Table of Contents

CREDITS: Dr. Rajiv Singhi, Co-Founder & Director, PayStreet Limited

Global trade finance runs on mature legal frameworks, most notably the International Chamber of Commerce (ICC) rulebooks UCP 600, URDG 758, and Incoterms 2020.

The problem is not the quality of the rules; it is the execution layer behind them. That execution layer remains slow, capital-intensive, and difficult for many firms to access, contributing to a persistent ~USD 2.5 trillion global trade finance gap.

Regulated stablecoins, combined with programmable settlement logic, cryptographic verification, and privacy-preserving compliance, create a practical way to modernize how trade instruments are executed without changing their legal foundations.

In other words, trade finance can move toward digital execution parity while keeping the same legal architecture.

Key Takeaways

- The ~USD 2.5 trillion trade finance gap is primarily an execution-layer issue, not a failure of trade rules.

- 80–90% of world trade still relies on letters of credit and guarantees, even though operational workflows remain slow.

- Stablecoin-enabled letters of credit can compress payment cycles from days to seconds through atomic settlement while keeping UCP 600 intact.

- Programmable collateral features (lock-ups/releases, haircuts, substitution, intraday reuse) reduce capital drag and improve balance-sheet efficiency.

- Zero-knowledge proofs support compliance and verification without exposing sensitive commercial data.

Background: Trade Finance Is Legally Advanced, Technically Constrained

Trade finance is governed by strong rulebooks that define how obligations should work and how risk should be allocated.

- UCP 600 standardises letters of credit

- URDG 758 governs demand guarantees

- Incoterms 2020 defines delivery and documentary milestones that shape payment conditions and risk transfer

On paper, this is a well-defined system with clear roles, responsibilities, and enforceable commitments.

In practice, the execution stack supporting these instruments remains constrained. Despite decades of refinement, 80–90% of world trade still relies on letters of credit and guarantees, while over 40% of SME trade finance requests are rejected.

Unmet demand stands at ~USD 2.5 trillion annually, driven by operational friction such as slow settlement, immobilised collateral, and duplicative compliance checks across intermediaries.

The result is a gap that persists even when the underlying trade is legitimate and economically sound.

The 7 Key Use Cases

Use Case 1: Stablecoins as the Digital “Cash Layer” of Trade Finance

Trade finance instruments already behave like software, they are conditional, state-based, and event-driven.

Stablecoins make it possible to express these constructs natively in code, allowing trade settlement to operate as a programmable execution workflow rather than a slow sequence of reconciliations.

This reframes stablecoins as a “cash layer” that can settle obligations once conditions are proven.

A trade-grade stablecoin is not merely a token; it is a multi-layer financial system. The base layers replicate controls found in banking infrastructure (custody, reserve backing, and compliance), while upper layers introduce programmability, privacy (via zero-knowledge proofs), and regulator-level oversight.

A key point is that these layers map directly to trade finance functions, which is why the approach can modernize execution without rewriting legal rulebooks.

It is an execution upgrade that aligns with how trade instruments already operate.

