Table of Contents

Algorithmic stablecoins are a fascinating, if controversial, corner of the crypto world. At their core, they're designed to hold a steady value—usually pegged to $1—but they do it without a vault full of cash or bonds to back them up.

Instead of relying on traditional reserves, these stablecoins use sophisticated algorithms and smart contracts to automatically control their own money supply. Think of it as a central bank's monetary policy, but running entirely on code, with no humans pulling the levers.

The Quest For a Truly Decentralized Dollar

To really get why someone would even try to build something so complex, you first have to look at the more common types of stablecoins, like USDT (Tether) and USDC (USD Coin). These are backed 1:1 by real-world assets, mostly cash and U.S. Treasury bills, stashed away in actual bank accounts. While this makes them incredibly stable, it also introduces a single point of failure and requires you to trust the company holding the money.

Algorithmic stablecoins emerged from a desire to cut out that middleman. The big idea was to create a stable currency that was both truly decentralized and highly capital-efficient, meaning it wouldn’t need to lock up billions in collateral just to operate.

Why Choose Algorithms Over Assets?

The drive to build these systems comes straight from the core crypto playbook. Developers and users who gravitate toward these models are usually chasing a few key ideals:

- Censorship Resistance: With no centralized bank accounts to freeze, a purely algorithmic stablecoin is, in theory, safe from government or corporate interference.

- Capital Efficiency: Instead of needing a dollar in a bank for every stablecoin in circulation, these systems use code to manage the peg. That frees up a massive amount of capital that can be put to work elsewhere in DeFi.

- Scalability: An algorithmic model can, again in theory, expand its supply to meet any level of demand without having to go out and buy an equivalent amount of real-world assets.

The ultimate goal is to create a stable medium of exchange that inherits the core properties of cryptocurrencies like Bitcoin—decentralization and permissionless access—while eliminating price volatility.

Of course, this vision comes with a mountain of risk and a history of spectacular failures. The automated market responses these coins use are deeply rooted in the principles of algorithmic trading. For a primer on the basics, you can check out our guide on how stablecoins work.

For a clearer picture, let's quickly compare the two approaches.

Algorithmic vs. Collateralized Stablecoins At a Glance

This table breaks down the fundamental differences between stablecoins that run on code versus those backed by assets.

| Feature | Algorithmic Stablecoins | Collateralized Stablecoins (Fiat & Crypto-Backed) |

|---|---|---|

| Peg Mechanism | Supply adjusted via algorithms and smart contracts. | Backed 1:1 by reserves like USD, T-bills, or other cryptos. |

| Centralization | Highly decentralized; no central custodian. | Centralized; relies on a trusted entity to hold collateral. |

| Capital Efficiency | Very high; does not require locked-up collateral. | Low; requires over-collateralization or 1:1 backing. |

| Censorship Risk | Low; no central assets to freeze or seize. | High; reserves can be frozen by banks or governments. |

| Stability Risk | High; prone to "death spirals" if confidence is lost. | Generally high stability, but has counterparty risk. |

As you can see, the trade-offs are significant. One path prioritizes decentralization and efficiency, while the other prioritizes trust and proven stability.

Despite their ambitious designs, algorithmic stablecoins are a tiny slice of the overall market. They represent a niche segment within the $227 billion+ stablecoin market as of early 2025, with their combined market cap hovering at just over $500 million.

The catastrophic collapse of Terra's UST in 2022, which wiped out over $60 billion in value, dealt a massive blow to confidence in purely algorithmic models and has kept most investors on the sidelines ever since.

How Algorithmic Stablecoins Actually Work

At their core, all algorithmic stablecoins are playing a game with supply and demand. The goal is simple: keep the price pinned to a specific value, usually $1. To do this, the protocol has to act like a central bank, automatically adjusting how many coins are in circulation.

