Table of Contents

Think of stablecoin loans as a way to get cash without having to sell your crypto. It’s a bit like a home equity loan, but for your digital assets. You use your volatile crypto, like Bitcoin or Ethereum, as collateral to borrow stablecoins pegged to a currency like the U.S. dollar.

Unlock Your Crypto's Value Without Selling

Imagine you need cash for a big expense, but all your value is tied up in your house. You wouldn't sell your home to pay for it; you’d probably get a loan against its value. Stablecoin loans work the same way. You "pledge" your crypto to a lending platform and get a loan in a stablecoin like USDC or USDT.

This is a smart way to get your hands on usable cash—what we call liquidity—from your crypto portfolio. Crucially, it doesn't trigger a taxable event the way selling your assets would. You keep ownership of your original crypto, hoping it goes up in value, while getting the funds you need right now for other investments or just to pay the bills.

Why Crypto Lending Is Exploding

It's a powerful idea, and the market for it is growing incredibly fast. The numbers speak for themselves, showing a huge amount of confidence in these financial tools.

In Q3 2025 alone, the market for crypto-collateralized lending shot up by $20.46 billion—a 38.5% jump—hitting a new record of $73.59 billion. This isn't just a niche market anymore; it's a clear sign that investors are getting comfortable putting their digital assets to work.

This growth is happening across two main types of platforms. Decentralized Finance (DeFi) now makes up 55.7% of the lending market, while the more traditional Centralized Finance (CeFi) platforms hold about 33.12%. You can dig into these stats in the latest crypto leverage report from Galaxy.

Of course, none of this would work without the "stable" part of stablecoins. If you're wondering how they hold their value, our guide explains how stablecoins maintain their peg in our detailed guide. Understanding that is key to grasping how these loans actually function.

How Do Stablecoin Loans Actually Work?

To really see why stablecoin loans are so useful, we need to peek under the hood. The whole system is built on a few core ideas that protect lenders while giving borrowers the cash they need. It all starts with one simple but crucial principle.

It All Starts With Over-Collateralization

The backbone of every stablecoin loan is over-collateralization. In plain English, this means you have to put up more crypto than the amount you want to borrow. Think of it like a security deposit for the lender—it guarantees they won't be left empty-handed if the market for your crypto collateral suddenly drops.

For instance, you might lock up $10,000 worth of your Bitcoin (BTC) to borrow $7,000 in USDC. That extra $3,000 acts as a buffer. If the price of your Bitcoin dips, the lender still has a cushion before their funds are at risk.

