Table of Contents

Think of stablecoin yield as a high-tech savings account for your digital dollars. It’s a way to put your crypto to work, earning interest-like returns by lending it out or providing it to various financial protocols. Instead of letting your stablecoins sit idle, you can generate a steady stream of passive income.

The Foundation of Stablecoin Yield Farming

At its heart, stablecoin yield is simply the reward you get for providing capital where it's needed. This isn't a new concept. When you put money in a traditional savings account, the bank lends it out and gives you a tiny slice of the profit. Earning yield on stablecoins follows the same playbook, but with a crypto twist—often with fewer middlemen and potentially better returns.

You’re essentially letting others borrow your digital dollars to fuel the crypto economy. This capital is in constant demand. Traders need it for leveraged positions, and decentralized exchanges need it to function smoothly. By supplying this liquidity, you get paid. It's that simple.

This dynamic is a cornerstone of Decentralized Finance (DeFi), creating a more open financial system where the rewards you earn are a direct reflection of the market's demand for your funds.

How Does It Actually Work?

The real magic of stablecoin yield is in the different ways you can earn it. Each method has its own set of rules, risks, and rewards. Your stablecoins aren't just collecting digital dust; they become active participants in the financial ecosystem.

Here's a quick rundown of the most common yield-generating avenues:

Centralized Finance (CeFi) Lending: This is the most familiar path. You deposit your stablecoins on a centralized platform, like Nexo or BlockFi (historically), and they lend them out to big-money borrowers. You get a cut in the form of a fixed or variable interest rate.

Decentralized Finance (DeFi) Lending: Here, you skip the company and interact directly with a smart contract on the blockchain. You add your stablecoins to a lending pool where others can borrow from, and you earn interest directly from the borrowers. Our guide on stablecoin lending dives much deeper into how this works.

Providing Liquidity: You can also deposit your stablecoins into a liquidity pool on a decentralized exchange (DEX) like Uniswap or Curve. These pools are what allow traders to swap tokens instantly. As a liquidity provider, you earn a percentage of the trading fees every time a swap happens.

Each of these strategies turns your stable digital dollars into a productive asset. To help you see how they stack up, here’s a quick comparison.

Comparing Stablecoin Yield Generation Methods

To give you a clearer picture, this table breaks down the most common ways to earn yield on stablecoins, highlighting how they work, their typical APY ranges, and the main risks involved.

| Method | How It Works | Typical APY Range | Primary Risk |

|---|---|---|---|

| CeFi Lending | Deposit stablecoins on a centralized platform that lends them to institutional borrowers. | 2% - 8% | Counterparty Risk (the platform could fail or mismanage funds) |

| DeFi Lending | Supply stablecoins to a decentralized lending pool governed by smart contracts. | 3% - 15% | Smart Contract Risk (bugs or exploits in the code) |

| Liquidity Providing | Add stablecoins to a liquidity pool on a DEX to facilitate token swaps. | 5% - 25%+ | Impermanent Loss & Smart Contract Risk |

| Yield Aggregators | Use a protocol that automatically moves your funds to find the best yields. | 5% - 30%+ | Composability Risk (risk stacks up across multiple protocols) |

Choosing the right method depends entirely on your risk tolerance and how hands-on you want to be. While higher APYs are tempting, they almost always come with higher risks.

