Table of Contents

In practice, “yield-bearing stablecoin” usually means one of two things:

- A stablecoin wrapper that accrues yield (you hold a token that represents a claim on an underlying stablecoin plus interest), or

- A stable-value token backed by cash-like assets (often short-term government debt exposure packaged into a token).

If your goal is 4–8% in 2026, the most reliable approach is not chasing a single magic token, but building a small, controlled set of yield-bearing tokens with clear yield sources, strong redemption mechanics, and a monitoring routine.

Key Takeaways

- Yield comes from cash-like backing, borrow demand, or crypto market structure, and the risk profile changes with the yield source.

- Many “yield-bearing stablecoins” are receipt tokens (they represent a deposit position). Your outcome depends on the protocol’s health and parameters.

- Treat 4–8% as a portfolio target. A blended approach is often more stable than concentrating in one token.

- Your setup should prioritize: self-custody hygiene, redemption clarity, smart contract risk awareness, and liquidity planning.

- Passive income is only “passive” if you still do basic monitoring (rates, peg behavior, protocol changes, and liquidity).

What Makes A Yield-Bearing Stablecoin “Best” For 2026

Before picking tokens, align the choice with a selection checklist:

Yield Quality

- Cashflow-based: backed by off-chain cash instruments or borrower interest.

- Incentive-heavy: boosted by rewards that can end quickly.

- Market-structure-based: tied to funding/basis conditions that can reverse.

Redemption And Liquidity

- Can you exit quickly and predictably?

- Is redemption direct, or do you rely on secondary market liquidity?

Operational Complexity

- Can you explain the yield source in one sentence?

- Can you verify where your funds sit (protocol position, vault share, receipt token)?

Risk Surface

- Smart contract risk (code + upgrades)

- Governance risk (parameters can change)

- Custody / venue risk (if strategy depends on centralized exchanges)

- Peg and liquidity risk (can the token deviate from $1 in stress?)

The Best Yield-Bearing Stablecoin Tokens To Know In 2026

1) sDAI (Savings DAI)

What It Is

sDAI is a yield-accruing wrapper around DAI.

Holding sDAI represents a claim on DAI deposited into Maker’s savings mechanism.

Where The Yield Comes From

Primarily from Maker system revenues and policy-set savings rates. The rate can change over time.

How You Earn Passive Income

You swap DAI into sDAI (or mint sDAI via the official flow), and your sDAI position accrues value relative to DAI.

How To Set It Up (Practical Steps)

Choose a supported chain where sDAI is active (often Ethereum mainnet and select L2s).

- Acquire DAI from a reputable venue and move it to your wallet.

- Convert DAI → sDAI using a trusted interface.

- Hold sDAI in your wallet. You do not need to “claim” in many designs; the value accrues automatically.

Main Risks To Understand

- Governance/policy risk (rates and parameters can change)

- Smart contract and upgrade risks

- Liquidity risk during stress (price can deviate in secondary markets)

Best For

Users who want a relatively straightforward, on-chain savings wrapper with moderate complexity.

2) aUSDC and aUSDT (Aave Interest-Bearing Tokens)

What They Are

When you supply USDC or USDT to Aave, you receive aUSDC or aUSDT.

These receipt tokens represent your deposit plus accrued interest.

Where The Yield Comes From

Borrowers pay interest. Rates are utilization-driven and can move quickly.

How You Earn Passive Income

Deposit stablecoins into Aave. Your aToken balance typically increases over time (or the token is designed so the value accrues).

How To Set It Up (Practical Steps)

Pick the Aave deployment you will use (chain and market).

- Send USDC/USDT to your wallet on that chain.

- Supply USDC/USDT to Aave to receive aUSDC/aUSDT.

- Hold the aTokens.

Withdrawing converts back to the underlying stablecoin plus earned interest.

Main Risks To Understand

- Smart contract risk and protocol risk

- Oracle and liquidation dynamics (more relevant if you also borrow)

- Rate volatility (yield can compress significantly)

Best For

Users who want interest that is tied to real borrow demand and prefer mature money markets.

3) cUSDC (Compound Interest-Bearing Token)

What It Is

cUSDC is a receipt token from supplying USDC to Compound. It represents a claim on USDC plus interest.

Where The Yield Comes From

Borrow interest paid within the Compound market.

How You Earn Passive Income

Supply USDC and hold cUSDC. Over time, cUSDC becomes redeemable for more USDC than you initially deposited.

How To Set It Up (Practical Steps)

- Get USDC on the chain where Compound is active.

- Supply USDC into Compound to receive cUSDC.

