Table of Contents

The convergence of traditional banking and blockchain technology is no longer a future concept; it's a present-day reality. While many associate stablecoins with crypto-native firms, a growing number of regulated financial institutions are strategically entering the market. This shift marks a critical evolution in finance, driven by the demand for 24/7 settlement, enhanced payment efficiency, and emerging regulatory frameworks like MiCA in Europe. These pioneering institutions are actively building the infrastructure for a new financial system.

This comprehensive roundup explores the key banks with stablecoins, detailing the specific players shaping this landscape. We move beyond theory to provide actionable insights into the regulated entities issuing, custodying, or building foundational technology for stablecoins and tokenized deposits. The embrace of stablecoins by traditional banks signifies a pivotal shift, where advanced technologies are becoming indispensable. To understand the broader impact of innovation, you can explore the transformative benefits of AI in finance.

Our goal is to help you identify the best partners and platforms for your specific needs, whether you are an investor, developer, or financial professional. For each bank and regulated entity profiled, you will find a detailed analysis of their:

- Stablecoin Products: A look at the specific stablecoins or tokenized deposits they offer or support.

- Operational Status: Current regulatory standing and operational capabilities.

- Key Use Cases: Real-world applications in payments, settlement, and custody.

- Strategic Partnerships: Collaborations driving their digital asset initiatives.

Each entry includes screenshots and direct links, providing a clear and direct path to engaging with these financial innovators. We will examine institutions like Custodia Bank, J.P. Morgan, and Société Générale, offering a definitive guide to the new financial frontier where banking meets blockchain.