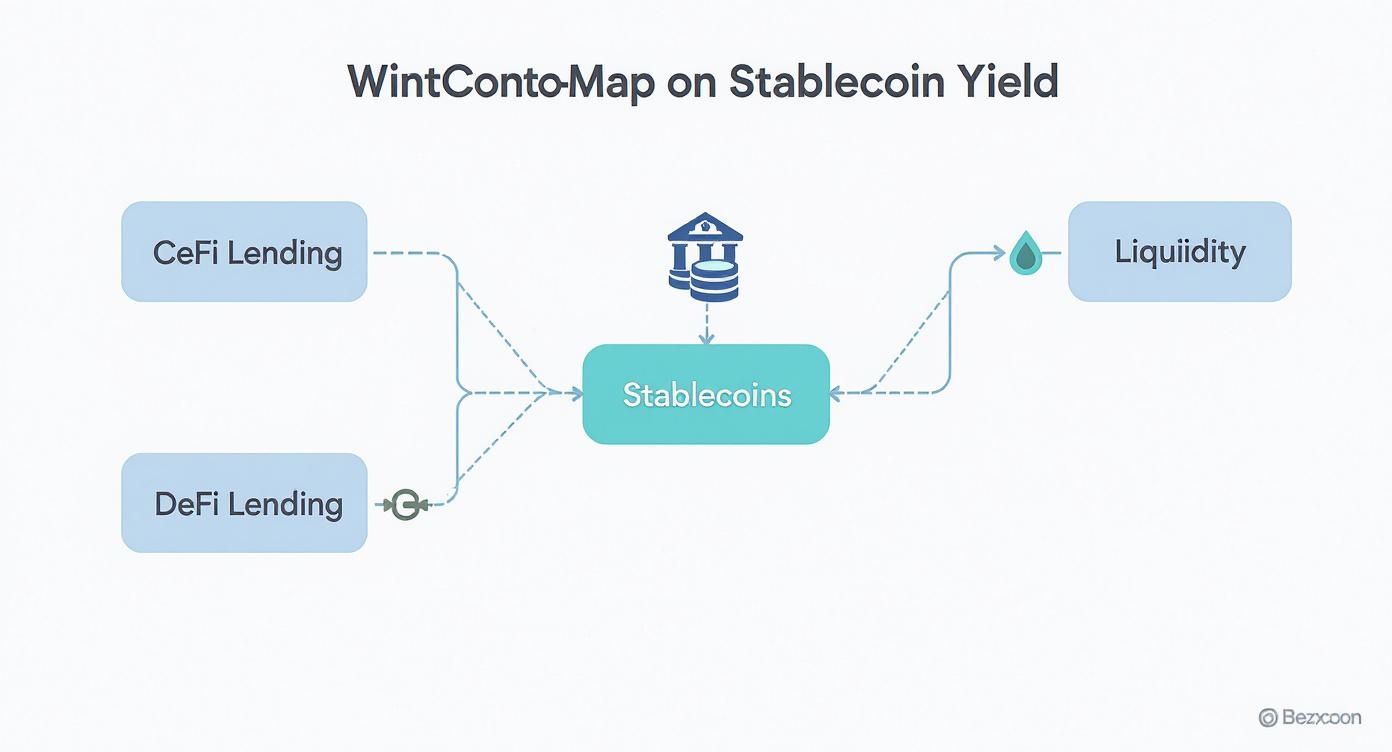

How Stablecoin Yield Is Actually Generated

Stablecoin yield doesn’t just materialize out of nowhere. It's a direct byproduct of real economic activity happening across the digital asset world. The returns you see are essentially a payment for providing capital—a valuable service that others are willing to pay for.

Think of it this way: your stablecoins are a resource. Whether someone needs them for borrowing, trading, or funding a project, you're the one supplying the fuel. To really get a handle on this, let's break down the main engines that crank out this yield. Each method is a bit like a different business model, but they all boil down to one simple idea: your money facilitates a transaction, and you get a cut of the profits.

CeFi Platforms: The Digital Bank Model

Centralized Finance (CeFi) platforms, like Nexo or BlockFi, function a lot like the bank down the street. When you deposit your stablecoins, they don't just sit in a digital vault collecting dust. The platform lends them out to other users and big institutional players who need capital for things like market-making or complex trading strategies.

Those borrowers pay interest on their loans, which is how the platform makes its money. A slice of that interest is then passed on to you as stablecoin yield. It’s a clean, straightforward model: you're the depositor, the platform acts as the bank, and other folks are the borrowers. The yield you get is your reward for providing the funds that make the whole system work.

This infographic lays out the core ways yield is generated, covering everything from centralized lending to decentralized protocols.

As you can see, whether it's through a company or a piece of code, your stablecoins are always put to work to earn a return.

DeFi Money Markets: Peer-to-Peer Lending, Reimagined

Decentralized Finance (DeFi) protocols like Aave or Compound essentially cut the bank out of the picture. Instead of a company managing everything, these platforms run on smart contracts—self-executing code on the blockchain that creates fully autonomous money markets.

It works like this:

- You supply your stablecoins into a shared lending pool.

- Borrowers can then take out loans directly from that pool, but they have to post other crypto assets as collateral first.

- The interest rate you earn isn't set by a committee; it’s determined by an algorithm based purely on supply and demand. If lots of people want to borrow, rates go up.

Your yield is paid directly from the interest those borrowers are paying. The smart contract handles everything automatically—matching lenders with borrowers, enforcing collateral rules, and distributing interest—making for a more transparent, peer-to-peer system.

