Table of Contents

Bank-issued stablecoins are moving from proof of concept to production-grade infrastructure in 2026.

Banks are using fiat-backed stablecoins (and closely related tokenized deposit models) to enable faster settlement, 24/7 treasury operations, and programmable money flows across internal systems and selected external networks.

What matters most in 2026 is not who minted a token first, but who can distribute it compliantly, redeem it reliably, and integrate it into real payment and settlement workflows.

Key takeaways

- Bank-issued stablecoins are increasingly paired with tokenized deposits to deliver regulated on-chain cash for institutional settlement and treasury.

- Most bank tokens remain institutional-first in 2026 due to compliance controls, onboarding requirements, and limited distribution.

- The next phase is embedded rails: stablecoins as a settlement layer inside transaction banking, not a standalone coin launch.

Bank-Issued Stablecoins and Bank-Group Fiat Tokens in 2026

1) JPM Coin (J.P. Morgan / Kinexys Digital Payments)

JPM Coin is an institutional “digital cash” system used for settlement and treasury-style flows inside J.P. Morgan’s network, often discussed as a deposit-token model rather than a retail stablecoin. It is designed for high-throughput, permissioned usage with enterprise-grade controls and integrations.

Pros

- Deep integration with transaction banking and institutional settlement workflows

- Enterprise-grade compliance controls and operational reliability

- Designed for high-volume use cases (treasury, liquidity, settlement)

Cons

- Limited access (primarily institutional clients, permissioned participation)

- Less useful for open, public-chain liquidity compared to broadly distributed stablecoins