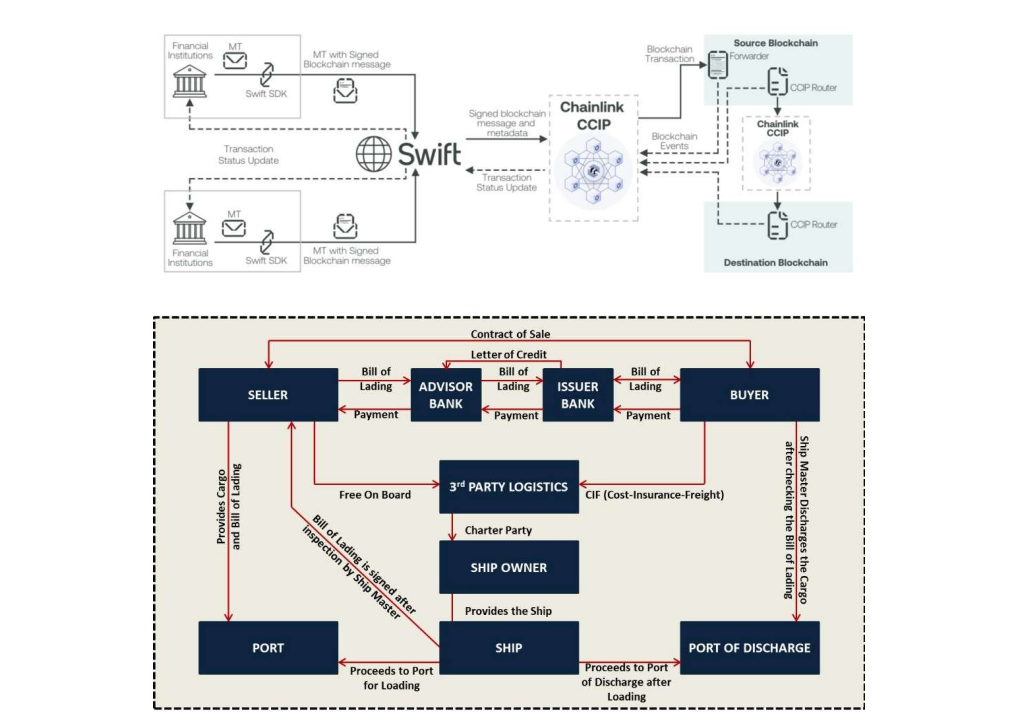

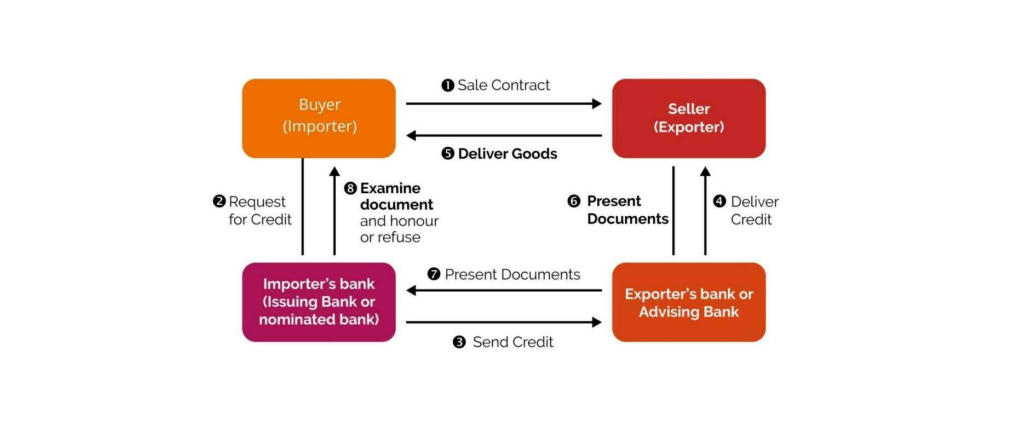

Use Case 2: Tokenised Letters of Credit With Functional Parity to UCP 600

Under UCP 600, a letter of credit is an independent, conditional payment obligation. A stablecoin-enabled LC keeps that legal structure intact while digitising execution.

The purpose is not to change the LC’s legal independence; it is to improve how documentary conditions are verified and how settlement occurs when those conditions are met.

In a stablecoin-enabled LC flow, stablecoins are locked in a programmable escrow at issuance. Documentary conditions that are aligned with Incoterms 2020 milestones, are verified cryptographically. Once compliant presentation is established, settlement occurs atomically, compressing payment cycles from days to seconds while leaving UCP 600 fully intact.

This turns LC settlement into an immediate execution outcome once compliance is proven, rather than a process that remains delayed by manual checks and operational handoffs.

Two practical implications follow from this structure:

- First, the LC can remain legally independent while being operationally faster and more deterministic.

- Second, the number of settlement “chokepoints” is reduced because the payment logic is executed at the same moment compliance is proven.

Use Case 3: Digital Demand Guarantees Under URDG 758 (Faster Invocation, Same Independence)

Demand guarantees are designed for immediacy and certainty, yet cross-border invocation today can be slow and capital-inefficient.

Stablecoin-backed guarantees address execution latency by using pre-funded, verifiable reserve pools and event-triggered execution, while preserving the legal characteristics that make guarantees effective.

In this model, collateral is locked upfront in a regulated stablecoin pool. A compliant demand (validated programmatically), triggers immediate beneficiary settlement.

The independence principle under URDG 758 is preserved; only execution speed and certainty improve. That distinction matters because the value of a demand guarantee depends on enforceable independence and predictable outcomes, not on procedural delay.

Operationally, pre-funding reduces ambiguity at the moment of invocation because funds are already locked and available. It also improves certainty for beneficiaries without changing the legal nature of the guarantee obligation.