The total value locked (TVL) in stablecoin-related DeFi protocols exceeded $265 billion by late 2025, underscoring the massive global demand for stablecoin-based yield products. This figure represents a substantial portion of the overall crypto market, with Tether (USDT) alone accounting for over $183 billion—roughly 62% of the total stablecoin market capitalization. You can explore more data on the scale of stablecoin markets at DeFiLlama.

Liquidity Provision: Fueling Decentralized Exchanges

Another powerful way to generate yield is by becoming a liquidity provider (LP) on a decentralized exchange (DEX) like Uniswap or Curve. DEXs don't have a central company matching buy and sell orders. Instead, they need massive pools of tokens to let users swap between different assets smoothly. That's where you come in.

By depositing your stablecoins into a liquidity pool (usually paired with another crypto asset), you're basically acting as a small-scale currency exchange. Your funds become the inventory that traders use to execute their swaps.

For providing this crucial service, you earn a percentage of the trading fees from that pool. Every time someone makes a trade using the liquidity you provided, a tiny fee is collected and split among all the LPs based on their share of the pool. This fee-based income is your direct reward for making the market run. A new, fascinating trend in this space involves tokenized real-world assets. If you're curious, you can learn more about how to use real-world assets to generate yield on stablecoins. This approach is exciting because it connects DeFi yields to tangible, off-chain value.

What Kind of APY Can You Realistically Expect?

When you start looking into stablecoin yields, the first question on your mind is probably, "Okay, but how much can I actually make?" The truth is, there's no single magic number. It's more of a spectrum, with your potential returns swinging based on everything from overall market mood to the specific strategies you pick.

Unlike a traditional savings account that might offer a fixed rate for a year, stablecoin yields are alive. They move with the pulse of the crypto economy. When the market is booming and traders are hungry to borrow stablecoins for leverage, you'll see lending rates climb. But during lulls, demand cools off, and those yields can dip. Your APY is a direct reflection of these real-time market forces.

This is why setting realistic expectations is your first line of defense. Chasing eye-popping, triple-digit APYs is often a shortcut to taking on way too much risk. Getting a feel for the typical return ranges will help you make much smarter, more sustainable decisions for your portfolio.

Typical APY Ranges by Strategy

The world of stablecoin yield isn't one-size-fits-all. The returns you can expect depend heavily on the risk and complexity of the strategy you’re using. It helps to think of it in tiers, where higher potential rewards almost always walk hand-in-hand with higher potential risks.

Here’s a general breakdown of what to expect:

Low-Risk (2% - 8% APY): This is the bread and butter. Think of lending blue-chip stablecoins like USDC or DAI on massive, battle-tested DeFi protocols like Aave or Compound. The yields are more modest, but they come from platforms with a long track record of security and billions of dollars in locked value.

Medium-Risk (5% - 15% APY): Here, we're talking about things like providing liquidity to stablecoin-to-stablecoin trading pairs on established exchanges like Curve. The risk creeps up a bit due to the mechanics of being a liquidity provider, but the returns from trading fees can be a nice step up.

High-Risk (15% - 30%+ APY): The highest yields are usually found in newer, less-proven protocols or through more complex strategies like "yield farming" that involve chasing extra token rewards. These opportunities come with significant smart contract risk and demand a lot more active management.

Even at the lower end of the spectrum, these ranges show exactly why stablecoins are so compelling. They often outperform what you'd find in a traditional high-yield savings account, offering a powerful way to earn passive income on your digital dollars.

Why Are Stablecoin Yields Often Higher?

If you're coming from the world of traditional finance, these APY numbers might seem too good to be true. The main reason for the difference comes down to two things: efficiency and demand.

DeFi protocols are incredibly lean. They run on code, without the massive overhead of office buildings, executive salaries, and legacy infrastructure. This means more of the value generated from lending and borrowing can flow directly back to the users providing the capital.

On top of that, the demand for stablecoins in the crypto market is relentless and operates 24/7. Traders, bots, and other protocols need constant access to liquidity, and they're willing to pay a premium for it. This creates a hyper-competitive and efficient market for capital that naturally drives up returns for lenders like you. Our detailed guide on how to earn APY on stablecoins dives much deeper into these mechanics.