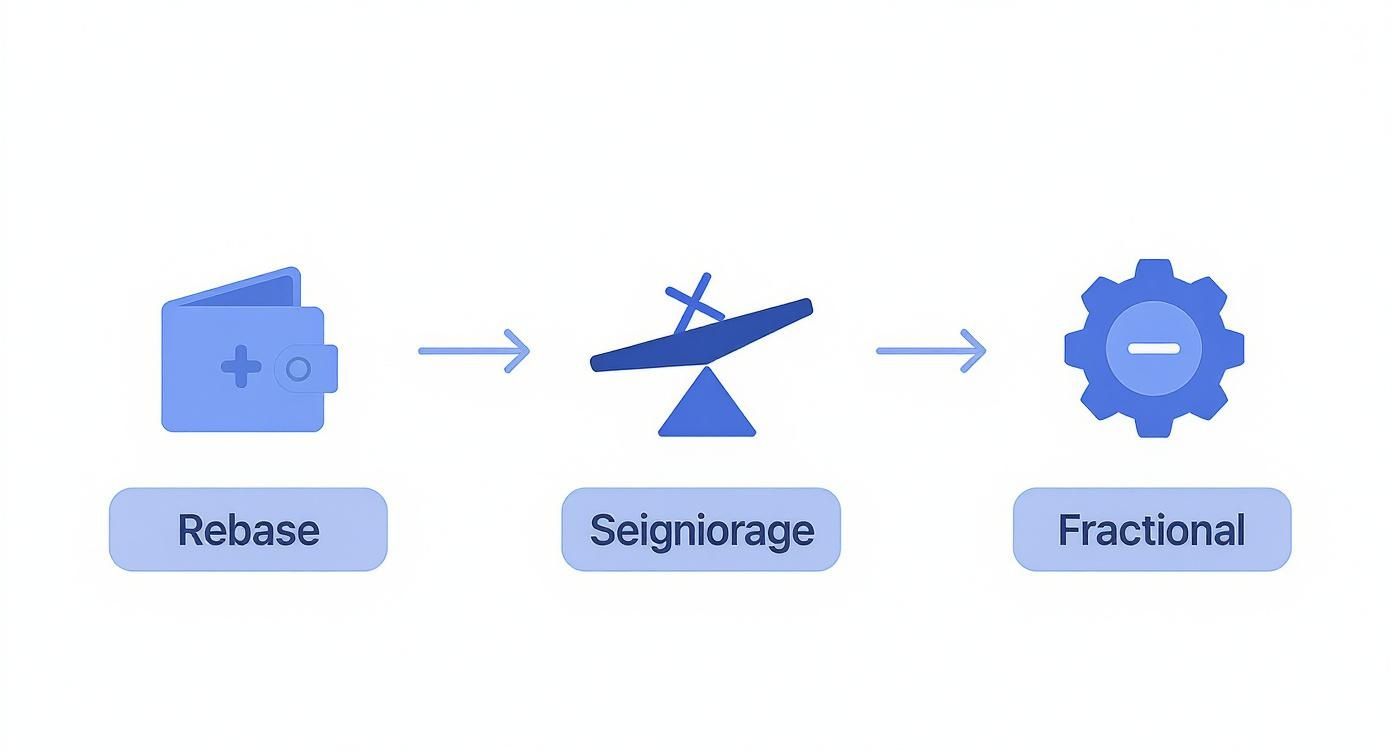

When the price nudges above $1, the system needs to create more coins to bring it back down. If the price slips below $1, it has to pull coins out of circulation to create scarcity and push the value back up. It’s this constant balancing act that defines them, but not all protocols go about it the same way. We can boil the designs down to three main types.

Rebase: The Elastic Money Supply

The most straightforward design is the rebase model. Think of the total supply of the coin as a single pizza. Every holder owns a slice. The size of the entire pizza changes based on demand, but your slice always represents the same percentage of the whole pie.

A rebase mechanism works by directly changing the number of coins in every single wallet.

- When Price > $1: The protocol triggers a “positive rebase.” It mints new coins and distributes them proportionally to everyone. If you held 100 coins, you might wake up to find 102 in your wallet. The total value of your holdings stays about the same, as the price of each individual coin is nudged back toward $1.

- When Price < $1: The opposite happens in a “negative rebase.” The protocol burns a portion of the coins from every wallet. Your 100 coins might become 98. The idea is that with fewer coins in circulation, each one becomes more scarce and, therefore, more valuable.

The key thing to remember is that while your balance changes, your share of the total supply doesn't. This can be jarring for newcomers who see their coin count fluctuating daily. To dig deeper, you can learn more about how rebase tokens function in our dedicated guide.