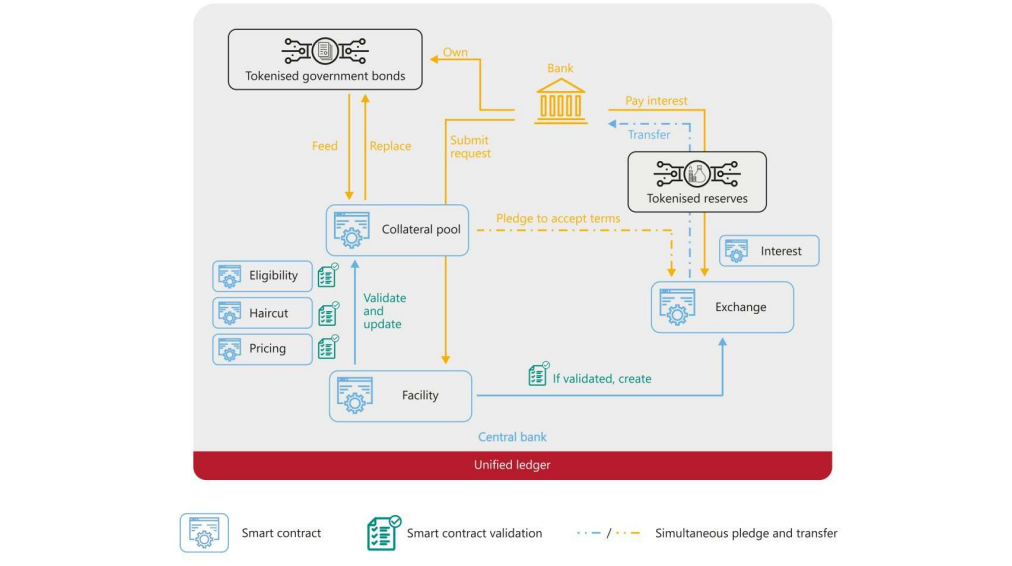

Use Case 4: Programmable Collateral and Liquidity (From Static to Dynamic)

Collateral inefficiency is a major contributor to the trade finance gap because capital often becomes immobilised in static, siloed balances.

Stablecoins enable collateral to behave as programmable liquidity: rule-based, reusable (where permitted), and responsive to defined events. This moves trade finance closer to modern collateral logic used in derivatives and repo markets.

Stablecoins enable:

- Programmable lock-ups and releases

- Automated haircuts

- Intraday liquidity reuse

- Real-time substitution

The collateral lifecycle shifts from static balances to dynamic, rule-based liquidity. Haircuts, substitutions, and releases can occur automatically, reducing capital drag and improving balance-sheet efficiency.

This is not about weakening controls; it is about implementing controls in code so that execution is timely and consistent. The result is improved liquidity management while maintaining disciplined collateral treatment.

Use Case 5: Privacy Without Opacity Using Zero-Knowledge Proofs

Public blockchains historically failed trade finance because trade requires confidentiality.

Trade finance workflows can involve sensitive pricing, counterparties, shipment details, and documentary data that cannot be exposed broadly without commercial and legal consequences.

The challenge is to support verification and compliance while protecting legitimate confidentiality needs.

Zero-knowledge proofs resolve this tension by allowing parties to prove:

- Sanctions compliance

- Reserve sufficiency

- Documentary conformity

Crucially, these proofs can be provided without revealing underlying commercial data, aligning with data-minimisation and bank-secrecy principles.

This makes privacy a designed property of the execution layer, rather than a reason to avoid digital settlement rails. It also supports regulator-level oversight without turning trade data into public information.