Data consistently shows that stablecoin yield rates aren't just a flash in the pan; they can maintain attractive levels over time. Throughout much of 2023, for example, the ecosystem saw both stability and growth. Coinchange, a prominent platform, reported a yield rate of 7.51% for December 2023, which was the tenth straight month its rate stayed above 7%. At the same time, the DeFi Yield Index, which tracks higher-risk strategies, jumped to 10.50% in December. You can dive deeper into these stablecoin yield trends.

The Real Risks of Chasing Stablecoin Yield

It’s easy to get drawn in by the promise of high yields on stablecoins. But let's be crystal clear: earning stablecoin yield is never a risk-free ride. Behind every attractive annual percentage yield (APY) is a set of risks you need to understand.

Think of it this way: knowledge isn't about fear; it's about power. By learning to spot and weigh the different risks, you can make smarter decisions and protect your hard-earned capital. It’s like a sailor learning to read the weather—you can’t stop a storm, but you can certainly choose a safer harbor.

Let's dive into the main risks you'll face. Each one is a potential weak link in the chain that generates those returns.

H3: Smart Contract Risk: "The Code Is Law"

When you put your money into a Decentralized Finance (DeFi) protocol, you're not trusting a bank manager. You're trusting a chunk of code. This is Smart Contract Risk—the danger that a bug, a design flaw, or a simple oversight in the code could be found and exploited by a hacker.

This is without a doubt one of the most common ways people lose money in DeFi. Imagine a high-tech vault with a lock that has a tiny, unknown defect. In the world of crypto, hackers are constantly looking for those defects. A single successful exploit can drain a protocol of all its funds in minutes, with no way to get it back.

The history of DeFi is littered with these kinds of exploits, and even protocols with expensive security audits aren't completely immune.

H3: Counterparty Risk: Who Are You Trusting?

While DeFi tries to remove the human element, Centralized Finance (CeFi) platforms bring it right back to the forefront. Counterparty Risk is the chance that the company you've handed your stablecoins to will simply fail. This could be from bad business decisions, going bankrupt, outright fraud, or a major security breach on their end.

When you deposit your stablecoins on a platform like a centralized lender, you’re no longer in control of your assets. You become an unsecured creditor. If that company goes under—as we saw with Celsius and BlockFi—getting your money back involves a long, painful, and often fruitless legal process.

A crucial concept here is the risk-adjusted return, which forces you to ask if the reward is truly worth the danger. A 15% APY from some brand-new, unaudited protocol is a world away from a 5% APY on a platform that has stood the test of time.

H3: Peg Stability Risk: When $1 Isn't $1

The whole point of a stablecoin is that it stays pegged to $1. Peg Stability Risk is the threat that a stablecoin breaks that peg and starts trading for much less. When this happens, chaos often follows.

There are a couple of key reasons a peg can break:

- Algorithmic Spirals: We all remember TerraUSD (UST). Algorithmic stablecoins rely on complex economic models to hold their value. Under extreme market stress, those models can fail spectacularly, leading to a "death spiral."

- Shaky Reserves: For stablecoins backed by real-world assets, the peg is only as strong as the reserves. If those reserves are poorly managed, aren't actually there, or lose their value, confidence can evaporate, triggering a "bank run" that de-pegs the coin.

Even a temporary de-peg can cause huge losses, especially for people who panic-sell or get automatically liquidated from their positions. It's a foundational risk for any stablecoin strategy.

H3: Regulatory Risk: The Rules of the Game Can Change

The regulatory landscape for crypto and stablecoins is still a work in progress. Regulatory Risk is the chance that a new law, a government crackdown, or a change in policy could suddenly derail a yield platform or even a specific stablecoin.

A government could, for example, ban certain DeFi activities, hit platforms with tough new rules, or take action against a stablecoin issuer. The proposed "GENIUS Act" in the U.S. is a perfect example, as it aims to stop issuers from paying yield directly. Even an operational blunder, like the $300 trillion Paxos stablecoin glitch, can bring unwanted heat from regulators.

This risk is unpredictable and can pop up with almost no warning, making it tough to manage but absolutely essential to keep in mind.

To help you put all this into practice, here's a checklist to run through when you're sizing up a new opportunity.

