Table of Contents

CREDITS: Eshita Nandini

Financial institutions have both welcomed and resisted the proliferation of stablecoins, the latter through attempts to dampen their functionality.

The end state of how stablecoins will assimilate into legacy banking is unclear, as regulation and adoption will define how the transition takes shape. However, while stablecoins currently depend on banks for custody and compliance, they are increasingly pushing settlement and liquidity off bank balance sheets, a trend started by earlier waves of non-banks.

It is clear that banks remain essential, but they are no longer central to where new financial activity occurs.

The waning pursuit of being a bank

Most non-banks (fintechs and stablecoin-enabled fintechs) hardly want to replace existing banking fortresses. Banks are heavily regulated, shaped by the creation of the Federal Reserve in 1913; regulation has continued to tighten ever since, especially after events like the 2008 global crisis (Basel III). This impacted new bank formation, making FDIC insurance time- and cost-intensive to obtain.

Non-banks historically partnered with chartered banks to avoid those costs. Some eventually pursue charters as they scale, but not all - Chime, for example, has continued without one as the bank partnership is actually advantageous for the business. Others, particularly crypto entities, have sought out alternatives such as national trust bank charters. We will continue to see more versions of "skinny charters" to gain regulatory recognition without full bank constraints.

These alternatives illustrate that not all non-banks need to be a bank, even if they need to operate within the banking system and depend on it. The shift away from traditional banking reflects a fundamental change in how users interact with money.

Deposits might be starting to fade

Deposits are no longer the default store of value for all customers, and this trend predates stablecoins. Fintechs made banking accessible via clean mobile interfaces, creating a new relationship between users and their money focused on diversification and movement vs. plain deposits.

- In 2025, over 72% of U.S. adults reported using mobile banking apps, up from 65% in 2022.

- In 2024, Cash App alone moved $283 billion in annual inflows across 55 million users.

Though legacy banks retain the bulk of existing deposits, they are losing the flow of new relationships.

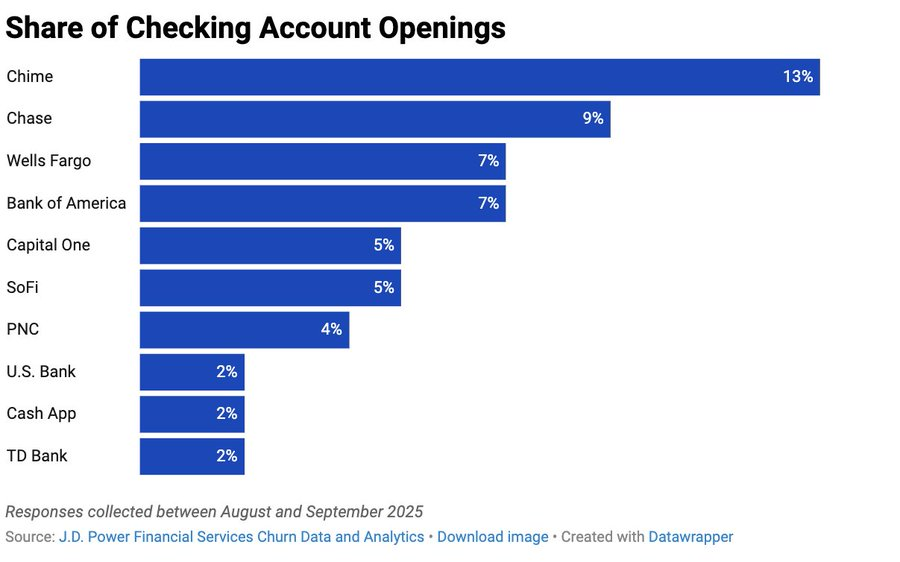

Chime captured an estimated 13% of all new checking account openings in Q3 2025, beating out Chase (9%) and Wells Fargo (7%).

This validates the importance of velocity when it comes to money. Users keep their traditional account open as dormant storage, but they move their daily direct deposit and spending to options like Chime.

