Table of Contents

USDT (Tether) remains the largest stablecoin by circulation, with a market cap around $186B as of late January 2026.

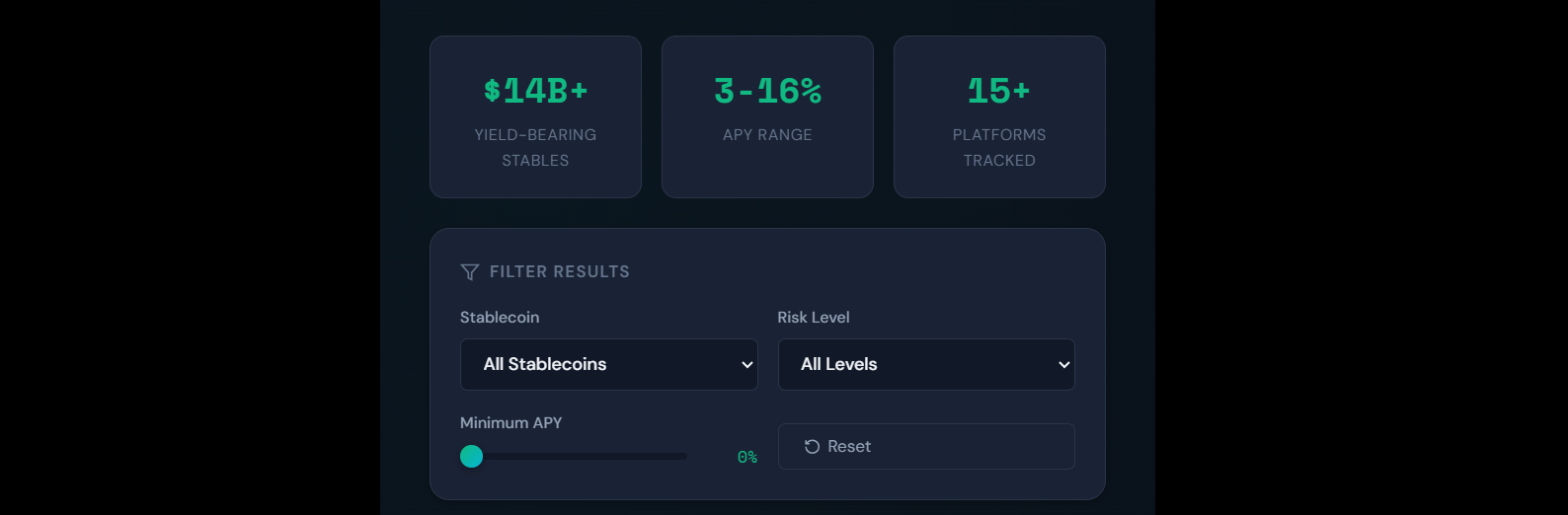

As traditional savings rates remain uneven globally, many crypto users continue to pursue USDT yield through lending, liquidity provision, and structured earn products, typically ranging from low single digits in lower-risk venues to double digits where risk is materially higher.

Key Takeaways

- Aave provides non-custodial USDT lending with variable rates and on-chain transparency.

- Ledn markets tiered USDT yields up to 8.5% APY, with KYC and jurisdiction limitations.

- EarnPark markets USDT yields up to ~30% APY, implying materially higher strategy and platform risk.

- Higher APY usually means higher risk (smart contract risk, counterparty risk, liquidity risk, and operational risk).

- Diversification and withdrawal planning matter more than headline APY.

Earning Returns on USDT: The 3 Core Methods

1) Lending

You supply USDT to a lending market or lender.

Borrowers pay interest, and suppliers receive a portion of that interest.

2) Staking (as marketed for stablecoins)

Stablecoins do not usually secure a network like proof-of-stake assets do. In practice, staking USDT typically means depositing USDT into a yield product where returns come from lending, liquidity provision, market-making, or internal treasury strategies.

3) Liquidity Provision (LP)

You add USDT (often paired with another asset) to a DEX pool and earn a share of trading fees and/or incentives. LP returns can be attractive, but depend on pool volume, incentive schedules, and strategy execution.

CeFi vs. DeFi control model:

- DeFi: You interact with smart contracts and keep wallet control, but you assume smart contract and on-chain execution risk.

- CeFi: The platform custody model is simpler operationally, but introduces counterparty, operational, and regulatory risk.

Key Elements to Evaluate When Selecting a USDT Yield Platform

1) Security Model and Incident History

Review audits, exploit history, custody controls (if custodial), and how withdrawals behave under stress.

2) Yield Source Clarity

Understand where returns come from: borrow demand, trading fees, incentives, strategy PnL, or internal re-hypothecation. Transparent yield sources typically produce more predictable outcomes.

