Table of Contents

In February 2024, Ethena Labs launched USDe with a promise that felt like either a breakthrough or a provocation, depending on who was listening: a dollar-pegged stablecoin that earns yield, holds no bank reserves, and backs itself entirely through crypto derivatives.

Two years on, USDe has not just survived, it has become the third-largest stablecoin in existence, surpassed $14 billion in market cap at its 2025 peak, and embedded itself so deeply into decentralized finance infrastructure that entire DeFi yield ecosystems have been reorganized around it.

This Q1 2026 report examines where USDe stands today: its current market position, the mechanics underpinning its stability and yield, the institutional moves that have defined the past two quarters, the stress tests it has survived, and the product roadmap unfolding in real time.

Key Takeaways

- Market Position: USDe holds a circulating supply of approximately $5.92 billion as of mid-March 2026.

- Yield Model: In 2025, variable yields ranged from 4%–15%, with funding rates averaging ~11% annualized in bull conditions and ~5% in 2025 overall.

- DeFi Dominance: Ethena-related assets on Aave reached $8.5 billion by September 2025.

- Stress Tests: USDe briefly depegged to $0.97 during the October 10, 2025 flash crash but recovered within hours.

- Regulatory Headwinds: Ethena exited the EU/EEA after BaFin barred USDe under MiCA.

Ethena's USDe Market Position

Starting 2025 with a market cap below $6 billion, USDe surged to over $14 billion, capturing nearly 5% of the total stablecoin market, significant because, as a synthetic dollar, it does not rely on US Treasury or dollar backings.

As of March 16, 2026, circulating supply sits at approximately $5.92 billion following a sharp contraction from the Q4 2025 deleveraging event.

The stablecoin market itself reached record scale in 2025. Total stablecoin market cap reached a new high of $251.7 billion in mid-2025, with USDT surpassing $150 billion and USDC at approximately $70–75 billion. The top five stablecoins control roughly 90% of total market cap.

Ethena reached a supply of $6 billion USDe in just 10 months, the fastest dollar-based asset to hit $5 billion supply behind only USDT and USDC, and exceeded $1.2 billion in annual revenue in December 2024, making it the protocol with the highest revenue per employee. USDe is used as collateral in approximately 60% of centralized exchanges.

The October 2025 market event was the defining test. USDe's market cap had surged 75% in the prior month to $9.3 billion with a weekly increase of 24%, making it among the fastest-growing financial instruments in the stablecoin sector before the correction. Today, with a $5.92B market cap, USDe remains the only stablecoin outside the fiat-backed category to hold a top-three position.

USDe's Delta-Neutral Mechanism

Understanding USDe's position in the market requires understanding why it is structurally unlike any other top stablecoin. It holds no bank deposits, no US Treasuries in its own name, and carries no fiat reserves. Its dollar peg is maintained entirely through derivatives.

Ethena users mint USDe by depositing LST, ETH, Bitcoin, and USDC. Through its delta-neutral strategy, where short BTC and ETH futures positions balance changes in the value of the underlying collateral, USDe maintains a 1:1 backing ratio.

According to Ethena, compared to stablecoins requiring over-collateralization of often over 200%, USDe is "the most capital-efficient synthetic dollar in the industry."

The mechanics work as follows: when a user deposits $100 of ETH, Ethena simultaneously opens a short position of equivalent notional value in perpetual futures markets. If ETH drops 50%, the collateral is worth $50, but the short position gains $50, keeping the total backing stable at $100.

The protocol opens a corresponding short perpetual position for the approximate same notional dollar value on a derivatives exchange. The backing assets are transferred directly to an off-exchange settlement solution and remain on-chain, custodied by off-exchange service providers to minimize counterparty risk.

Ethena delegates, but never transfers custody of, backing assets to derivatives exchanges to margin the short perpetual hedging positions.