- Coverage is network-dependent, not universally interoperable

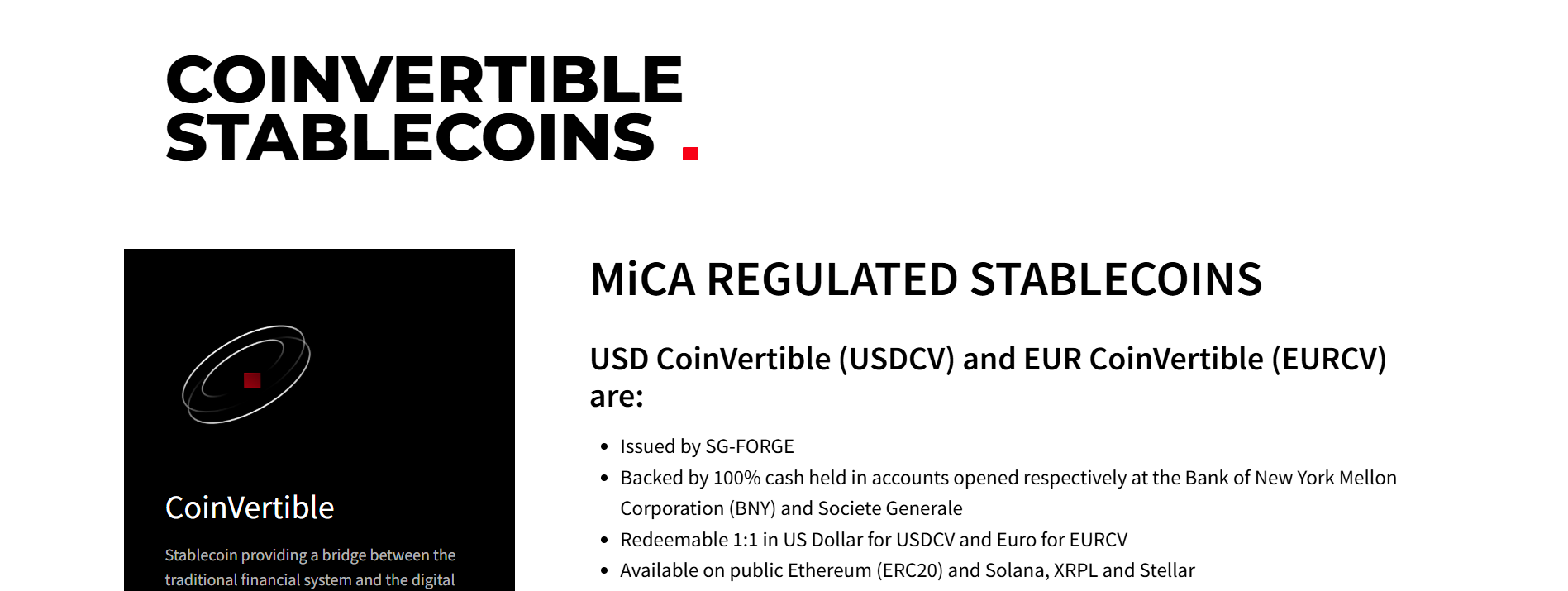

2) EUR CoinVertible (EURCV) (Société Générale–FORGE)

EURCV is a euro-denominated bank-affiliated stablecoin designed to support regulated on-chain settlement and tokenized asset workflows. It is positioned for institutional use cases where euro on-chain cash is needed for DvP, collateral, and payments.

Pros

- Euro-denominated option built for regulated financial-market workflows

- Strong alignment with institutional tokenization and settlement use cases

- Bank-affiliated governance can be attractive for compliance-led adopters

Cons

- Distribution and liquidity can be narrower than mainstream stablecoins

- Access may be routed through institutional partners and approved venues

- Utility depends heavily on which chains/venues support it in practice

3) USD CoinVertible (USDCV) (Société Générale–FORGE)

USDCV is the USD counterpart to EURCV, designed for regulated on-chain settlement and institutional liquidity pathways. It is aimed at use cases where USD settlement finality is required alongside tokenized assets and institutional DeFi connectivity.

Pros

- USD settlement instrument positioned for institutional tokenization markets

- Bank-affiliated issuance can simplify internal risk approvals

- Potentially useful for cross-venue USD liquidity and settlement flows

Cons

- Not as universally distributed as USDC/USDT, so liquidity can be fragmented

- Practical usefulness is highly dependent on supported venues and integrations

- Typically not built for retail-first distribution

4) EURI (Eurite) (Banking Circle)

EURI is a euro stablecoin issued by Banking Circle, positioned around regulated issuance and payments-centric distribution. The product is designed to support exchange rails and payment flows rather than being a purely DeFi-native stablecoin.

Pros

- Euro-denominated stablecoin with a payments and regulated-issuer posture

- Clear use case alignment with exchanges and payment rails

- Can help firms that need euro on-chain liquidity without building banking rails

Cons

- Ecosystem depth may be smaller than long-established USD stablecoins

- Liquidity and acceptance vary across venues and jurisdictions

- Bank-grade onboarding requirements can reduce “plug-and-play” adoption

5) Avit (Custodia Bank + Vantage Bank) (Tokenized demand deposits)

Avit is positioned as tokenized bank deposits rather than a conventional, broadly marketed stablecoin, with pilots conducted on permissionless blockchain rails. It is best understood as an attempt to put demand deposits on-chain with bank-style compliance and redemption structure.

Pros

- Deposit-token framing can appeal to banks and regulated institutions

- Built to integrate with bank-style compliance, stablecoin settlement, and redemption controls

- Demonstrates a workable model for on-chain bank money on public rails

Cons

- Pilot/limited scope relative to mainstream stablecoin distribution

- Adoption depends on banking partnerships and regulatory comfort

- Not designed to compete with retail liquidity networks

6) A$DC (ANZ)

A$DC is an Australian dollar stablecoin issued by ANZ and used in disclosed real-world transaction pilots involving tokenized payments and smart contract settlement logic. It demonstrates how banks can use stablecoins to settle cross-border B2B payments with fewer cut-off constraints and clearer transaction automation.