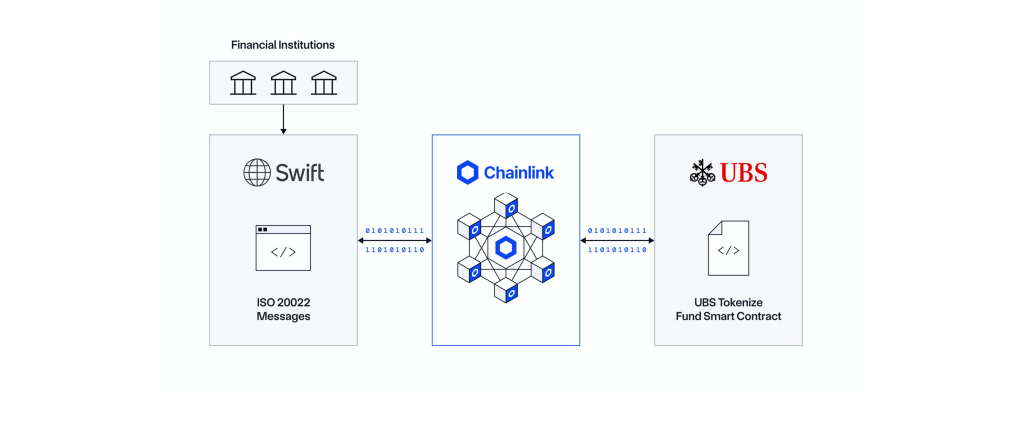

Use Case 6: Interoperability With Banks, SWIFT, and ISO-20022 Messaging

Stablecoin-based trade finance does not replace banks, SWIFT, or ISO-20022 messaging. It interoperates with them. That interoperability is central because trade finance is a network of institutions and processes, not a single system that can be swapped out.

A workable execution layer must fit into existing operational workflows.

In the interoperable model, existing bank systems generate trade events and messages, while stablecoins act as the settlement rail. This preserves institutional workflows while enabling real-time, atomic settlement once conditions are met. It also allows trade finance to modernize incrementally rather than requiring a full rebuild of existing infrastructure.

Use Case 7: Digital Execution Parity and the Next Evolution of ICC Trade Rules

ICC frameworks have historically evolved alongside commerce, from paper to electronic documents, and from domestic to global trade.

The next step is digital execution parity, not legal reinvention.

The goal is to maintain the legal foundations while enabling the execution layer to operate with modern speed, verification, and control.

Potential future enhancements include:

- Recognition of tokenised settlement rails

- Guidance on programmable escrows

- Digital invocation standards for guarantees

- Acceptance of cryptographic verification

These enhancements would not change what trade instruments are legally; they would clarify how modern execution methods can be recognized and standardized. Over time, that guidance can reduce uncertainty for institutions and increase consistency across implementations.

Conclusion

The global trade finance gap is not a failure of rules; it is a failure of execution.

Regulated stablecoins when combined with programmability, privacy, and interoperability, can offer a realistic path to faster settlement, lower capital costs, reduced rejection rates, and wider SME participation.

This is not about replacing trade finance; it is about re-platforming it onto an execution layer that matches the sophistication of its legal foundations.

Trade finance is not being disrupted, it is being re-platformed.

Read Next:

- 2025 Stablecoin Year-End Report

- 2025 Stablecoin Spending Report

- Who Is Winning the Stablecoin Infrastructure Race?

FAQs:

1. What is the trade finance gap, and what causes it?

Unmet demand is approximately ~USD 2.5 trillion annually, driven mainly by execution friction such as slow settlement, immobilised collateral, and duplicative compliance, rather than weak legal rules.

2. How can stablecoins act as trade finance infrastructure?

Trade instruments already behave like software (conditional, state-based, event-driven). Stablecoins allow those constructs to be expressed and executed natively in code as a digital settlement rail.

3. How does a stablecoin-enabled letter of credit remain consistent with UCP 600?

It preserves the LC as an independent, conditional payment obligation while digitising execution: stablecoins are locked in programmable escrow, conditions aligned with Incoterms 2020 milestones are verified cryptographically, and settlement can occur atomically.

4. What does “atomic settlement” mean for letters of credit?

It means settlement happens immediately once compliant presentation is proven, compressing settlement cycles from days to seconds while leaving the LC’s legal structure intact.

5. How do stablecoin-backed demand guarantees preserve URDG 758 principles?

Collateral is locked upfront in a regulated stablecoin pool, and a compliant demand validated programmatically triggers immediate settlement, while the URDG 758 independence principle remains intact.

6. Why are zero-knowledge proofs relevant for trade finance?

They allow proof of sanctions compliance, reserve sufficiency, and documentary conformity without exposing underlying commercial data, supporting privacy without sacrificing verification.

7. Do stablecoins replace SWIFT or ISO-20022 messaging?

No. The interoperable model keeps banks, SWIFT, and ISO-20022 messaging in place while using stablecoins as the settlement rail for real-time, atomic settlement.

Disclaimer:

This content is provided for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice; no material herein should be interpreted as a recommendation, endorsement, or solicitation to buy or sell any financial instrument, and readers should conduct their own independent research or consult a qualified professional.

{kind=link}