Table of Contents

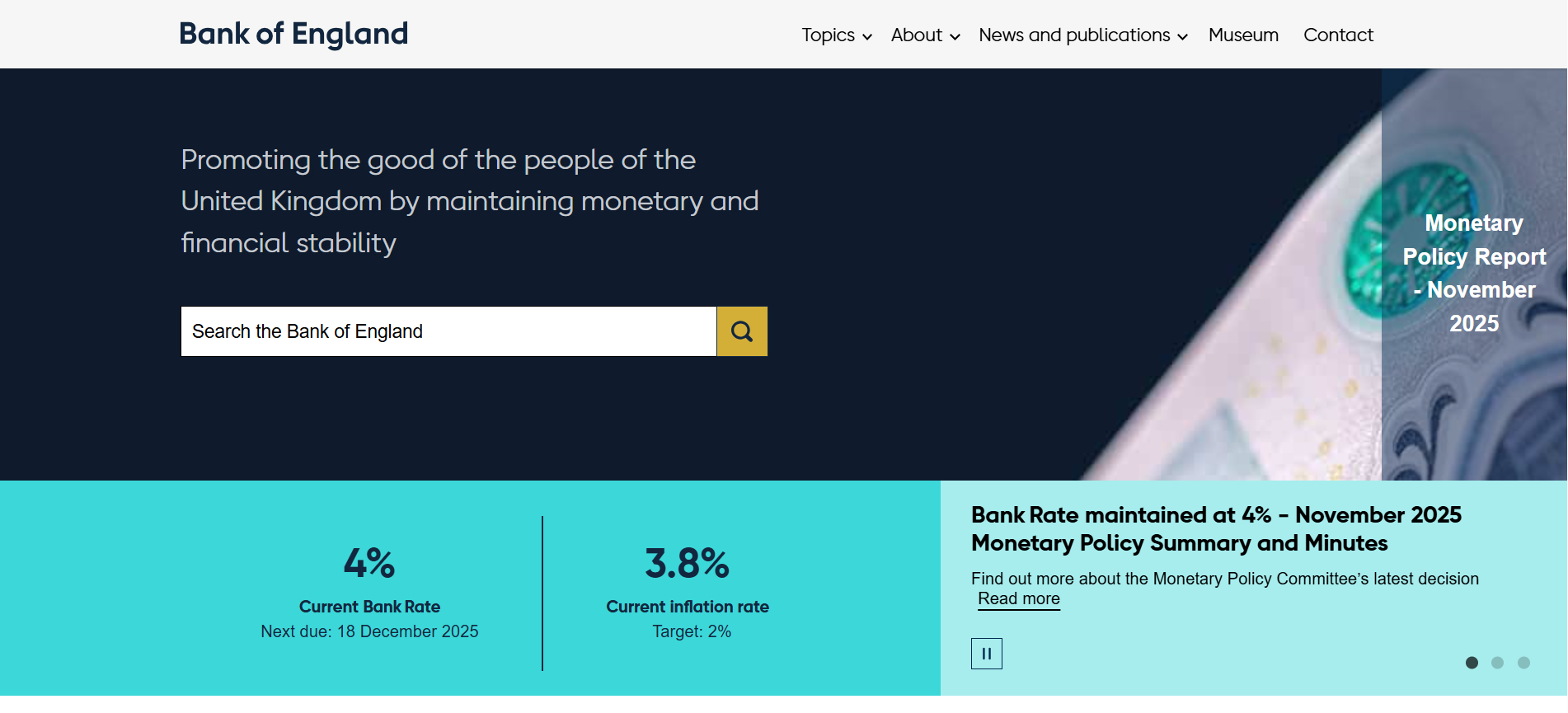

The Bank of England (BoE) has unveiled a significant shift in its approach to regulating stablecoins, proposing rules that aim to foster innovation in the UK's digital finance sector while safeguarding financial stability.

Released on November 10, 2025, this consultation paper outlines a framework for sterling-denominated systemic stablecoins, allowing issuers greater flexibility in asset backing and introducing temporary holding limits to manage risks during the early adoption phase.

This move comes amid growing global interest in stablecoins as a bridge between traditional finance and cryptocurrencies, positioning the UK as a competitive player in the world of digital payments.

Key Takeaways

- The BoE proposes allowing systemic stablecoin issuers to hold up to 60% of backing assets in short-term UK government debt securities, with at least 40% in unremunerated central bank deposits, marking a relaxation from earlier requirements for full central bank backing.

- Temporary per-coin holding limits are set at £20,000 for individuals and £10 million for non-financial businesses to prevent rapid shifts from bank deposits, with exemptions available for certain business use cases.

- The regime focuses exclusively on systemic sterling-denominated stablecoins used for retail and wholesale payments, excluding non-systemic or crypto-trading focused stablecoins regulated solely by the Financial Conduct Authority (FCA).

- Transitional measures include a "step-up" regime permitting up to 95% in government debt for new or transitioning issuers, alongside potential access to BoE liquidity facilities during market stress.

- Compared to the US, the UK's rules are stricter with holding caps, but they aim to match the pace of US implementation while encouraging a safe environment for stablecoin growth.

Background on BoE's Stablecoin Regulation Evolution

The BoE's latest proposals build on its 2023 discussion paper, which initially mandated that all backing assets for systemic stablecoins be held in non-interest-bearing deposits at the central bank.