From the study, 52% of these new accounts were opened as "additional" accounts vs. primary. Users are not moving over completely because they still need the full service of a traditional bank/checking account.

But, Chime is winning over users by solving for constraints that legacy banks didn't:

- MyPay: Allows members to access up to $500 of their pay before payday. For the 60% of Americans living paycheck to paycheck, this is an important feature.

- Credit Builder: A 0% interest secured card that builds credit history, locking users in by turning their daily spend into a credit score asset.

Stablecoins as the wedge

Crypto providers (stablecoin-enabled banks, wallets, issuers, onramps) do not provide the full "operating system" (checking, bill pay, etc.) needed to consolidate a user's entire financial life. But they possess a powerful wedge, which is stablecoins. While Chime offers movement when it comes to fiat, stablecoins offer instant global settlement and yields that traditional finance struggles to offer at scale.

Providers should not try to replace the checking account on day one. The friction of moving a "primary account" is too high. Instead, they must aggressively monetize their unique advantages, yield and velocity, to win the user's daily flow. Once they own the velocity, introducing the rest of the stack (direct deposit, bill pay) becomes a retention mechanism.

Although users with existing banking relationships still treat non-banks as secondary spending accounts, this friction is temporary. As deposits drift to regulated non-banks and stablecoins, the traditional banking model faces a challenge as deposits are the raw material for lending.

When capital sits in stablecoins or yield-generating protocols instead of bank deposits, traditional banks lose their primary source of lending capacity. Credit will fragment. Some will remain with consolidated mega-banks that can still attract deposits at scale. Others will move to specialized non-bank lenders. And increasingly, some will flow to DeFi protocols that can offer programmatic, overcollateralized lending without traditional bank infrastructure.

Users get better yields and faster settlement through stablecoins, but banks lose the deposit base that funds mortgages, business loans, and consumer credit. As stablecoin-enabled financial services refine their user experience, this will only continue.

The transformation of financial behavior

Stablecoins are the next phase of users pursuing better ways to store and use their funds. Today, most usage (outside of remittances and payments in inflation-prone economies) is tied to trading.

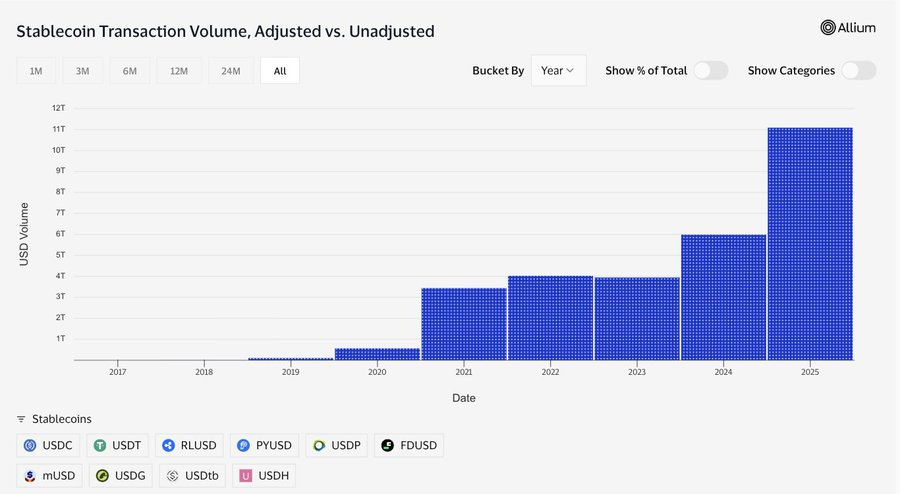

Major stablecoins have processed over $11 trillion in transaction volume (adjusted for noise and bot activity) in 2025, an 85% increase from 2024.

Yet despite this surge in onchain velocity, stablecoins have not triggered deposit flight. A July 2025 study found no material outflow from community banks attributable to stablecoin usage. Part of it is because people trust what they understand, which is banks for now.