1. Custodia Bank – Avit

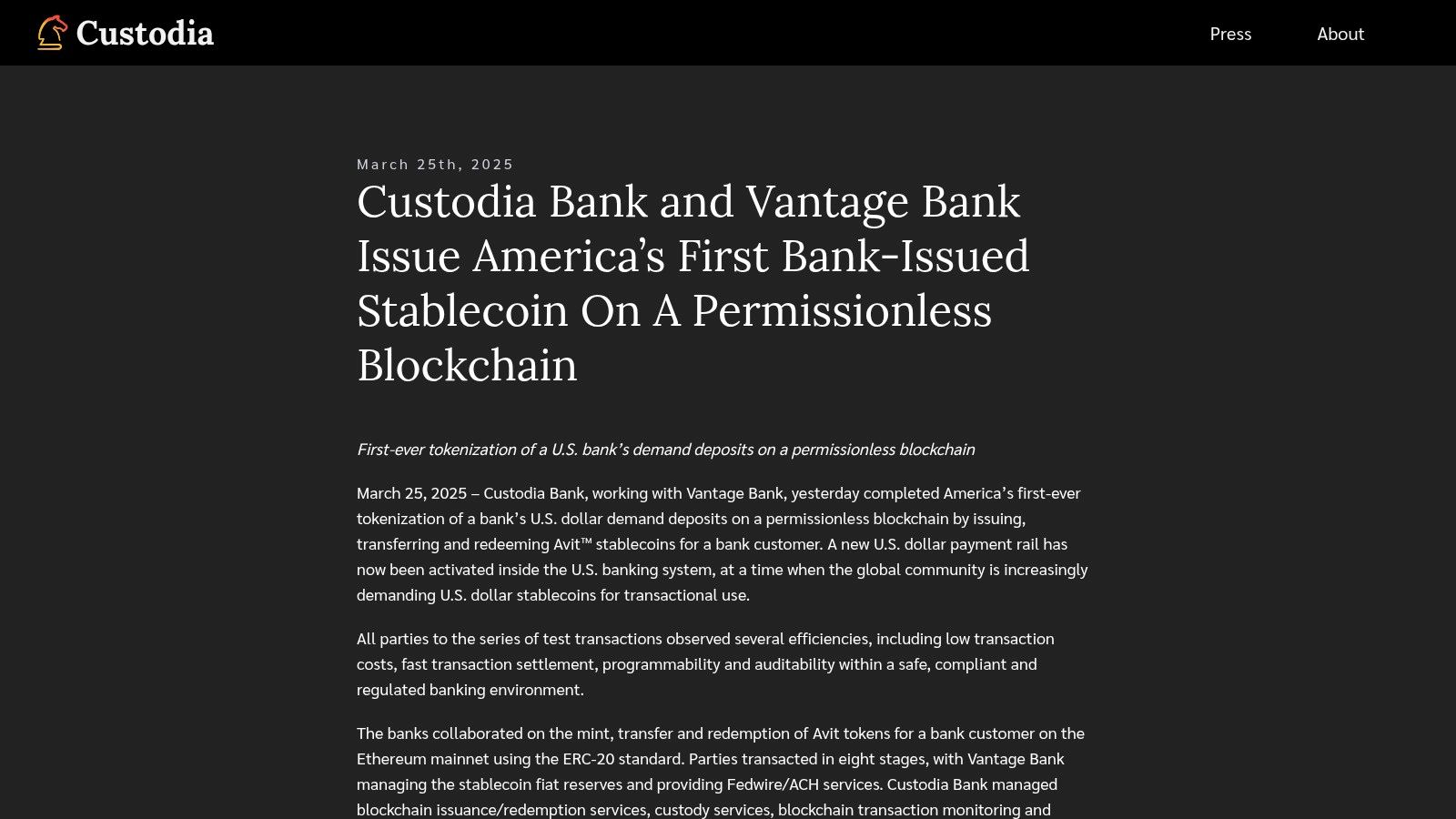

Custodia Bank, a Wyoming-chartered Special Purpose Depository Institution (SPDI), has positioned itself at the forefront of digital asset banking by conducting a regulated pilot for its bank-issued token, Avit. This initiative represents a significant step forward for banks with stablecoins, demonstrating how traditional financial institutions can bridge the gap to public blockchain infrastructure. Avit is not just a stablecoin; it is a tokenized representation of a U.S. dollar demand deposit held at the bank, issued as an ERC-20 token on the public Ethereum blockchain.

The bank’s website provides a transparent overview of the pilot program, detailing the complete lifecycle of Avit from minting to redemption. This clarity is crucial for institutional clients and developers seeking to understand the operational and compliance frameworks of a true bank-backed digital dollar. Custodia’s approach emphasizes regulatory adherence at every step, integrating Bank Secrecy Act (BSA), Anti-Money Laundering (AML), and Office of Foreign Assets Control (OFAC) checks directly into the token’s functionality.

Key Features and Operational Flow

Custodia Bank’s pilot stands out for its public, yet regulated, nature. Unlike many private blockchain experiments, this test was conducted on Ethereum, allowing for public auditability while maintaining strict access controls for participants.

- Token Standard: Avit is an ERC-20 token, ensuring compatibility with the vast Ethereum ecosystem of wallets, smart contracts, and decentralized applications.

- Regulated Mint & Redeem: Only fully onboarded and verified institutional clients can mint or redeem Avit tokens. The process requires a direct banking relationship with Custodia.

- On-Chain Transparency: All transactions are recorded on the Ethereum blockchain, providing a public, immutable ledger of token movements.

- Documented Pilot: Custodia published a detailed eight-stage flow of its live test, covering account setup, minting Avit against USD deposits, on-chain transfers between whitelisted addresses, and final redemption back to USD.

Access and Practical Implementation

Avit is exclusively available to institutional and business clients who establish a banking relationship with Custodia. It is not a retail product. The primary use cases are institutional settlement, business-to-business payments, and programmable money applications where the legal status and backing of a regulated bank deposit are paramount. This model aligns with the growing trend of specialized financial products, where the bank provides what can be described as Ecosystem-Specific Stablecoins (ESS) and Money-as-a-Service (MaaS). Developers and institutions interested in this framework can use the bank’s website to request contact and learn more about the technical and legal requirements for participation.