3) Liquidity and Withdrawals

Confirm whether your USDT is fully liquid, subject to lockups, or exposed to withdrawal gates and processing delays.

4) Track Record and Transparency

Assess operational maturity, disclosures, and user trust. For DeFi, on-chain transparency helps, but it does not eliminate smart contract risk.

5) Net Yield After Fees

Focus on your net yield after performance fees, withdrawal fees, and on-chain costs.

Top Platforms for Earning Yield With USDT in 2026

1) Aave: DeFi Benchmark for USDT Lending

Aave is one of the most widely used non-custodial money markets in DeFi. It is commonly used for USDT lending because it offers deep liquidity, transparent on-chain rates, and a mature risk framework relative to smaller protocols.

Platform Overview:

- Type: DeFi (non-custodial)

- Access: Wallet-based (you control your assets through your wallet)

- Deployment: Available across multiple networks and markets (depending on the Aave version and the specific market)

Current USDT Yield Context (2026)

USDT lending rates on Aave are variable and move with utilization (borrow demand versus supplied liquidity). In normal conditions, USDT supply rates often cluster in the low-to-mid single digits, but can rise during periods of higher leverage demand.

How to Get Started:

- Open the Aave application in your browser.

- Connect your wallet (for example, via a common wallet connection method).

- Select the market/network you want to use.

- Supply USDT.

- Monitor the live supply APY and utilization, and manage your position.

Risk Factors:

- Smart contract risk: Even mature protocols can have vulnerabilities.

- Rate volatility: Supply APY can drop quickly when utilization falls.

- Network costs: Transaction fees vary by network and can affect small deposits.

- Liquidity under stress: In extreme market conditions, exits can become slower or more expensive.

Pros:

- Non-custodial and transparent

- Mature DeFi brand with significant liquidity

- Rates update dynamically based on market conditions

- No KYC required

Cons:

- Yields can be lower than aggressive yield products

- Requires comfort with wallets and network selection

- Fees can reduce net yield (especially on higher-cost networks)

2. Ledn: Compliant Yield Generation With Defined Tiers

Ledn markets a more traditional, account-based earning experience for USDT. It positions itself toward users who prefer clearer rate tiers and a custodial interface rather than direct DeFi interaction.

Platform Overview:

- Type: CeFi (custodial)

- User model: Account-based deposits and interest accrual

- Core tradeoff: Reduced operational complexity versus increased counterparty dependence

USDT Earning Options

Ledn typically markets tiered APY structures for USDT, including higher tiers for larger balances. This approach is designed to provide predictable expectations compared to variable DeFi money markets.

Account Setup Process:

- Create an account on Ledn.

- Complete identity verification (KYC).

- Deposit or transfer USDT into your Ledn account.

- Select the relevant earning product (if multiple options exist).

- Track interest accrual through the platform interface.

Security Measures (What to Evaluate):

Because Ledn is custodial, your main diligence areas include:

- Custody structure and counterparties

- Segregation language for client assets

- Transparency of risk management and lending partners

- Behavior during market stress (withdrawal timing and communication)

Advantages:

- Defined yield tiers and a straightforward user experience

- KYC and compliance structure that may suit certain investors

- Lower operational burden than DeFi (no wallet management for earning)

Limitations:

- Custodial counterparty risk

- Jurisdiction restrictions and KYC requirements

- Less on-chain transparency versus DeFi markets

- Yield sustainability depends on the platform’s lending relationships and risk controls

3. EarnPark: Higher-APY Positioning With Strategy Complexity

EarnPark positions itself as a hybrid yield platform and markets higher USDT yields than plain lending. Higher advertised APY generally implies a more complex strategy stack, which increases both diligence requirements and tail risk.

Platform Introduction

EarnPark markets USDT yields that can reach double digits and may approach ~30% in promotional ranges depending on product conditions. "Up to" yields are not guarantees and typically vary based on strategy performance and market conditions.

Yield Mechanisms (Common Structure for This Category):

Platforms in this category often generate returns through combinations of:

- Liquidity provision and fee capture

- Automated allocation across DeFi venues

- Trading or market-making style strategies

- Compounding logic at a defined cadence

The critical diligence point is not just the advertised yield, but the underlying strategy, where funds are routed, and whether risk controls are clearly disclosed.

Getting Started Guide:

- Register for an EarnPark account.

- Complete any required verification steps.

- Choose the specific USDT product/strategy tier offered.

- Deposit USDT.

- Monitor realized returns and compare them with advertised target ranges.

Risk Assessment:

- Platform and operational risk: Custody, governance, and business continuity matter.