- Hold cUSDC and redeem when you want to exit.

Main Risks To Understand

- Protocol and smart contract risk

- Market-specific risks (liquidity and parameter changes)

- Yield variability based on utilization

Best For

Users who want a long-established lending-market primitive and understand utilization-driven rates.

4) yvUSDC (Yearn Vault Shares For USDC Strategies)

What It Is

Yearn vault tokens (often prefixed with “yv”) represent shares in an automated strategy vault. yvUSDC typically reflects USDC deployed into a curated set of yield strategies.

Where The Yield Comes From

Strategy returns can combine lending, liquidity provision, and other on-chain sources depending on the vault.

How You Earn Passive Income

Deposit USDC, receive yvUSDC shares, and the share value increases as the vault earns.

How To Set It Up (Practical Steps)

- Acquire USDC and move it to your wallet on the vault’s chain.

- Deposit into the Yearn USDC vault to receive yvUSDC.

- Hold yvUSDC and withdraw when desired.

Main Risks To Understand

Strategy complexity risk (multiple legs can fail differently)

- Smart contract risk across multiple protocols the vault uses

- Liquidity and slippage when exiting in certain conditions

Best For

Users comfortable with “delegating” strategy execution to a vault and accepting additional complexity in exchange for yield optimization.

5) sUSDe (Ethena’s Yield-Acruing Token)

What It Is

sUSDe is a yield-accruing form of USDe. It is commonly associated with yield that can be influenced by derivatives and hedging mechanics.

Where The Yield Comes From

Protocol revenue that may be linked to market structure (for example, derivatives funding/basis dynamics) and other sources depending on how the system is designed at the time.

How You Earn Passive Income

You hold sUSDe rather than USDe, and the position accrues yield according to the protocol’s distribution mechanics.

How To Set It Up (Practical Steps)

Acquire USDe (or follow the protocol’s conversion path) on the supported chain.

- Convert USDe → sUSDe through a trusted interface.

- Hold sUSDe; convert back to USDe when exiting.

Main Risks To Understand (Higher Than The Options Above)

- Market-structure risk (yields can compress or reverse)

- Protocol risk and smart contract risk

- Operational dependencies if the design relies on external venues/liquidity

Best For

A limited “satellite” sleeve for advanced users who explicitly accept higher complexity and tighter monitoring requirements.