Stablecoin Yield Risk Assessment Checklist

| Risk Category | Key Question to Ask | Red Flag Example |

|---|---|---|

| Smart Contract | How many independent security audits has the protocol had? Is the code open-source? | The protocol has no public audits, or the team is anonymous. |

| Counterparty | If it's a CeFi platform, are they transparent about their finances and operations? Where are they based? | The company refuses to provide proof of reserves or has a complex, opaque corporate structure. |

| Peg Stability | What backs this stablecoin? Is it cash, treasuries, or a volatile crypto asset? | The stablecoin is algorithmic and has a history of briefly de-pegging during market stress. |

| Regulatory | Is the platform operating in a clear regulatory jurisdiction, or is it in a legal gray area? | The project's founders publicly state they are "anti-regulation" or based in an offshore haven. |

| Overall | Is the APY unrealistically high compared to competitors? If so, why? | A new protocol offers 50% APY when the market average is 5%, without a clear reason for the difference. |

Running through these questions doesn't guarantee you'll never have a problem, but it dramatically improves your odds by forcing you to think critically instead of just chasing the highest number.

How to Find and Vet Safe Yield Opportunities

Knowing the risks is one thing, but actually putting that knowledge to work is what keeps your capital safe. To build a sustainable stablecoin yield strategy, you need a repeatable process for sniffing out solid opportunities. This isn't about finding some secret formula; it’s about developing a keen eye for quality and a healthy dose of skepticism for anything that looks too good to be true.

Think of yourself as a detective. Before you even think about deploying funds, your job is to gather the evidence, cross-reference your sources, and build a rock-solid case for why a particular platform or protocol deserves your trust. A few hours of due diligence upfront can save you from a world of hurt down the line. Let's build your playbook.

Check for Reputable Security Audits

The absolute first box to check for any DeFi protocol is a history of professional security audits. An audit is where a specialized firm pores over a protocol's smart contracts, hunting for bugs, vulnerabilities, and potential attack vectors. It’s like hiring a team of elite locksmiths to try and crack a new bank vault before it opens for business.

But remember, not all audits are created equal. You need to look for:

- Multiple Audits: One audit is good, but several audits from different, well-known firms like Trail of Bits, CertiK, or OpenZeppelin are far better.

- Public Reports: Trustworthy projects share their audit reports openly. Actually read them. Pay close attention to any critical issues that were flagged and confirm that the team has addressed them.

To truly vet yield opportunities, you have to appreciate the importance of security and know how to use high-quality smart contract audit tools. No audit can guarantee 100% safety, but a complete lack of them is a massive, blinking red flag.

Analyze Total Value Locked (TVL)

Total Value Locked (TVL) is a vital metric that tells you how much money users have collectively deposited into a DeFi protocol. Think of it as a barometer for market trust and confidence. A high and steadily growing TVL is a good sign that other people have done their homework and feel comfortable parking their capital there.

You can use data aggregator sites like DeFiLlama to track the TVL of almost any protocol out there. When you're looking at TVL, watch for:

- Sustained Growth: A protocol with a long track record of maintaining or growing its TVL is generally more stable.

- Resilience: How did the TVL fare during major market crashes? Protocols that hold onto a good chunk of their value show that their users have real, long-term conviction.

A sudden, steep drop in TVL can signal a loss of confidence, a potential exploit, or just users chasing shinier yields elsewhere. It’s a critical health indicator you should always keep an eye on.

Verify the Source of the Yield

This is the most important question you will ever ask: where does the yield actually come from? If you can't get a simple, clear answer, just walk away. Sustainable yield is always generated by real economic activity.

A legitimate protocol will be transparent about its revenue sources, which are typically borrowing fees, trading fees, or liquidation penalties. An unsustainable one might be paying out yields using its own inflationary token, a model that often collapses under pressure.

When you look at the historical data, stablecoin yields consistently outperform traditional "risk-free" rates. For instance, in December 2023, the DeFi Risk-Free Rate—a benchmark for the safest stablecoin strategies—was 4.30%. At the same time, the rate on short-term government bonds was just 4.02% and trending down.

Use On-Chain Data Tools

Don't just take a project's marketing at face value—verify everything yourself using on-chain data. Tools like Dune Analytics and Nansen let you peer directly at the blockchain and see exactly what's happening inside a protocol. You can build your own dashboards or use pre-made ones to track key metrics like:

- Daily active users

- Borrowing volume versus available supply

- The concentration of token holders (are a few whales in control?)

This gives you a direct, unfiltered window into a protocol's health. Learning to use these tools is a skill that separates the savvy investors from the crowd. If you want to streamline this research, our guide on the best stablecoin aggregators can point you to platforms that help find and compare yields efficiently.