Website: custodiabank.com/press/custodia-issues-Stablecoin/

2. Vantage Bank – Avit collaboration hub

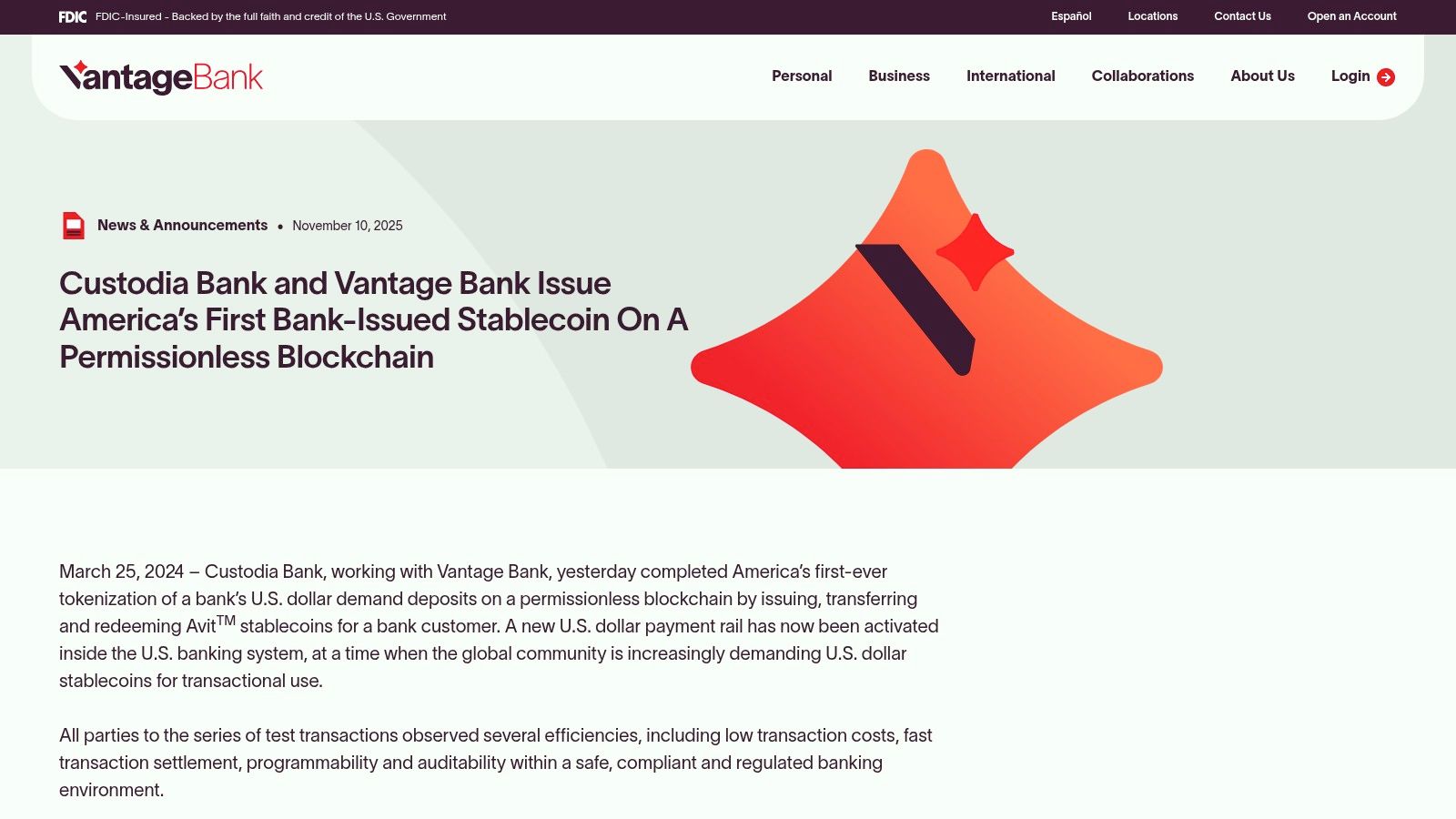

Vantage Bank, a Texas-chartered community bank, provides a crucial look into the operational backbone supporting bank-issued tokens through its Avit collaboration hub. While Custodia Bank spearheads the issuance of Avit, Vantage Bank’s involvement highlights the practical requirements for managing fiat reserves and integrating with traditional payment systems. This partnership serves as a powerful case study for how community and regional banks can participate in the emerging digital asset ecosystem, making it a key resource for institutions evaluating banks with stablecoins.

The bank's resource page details its specific role in the Avit pilot, clarifying the division of responsibilities. Vantage manages the U.S. dollar deposits that back the Avit tokens and handles the settlement of funds through traditional payment rails like Fedwire and ACH. This behind-the-scenes perspective is invaluable for businesses, developers, and other financial institutions seeking to understand the complete operational lifecycle of a compliant, bank-backed stablecoin.

Key Features and Operational Flow

Vantage Bank’s contribution demonstrates how a consortium model can effectively distribute the complex duties of stablecoin management between specialized financial institutions. This approach allows banks to leverage their core competencies while collaborating on innovation.

- Bank-Managed Fiat Reserves: Vantage Bank holds and manages the 1:1 U.S. dollar reserves backing every Avit token, ensuring asset safety and regulatory compliance.

- Traditional Payment Rail Integration: The bank is responsible for processing USD inflows and outflows for minting and redemption via established systems like Fedwire and ACH.

- Compliance-Aligned Documentation: The collaboration outlines a clear, compliance-first operational framework, providing a blueprint for other banks interested in similar partnerships.

- Consortium Model: The partnership between Vantage and Custodia signals a pathway for other banks and credit unions to join and create a network for interoperable, bank-issued digital currency.