Industry feedback highlighted concerns that such strict rules could stifle innovation and make UK stablecoins less competitive. In response, the BoE has softened its stance, incorporating more flexible asset options while aligning with the UK's National Payments Vision.

HM Treasury plays a key role in designating which stablecoins are "systemic," based on factors like transaction volume, interconnectedness, and potential risks to financial stability.

This step reflects a broader push to integrate digital assets into the economy without compromising safety.

Details of Backing Asset Requirements

Under the proposed regime, systemic stablecoin issuers must maintain backing assets that ensure redemption at par value, promoting trust and stability. The core requirement is a 60/40 split: up to 60% in short-term sterling-denominated UK government debt securities (such as Treasury bills) and at least 40% in unremunerated deposits at the BoE.

This allows issuers to earn some yield on assets while limiting impacts on monetary policy.

Temporary deviations are permitted for handling large redemptions, but issuers must notify the BoE and rebalance promptly. For liquidity management, securities can be lent via repurchase agreements, though borrowing is prohibited.

- Transitional provisions offer flexibility: new systemic issuers or those shifting from FCA oversight can start with up to 95% in government debt, gradually reducing to 60% as they scale.

Additionally, the BoE may provide liquidity backstops in crises, similar to those for banks, to prevent fire sales of assets.

Holding Limits and Risk Mitigation Measures

To address risks like sudden outflows from traditional bank deposits, the BoE introduces temporary holding caps on a per-coin basis. Individuals are limited to £20,000 per stablecoin issuer, while non-financial businesses face a £10 million cap.

These limits are designed to be phased out as the market matures and risks diminish.

Exemptions apply for businesses needing higher balances for operational purposes, such as retailers accumulating payments or crypto trading platforms serving clients. The BoE is seeking feedback on alternatives, including operational challenges and potential impacts on usability.

The consultation, open until February 10, 2026, invites input on refining these measures to balance innovation with protection against financial instability.

Scope and Oversight of the Regime

The rules target only systemic stablecoins, those denominated in sterling and used widely for payments, potentially posing risks to UK financial stability. This includes retail (e.g., everyday consumer transactions), corporate (e.g., business-to-business), and certain wholesale settlements, but excludes non-systemic stablecoins or those primarily for crypto trading, which fall under FCA jurisdiction.

HM Treasury will recognize systemic status based on criteria like scale and substitutability, with prospective designations for emerging issuers.

Oversight is shared: the BoE handles prudential and stability aspects under the Banking Act 2009, while the FCA manages conduct, consumer protection, and competition. Detailed Codes of Practice, including rules on asset maturity and supervision, are slated for consultation and finalization in late 2026.

Global Comparisons and Implications for UK Crypto Sector

The UK's approach is more stringent than the US, where no holding limits exist, potentially making American stablecoins more attractive for large holders. In contrast, the EU's Markets in Crypto-Assets (MiCA) framework emphasizes issuer licensing and reserves but lacks similar caps.

Experts note that while the BoE's caps could initially hinder adoption, the flexible backing rules signal a commitment to competitiveness, aiming to roll out the regime as swiftly as the US.

On X (formerly Twitter), reactions vary: the Crypto & Digital Assets APPG welcomed the softened stance but expressed concerns over caps inhibiting innovation, with no timeline for removal. Industry voices highlight potential boosts to UK fintech, but warn of over-regulation stifling growth.

Overall, these proposals could enhance stablecoin trust, driving broader adoption in payments while mitigating systemic risks.

Conclusion

The Bank of England's proposals represent a pragmatic evolution in stablecoin regulation, striking a balance between encouraging technological advancement and protecting the financial system. By allowing diversified backing assets and implementing transitional safeguards, the UK aims to create a robust ecosystem for digital payments.

As the consultation progresses, stakeholder input will be crucial in fine-tuning these rules, potentially cementing the UK's role as a global leader in regulated crypto innovation.

With finalization expected in 2026, this framework could pave the way for safer, more efficient financial services.

Read Next:

- The 2025 STABLE Act: Complete Breakdown of America's New Stablecoin Regulation

- mUSD Stablecoin: Complete Breakdown of the MetaMask's New Dollar Token

- Hong Kong Stablecoin Regulation 2025: What You Should Know

FAQs:

1. What are the new Bank of England rules for stablecoin backing assets?

The BoE allows up to 60% of backing assets in short-term UK government debt securities and at least 40% in unremunerated central bank deposits, a more flexible approach than initial plans requiring full central bank holdings.

2. Why is there a £20,000 holding limit for individuals in UK stablecoins?

This temporary per-coin cap is intended to mitigate risks of rapid bank deposit outflows and financial instability during the early stages of stablecoin adoption, with plans to loosen or remove it over time.

3. How do UK stablecoin regulations compare to the US?

The UK imposes holding caps absent in the US, making its regime tougher, but it seeks to implement rules at a similar pace to foster competitiveness in digital finance.

4. Which stablecoins fall under the BoE's new systemic regulations?

Only sterling-denominated systemic stablecoins used for widespread payments; non-systemic or crypto-trading stablecoins remain under FCA oversight.

5. When will the BoE finalize its stablecoin rules?

The consultation ends on February 10, 2026, with detailed Codes of Practice and final rules expected in late 2026.

6. What transitional support is available for stablecoin issuers?

New or transitioning issuers can hold up to 95% in government debt initially under a step-up regime, with access to BoE liquidity in stress scenarios to ensure orderly growth.

{kind=link}