Yield comes from two primary sources:

- Funding rates paid by long traders on perpetual exchanges

- Staking rewards on ETH collateral

Aggregated futures funding rates for BTC and ETH have been positive during bull markets, averaging about 11% annualized in 2024 and approximately 5% in 2025. Sustained high rates reflect an environment where the market is paying to be long, allowing Ethena to capture that spread through its delta-neutral strategy. (Source: Substack)

The third yield source, introduced specifically to stabilize returns during funding-rate downturns, is interest on liquid stablecoins, including USDC interest from Coinbase and returns from short-term US Treasury exposure via BlackRock's BUIDL fund.

Ethena employs an adaptive model that adjusts the collateral mix between short ETH/BTC perpetual positions and yield-bearing stablecoins depending on market conditions.

- During periods of elevated funding rates, Ethena maintains a higher reliance on delta-neutral strategies.

- During periods where funding rates yield less than US Treasuries, typically during market downturns, Ethena allocates a higher proportion of USDe backing to liquid stablecoins.

USDe's Yield Performance

The yield story is what separates USDe from every other stablecoin at scale. This is not a passive reserve product.

Every USDe can be staked into sUSDe to receive protocol earnings.

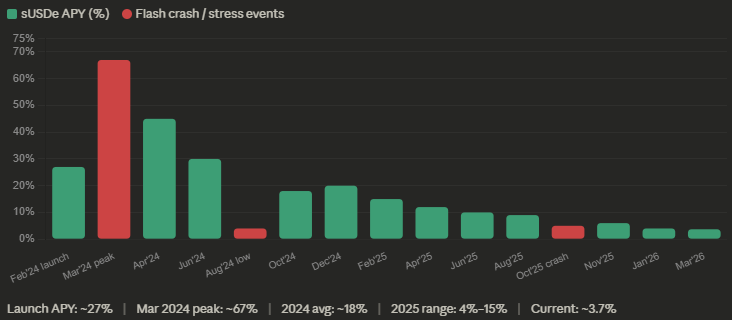

At launch, USDe's APY started around 27%, then spiked past 60% in early 2024 as the first wave of capital entered the protocol. Once liquidity built up and markets stabilized, yields leveled out near 19% APY.

The yield structure in 2025 moderated as USDe supply scaled and funding rates normalized. In 2025, sUSDe variable yields ranged from approximately 4–15%. As of early 2026, current yields are approximately 3.72% according to Messari data, a compression that reflects both the broader market contraction following the October 2025 event and reduced leveraged demand for long exposure in perpetual markets.

Importantly, the yield distribution mechanism is designed to prevent gaming: Ethena calculates the protocol's earnings daily and sets a dollar-denominated APY weekly. Payouts to sUSDe holders are made in small payments over 8-hour intervals throughout the following week.

This weekly cycle is designed to smooth out volatility and prevent anyone from gaming the system by timing entry and exit around large payouts.

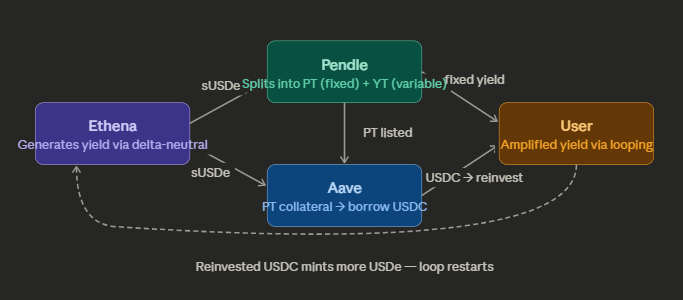

The DeFi Flywheel: Ethena, Pendle, and Aave

No report on USDe in 2025–2026 is complete without examining the DeFi leverage loop that made USDe a systemic fixture of on-chain finance. Three protocols became so intertwined that analysts coined the term "Aavethena" to describe the relationship.

Ethena generates yield, Pendle packages it, and Aave leverages it. This structure accounts for the majority of Ethena's deposits on Aave and most of Pendle's total value locked, making it one of the most influential yield engines on-chain.