A recent survey found that nearly 75% of consumers would consider using stablecoins only if offered through their bank. For now, stablecoins will thrive through banks, not outside of them. This explains why platforms like SoFi, which holds a full national bank charter operates the SoFiUSD stablecoin; they are positioned as a trusted entity, while providing forward-looking options. It's a modern experience, but fundamentally a traditional product.

This explains why banks are lobbying aggressively (i.e. market structure bill) that seek to restrict how stablecoins can offer yield or operate without banking charters. The defensive position is expected and we've seen it before when regulators torched Libra before it could actually threaten monetary and banking orthodoxy.

But defensive regulations only work if user behavior stops evolving. It hasn't.

Automation will eliminate the trust barrier

The constraint keeping stablecoins tethered to banks is trust and usability. Today's onchain activity is largely user-managed, driven by crypto-native users willing to manage risk. In 2025, there were roughly 198 million wallets engaged in DeFi. Mainstream users won't reflect the same behavior.

This is where agent-managed wallets finish the rest of the transition. When automation handles everything from risk management to yield allocation, the friction to use these products disappears. This mirrors the evolution of robo-advisors and passive investing, now enhanced by access to onchain rails (vaults being central to this experience).

As users embrace automation, less capital will sit idle in traditional bank deposits. Even checking account stickiness, rooted in interoperability, may fade as users rely on agents to manage their funds.

Stablecoins backed by tokenized T-bills can offer 4-6% yields that track the risk-free rate, something traditional savings accounts struggle to match due to overhead and profit margins. When agents can move capital between checking (0% yield), stablecoin savings, and optional higher-yield strategies for risk-tolerant users, the traditional deposit account loses its appeal.

Stablecoins compress the gap between deposits and the risk-free rate, while also offering access to strategies across the risk spectrum. Traditional banks can't compete with that optionality as we know that users opt for convenience

Banks become the infrastructure layer

The number of FDIC-insured commercial banks in the U.S. has collapsed by more than 70% since 1984, driven by consolidation and regulatory barriers. In some ways, bank failures are a feature where only the largest or most agile survive.

This pattern will continue, especially as deposits become more dynamic and less “parked.” Smaller and mid-sized banks, those most dependent on sticky retail deposits, will struggle to compete for liquidity that increasingly flows through onchain rails. Consolidation will follow. While insured deposit rules (like the 10% ceiling) technically limit bank dominance, exceptions are made in moments of fragility, as we saw with JPMorgan’s acquisition of First Republic in the 2023 liquidity crisis.

What remains most defensible for banks is their role in compliance, custody, access to central bank liquidity, and deposit insurance. But they’re also not where the capital wants to move. Capital wants composability, instant settlement, and programmability. Banks become scaffolding for new financial infrastructure, this scaffolding is increasingly fixed, even as the rails above it evolve.

The infrastructure problem is largely solved. Bridging is no longer a disjointed nightmare, and we have alternatives to raw key management. The technical friction that once protected legacy finance is gone. What remains is trust and convenience - both of which are being actively challenged.

The environment today is fundamentally different from 2019. Back then, there were few established crypto companies and fewer use-cases that could stand independently against regulatory pushback. Now, stablecoins process more volume than most payment networks, DeFi manages tens of billions in assets, and the talent base has matured significantly.

Banks will win the near term. They have trust, regulatory clarity, and the infrastructure to serve the basic requirements of financial life. But trust follows utility, and utility is shifting. Fintechs proved users will move for better UX and stablecoins prove they'll move for better rails.

Users will adapt to stablecoin-enabled products and eventually onchain finance that challenges the foundation of capital that they are used to. To assume otherwise would be to ignore every lesson from the past two decades of financial innovation. Banks will either evolve into active participants, or they'll calcify into compliance layers as capital flows elsewhere. The timeline of when remains variable.

{kind=link}