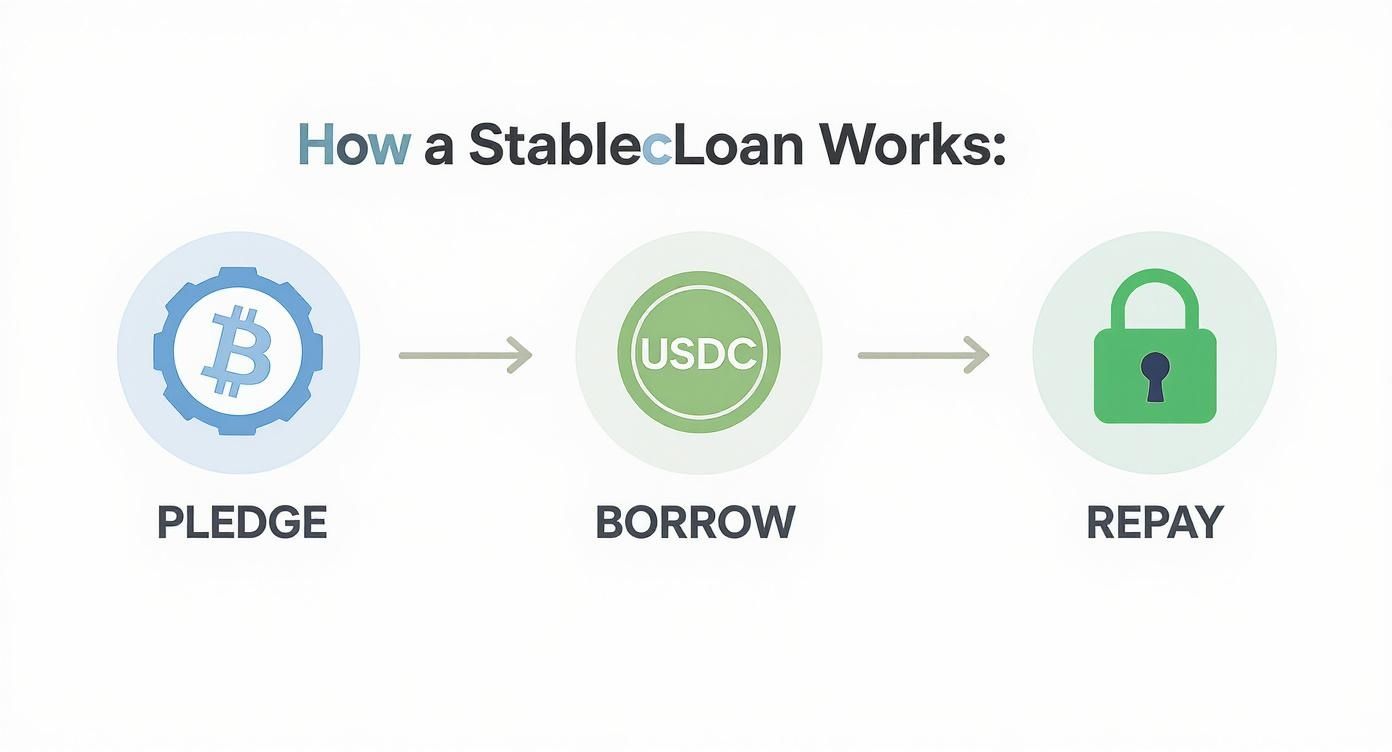

This diagram shows you exactly how the process flows, from locking up your assets to getting them back.

As you can see, you’re pledging a volatile asset to borrow a stable one. Once you repay the loan, your original collateral is unlocked and returned to you.

Before we dive deeper, let's break down the essential terms you'll encounter. This table demystifies the key concepts that make stablecoin loans possible.

Key Concepts in Stablecoin Loans Explained

| Term | Simple Explanation | Why It Matters |

|---|---|---|

| Collateral | The crypto asset (like BTC or ETH) you lock up to secure the loan. | This is the lender's insurance. The quality and amount of your collateral determine how much you can borrow. |

| Loan-to-Value (LTV) | The ratio of your loan amount to your collateral's value, shown as a percentage. | This is the most critical metric for loan health. If it gets too high, you risk losing your collateral. |

| Liquidation | The automatic sale of your collateral by the platform if its value drops too much. | This is the system's safety net to protect lenders. For borrowers, it's a worst-case scenario to be avoided at all costs. |

| Interest Rate | The cost of borrowing, which you pay to the lender over time. | In DeFi, this rate isn't fixed. It changes constantly based on how many people are lending versus borrowing a specific stablecoin. |

Understanding these four pillars is the foundation for safely navigating the world of crypto lending and borrowing.

Loan-to-Value (LTV): The One Number You Must Watch

The relationship between your loan and your collateral is boiled down into one critical metric: the Loan-to-Value (LTV) ratio. This percentage is the single most important health indicator for your loan.

Let's stick with our earlier example:

- You Borrowed: $7,000 USDC

- Your Collateral is Worth: $10,000 in BTC

- The Math: ($7,000 ÷ $10,000) * 100 = 70% LTV

A lower LTV is always safer. It means you have a bigger financial cushion protecting you from market swings. Most platforms set a maximum LTV, usually somewhere between 50% and 75%. The exact limit depends on the collateral you use; blue-chip assets like Bitcoin and Ethereum generally let you borrow more (a higher LTV) than smaller, more volatile altcoins. You can dig deeper into how crypto collateralizes stablecoins in our detailed overview.

What Determines Your Interest Rate?