Wrapping Up Your Stablecoin Yield Strategy

So, where do you go from here? Getting into stablecoin yield is a game of balance. The appeal of earning passive income is strong, but it's matched by some very real risks. The secret isn't just hunting down the highest APY you can find; it's about building a smart, sustainable strategy that’s built on solid research and careful risk management.

At this point, you have a solid grasp of how stablecoin yield is made, the different kinds of risks you'll encounter, and how to properly investigate new opportunities. If there's one thing to take away, it's this: safety trumps speed. A portfolio built on hype can evaporate overnight, but one built on knowledge will stand the test of time. This framework should give you the confidence to move from theory to action.

A Final Checklist for Success

Let's pull it all together. Think of these as the golden rules for navigating stablecoin yield opportunities without getting burned.

Start Small. Seriously. Never put in more than you’d be okay with losing, especially when you're testing out a new platform or protocol. Think of it as tuition money—use a small amount to get comfortable with the process firsthand.

Diversify Everything. Don't put all your eggs in one basket. That means not just one protocol, not just one stablecoin, and not just one type of yield strategy. Spreading your funds around protects you if any single part of your plan goes wrong.

Verify, Then Trust. Take every claim with a grain of salt. Do your own homework. Read the security audits, dig into the on-chain data using tools like DeFiLlama, and don't stop until you know exactly how the yield is being generated.

Stay Plugged In. Crypto doesn't sleep. You need to keep up with market news, protocol updates, and any new regulations coming down the pike. A well-informed investor is always one step ahead.

At the end of the day, the goal is to generate consistent returns that make sense for the risk you're taking. Follow these rules, and you'll shift from being someone who just watches from the sidelines to a sharp, active participant in the world of stablecoin yield.

Frequently Asked Questions About Stablecoin Yield

As you get deeper into earning yield on your digital dollars, you'll probably find a few questions keep coming up. I've put this section together to tackle the most common ones head-on, giving you straightforward answers to help you feel more confident.

Think of it as your go-to reference for those practical, "what-if" questions that pop up right when you're about to jump in.

Is Earning Stablecoin Yield Truly Passive?

It's often pitched as "passive income," but a better term is probably semi-passive. While you won't be glued to charts like a day trader, it’s definitely not a "set it and forget it" game. To do this well, you need to stay engaged and do your homework.

Here’s what you should be keeping tabs on:

- Platform Health: Is the protocol’s TVL growing or shrinking? Have there been any recent security updates? What’s the community saying in governance forums?

- Market Conditions: A sudden crypto winter or bull run can dramatically shift borrowing demand, which is what fuels your yield.

- Position Management: You’ll want to check in on your positions every so often to make sure they still fit your goals and risk appetite.

A good rule of thumb is to check on your positions weekly. It's the sweet spot—enough to catch any major changes without getting sucked into obsessively tracking daily APY swings. It lets you enjoy the benefits of yield farming while still being a responsible manager of your own money.

How Is Stablecoin Yield Taxed?

This is a big one, and the honest answer is: it depends entirely on where you live. Tax laws are different everywhere, and they're still catching up to crypto.

That said, in most places (like the United States), the yield you generate from stablecoins is typically viewed as ordinary income. This means you'll pay taxes on it at your regular income tax rate, just like a salary.

Keeping clean records is non-negotiable. You need to log every time you earn yield—the date, the amount, and its value in your local currency when you received it. Because this area is so complex and constantly changing, I can't stress this enough: talk to a tax professional who actually understands digital assets. It will save you a world of headaches later.

What Is the Safest Way for a Beginner to Get Started?

If you're just starting out, your number one goal should be minimizing risk, not chasing the highest APY you can find. The safest way in is to stick with the big, battle-tested players in the space.

Here’s a simple path to get you started on the right foot:

- Choose Established Platforms: Start with DeFi heavyweights like Aave or Compound, or a highly trusted centralized exchange. These guys have been around the block and have survived major market turmoil.

- Stick to Major Stablecoins: Use stablecoins with massive liquidity and solid backing, like USDC or DAI. Leave the new, experimental algorithmic stablecoins for when you have more experience under your belt.

- Start Small: Only deposit an amount you'd be okay with losing. Think of it as tuition money. This lets you learn the entire process—from connecting your wallet to claiming rewards—without putting your real savings on the line.

At Stablecoin Insider, we provide the in-depth analysis and news you need to stay ahead in the world of digital assets. Explore our expert insights and detailed guides to make smarter, more informed decisions. Learn more at https://stablecoininsider.com.

{kind=link}