Access and Practical Implementation

The information provided by Vantage Bank is primarily educational and informational, targeted at other financial institutions, fintech partners, and institutional clients. It is not a direct-to-consumer platform for minting or redeeming Avit. The key takeaway is the demonstration of a workable model for integrating public blockchain technology with traditional banking infrastructure. This collaborative approach makes the concept of bank-issued stablecoins more accessible and less daunting for community and regional banks that may lack the resources to build a full-stack solution independently. Institutions can explore this model to understand the practical steps for reserve management and payment settlement in a digital asset context.

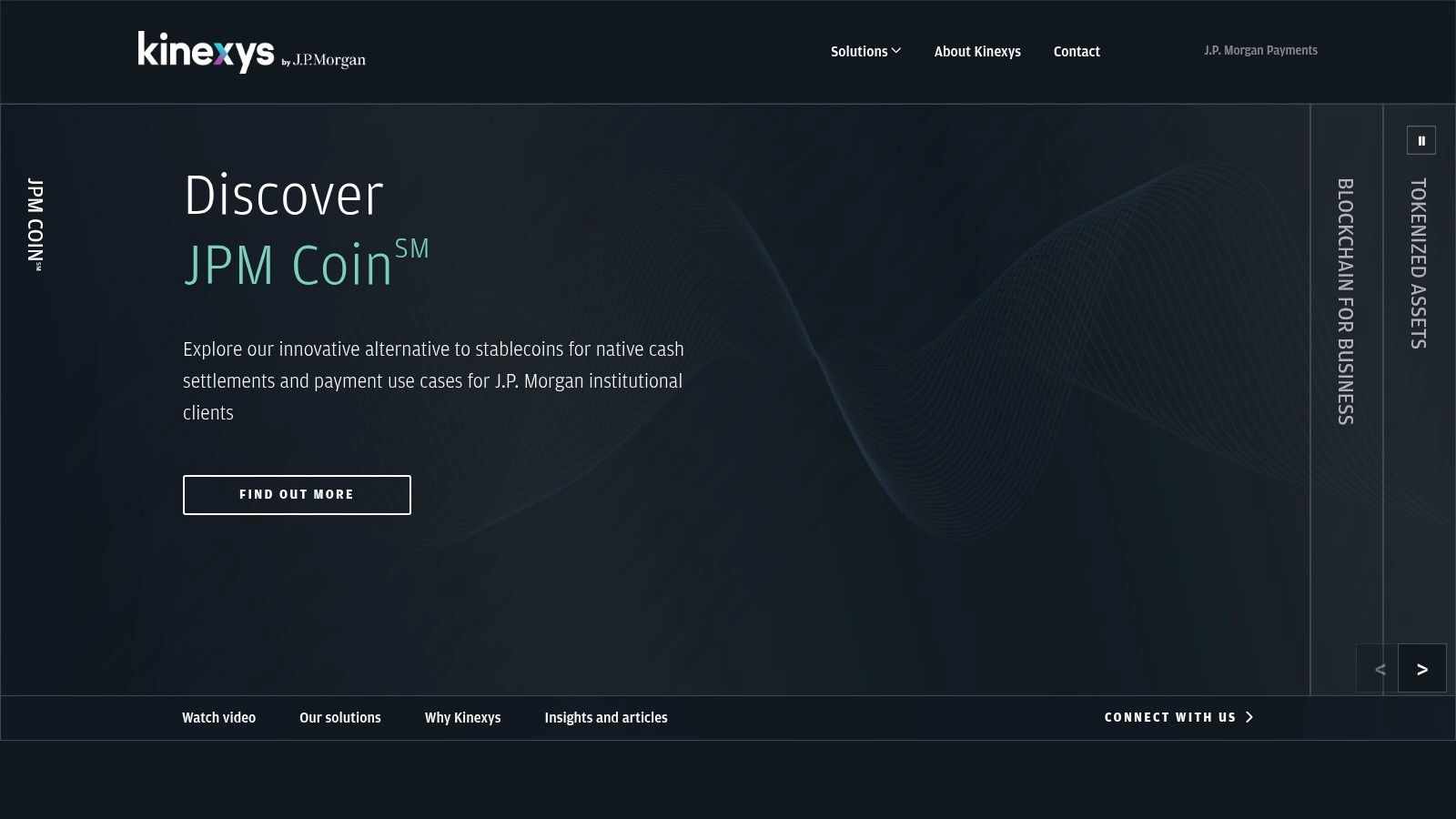

3. J.P. Morgan – Kinexys (formerly Onyx) / JPM Coin

J.P. Morgan, a global financial powerhouse, has established a significant presence in the digital asset space with its Kinexys platform, formerly known as Onyx. At the core of this initiative is JPM Coin, a permissioned, blockchain-based system that facilitates real-time value transfer for institutional clients. Rather than being a public stablecoin, JPM Coin represents tokenized U.S. dollar deposits held at the bank, enabling 24/7 payment and settlement on a private distributed ledger.