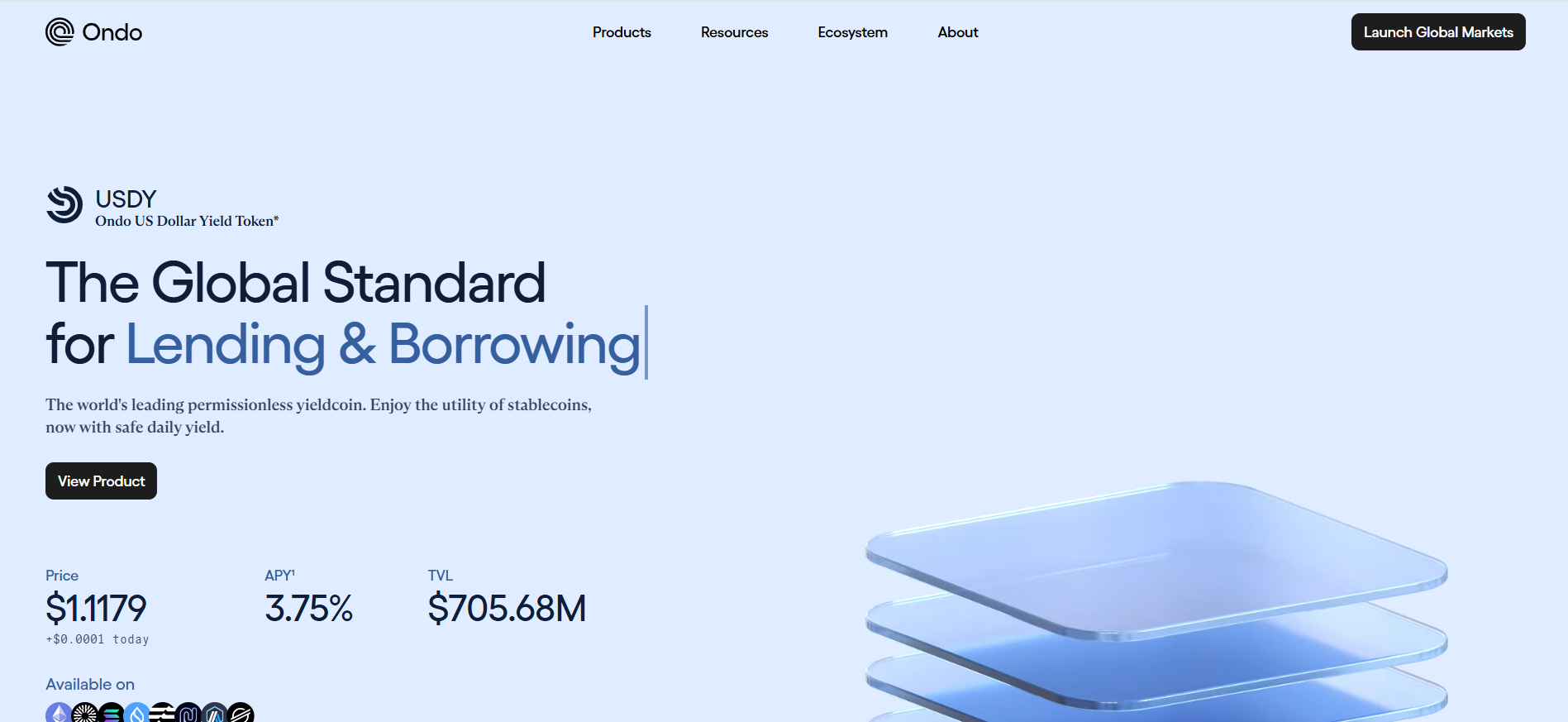

6) USDY (Yield-Bearing Stable-Value Token Linked To U.S. Treasury Yield)

What It Is

USDY is a yield-bearing stable-value token design that aims to pass through cash-like yield tied to short-duration government-debt style exposure through an issuance structure.

Where The Yield Comes From

Primarily cash-like, short-duration instruments (structure-dependent). In many such designs, yield is delivered via token mechanics rather than a separate interest payment.

How You Earn Passive Income

Hold USDY under the token’s accrual model. Depending on design, the yield may appear as a changing exchange rate, rebasing, or another mechanism.

How To Set It Up (Practical Steps)

Confirm eligibility and transfer constraints (some treasury-linked tokens use allowlists).

- Acquire USDY through a compliant route.

- Hold in your wallet and follow the accrual mechanics for accounting.

Main Risks To Understand

- Transfer restrictions / eligibility constraints

- Issuer and structure risk (how backing, custody, and redemptions work)

- Secondary liquidity risk (exiting may depend on venue liquidity)

Best For

Users who want treasury-linked yield exposure in token form and can handle compliance constraints.