Seigniorage: The Two-Token Seesaw

The next major design is the seigniorage model, which uses a more complex two-token system. Picture a financial seesaw. On one end is the stablecoin, and on the other is a second, highly volatile token—often called a "share" or "governance" token.

This second token is designed to absorb the price shocks for the stablecoin. Here’s how they work together to defend the peg.

When the Stablecoin Price > $1:

The protocol mints new stablecoins to increase the supply. It often gives these newly created coins to people who are staking the volatile share token, rewarding them for supporting the network. This new supply helps push the price back down to $1.

When the Stablecoin Price < $1:

This is where it gets clever. The protocol creates an arbitrage incentive. It lets users buy "bonds" or "coupons" using the de-pegged stablecoin, but at a discount. These bonds promise to be redeemable for one full stablecoin later on, but only after the price has recovered.

At the same time, the system might mint and sell more of its volatile share token, using the money to buy stablecoins off the market and burn them. People holding the share token are essentially placing a bet on the protocol’s future success. They absorb the pain when things go wrong but reap the rewards when the system expands. The infamous Terra/Luna ecosystem was a prime example of this model.

Fractional-Algorithmic: The Hybrid Engine

Finally, we have fractional-algorithmic stablecoins. This model is a hybrid that tries to get the best of both worlds: the safety of collateral-backing and the capital efficiency of pure algorithms. It’s like a hybrid car that runs on both a gas engine (the collateral) and an electric motor (the algorithm).

With this setup, the stablecoin is only partially backed by assets like USDC or ETH. The rest of its value is propped up by the protocol's own governance token, much like in a seigniorage system.

The magic is in its dynamic collateral ratio (CR). The protocol is always watching the market to gauge confidence.

- When demand is high and the stablecoin is trading at or above its peg, the protocol can lower the CR. This means fewer real assets are needed to mint new stablecoins, making the whole system more efficient.

- When demand falls and the peg is under threat, the protocol increases the CR. This requires more hard collateral to be locked up, which is meant to reassure the market that the stablecoin is securely backed.

This hybrid approach hopes to build a more resilient system—one that can survive a market downturn better than a purely algorithmic model but remains more decentralized and efficient than a fully collateralized one. Each of these designs represents a bold experiment in the quest to create a truly independent, stable digital currency.

Theory is one thing, but seeing how these algorithmic stablecoin models actually behave in the wild is where the real learning happens. The history of these protocols is a story of bold experiments, with each design trying a different recipe for achieving a decentralized peg.

Let's dive into some real-world examples to see how these mechanisms perform under pressure and understand the trade-offs each one makes.

Rebase Model Spotlight: Ampleforth (AMPL)

The rebase model is probably the most straightforward approach to managing supply, and no project demonstrates it better than Ampleforth (AMPL). Launched back in 2019, AMPL’s big idea was to be a non-dilutive currency by directly adjusting its total supply every single day based on price.

You can think of it as an "elastic" currency. Every 24 hours, the Ampleforth protocol looks at the average price of AMPL.

- If AMPL is trading above $1.06, the protocol kicks off a positive rebase, and everyone holding AMPL suddenly has more tokens in their wallet.

- If the price dips below $0.96, a negative rebase happens, reducing the token count for every single holder.

The mechanism itself is impartial—your slice of the total AMPL pie never changes. What does change is your wallet balance. It's an attempt to create a stable unit of account that’s separate from its market price, but watching your token count go up and down can be a pretty strange experience for most people.

Seigniorage Model Case Study: Terra Classic (USTC)

You can't talk about algorithmic stablecoins without talking about the most famous—and infamous—seigniorage model: Terra Classic, which you probably remember as Terra (UST). The protocol relied on a two-token dance to keep its peg, using the stablecoin UST and its volatile sibling, LUNA.

The whole system was built on a mint-and-burn seesaw.

Users could always swap 1 UST for exactly $1 worth of LUNA, and vice versa. This created a powerful arbitrage loop that was supposed to keep UST locked to the dollar. If UST’s price slipped to $0.99, a trader could scoop it up on the cheap, swap it for $1 of LUNA, and instantly make a profit. That buying pressure was designed to push UST’s price right back up.

This elegant mechanism worked incredibly well for a while, especially in bull markets. It helped UST swell to an $18 billion market cap. But it also created a dangerously reflexive loop. Faith in UST was completely tied to the price of LUNA.