The bank's website for Kinexys serves as an enterprise portal, detailing the infrastructure's capabilities for multinational corporations and financial institutions. It positions JPM Coin not as a competitor to retail stablecoins but as a regulated, enterprise-grade alternative for institutional cash management, intraday repo, and complex multi-party settlements. The platform emphasizes security, scalability, and integration with J.P. Morgan's existing banking services, showcasing a mature, production-ready solution that has already processed billions of dollars in transactions.

Key Features and Operational Flow

JPM Coin operates on a private, permissioned blockchain network, ensuring that only onboarded and verified J.P. Morgan institutional clients can participate. This closed-loop system is designed for high performance and regulatory compliance, offering a stark contrast to the open nature of public stablecoins.

- Institutional Focus: The system is exclusively for J.P. Morgan’s institutional and corporate clients to transfer tokenized deposits between their accounts within the bank's network.

- 24/7 Settlement: JPM Coin overcomes traditional banking hour limitations, allowing for near-instantaneous, round-the-clock clearing and settlement of payments.

- Programmable Payments: The underlying blockchain infrastructure allows for programmable money functionalities, enabling automated and conditional payments for sophisticated treasury operations.

- Proven Production Use: Unlike pilot programs, JPM Coin is a fully operational system that has handled significant transaction volumes, demonstrating its reliability at an enterprise scale.

Access and Practical Implementation

Access to JPM Coin is restricted to institutional clients who have an established banking relationship with J.P. Morgan. The Kinexys website provides a gateway for these clients to learn about the solution and engage with the bank's consulting teams to design and implement tailored use cases. The primary applications are in corporate treasury, where it can be used to optimize liquidity, and in securities settlement, where it enables atomic delivery-versus-payment transactions. This approach firmly places it among the most significant bank-issued stablecoins detailed in our 2025 complete list, though its private nature makes it distinct. Pricing and specific onboarding requirements are not publicly listed and are part of the enterprise engagement process.

Website: https://www.jpmorgan.com/onyx/index.htm

4. Société Générale – SG‑FORGE (CoinVertible: EURCV and USDCV)

Société Générale, a major global banking group, enters the digital asset space through its fully integrated subsidiary, SG-FORGE. This entity has launched CoinVertible, a range of institution-grade stablecoins, including the Euro-denominated EURCV and the US Dollar-denominated USDCV. These are not merely stablecoins; they are regulated electronic money tokens (EMTs) under Europe's comprehensive Markets in Crypto-Assets (MiCA) framework, representing a significant commitment from a traditional bank to public blockchain infrastructure.

The SG-FORGE website offers a detailed look into the CoinVertible ecosystem, emphasizing transparency, regulatory compliance, and institutional-grade security. The platform clearly articulates the backing mechanism, with each token fully collateralized by high-quality liquid assets held in segregated, bankruptcy-remote accounts. This structure is designed to provide institutional investors with confidence in the token's stability and redeemability, positioning SG-FORGE as a key player among banks with stablecoins.

Key Features and Operational Flow

CoinVertible is designed to bridge the gap between traditional finance and decentralized ecosystems by offering a regulated, transparent, and multi-chain digital currency. Its operational model is built around security and compliance.

- Regulated Status: Issued as an Electronic Money Token (EMT) under the MiCA regulation, providing a high degree of investor protection and legal clarity within the European Union.

- Transparent Collateral: SG-FORGE provides daily disclosure of the collateral composition, ensuring complete transparency for token holders. The assets are held in a bankruptcy-remote structure to protect them from the issuer's credit risk.

- Multi-Chain Issuance: EURCV is available on Ethereum, Solana, and the XRPL, while USDCV is available on additional chains. This multi-chain strategy enhances interoperability and utility across different blockchain ecosystems.

- Institutional Onboarding: The primary issuance and redemption mechanism is through a direct, robust Know Your Customer (KYC) and Anti-Money Laundering (AML) onboarding process designed for institutional clients.

