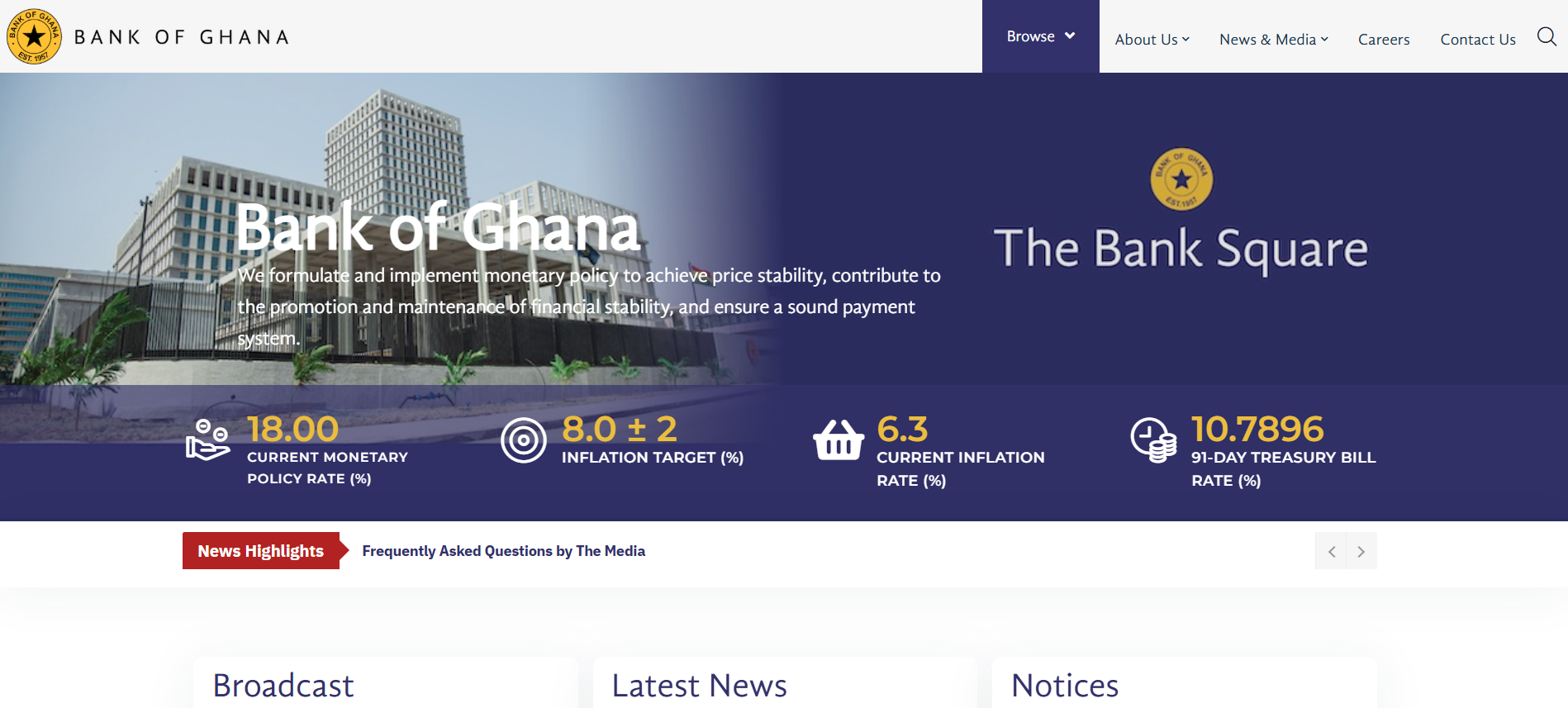

The Bank of Ghana (BoG) will oversee licensing and supervision of virtual asset service providers, including exchanges, wallet operators, and custody services.

BoG Governor Dr. Johnson Pandit Asiama confirmed the development, stating the law brings digital asset activities "within clear, accountable, and well-governed boundaries."

Individual traders face no legal risks for cryptocurrency transactions, but service providers must comply with licensing requirements, anti-money laundering (AML) protocols, and Financial Action Task Force (FATF) standards, including the Travel Rule for transaction data sharing.

Key Takeaways

- Ghana's VASP Bill, 2025 legalizes crypto trading for individuals without arrest risks.

- BoG mandates licensing and AML compliance for all virtual asset service providers.