When the market took a nosedive in May 2022 and UST de-pegged, it triggered the infamous "death spiral." Panicked users rushed to redeem their UST for LUNA, forcing the protocol to mint billions of new LUNA tokens. This absolutely cratered LUNA's price, which in turn destroyed any remaining confidence in UST. The collapse wiped out over $40 billion in value and stands as the ultimate cautionary tale about the risks baked into pure seigniorage designs.

Fractional-Algorithmic In Practice: Frax Finance (FRAX)

Learning from the spectacular failures of purely algorithmic models, Frax Finance (FRAX) came along with a hybrid, or "fractional-algorithmic," design. The goal was to find a middle ground—to get the capital efficiency of an algorithm but with the safety net of hard collateral. FRAX is partially backed by real assets and partially stabilized by an algorithm.

Its secret sauce is a dynamic Collateral Ratio (CR), which shifts depending on how the market feels about FRAX.

- When FRAX trades above $1, the protocol lowers the CR. This means less collateral is needed to mint new FRAX, making the system more efficient.

- When FRAX trades below $1, the protocol raises the CR, demanding more collateral backing for each token. This helps calm the market by proving the stablecoin is well-supported by tangible assets.

This hybrid approach makes FRAX more resilient than its predecessors. Still, while it's an improvement, it does rely on trust in its algorithmic side. This is what sets it apart from stablecoins that are fully backed by collateral. If you're curious about those, our guide on how crypto-collateralized stablecoins work is a great place to start.

To help visualize these differences, here’s a quick breakdown of the three core designs.

Key Algorithmic Stablecoin Protocol Designs

| Model Type | Peg Mechanism Explained | Key Protocol Example | Primary Risk Factor |

|---|---|---|---|

| Rebase | The total token supply expands or contracts across all wallets to push the market price back towards the peg. | Ampleforth (AMPL) | Highly pro-cyclical and difficult for users to grasp, as wallet balances change constantly. |

| Seigniorage Shares | A two-token system where a volatile token is minted or burned to absorb price fluctuations of the stablecoin via arbitrage. | Terra Classic (USTC) | The infamous "death spiral," where a loss of confidence can cause both tokens to collapse simultaneously. |

| Fractional-Algorithmic | A hybrid approach that combines partial collateral backing with seigniorage mechanics to maintain the peg. | Frax Finance (FRAX) | Still exposed to bank-run scenarios if trust in the algorithmic component falters during market stress. |

Each of these protocols marks a major chapter in the evolution of decentralized money. They've given us invaluable lessons on what works—and what spectacularly doesn't—in the ongoing search for a truly stable and independent digital dollar.

The Risks and Infamous Failures

The dream of a truly decentralized, capital-efficient stablecoin is one of crypto’s holy grails. But the road to building one is paved with spectacular blow-ups. It turns out that the very mechanics giving algorithmic stablecoins their theoretical edge also open them up to unique and catastrophic vulnerabilities.

Without a safety net of real-world collateral, these protocols are built on a fragile tripod of game theory, market sentiment, and raw code. When one of those legs gives out, the whole structure comes crashing down.

The history of these assets is written as much in their collapses as in their innovations. Understanding what can go wrong isn't just a good idea—it's absolutely essential for anyone venturing into this corner of the market.

This chart gives you a quick visual recap of the main designs we've been talking about.

Whether it’s the elastic supply of a Rebase model or the dual-token dance of a Seigniorage system, each is a different attempt at the same problem, and each carries its own distinct baggage of risk.

The Terra UST Death Spiral: A Case Study

Nothing illustrates the inherent dangers of algorithmic stablecoins better than the implosion of Terra’s UST in May 2022. For a while, UST was the golden child of the seigniorage model, swelling to an $18 billion market cap and becoming the foundation of a booming DeFi ecosystem. Its stability was entirely propped up by an elegant arbitrage relationship with its sister token, LUNA.

The idea was simple enough: users could always burn 1 UST to mint $1 worth of LUNA, or vice-versa. This mechanism created a powerful financial incentive for traders to step in and defend the peg. But this beautiful theory hid a fatal flaw. The entire system was reflexive—UST’s value was backed by faith in LUNA, and LUNA’s value was derived from the growth of UST. It was a house of cards.