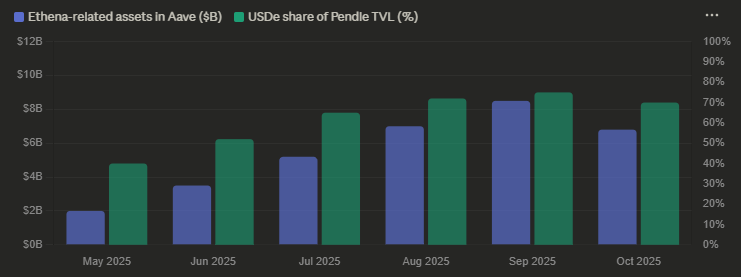

The numbers backing this structure were staggering by mid-2025. Between May and August 2025, the total value locked in Pendle skyrocketed from $3 billion to $10 billion. As of September 2025, USDe and its derivatives accounted for roughly 75% of all funds locked in Pendle, with Pendle holding about 60% of the total USDe supply. (Incrypted)

Aave's role was equally pivotal. Following a vote in April 2025 to add a new type of collateral, Aave introduced PT tokens for eUSDe and later sUSDe. Within weeks, the volume of collateralized positions with a May 2025 maturity grew from $164 million to $500 million. The next batch in July peaked at $1.5 billion, and the September batch reached $2.3 billion. As of March 16, total Ethena-related assets on Aave are estimated at $6.8 billion, of which $4.2 billion are PT.

By September 2025, Aave held $8.5 billion in Ethena assets, with a significant portion tied to rehypothecated Pendle principal tokens.

At its peak, Aave held over 50% of Ethena's stablecoin supply across USDe, sUSDe, and sUSDe Pendle PTs.

When Aave later added sUSDe Pendle PTs, users could leverage loop fixed yield as well. Aave became the largest market using Pendle PTs as collateral in DeFi.

The flywheel also created systemic risk exposure. Over $4.2 billion of sUSDe was locked in Pendle principal tokens and looped via Aave, enabling leveraged yields. This strategy accounted for approximately 60% of USDe's $11.3 billion supply.

BlackRock, Institutional Backing, and Funding

Ethena's institutional credibility has been constructed through a deliberate sequence of capital partnerships and product decisions that would have been inconceivable for a DeFi protocol just 18 months prior.

Funding History:

- February 2024: $14 million strategic round at a $300 million valuation, co-led by Dragonfly Capital and Arthur Hayes' family office Maelstrom

- December 2024: $100 million raise completed with Franklin Templeton and Fidelity Investments-affiliated F-Prime Capital among the backers

- August 2025: $20 million from M2 Capital for the Converge platform

- MEXC Ventures invested $16 million in Ethena and purchased $20 million in USDe

The BlackRock partnership is one of the most significant in the stablecoin sector:

- In October 2024, Ethena allocated $46 million of its reserve fund into BlackRock's BUIDL tokenized money market fund, Superstate's USTB, Mountain's USDM, and Sky's USDS.

- In December 2024, it went further: Ethena launched USDtb, a stablecoin holding over 90% of its reserves in BlackRock's BUIDL tokenized money market fund, which invests in US government debt, cash, and repos.

USDtb is designed to reduce risk for USDe during negative funding rate environments.

BlackRock's BUIDL fund crossed $1 billion in assets on the back of a $200 million allocation from Ethena. Ethena's USDtb token reached a $540 million supply at that point.

Q4 2025 Stress Tests

2025 produced two major stress events that tested whether USDe's design could hold under real-world extreme pressure. Both events are now part of the permanent record on delta-neutral stablecoin architecture.

1. The Bybit Hack - February 2025

In February 2025, Bybit suffered a $1.4 billion security breach. Since Ethena uses Bybit as one of its primary perpetual exchange venues for delta hedging, the exposure question was immediate.

Ethena Labs confirmed that USDe remained fully collateralized, with exposure to Bybit limited to less than $30 million. The company maintains its crypto assets in off-exchange custody to protect against such security breaches.

The collateral architecture, specifically the off-exchange settlement model where Ethena delegates but never transfers custody of assets to derivative exchanges, directly contained the damage.