Access and Practical Implementation

While direct minting and redemption are reserved for onboarded institutional clients, SG-FORGE has pursued a hybrid access model. The EURCV stablecoin is listed on select public exchanges like Bitstamp, allowing broader access for eligible users, though the website notes that there are selling restrictions for U.S. persons. This dual approach caters to both large-scale institutional settlement needs and the liquidity requirements of the wider digital asset market. For developers and institutions, the platform serves as a primary resource for understanding the technical specifications, compliance requirements, and potential use cases, including on-chain trading, collateralization, and corporate treasury management.

Website: https://www.sgforge.com/product/coinvertible/

5. PayPal – PayPal USD (PYUSD)

While not a traditional bank, payments giant PayPal has made a landmark entry into the stablecoin space with its PayPal USD (PYUSD), marking one of the most significant mainstream adoptions of digital currency. PYUSD is designed to bridge the gap between fiat and digital economies for millions of U.S. consumers. It is a U.S. dollar-denominated stablecoin issued by Paxos Trust Company, a regulated financial institution, ensuring it is fully backed by U.S. dollar deposits, short-term U.S. Treasuries, and similar cash equivalents.

The integration of PYUSD directly within the PayPal and Venmo ecosystems provides an exceptionally simple on-ramp for users already familiar with these platforms. PayPal’s website clearly outlines how eligible U.S. customers can buy, sell, hold, and transfer PYUSD. This initiative brings the functionality of stablecoins to everyday financial activities, from peer-to-peer payments to online checkouts, positioning PYUSD as a key player in the evolution of digital payments.

Key Features and Operational Flow

PayPal’s approach prioritizes user experience and accessibility, leveraging its existing infrastructure to lower the barrier to entry for digital currency usage. The collaboration with Paxos provides the regulatory foundation, while PayPal delivers the user-facing application.

- Regulated Issuance: PYUSD is issued by Paxos Trust Company, a New York Department of Financial Services (NYDFS) regulated entity, and is redeemable 1:1 for U.S. dollars.

- Multi-Chain Support: The stablecoin is available as an ERC-20 token on Ethereum and as an SPL token on Solana, offering users flexibility and access to different blockchain ecosystems.

- Seamless Integration: Users can manage PYUSD directly within their PayPal or Venmo wallets, send it to other users on the platform (typically without fees), or transfer it to external compatible cryptocurrency wallets.

- Checkout Functionality: PYUSD can be selected as a funding source for online purchases at millions of merchants that accept PayPal, automatically converting it to fiat at checkout.

Access and Practical Implementation

PYUSD is available to eligible U.S. PayPal and Venmo customers, although availability may vary by state. The primary use case is simplifying digital transactions, including frictionless cross-border payments. Users can easily convert other supported cryptocurrencies to PYUSD within the app, often with a conversion fee. The native integration makes it an attractive option for those looking to use stablecoins to pay for goods and services overseas without leaving a familiar financial app. While PayPal handles the user experience, the underlying asset is managed with the transparency and regulatory oversight of Paxos, which publishes monthly reserve attestation reports.

Website: www.paypal.com/us/digital-wallet/manage-money/crypto/pyusd

6. Circle – USDC

While not a bank itself, Circle's platform for its USD Coin (USDC) is an essential part of the stablecoin ecosystem, providing institutional-grade infrastructure that often interfaces directly with the banking system. Circle's website serves as the primary resource for understanding the mechanics, reserves, and multi-chain architecture of USDC, one of the world's most trusted and widely adopted digital dollars. The platform clearly distinguishes its offerings for individuals, who typically acquire USDC on exchanges, and institutions, which can mint and redeem directly.

The website provides in-depth details about USDC's reserve composition, which is a critical factor for users evaluating its stability. By holding reserves in cash and cash equivalents custodied with traditional financial giants like BNY Mellon, Circle bridges the gap between digital assets and the established financial world. This transparent approach, supported by monthly attestations, is a key reason why USDC is a cornerstone asset for many businesses and developers in the digital economy.

Key Features and Operational Flow

Circle’s model is built on transparency and broad accessibility, making USDC a foundational element for DeFi, payments, and treasury management. It stands out by offering a robust, regulated pathway for institutions to move significant value between the fiat and crypto worlds.

- Reserve Structure: USDC is fully backed by reserves held in segregated accounts, consisting of cash and short-duration U.S. government obligations, offering a high degree of stability.

- Institutional Mint & Redeem: Qualified institutions can use Circle Mint to directly mint and redeem USDC on a 1:1 basis with U.S. dollars, providing a seamless on- and off-ramp.