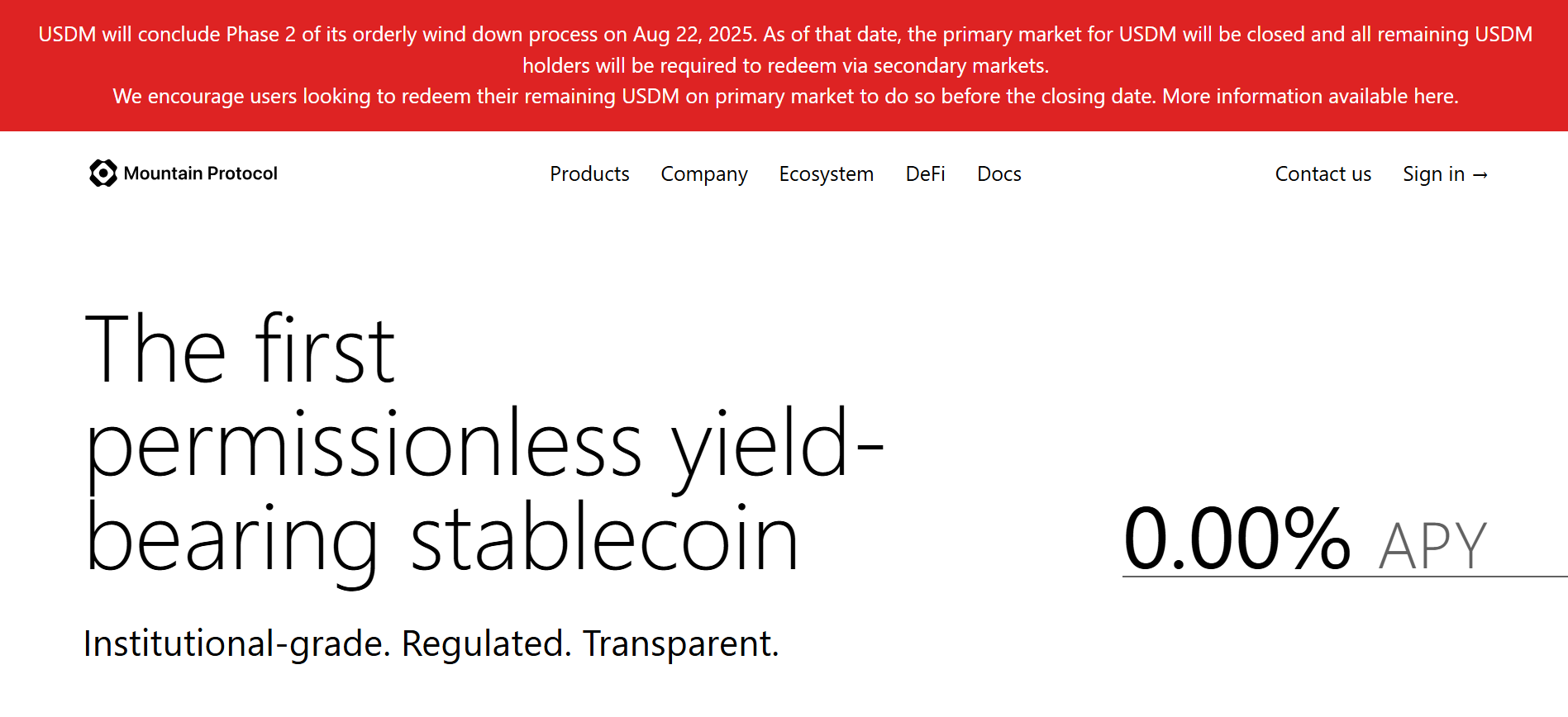

7) USDM (Yield-Bearing Stablecoin Style Token)

What It Is

USDM is widely discussed as a yield-bearing stablecoin structure designed to deliver yield via backing that targets cash-like returns.

Where The Yield Comes From

Typically cash-equivalent backing mechanics, depending on issuer design and redemption rules.

How You Earn Passive Income

Hold the token under its yield distribution or accrual model.

How To Set It Up (Practical Steps)

- Confirm supported chains and liquidity venues.

- Acquire USDM via a reputable route.

- Hold in your wallet and track the yield model for your records.

Main Risks To Understand

- Issuer and custody structure risk

- Redemption conditions and liquidity during market stress

- Token mechanics (how yield is reflected and whether it impacts accounting)

Best For

Users seeking a stable-value token whose yield is designed to come from cash-like backing rather than DeFi utilization.

8) “Lending Receipt Tokens” Beyond Aave And Compound (General Class)

Depending on chain and market, you may encounter other interest-bearing receipt tokens (from lending protocols, app-specific savings products, or chain-native money markets). The evaluation method is consistent:

- Who are the borrowers?

- What determines the rate?

- How quickly can you exit?

- What is the protocol’s track record and risk controls?

This is not a single token, but it is an important bucket because many 4–8% portfolios use more than one money market to diversify protocol risk.

How To Set Up A 4–8% Yield-Bearing Stablecoin Portfolio In 2026

Step 1: Choose Your “Core + Satellite” Structure

A professional structure for targeting 4–8% often looks like this:

Core (Lower Complexity, Rate-Linked)

- Treasury-linked yield tokens and/or simpler on-chain savings wrappers

Satellite (Utilization-Driven Yield)

- Lending receipt tokens from mature money markets (aUSDC, aUSDT, cUSDC)

Optional High-Yield Sleeve (Highest Monitoring Requirement)

- Higher complexity designs such as sUSDe, sized conservatively

This structure is designed to keep your portfolio from being dominated by one failure mode.

Step 2: Pick Your Chains And Reduce Operational Risk

To earn passive income reliably, most problems are operational, not theoretical.

Operational rules that reduce failure risk:

- Avoid unnecessary bridges; stay on one chain unless you have a clear reason.

- Keep a small buffer of native gas token for transactions.

- Use a hardware wallet if the position size is meaningful.

- Use separate wallets: one for long-term holds, one for daily activity.

Step 3: Execute The “Hold To Earn” Workflow (Generic, Repeatable)

Here is the standard workflow you will use for most yield-bearing tokens:

- Acquire the underlying stablecoin (USDC, USDT, DAI) on your chosen chain.

- Convert or deposit into the yield-bearing version (sDAI, aUSDC, cUSDC, yvUSDC, sUSDe).

- Verify the position (token balance, deposit receipt, or share value behavior).

- Hold for the intended horizon.

- Redeem back to the underlying stablecoin when needed.