The incident highlighted exchange and custody risk: while Ethena's collateral held in off-exchange custody remained secure, the event showed the importance of venue diversification and reducing single points of failure across trading and custody infrastructure.

2. The October 10, 2025 Flash Crash

The October event was sharper and more contested. USDe briefly depegged to $0.97 during a $19 billion fallout event on October 11, 2025, though it recovered within hours. Its delta-neutral hedging relies on CEX perpetuals, exposing it to extreme volatility.

The political fallout was significant. OKX CEO Star Xu publicly stated that the October 10 crash, where Bitcoin fell 16.5%, was caused by Binance's temporary user-acquisition campaign. He claimed the campaign offered up to 12% APY on USDe, allowed it as collateral with insufficient limits, and created a dangerous leverage loop that unraveled when USDe depegged.

Industry leaders including CZ, Haseeb Qureshi, and Evgeny Gaevoy disputed the claim, citing macro factors.

The crash triggered a significant supply contraction. USDe supply fell from its $14B+ peak to approximately $8.5B within weeks of the event, and has continued declining into Q1 2026.

Despite the October shock, the post-event resilience data is notable: despite a 50% contraction in USDe's total value in November 2025 due to market volatility, sUSDe liquidity on decentralized exchanges hit an all-time high of $248 million.

Q1 2026 Developments

The institutional moves in Q1 2026 represent Ethena's most consequential pivot: from a DeFi-native yield product into a regulated financial infrastructure layer.

1. Kraken Custody Partnership (January 6, 2026)

Under the partnership, the underlying assets for USDe will be warehoused in isolated, cold-storage vaults on a one-for-one basis. This makes the setup bankruptcy remote, such that the underlying assets are shielded from the balance sheet risk of the custodian.

Beginning in January 2026, Kraken Custody participates in Ethena's ongoing transparency processes, including monthly custodian attestations and weekly Proof of Reserves reporting, supporting enhanced visibility into the backing of USDe.

This is a direct institutional signal. Weekly on-chain Proof of Reserves from a US state-chartered bank is the kind of compliance architecture that opens Ethena to asset managers and regulated institutional capital that would otherwise be prohibited from touching a synthetic stablecoin.

2. Spark Liquidity Layer Integration (January 2026)

Ethena Labs announced that the direct allocation of USDe and sUSDe has been approved and will be integrated into the Spark Liquidity Layer, with a total allocation of up to $1.1 billion in the short term.

Incorporating Ethena into the Spark Liquidity Layer will allow Spark to directly receive Ethena rewards without going through lending.

3. Exchange Listings (January–February 2026)

In late January 2026, both HTX and KuCoin announced listings of Ethena's USDe and ENA tokens. HTX listed the USDe/USDT spot trading pair on January 30, 2026, while KuCoin added the ENA trading pair on January 26.

4. HyENA Launch Performance (December 2025 – January 2026)

HyENA, a decentralized perpetuals exchange built on Hyperliquid, launched on December 9, 2025, enabling traders to use USDe as collateral and the quote asset. HyENA quickly gained traction, recording over $440 million in volume across 6,500 users by early January 2026.

5. Bybit Mantle Vault (February 2026)

Bybit's Mantle Vault, which utilizes Ethena staking (sUSDe), saw its Assets Under Management increase by 50% in January 2026, surpassing $150 million. This growth is attributed to the product's consistent stablecoin on-chain yield, which uses market-neutral strategies to minimize volatility exposure for investors.

6. Aave DAO Onboards May 2026 PT Tokens (February 2026)

The Aave DAO approved Proposal 442 to onboard May 2026 expiry PT tokens for USDe and sUSDe to the Aave V3 Core instance, supporting them as collateral assets.

7. Governance: DAO Restructuring (February 2026)

The Ethena DAO approved a proposal to reduce the Ethena Risk Committee from five to three voting members to improve accountability and clarify ownership.

The Product Roadmap: Beyond The Synthetic Dollar

According to founder Guy Young, Ethena accounted for approximately 85% of on-chain USD asset growth in 2024, excluding USDT and USDC.