- Multi-Chain Support: USDC is available on numerous blockchains, including Ethereum, Solana, Avalanche, and Polygon, enabling developers to build applications across different ecosystems with a consistent dollar asset.

- Transparent Attestations: Circle publishes monthly attestation reports from a third-party accounting firm, providing public verification of its reserve holdings.

Access and Practical Implementation

For retail users, acquiring USDC is as simple as purchasing it on any major U.S.-based cryptocurrency exchange or through compatible wallets. Its wide integration makes it one of the most liquid and accessible stablecoins. Institutions and high-net-worth individuals, however, can apply for a Circle Mint account for direct, fee-efficient minting and redemption. The minimum transaction sizes for Circle Mint make it suitable for businesses that need to manage large-scale treasury operations, conduct cross-border payments, or provide liquidity in DeFi. This infrastructure makes USDC an attractive asset for those looking to earn returns, and there are various strategies for how to earn high yield with USDC.

Website: https://www.circle.com/usdc

7. Gemini – Gemini Dollar (GUSD)

Gemini Trust Company, a New York Department of Financial Services (NYDFS) regulated trust, issues the Gemini Dollar (GUSD), a stablecoin backed 1:1 by U.S. dollars. While not a traditional bank, Gemini operates under a similar regulatory microscope, offering a highly compliant and transparent stablecoin. This makes it a crucial player in the ecosystem of institutions bridging traditional finance and digital assets, effectively serving a similar role to banks with stablecoins by providing a regulated on-ramp to the digital economy.

The Gemini website clearly outlines the value proposition of GUSD, emphasizing its regulatory oversight, security, and redeemability. Users can find detailed information on the monthly reserve attestations performed by an independent accounting firm, which verify that the outstanding GUSD supply is fully collateralized by U.S. dollars held in FDIC-insured bank accounts. This commitment to transparency provides users with confidence in the asset's stability and backing.

Key Features and Operational Flow

GUSD’s integration within the Gemini exchange ecosystem creates a seamless experience for users looking to move between fiat and digital currency. The entire lifecycle, from acquiring GUSD with USD to redeeming it back, is managed within a single, regulated platform.

- Regulated Issuer: GUSD is issued by Gemini Trust Company, LLC, a trust company chartered by the NYDFS, subjecting it to stringent capital reserve, cybersecurity, and compliance standards.

- Transparent Reserves: Gemini publishes monthly attestation reports from independent auditors, providing public verification of the U.S. dollar reserves backing GUSD.

- Token Standard: As an ERC-20 token on the Ethereum blockchain, GUSD is compatible with a wide array of wallets, DeFi protocols, and decentralized applications.

- Seamless Conversion: Users on the Gemini platform can instantly convert U.S. dollars to GUSD and vice versa at a 1:1 ratio with no fees for the conversion itself.

Access and Practical Implementation

GUSD is available to both retail and institutional users through the Gemini exchange. The primary requirement is to create and verify an account on the platform, which involves standard KYC/AML procedures. Once an account is funded via bank transfer (ACH or wire), users can directly purchase GUSD. This straightforward on-ramp makes it a popular choice for those entering the digital asset space or for developers needing a reliable, programmable U.S. dollar for their applications. Given its fungibility, users often need to exchange it for other stablecoins, and understanding the nuances of these transactions is key; you can learn how to swap stablecoins efficiently to manage your assets effectively.

Website: www.gemini.com/dollar

7-Bank Stablecoin Comparison

| Name | Implementation complexity | Resource requirements | Expected outcomes | Ideal use cases | Key advantages |

|---|---|---|---|---|---|

| Custodia Bank – Avit | Moderate–high (bank + public‑chain integration) | Bank onboarding, compliance, custody, Ethereum gas | Regulated tokenized USD deposits with on‑chain auditability | Institutional pilots; bank‑to‑bank tokenized deposits | Bank‑issued, permissionless chain auditability, documented flow |

| Vantage Bank – Avit collaboration hub | Moderate (operational split & settlement design) | Reserve management, Fedwire/ACH integration, consortium coordination | Clear bank operational model for stablecoin settlement | Banks/credit unions evaluating participation or consortiums | Detailed reserve & settlement procedures; practical bank roadmap |

| J.P. Morgan – Kinexys / JPM Coin | High (enterprise private ledger + bank systems) | Enterprise integration, dedicated infrastructure, onboarding support | Near‑real‑time, 24/7 institutional cash settlement at scale | Large corporates and financial institutions for treasury settlement | Production‑proven, Tier‑1 bank backing, low‑latency settlement |

