Table of Contents

In a significant setback for cryptocurrency regulation, major U.S. banks have rejected a White House compromise on stablecoin rewards, halting negotiations over the U.S. Clarity Act.

The proposal, aimed at allowing limited rewards resembling interest yields on stablecoins, was intended to bridge gaps between traditional finance and the crypto sector.

This opposition, voiced during high-level talks in Washington, D.C., could delay the bill's passage indefinitely, potentially slowing mainstream adoption of digital assets.

President Donald Trump, a vocal proponent of the legislation, publicly criticized the banks for what he called "undermining America's economic future."

As of March 5, 2026, the impasse highlights ongoing tensions between Wall Street giants and the administration's pro-crypto stance.

Key Takeaways

- Banks' Opposition: Major institutions rejected limited rewards on stablecoins, fearing competition with traditional banking products.

- White House Proposal: A compromise allowing capped, interest-like yields to promote crypto while maintaining oversight.

- Trump's Criticism: The President accused banks of undermining his pro-crypto agenda, signaling potential executive action.

- Impact on Crypto: Delays in the U.S. Clarity Act could slow stablecoin growth and broader digital asset adoption.

- Broader Implications: Highlights tensions between legacy finance and emerging tech, with risks of offshoring innovation.

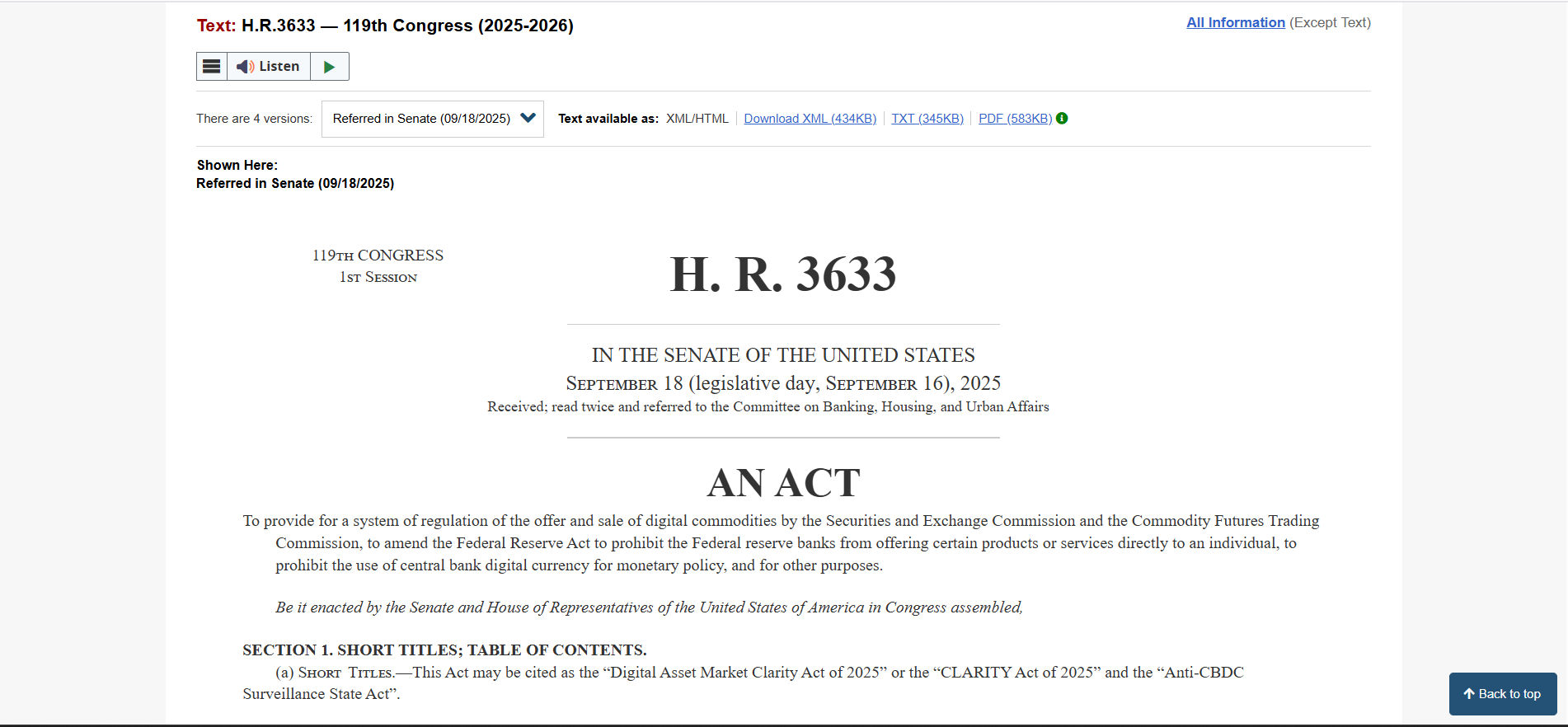

The U.S. Clarity Act, introduced in late 2025, seeks to provide regulatory clarity for stablecoins (digital currencies pegged to fiat like the U.S. dollar).

Stablecoins, such as USDT and USDC, have surged in popularity, with a market cap exceeding $200 billion.

The White House's compromise offered a middle ground: permitting capped rewards to make stablecoins more attractive to users while addressing banks' concerns over competition with traditional deposits.

However, banks argue that even limited yields could erode their deposit base, leading to financial instability.

Negotiations Breakdown and Key Details

The stalemate emerged after weeks of closed-door discussions involving representatives from JPMorgan Chase, Bank of America, and Citigroup, alongside White House officials and crypto industry leaders like Circle and Tether executives.

Sources close to the talks revealed that the White House proposed rewards capped at 2% annually, tied to Treasury yields, with strict oversight by the Federal Reserve. This was seen as a concession to banks, who fear stablecoins could siphon trillions from savings accounts.

Despite the olive branch, banks unanimously opposed the measure, citing risks to monetary policy and consumer protection.

"Allowing yields on stablecoins blurs the line between banking and unregulated crypto," a banking lobbyist stated anonymously.