The protocol is now executing a deliberate expansion into three adjacent verticals:

- Traditional finance

- Consumer payments

- On-chain derivatives infrastructure

1. iUSDe: Exporting Yield to TradFi

In 2026, Ethena introduced iUSDe, an institutional-grade version with compliance wrappers, custody integrations, and reporting standards, designed to onboard mid-sized hedge funds, family offices, and crypto-native asset managers.

iUSDe is intended to facilitate adoption by traditional financial institutions, including asset managers, ETFs, prime brokers, private credit funds, and investment trusts. It employs a wrapper mechanism that can program transfer restrictions so that it can be held and used by traditional financial entities subject to regulatory oversight.

Ethena is preparing to expand its presence into traditional finance markets valued at over $190 trillion. iUSDe will be presented to asset managers, private credit funds, and other entities in traditional financial markets, offering a product with higher returns compared to traditional fixed-income options.

2. Two New Business Lines (Q1 2026)

Ethena announced the launch of two new business lines in Q1 2026. Co-founder Guy Young stated both initiatives "have the potential to be the size of USDe." The specific products have not yet been publicly named as of this writing.

3. Telegram Payments App

Ethena is building a Telegram app that leverages the TON blockchain and Apple Pay, enabling direct mobile tap payments for Telegram's estimated one billion users.

4. Converge Blockchain

In collaboration with Securitize, Ethena is building Converge, a blockchain network targeting institutional settlement of real-world assets, with ENA as the staking token for the Converge Validator Network.

5. ENA Buyback Program (DAT)

Ethena's DAT initiative announced two rounds of ENA buybacks in 2025: $360 million in July and $530 million in September, totaling $890 million in committed capital. By systematically removing ENA from circulation, DAT creates demand and confidence for the token.

USDe's Regulatory Landscape

1. EU / MiCA - Market Exited:

German regulator BaFin barred USDe under MiCA, citing unregistered securities concerns. Ethena exited the EU/EEA market entirely.

MiCA compliance would require 1:1 reserve backing that USDe's synthetic structure cannot satisfy.

2. United States - GENIUS Act Risk:

The GENIUS Act requires 1:1 fiat backing for stablecoins, which sUSDe lacks. Passage in mid-2025 barred yield-bearing regulated stablecoins, paradoxically shifting capital flows toward USDe as a crypto-native alternative. However, direct enforcement risk on synthetic structures remains unresolved.

3. Asia / Offshore - Growth Markets:

Regulatory exits from EU have redirected growth focus to Asia and offshore markets.

Expansion onto Sui, integrations with TON/Telegram, and listings on HTX and KuCoin signal a deliberate pivot toward markets with more permissive synthetic asset frameworks.

4. iUSDe - The Compliance Workaround:

iUSDe's wrapper architecture, adding transfer restrictions, custody integrations, and reporting layers to sUSDe, is Ethena's direct response to TradFi regulatory requirements. It positions the yield-bearing product as a fixed-income alternative rather than a stablecoin, potentially avoiding the stablecoin classification entirely.

The GENIUS Act in the US requires 1:1 fiat backing for stablecoins, which sUSDe lacks. Ethena exited the EU market after MiCA compliance challenges, reducing regional adoption but focusing growth in less-regulated markets.

The GENIUS Act created a paradox that Ethena benefited from directly. USDe supply doubled to $10 billion monthly after the GENIUS Act banned yield-bearing regulated stablecoins, shifting capital to crypto-native alternatives.

By removing the ability of regulated issuers to offer yield, US legislators inadvertently directed institutional DeFi demand toward Ethena's product.

Risk Factors

1. Funding Rate Compression

The core risk for USDe remains what it has always been: prolonged negative funding rates.

If perpetual futures traders go net short, as they did during the FTX collapse of November 2022 (when the effective return on the strategy was -0.6%), the protocol's reserve fund must absorb yield deficits.

Ethena has an insurance fund to mitigate negative yields and support the price of USDe during liquidity challenges by extending the cooldown period for unstaking.