Forget the fixed rates you see at a traditional bank. In the world of DeFi, interest rates for stablecoin loans are fluid and determined by code based on simple supply and demand in a lending pool.

- When Lots of People Borrow: If there's a rush to borrow USDC but not enough people are supplying it, the interest rate for borrowers shoots up. This encourages more people to deposit their USDC to earn that higher yield.

- When Lots of People Lend: On the flip side, if the pool is swimming in USDC with few borrowers, the interest rate will drop to make borrowing more attractive.

This creates a beautiful, self-regulating system. The rates are always adjusting in real-time to match what the market is doing for that specific stablecoin.

This automatic adjustment mechanism is a fundamental shift from traditional finance. It ensures money is always available at a fair, market-driven price, all powered by transparent and efficient smart contracts.

Liquidation: The System's Safety Valve

So, what happens if the crypto market takes a nosedive and the value of your collateral plummets? This is where the platform's built-in safety nets—liquidation thresholds and margin calls—kick in to protect the lender’s money.

A liquidation threshold is a pre-set LTV percentage where the protocol automatically sells off your collateral to pay back your loan. For example, a platform might set its liquidation threshold at 85%. If a market crash causes your BTC collateral's value to drop, pushing your LTV from a safe 70% all the way up to 85%, a liquidation is triggered.

Before that happens, many platforms (especially centralized ones) will send you a margin call. This is essentially a warning that your loan is in the danger zone, giving you a chance to fix it. To avoid getting liquidated, you have two main options:

- Add More Collateral: Deposit more crypto to bring your LTV back down.

- Repay Part of the Loan: Pay back some of the stablecoins you borrowed, which has the same effect of lowering your LTV.

These aren't just abstract concepts—they are practical rules of the road. Understanding them is absolutely critical for managing your loans and making sure you don't lose your valuable crypto assets.

Choosing Your Platform: DeFi vs. CeFi

When you’re ready to get a stablecoin loan, you’ll quickly hit a fork in the road. One path leads to Centralized Finance (CeFi), and the other to Decentralized Finance (DeFi). Both will get you the loan you need, but how they get you there—and the principles they’re built on—are worlds apart.

Think of CeFi platforms as the crypto equivalent of your online bank. They're run by familiar companies, have real people you can contact for customer support, and generally offer a polished, user-friendly experience.

DeFi, on the other hand, is the open frontier. It’s a financial system built on code, not corporations, running automatically on the blockchain.

The Centralized Finance (CeFi) Approach

CeFi lending platforms are custodial. In plain English, that means you hand over your crypto collateral to the company, trusting them to keep it safe.

To get started, you'll almost always have to complete a Know Your Customer (KYC) process. This is the standard identity verification where you submit personal documents, just like opening a traditional bank account.

- Pros: Usually much easier to use, have dedicated customer support, and sometimes offer insurance on your deposits.

- Cons: You’re not in control of your own crypto (this is known as counterparty risk), and all your activity is linked to your real identity.

For anyone just dipping their toes into crypto lending, the familiar interface and support from CeFi platforms make them a very approachable starting point.

The Decentralized Finance (DeFi) Path

DeFi protocols run on a totally different philosophy: self-sovereignty. Here, there’s no company in the middle. Instead, the entire system is powered by smart contracts—bits of code that automatically execute the terms of a loan on a blockchain like Ethereum.

This makes the whole process transparent and automated. You interact with the protocol directly from your own crypto wallet, which means you never hand over your private keys. No KYC, no asking for permission, and no one who can freeze your funds.

DeFi represents a fundamental shift. Instead of trusting a company, you trust verifiable code. You become your own bank, with all the freedom—and responsibility—that comes with it.

Platforms like Aave pioneered this space, building global, permissionless money markets that are open to anyone. These protocols are the engine behind the explosive growth of stablecoin loans. For a sense of scale, an incredible $51.7 billion in stablecoins were borrowed in August 2025 alone. You can dig into the data behind this growth in Visa's on-chain lending report.

If you want to understand the lender's side, you can learn more about earning stablecoin yield with Aave in our guide which breaks down how these decentralized pools operate.