The moment of truth came when a few large, coordinated withdrawals rocked the network during a time of intense market fear. UST slipped just below $1. That tiny crack was all it took. A wave of panic set in as users scrambled to redeem their UST for LUNA. To meet this demand, the protocol was forced to mint astronomical amounts of new LUNA, flooding the market and cratering its price.

This triggered the now-infamous "death spiral." As the LUNA price collapsed, it took exponentially more LUNA to redeem one UST, leading to hyperinflation. Confidence evaporated. More people fled UST, which forced the protocol to mint even more LUNA. Within a few days, the self-reinforcing feedback loop vaporized over $40 billion in value, sending shockwaves across the entire crypto industry.

Categorizing the Core Risks

The Terra collapse was the biggest, but it was far from the first. Countless algorithmic stablecoins have failed, usually because of the same underlying weaknesses. We can really boil the primary risks down to three main categories.

- Reflexivity and Bank Runs: This is the "death spiral" risk in a nutshell. These systems run on confidence. Once that trust is broken and the peg starts to wobble, a classic bank run can trigger a self-perpetuating collapse that's nearly impossible to stop.

- Oracle Manipulation: Algo-stables depend on oracles—third-party data feeds that tell the protocol what assets are worth in the real world. If an attacker can corrupt that data feed, they can trick the protocol into making bad decisions, like issuing unbacked currency or accepting worthless collateral. Even glitches can be disastrous, a risk that affects even fully-backed coins, as highlighted in a reported incident involving a potential $300 trillion stablecoin glitch from Paxos.

- Governance Attacks: In many of these systems, token holders get to vote on protocol rules. An attacker with deep pockets could accumulate enough governance tokens to pass a vote that benefits them at everyone else's expense, like changing collateral requirements or minting rules to their advantage.

Many critics have pointed out the uncomfortable similarities between some of these failed projects and a classic Ponzi Scheme. The Terra ecosystem’s own Anchor Protocol, for example, lured in billions by promising an unsustainable ~20% annual yield on UST deposits. This attracted enormous capital but ultimately just added fuel to the fire.

These failures are a brutal reminder that code isn't magic. In the face of pure market panic, even the most elegantly designed economic incentives can break.

The Future of Algorithmic Designs

After the spectacular collapses that rattled the crypto world, it’s tempting to dismiss algorithmic stablecoins as a failed experiment. But the vision of a truly decentralized and capital-efficient digital dollar is very much alive. Developers are going back to the drawing board, learning from the wreckage to build something stronger.

The biggest shift? A clear move away from purely uncollateralized designs. The market learned a brutal lesson: trust is everything, and during a storm, you need a solid anchor. This has kickstarted a new wave of innovation centered around hybrid or fractional-algorithmic models.

These next-gen protocols are trying to get the best of both worlds. They mix the smarts of an algorithm with the security of real collateral, including both crypto and, more recently, Real-World Assets (RWAs). Think of it as giving the algorithm a solid foundation to work from. By bringing in assets like tokenized U.S. Treasury bills, these new designs hope to be both decentralized and provably backed by tangible value.

A Shifting Regulatory Landscape

At the same time, regulators are finally starting to draw some lines. The Terra/UST implosion was a global wake-up call, forcing governments to confront the risks these assets pose. Now, lawmakers are actively trying to build frameworks that can protect consumers without killing innovation.

Future rules are likely to zero in on a few key areas:

- Reserve Transparency: Forcing any collateralized stablecoin to provide clear, verifiable proof of its reserves.

- Capital Requirements: Making issuers hold a certain amount of capital to soak up potential losses.

- Orderly Redemption: Creating clear guidelines for how people can cash out their stablecoins, especially when the market is panicking.

This push for regulatory clarity might feel like a headache for some projects, but it's a huge win for the ecosystem in the long run. It gives builders a clearer roadmap for creating compliant products and helps rebuild investor trust by setting up some much-needed guardrails.

The real challenge for both regulators and builders is finding that sweet spot—a system that captures the efficiency of algorithms while providing the stability and trust needed for mass adoption.

The Unwavering Pursuit of a Better Stablecoin

Even with all the setbacks, some of the brightest minds in DeFi are still obsessed with cracking the algorithmic code. Why bother? Because the prize is massive. A successful algorithmic stablecoin could offer a level of capital efficiency and decentralization that fully backed models can't touch. It would be a foundational piece for a more open and accessible global financial system.