Pros

- AUD-denominated bank-issued token supporting real transaction pilots

- Useful for programmable settlement in controlled B2B environments

- Strong narrative fit with tokenized asset settlement in local markets

Cons

- Primarily a pilot/limited distribution asset, not broadly liquid

- Cross-border usage depends on counterparties and supported rails

- AUD stablecoin demand is structurally smaller than USD demand

7) COPW (Wenia / Grupo Bancolombia group)

COPW is a Colombian peso stablecoin launched under a bank-group initiative via Wenia, designed to support local digital-asset use cases and peso-denominated on-chain value transfer. It reflects a regional-bank pattern: issue local-currency stablecoins to expand domestic rails and digital finance access.

Pros

- Local-currency on-chain liquidity for Colombia-focused use cases

- Bank-group backing can improve trust and compliance posture

- Strong fit for domestic payments and local exchange ecosystems

Cons

- Local-currency stablecoins can face thinner liquidity than USD tokens

- Utility is often geographically concentrated and venue-dependent

- Cross-border corridors may still require USD/EUR bridging

What’s next for bank-issued stablecoins in 2026

1) Stablecoin vs tokenized deposit becomes a design choice, not a debate

Banks are increasingly choosing the structure that best fits their regulatory perimeter and balance-sheet preferences. Expect more deposit-token style launches for bank-to-bank and bank-to-corporate settlement, with stablecoin-style issuance where distribution requires it.

2) Expansion will be driven by settlement networks and transaction banking

The big shift is stablecoins embedded into existing bank products: cash management, liquidity sweeps, intraday funding, collateral movement, and settlement automation. Going live in 2026 increasingly means integration into operational systems, not just minting on a chain.

3) Interoperability becomes the competitive moat

Banks that connect to multiple rails: permissioned networks, select public chains, and institutional settlement layers, will win distribution. In practice, the most valuable bank-issued tokens will be those that move cleanly across the venues where clients already trade, borrow, and settle.

Conclusion

In 2026, bank-issued stablecoins are best viewed as regulated, workflow-specific digital cash rails rather than mass-market coins.

The most practical tokens are the ones that combine clear redemption mechanics, strong compliance controls, and tight integration into transaction banking and settlement networks.

For operators, the decision is less about headline adoption and more about where the token can actually move: the counterparties you pay, the venues you settle on, and the rails your treasury already uses.

Read Next:

- Savings GHO (sGHO) from Aave: Full 2026 Review

- Tether (USDT) January 2026 Reserves Report

- How to Earn High Yield with USDC: Top 3 Platforms in 2026

FAQs:

1. Are bank-issued stablecoins safe?

They can be safer operationally when integrated into regulated banking controls, but risk depends on structure (stablecoin vs tokenized deposit), redemption terms, and counterparty exposure. Always assess issuer governance, redemption mechanics, and where the token actually circulates.

2. Why are most bank-issued stablecoins not retail products?

Retail distribution introduces higher compliance complexity, consumer-protection considerations, and broader fraud/AML exposure. Most banks start with institutional flows where onboarding is controlled and the value of 24/7 settlement is immediately measurable.

3. Which bank-issued stablecoins are most relevant for institutions in 2026?

JPM Coin is notable for institutional settlement inside a major bank network, while SG-FORGE’s EURCV/USDCV and Banking Circle’s EURI target regulated on-chain cash for markets and payments. Regional models like COPW matter when local currency rails are the priority.

4. Do bank-issued stablecoins replace USDC or USDT?

Not broadly in 2026. Bank-issued tokens tend to solve specific settlement and treasury problems inside defined networks, while USDC/USDT dominate general liquidity, exchange rails, and cross-chain circulation.

5. What should teams evaluate before adopting a bank-issued stablecoin?

Start with: legal structure, redemption rights, reserve or deposit treatment, onboarding/whitelisting, chain/network governance, operational hours, compliance tooling, and real liquidity on the venues you use. If any of those are unclear, the token will not scale inside a real treasury or payments stack.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}