If you cannot describe the conversion and redemption steps clearly, reduce size or pick a simpler token.

Step 4: Decide How You Will Measure Yield

Yield-bearing tokens pay you in different ways.

You should know which mechanism applies:

- Accruing exchange rate: your token redeems for more of the underlying over time

- Rebasing balance: your wallet balance increases over time

- Distributions: yield is paid as separate transfers (less common for pure on-chain wrappers)

Risk Management: How People Lose Money With “Stable” Yield

Passive income strategies fail when users ignore the predictable risk points:

1) Liquidity And Exit Risk

Even if something is designed to track $1, price can deviate in stress if market liquidity dries up. Your plan must include where you will exit and at what cost.

2) Smart Contract And Upgrade Risk

Receipt tokens depend on protocol code. Upgrades, admin keys, governance changes, or unexpected interactions can change risk rapidly.

3) Incentive Risk

If a big portion of the headline yield comes from rewards, the yield can fall quickly when incentives end. Plan for this by treating incentives as temporary.

4) Concentration Risk

Concentrating in one protocol, one chain, or one token concentrates failure modes. Diversification is not about chasing more tokens; it is about reducing single-point failures.

5) Market-Structure Risk (For Higher-Yield Designs)

If yield relies on market conditions (such as derivatives funding), the regime can change. This is why higher-yield tokens should usually be sized as satellites, not cores.

Practical Monitoring Routine (15 Minutes Per Week)

A simple routine keeps “passive” from becoming careless:

- Check current yield range vs your entry expectations (is it materially lower?)

- Check peg behavior and liquidity (are spreads widening?)

- Check protocol announcements (parameter changes, caps, new risks)

- Check your wallet security posture (approvals, hardware wallet status)

- Confirm you still have a clear redemption path

Quick Comparison Table (Decision Support)

| Token | Yield Mechanism | Complexity | Best Use | Primary Risk |

|---|---|---|---|---|

| sDAI | Savings wrapper accrual | Medium | Core / cash management | Governance + protocol risk |

| aUSDC / aUSDT | Lending receipt yield | Medium | Satellite yield | Rate volatility + protocol risk |

| cUSDC | Lending receipt yield | Medium | Satellite yield | Utilization swings + protocol risk |

| yvUSDC | Strategy vault shares | Higher | Yield optimization sleeve | Strategy complexity + multi-protocol risk |

| sUSDe | Protocol distribution/accrual | Highest | Small high-yield sleeve | Market-structure + operational dependencies |

| USDY | Treasury-linked accrual model | Medium | Core (eligibility-dependent) | Issuer/structure + transfer constraints |

| USDM | Cash-like yield design | Medium | Core (design-dependent) | Issuer/structure + redemption rules |

Conclusion

If you want yield-bearing stablecoins that can support a 4–8% portfolio target in 2026, focus on tokens with legible yield sources and predictable redemption mechanics.

For many holders, that means combining a simpler savings wrapper (such as sDAI) with mature lending receipt tokens (such as aUSDC/aUSDT and cUSDC) and using higher-complexity tokens (such as sUSDe or strategy vault shares like yvUSDC) only as carefully sized satellites.

Read Next:

- 2025 Stablecoin Year-End Report

- Best Chain for Stablecoin Micropayments in 2026

- Best Stablecoin On/Off-Ramps for 2026 Compared

FAQs:

1. What Is The Simplest Yield-Bearing Stablecoin To Hold?

A savings wrapper like sDAI or a large lending receipt token like aUSDC can be simpler to operate than strategy vaults, because the workflow is straightforward: convert/deposit, hold, redeem.

2. How Do I Actually Earn Passive Income From These Tokens?

You either (1) hold a token that accrues redeemable value over time, or (2) hold vault shares whose share price increases as the vault earns. Your “income” is usually realized when you redeem back to the underlying stablecoin.

3. Is 4–8% Guaranteed In 2026?

No. Yield changes with interest rates, borrow demand, incentives, and market conditions. A portfolio approach can target a band, but the result is not guaranteed.

4. Which Tokens Should Be “Core” Holdings?

Core holdings are usually the ones with the clearest yield source and redemption path. Many users treat cash-like or policy-based wrappers as core and lending receipts as satellites.

5. What Is The Biggest Mistake People Make?

They size positions based on headline APY rather than the redemption path and failure modes. Your exit plan matters as much as the yield.

6. How Do I Reduce Risk Without Giving Up All Yield?

Use a blended structure (core + satellite), diversify across one or two mature protocols, avoid unnecessary bridging, and keep higher-complexity tokens as a small sleeve.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}