2. Leverage Loop Systemic Risk

Chaos Labs warned that a 20% drop in crypto prices could trigger $1.2 billion in liquidations on Aave, given the $4.2 billion of sUSDe locked in leveraged Pendle-Aave loop strategies. The October 2025 event demonstrated this was not theoretical.

3. Exchange Counterparty Concentration

USDe's hedging operations are distributed across multiple centralized exchanges but remain exposed to any single venue's failure or manipulation. The Bybit hack validated the off-exchange custody model, but the October crash debate, in which Binance's pricing feed changes for USDe were cited as a trigger, highlights a structural dependency on exchange behavior.

4. Overcollateralization as a feature, not a floor

The protocol's 24/7 mint/redeem function is critical during stress but is untested in prolonged crises. A sustained multi-week period of negative funding rates during a bear market, without sufficient reserve fund coverage, remains the primary tail risk scenario.

5. Regulatory Overhang

Regulatory clarity could limit sUSDe's reach in major markets, capping growth. A US enforcement action would directly threaten its market position.

Lawsuits and arbitrations began mounting against Binance in February 2026 related to the October crash, adding legal uncertainty to the ecosystem.

Ethena's USDe Key Metrics

Conclusion

Ethena's USDe enters Q1 2026 contracted but structurally intact. The supply decline from $14 billion to $5.92 billion reflects the leverage unwind that followed October 2025, a direct consequence of how deeply the Aave-Pendle loop had become the primary demand driver for USDe. That dependency is now the protocol's most documented risk.

What the past six months have also confirmed: USDe survived a $1.4 billion exchange hack with under $30 million in exposure, depegged briefly to $0.97 during the largest single-day liquidation event of 2025, and recovered within hours. The off-exchange custody model and delta-neutral architecture held under conditions designed to break them.

The Q1 2026 institutional moves (Kraken Custody with weekly Proof of Reserves, Spark Liquidity Layer integration, Franklin Templeton and F-Prime Capital backing, and iUSDe targeting regulated TradFi capital), indicate a protocol actively converting DeFi credibility into institutional infrastructure. That transition is in progress, not complete.

The central risk heading into the rest of 2026 remains unchanged: sustained negative funding rates combined with a leveraged DeFi unwind, against a reserve fund sized at 1.18% of TVL. The mechanism is sound. The margin for error is not wide.

Read Next:

FAQs:

1. What is Ethena USDe?

Ethena USDe is a synthetic dollar stablecoin built on Ethereum. It maintains a 1:1 peg to the US dollar not through fiat reserves, but through a delta-neutral derivatives strategy: for every unit of crypto collateral held long, Ethena opens an equal and opposite short position in perpetual futures markets.

2. What is the difference between USDe and sUSDe?

USDe is the stablecoin itself. sUSDe (staked USDe) is what users receive when they stake USDe in the Ethena protocol. sUSDe is a yield-bearing token that accrues the protocol's earnings, primarily from perpetual futures funding rates and ETH staking rewards. Users stake USDe, receive sUSDe, and the sUSDe appreciates in value against USDe over time as yield accumulates.

3. How does Ethena USDe generate yield?

Three sources: (1) Funding rates from short perpetual futures positions, when more traders go long than short, longs pay shorts a periodic fee, which Ethena captures. (2) ETH staking rewards from liquid staked ETH held as collateral. (3) Interest on liquid stablecoins and tokenized Treasury products (including BlackRock's BUIDL), which backstop the system during low-funding-rate periods. sUSDe averaged approximately 18% APY in 2024 and has ranged from 4%–15% in 2025.

4. What is the current USDe market cap?

As of March 16, 2026, USDe's circulating supply is approximately $5.92 billion, making it the third-largest stablecoin by market cap, behind USDT and USDC. Its 2025 peak was over $14 billion.

5. Why did Ethena exit the EU?

German regulator BaFin barred USDe under the EU's MiCA framework, citing unregistered securities concerns. MiCA requires 1:1 fiat backing for stablecoins, which USDe's synthetic structure cannot satisfy. Ethena (through its German subsidiary Ethena GmbH) settled with BaFin and ceased EU operations.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}