Making the Right Choice for You

So, which path is right for you? It really boils down to your personal priorities and how comfortable you are with the technology. This table lays out the key trade-offs between the two models.

| Feature | Centralized Finance (CeFi) | Decentralized Finance (DeFi) |

|---|---|---|

| Asset Custody | The platform holds your crypto. | You maintain full control of your keys. |

| Identity Verification | KYC is almost always required. | No personal information is needed. |

| Trust Model | Trust in the company's integrity. | Trust in the security of the smart contract. |

| User Experience | Often simpler and more intuitive. | Can have a steeper learning curve. |

| Key Risk | Counterparty risk (company failure). | Smart contract risk (code exploits). |

Ultimately, CeFi gives you convenience and a human safety net in exchange for custody of your assets. It’s a trade-off many people are happy to make for a smoother experience.

DeFi, however, offers total financial freedom and transparency, but it puts all the responsibility squarely on your shoulders. If a smart contract has a bug or you lose your private keys, there’s no help desk to call. Your choice should match your risk tolerance and technical confidence. As you get more experienced, you might even find yourself using both for different purposes.

Practical Strategies for Using Stablecoin Loans

Knowing how stablecoin loans work is one thing, but actually putting them to use is where the magic happens. Smart investors and everyday crypto holders are using these loans for way more than just cashing out. They're deploying clever strategies to boost returns, manage their portfolios, and even build new income streams.

Let's break down three of the most powerful ways you can put stablecoin loans to work for you.

Amplify Your Portfolio Through Leverage

One of the most popular reasons to take out a stablecoin loan is to get some leverage. Think about it this way: you're holding a good amount of Ethereum (ETH) and you're bullish on its long-term potential. Selling it is the last thing you want to do, but you've spotted another promising crypto asset you want to get in on.

This is the perfect scenario for a stablecoin loan. Instead of selling your ETH, you can use it as collateral to borrow stablecoins like USDC. Then, you simply use that USDC to buy the new asset.

- Your Goal: To get more skin in the game without selling your core assets.

- The Action: You deposit $20,000 worth of ETH into a lending protocol and borrow $10,000 in USDC. You immediately use that USDC to buy another token.

- The Outcome: You still own your original $20,000 in ETH, but now you also hold $10,000 in the new token. If both of them go up, your gains are magnified.

Of course, leverage is a double-edged sword. While it can amplify your wins, it also magnifies your losses. If the market takes a dive, your risk of liquidation goes up.

Access Real-World Liquidity Without the Tax Headache

Beyond the crypto markets, stablecoin loans are an incredibly practical way to get cash for real-world expenses—without triggering a tax event. In most places, selling your crypto for a profit is a taxable event. Borrowing against it? Not so much.

This makes stablecoin loans a fantastic tool for funding big life purchases.

A stablecoin loan acts as a bridge between your digital assets and your real-world financial needs. It unlocks the value of your crypto holdings, making them liquid and usable for things like a down payment on a house, funding a business, or covering unexpected medical bills.

Say you need $50,000 for a home renovation. You could lock up $100,000 of your Bitcoin as collateral and borrow the stablecoins you need. You get the cash, you sidestep a potentially hefty tax bill, and you get to keep your Bitcoin, which could continue to appreciate. It's a powerful way to make your crypto portfolio work for you here in the physical world.

This screenshot from Aave shows a typical DeFi lending dashboard. It’s clean, transparent, and shows you exactly what you can supply and borrow, along with the live interest rates for each.

You can see right away how market-driven these platforms are, with rates that adjust in real-time based on supply and demand.

Generate Passive Income with Yield Farming

If you're up for a more advanced strategy, stablecoin loans are the key that unlocks yield farming. At its core, yield farming is all about borrowing stablecoins at a low interest rate on one platform and lending them out for a higher rate on another. That difference, or "spread," is your profit.

Here’s a simple look at how it works:

- Borrow Low: You find a lending protocol where you can borrow stablecoins for a 3% annual interest rate.

- Lend High: You take those borrowed stablecoins over to a different platform or liquidity pool that's paying out a 6% APY to lenders.