- Existing operators must register and comply starting phased rollout in 2026.

- 2026 focus includes exploring gold-backed stablecoins for cross-border settlements.

- Market saw $3B in crypto volume (2023-2024) with 3M users (17% adult population).

Background and Market Context

Prior to the VASP Bill, cryptocurrency activity in Ghana operated in a regulatory gray area despite rapid growth. Central bank estimates indicate approximately 3 million Ghanaians, about 17% of the adult population, engaged in digital asset transactions.

From July 2023 to June 2024, the market processed roughly $3 billion in cryptocurrency volume, according to data from Web3 Africa Group and Chainalysis reports.

Adoption has been driven by remittances, inflation hedging, and financial inclusion for unbanked populations. Ghana ranks among the top five Sub-Saharan African countries for on-chain cryptocurrency value received in recent periods.

The unregulated environment previously exposed users to fraud risks and complicated enforcement of financial crimes.

The new law addresses these concerns while aligning with lessons from the 2022 global cryptocurrency downturn and Ghana's domestic financial challenges, including cedi volatility and high interest rates.

Key Provisions of the VASP Bill

The legislation empowers the BoG as primary regulator, with collaboration from the Securities and Exchange Commission (SEC) for certain activities.

Core requirements include:

- Mandatory licensing for all virtual asset service providers.

- Implementation of customer due diligence, suspicious transaction reporting to the Financial Intelligence Centre, and AML/counter-terrorist financing measures.

- Compliance with international standards to facilitate cross-border cooperation.

- Phased rollout of supervisory rules starting in 2026, requiring existing operators to register and meet standards.

Cryptocurrencies remain non-legal tender, the Ghanaian cedi retains exclusive status, and the framework does not provide compensation guarantees for platform failures. Users retain exposure to market and operational risks.

Plans for Asset-Backed Digital Instruments

In 2026, the BoG intends to prioritize blockchain applications in payments, trade finance, foreign exchange settlement, and market infrastructure to support cross-border commerce.

Governor Asiama highlighted "targeted exploration" of asset-backed digital settlement instruments, explicitly including gold-backed stablecoins.

Ghana, Africa's largest gold producer, has existing initiatives like the domestic gold purchase program (accumulating over 65 tons since 2021) and blockchain efforts for gold tracking to curb illegal exports.

These foundations position the country to integrate gold reserves into digital assets for enhanced stability and transparency.

Regional Comparison

Ghana's approach mirrors trends across Africa. Nigeria operates under SEC oversight, South Africa has licensed multiple platforms via its Financial Sector Conduct Authority, and Kenya recently passed a similar VASP bill awaiting presidential approval.

Sub-Saharan Africa recorded over $205 billion in on-chain value in recent periods, reflecting 52% year-over-year growth.

Implications for Stakeholders

The framework aims to reduce fraud, attract institutional investors and compliant international exchanges, generate tax revenue, and support youth-led fintech in payments and remittances. It also enhances monetary policy visibility amid import-dependent economic pressures.

Implementation will occur in phases, with detailed guidelines expected in early 2026.

Conclusion

Ghana's VASP Bill establishes regulated cryptocurrency access while prioritizing risk management and innovation.

Coupled with 2026 gold-backed stablecoin exploration, it positions the nation as a structured digital asset hub in Africa, balancing adoption growth with financial stability.

Read Next:

- 2025 Stablecoin Year-End Report

- Best Chain for Stablecoin Micropayments in 2026

- Best Stablecoin On/Off-Ramps for 2026 Compared

FAQs:

1. What does the new law change for individual crypto traders in Ghana?

Individual trading is now fully legal; no arrests for legitimate cryptocurrency transactions.

2. Do crypto companies need approval to operate?

Yes, all virtual asset service providers (exchanges, wallets, custody) require BoG or SEC licenses and must meet AML, reporting, and FATF standards.

3. Is cryptocurrency legal tender in Ghana?

No, the Ghanaian cedi remains the only legal tender.

4. When will regulations fully take effect?

Licensing and supervision roll out in phases during 2026; existing providers must comply to continue operations.

5. What are plans for gold-backed stablecoins?

BoG will target exploration in 2026 as part of asset-backed digital instruments for payments and trade finance.

6. Does the law protect users from losses?

No, users bear market, volatility, and platform risks; regulation focuses on oversight, not compensation.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}