| Société Générale – SG‑FORGE (EURCV / USDCV) | High (MiCA compliance, multi‑chain issuance) | Regulatory compliance, collateral custody, exchange listings | Regulated e‑money tokens with transparent, daily collateral disclosure | Euro liquidity providers, institutional trading, regulated issuance | Major bank sponsor, daily collateral transparency, multi‑chain availability |

| PayPal – PayPal USD (PYUSD) | Low–moderate (consumer app integration; issuer via Paxos) | PayPal/Venmo accounts, Paxos custody, network fees for on‑chain transfers | Easy retail on‑ramp/off‑ramp; in‑app transfers and checkout use | Retail payments, P2P transfers, mainstream crypto entry | Integrated UX in PayPal/Venmo, simple consumer access, fee‑friendly in‑app flows |

| Circle – USDC | Moderate (multi‑chain, institutional mint/redeem) | Institutional onboarding for Circle Mint, reserve custody (BNY Mellon) | High liquidity, broad integrations, institutional mint/redeem capability | Exchanges, cross‑border payments, institutional treasuries | Wide adoption, monthly reserve disclosures, multi‑chain support |

| Gemini – Gemini Dollar (GUSD) | Low–moderate (exchange‑issued, regulated trust) | Gemini account, trust regulation compliance, monthly attestations | Regulated, 1:1 redeemable stablecoin with platform conversion | Users seeking regulated exchange on/off‑ramp and compliance | NYDFS‑regulated issuer, regular attestations, straightforward on‑platform redeemability |

Navigating the Future: Your Next Steps in Bank-Driven Digital Assets

The line between traditional banks and blockchain is blurring, creating a spectrum of digital dollar solutions. From Custodia Bank’s public-chain tokens to J.P. Morgan’s private-ledger model, each institution offers unique stablecoin infrastructure. This section distills core insights and equips you with actionable steps for 2025 and beyond.

Reviewing Bank Stablecoin Models

- Custodia Bank – Avit: Direct issuance on public chains with transparent reserves.

- Vantage Bank – Avit Collaboration Hub: Modular APIs for fintech integration.

- J.P. Morgan – Kinexys (JPM Coin): Private network optimized for interbank settlement.

- Société Générale – SG-FORGE (EURCV, USDCV): MiCA-compliant e-money tokens on public blockchains.

- PayPal – PayPal USD (PYUSD): Retail-focused stablecoin with strong on-ramp off-ramp rails.

- Circle – USDC: Open reserve attestations and multi-chain support.

- Gemini – GUSD: Compliance-first approach with regular audits.

Actionable Next Steps

For Developers

- Explore each bank’s SDKs and API docs to prototype payment rails.

- Spin up testnet wallets on public chains (Avit, SG-FORGE) and private networks (Kinexys).

- Integrate webhook notifications for on-chain events and settlement confirmations.

For Investors

- Review regulatory filings and reserve attestations for each token.

- Compare yield opportunities in regulated custody vs decentralized protocols.

- Monitor bank partnerships and new product roadmaps via official developer portals.

For Businesses

- Assess treasury needs: cross-border settlement vs domestic payroll.

- Evaluate custodian risk by checking proof of reserves frequency.

- Build conditional payment flows using smart contracts or API triggers.

Key Factors to Consider

- Regulatory Status: MiCA compliance, US money-transmitter licenses, state charter variations.

- Reserve Structure: Attestation frequency, composition (cash, T-bills), risk buffers.

- Operational Scalability: Transaction throughput, API rate limits, network uptime.

- Partnership Ecosystem: Banking corridors, custodial integrations, payment rail coverage.

Staying Ahead in 2025 and Beyond

As bank-issued and bank-backed stablecoins gain traction, your ability to monitor and manage these digital assets will matter more than ever. Robust methods for tracking stablecoin fund flows will be essential for operational efficiency and compliance.

Banks with stablecoins represent a fundamental shift in how enterprises handle liquidity, remittances, and treasury management. By staying informed on evolving regulations and forging early integrations, you position yourself at the forefront of digital currency adoption.

Embrace the convergence of banking and blockchain as a catalyst for innovation. The diversified models we explored—from public-chain jostling for transparency to private-ledger efficiency—are all part of a vibrant ecosystem. Your next move could define your competitive edge in 2025 and beyond.

Ready for deeper insights? Discover expert analysis, regulatory updates, and hands-on guides at Stablecoin Insider. Explore how our platform keeps you ahead in the rapidly evolving world of banks with stablecoins by visiting Stablecoin Insider.

{kind=link}