The rejection has fueled speculation that banks are protecting their turf amid rising crypto integration, with DeFi platforms already offering yields far exceeding traditional rates.

President Trump's response was swift and pointed. In a post on X (formerly Twitter), he accused banks of "sabotaging innovation" and vowed to push the bill forward without their input.

"The big banks are scared of competition. We're building a stronger America with crypto, not bowing to Wall Street elites," Trump wrote, garnering millions of views. This echoes his 2024 campaign promises to make the U.S. a "crypto capital," including tax incentives for digital assets.

The delay could have ripple effects. Analysts predict that without the Clarity Act, stablecoin issuers might relocate offshore, costing the U.S. economy jobs and tax revenue.

Crypto adoption, already at 15% among Americans, could stagnate as regulatory uncertainty persists. Meanwhile, global competitors like the EU and Singapore advance their own stablecoin frameworks, potentially leaving the U.S. behind.

Conclusion

The rejection of the White House's stablecoin rewards compromise marks a pivotal moment in U.S. crypto policy.

As negotiations stall, the U.S. Clarity Act hangs in the balance, testing the administration's ability to reconcile innovation with financial stability.

President Trump's criticism underscores a growing divide, but it may galvanize support among crypto advocates.

Moving forward, compromise will be essential to unlock stablecoins' potential without destabilizing the economy.

With global competition intensifying, resolving this impasse swiftly could define America's role in the digital future.

Read Next:

- 9 Fastest-Growing Stablecoin Use Cases In 2026

- Top 10 Stablecoin Compliance Tools in 2026

- Solana's New Payments.org Just Changed Stablecoin Payments in 2026

FAQs:

1. What is the U.S. Clarity Act?

The U.S. Clarity Act is proposed legislation to regulate stablecoins, providing clear guidelines for issuance, reserves, and integration with traditional finance.

2. Why did banks reject the stablecoin rewards proposal?

Banks opposed it due to concerns that interest-like yields on stablecoins could compete with deposits, potentially causing financial instability.

3. How has President Trump responded to the banks' rejection?

Trump criticized banks for undermining his agenda, posting on X about their fear of crypto competition and vowing to advance the bill.

4. What are the potential impacts on crypto adoption?

Delays could slow mainstream use of stablecoins, lead to offshoring, and hinder U.S. leadership in digital assets amid global advancements.

5. Could the Clarity Act still pass without bank support?

Yes, through congressional action or executive orders, though it may face legal challenges and require broader stakeholder buy-in.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}