This innovation is happening against the backdrop of a booming stablecoin market. The total market size is expected to hit around $300 billion in 2025, even with titans like USDT and USDC controlling over 90% of it. Some projections even see the market growing to between $500 billion and $750 billion in the near future, making the search for a better stablecoin model more urgent than ever. You can read more about the expanding stablecoin market in an analysis from J.P. Morgan Global Research.

So while the original dream of a purely algorithmic stablecoin might be on hold, its spirit lives on in these smarter, hybrid designs. As we look forward, you can read our detailed analysis on the future of stablecoins and how their role in the digital economy is changing. The future probably won’t be a winner-take-all fight, but a diverse landscape where different models—from fully collateralized to hybrid-algorithmic—coexist to meet different needs.

Common Questions About Algorithmic Stablecoins

It's natural to have questions when digging into something as intricate as algorithmic stablecoins. Their history is a fascinating mix of groundbreaking ideas and spectacular implosions. Let's tackle some of the most common questions to help clarify the concepts.

Are Algorithmic Stablecoins a Safe Investment?

That's the million-dollar question, isn't it? The honest answer is: it’s complicated. If we look at the track record, purely algorithmic designs have proven to be exceptionally risky. Their stability hinges entirely on market sentiment and intricate economic games, which can shatter under pressure. We all saw what happened with Terra/UST.

But the story doesn't end there. The newer, hybrid models that mix algorithmic mechanics with some real collateral backing (like FRAX) are a different breed. They're built to be tougher. While they're still not as straightforwardly "safe" as fully-backed coins like USDC, they're a massive step up from the first generation. Ultimately, safety is all about the specific design and how much actual collateral is in the vault.

What Exactly Is a 'Death Spiral'?

A "death spiral" is the nightmare scenario for algorithmic stablecoins, particularly the seigniorage models. It's a vicious, self-feeding cycle where a small crack in confidence quickly turns into a complete system collapse.

It usually unfolds like this:

- The Peg Wobbles: The stablecoin dips just below its $1 target, maybe to $0.99.

- The Rush for the Exits: Seeing the weakness, people get nervous and start cashing out their stablecoins for the system's volatile "share" token.

- The Share Token Gets Wrecked: To pay everyone out, the protocol has to mint a mountain of new share tokens, flooding the market and tanking their price.

- Game Over: As the share token’s value evaporates, everyone realizes the stablecoin has no meaningful backing left. The last bit of faith disappears, the bank run accelerates, and both tokens spiral toward zero.

This is the exact mechanism that incinerated over $40 billion when Terra's UST and LUNA collapsed in May 2022.

With So Much Risk, Why Bother With Them?

It's a fair point. Despite the dangers, the allure of algorithmic stablecoins comes down to two powerful ideas: true decentralization and capital efficiency. For many in the DeFi space, they represent the holy grail—a form of stable money completely free from the traditional banking system.

The core drive is to build a censorship-resistant stable asset. Since they don't depend on dollars sitting in a bank account, there's no central party that can freeze your funds or block a transaction. This offers a degree of financial freedom that collateralized stablecoins simply can't.

On top of that, they don't require locking away billions of dollars in idle reserves. That capital can be put to work elsewhere in DeFi, making the whole ecosystem more dynamic and, in theory, more scalable.

Can Decentralized Stablecoins Be Frozen?

This gets to the heart of the centralization vs. decentralization debate. The power to freeze assets is a hallmark of centralized control, something most algorithmic designs are built to resist.

- Centralized Stablecoins (USDT, USDC): Absolutely. The companies behind them work with law enforcement and can blacklist addresses, freezing funds instantly. It’s a core part of their compliance model.

- Decentralized Stablecoins (DAI, FRAX): It's a different story. These protocols are run by code and governed by a distributed community. There's no single "off" switch. While a community governance vote could theoretically target an address, it's a public, messy, and much more difficult process.

For users who prioritize censorship resistance above all else, this inability to be frozen is the entire point.

At Stablecoin Insider, we provide the in-depth analysis you need to understand the evolving world of digital currencies. From protocol mechanics to regulatory shifts, stay ahead of the curve with our expert coverage. https://stablecoininsider.com

{kind=link}