- Strategy risk: Returns can compress quickly or underperform in adverse markets.

- DeFi exposure risk: If strategies route on-chain, you inherit smart contract and liquidity risks.

- Transparency risk: If disclosures are limited, it becomes harder to validate sustainability.

Benefits:

- Higher potential headline yields than plain lending

- Strategy variety and automation (depending on product design)

- Often designed to be more hands-off than pure DeFi farming

Drawbacks:

- Higher risk stack compared to simple lending

- “Up to” APY is not a guarantee

- Requires deeper diligence on strategy, custody, and counterparties

- Less proven than mature DeFi markets in many cases

Comparative Analysis

| Feature | Aave | Ledn | EarnPark |

|---|---|---|---|

| Platform type | DeFi (non-custodial) | CeFi (custodial) | Hybrid positioning |

| USDT yield style | Variable market rate | Tiered advertised APY | “Up to” APY via strategies |

| Typical positioning | Transparent DeFi lending | Defined tiers + simplicity | Higher-APY strategy products |

| KYC required | No | Yes | Often yes / depends on product |

| Best for | DeFi users prioritizing self-custody | Users seeking defined tiers and simplicity | Users pursuing higher potential yields with higher risk tolerance |

Risk Management Strategies

1. Diversification Across Platforms

Avoid concentrating all USDT with a single provider. Split allocation across 2–3 venues with different risk profiles (for example, one DeFi money market and one custodial product), depending on your comfort level.

2. Understanding Smart Contract Risks

If you use DeFi, assume smart contract risk is always present. Review audits, prefer battle-tested protocols, and size positions so a worst-case outcome is survivable.

3. Monitoring Platform Health

Track signals that often change before problems become obvious:

- Utilization spikes and rate changes (DeFi lending markets)

- Withdrawal delays or new restrictions (custodial platforms)

- Shifts in terms, counterparties, or disclosures

- Community sentiment and incident reports

4. Setting Realistic Expectations

Headline APY is not a guarantee. Treat high yields as compensation for risk. Decide in advance what downside you can tolerate.

5. Emergency Planning

- Keep a portion of USDT liquid and outside yield products.

- Know your withdrawal steps and timeframes before you need them.

- Keep backup venues available in case one platform becomes congested or restricts withdrawals.

Tax Implications and Reporting

Tax Treatment

- Yield earned from interest or rewards is commonly treated as taxable income in many jurisdictions.

- The tax treatment and reporting requirements vary by country and personal situation.

Platform Documentation

- Custodial platforms may provide statements or export tools.

- DeFi often requires you to self-track wallet transactions and income events.

Record Keeping

Maintain records of:

- Deposits and withdrawals

- Rewards received and the timestamp/value when received

- Fees paid and on-chain transaction hashes

Consider crypto tax software for transaction-heavy DeFi activity.

Professional Advice

If your activity is large, frequent, or cross-border, consult a tax professional familiar with digital assets.

Conclusion

In 2026, USDT yield still spans a clear risk spectrum:

- Aave is a strong default for users who want self-custody, transparent variable rates, and mature DeFi infrastructure.

- Ledn targets users who want a simpler experience with defined tier structures, while accepting custodial counterparty risk and KYC.

- EarnPark markets higher potential yields through more complex strategies, which generally increases platform, strategy, and transparency risk.

If you want sustainable results, optimize for risk management first: diversify allocations, maintain liquidity buffers, and avoid treating “up to” APY as a base case.

Read Next:

- Complete Guide to Smart Contract Managed Lending in 2026

- Best Options for Yield-Bearing Stablecoin Accounts in 2026

- How to Earn Stablecoin Yield with Coinbase Prime as an Institution in 2026

FAQs:

1. Is earning yield on USDT safe in 2026?

No approach is risk-free. The main risks are smart contract failures (DeFi), counterparty and custody risk (CeFi), liquidity constraints, and the possibility of USDT de-pegging. Choose platforms with clear disclosures and avoid concentrating funds.

2. What is the difference between APR and APY?

APR is the annual rate without compounding assumptions. APY reflects compounding effects, meaning it assumes reinvestment of yield at a given frequency.

3. Can I lose USDT while earning yield?

Yes. Loss scenarios include protocol exploits, platform insolvency, operational failure, or forced unwind events. The higher the advertised yield, the more you should assume additional risk layers exist.

4. How often are rewards paid out?

It depends on the platform. DeFi lending typically accrues continuously, while custodial products often credit periodically (daily, weekly, or monthly) based on product terms.

5. Do USDT lending rates rise during volatile markets?

They can. Volatility often increases borrow demand and utilization, which can raise lending rates. However, this is not guaranteed and can reverse quickly depending on market conditions.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}