- Earn the Spread: You pocket the 3% difference as pure profit. It’s a passive income stream generated entirely with borrowed capital.

This strategy can get pretty complex, often involving several platforms and constant monitoring to chase the best yields. We've put together a full guide on how to farm stablecoin incentives if you want to dive deeper. Just remember, while it can be very profitable, yield farming has its own set of risks, like smart contract bugs or interest rates shifting and wiping out your profit margin.

Navigating the Risks and Regulatory Landscape

Stablecoin loans offer some incredible flexibility, but let's be clear: they aren't a free lunch. Like any financial instrument, they come with their own set of challenges. Understanding these risks—from buggy code to wild market swings—is the absolute key to borrowing and lending safely.

The specific risks you'll encounter usually hinge on whether you're using a DeFi or CeFi platform. Each path has its own distinct set of potential traps you need to watch out for.

Key Risks in DeFi and CeFi

When you dive into DeFi, your number one boogeyman is smart contract risk. The whole system is automated by code, and if that code has a flaw, hackers can swoop in and drain the protocol. The best platforms go through intense security audits, but you have to remember that no code is ever 100% perfect.

Then there's liquidation risk, which we touched on before. If your collateral's value suddenly nosedives, the protocol will automatically sell off your assets to cover the loan, often at a terrible price. This isn't a bug; it's a core feature of DeFi lending, which is why you have to keep a close eye on your loan’s health.

On the CeFi side of the fence, the big one is counterparty risk. When you hand your crypto over to a centralized company, you're placing your trust in them to be good stewards of your funds. If they go bankrupt, mismanage the money, or get hacked, your assets could vanish. You're swapping code risk for human and corporate risk.

Understanding this trade-off is fundamental. With DeFi, you trust the code's integrity. With CeFi, you trust the company's integrity. Both require a degree of faith, but in very different things.

The Evolving Regulatory Environment

Regulators are officially off the sidelines and are now actively shaping the rules of the game for stablecoins and crypto lending. This growing oversight is a bit of a double-edged sword. It can add new layers of complexity, but it also brings a much-needed dose of legitimacy and safety to the market.

Governments are finally starting to lay down clear rules, which is a great sign of the industry's growing maturity. In fact, 2025 has been a big year for this, with the US passing the GENIUS Act to bring more transparency and oversight to stablecoins. That, combined with new rules in Hong Kong and the EU's MiCA framework, is making stablecoins a much more solid bet in major financial hubs. These trends show stablecoins are solidifying their role in both the crypto ecosystem and broader financial infrastructure, as you can explore in this 2025 crypto adoption report.

At the end of the day, these rules are meant to protect consumers and keep the financial system stable. As the policies get clearer, expect more defined guidelines on everything from how assets are held to what needs to be reported. For a closer look at how U.S. agencies are tackling this, you might find our deep dive on FDIC stablecoin regulations useful. This march toward sensible regulation is helping build a safer playground for everyone involved.

Best Practices for Safe Crypto Borrowing

Jumping into stablecoin loans can unlock some seriously powerful financial moves, but you need a solid game plan to do it safely. Whether you're borrowing to free up cash or lending to earn some yield, discipline is the name of the game. A few core habits can be the difference between a winning strategy and a very expensive lesson.

For borrowers, your number one job is keeping your loan healthy to stay clear of liquidation. Think of your Loan-to-Value (LTV) ratio as a live number, not a "set it and forget it" metric. It needs your attention, especially when the market gets choppy.

Smart Habits for Borrowers

Your main objective is to maintain a comfortable distance from the platform's liquidation point. The first rule? Fight the urge to max out your loan. Creating that safety buffer from day one is the single most important step you can take.

Here are a few practical ways to keep your loan in the safe zone:

- Maintain a Healthy Collateral Buffer: Never borrow right up to the limit. If a platform lets you borrow up to an 80% LTV, it's smarter to aim for 50% or even lower. This gives your collateral plenty of breathing room to handle market dips without triggering a margin call.

- Set Up LTV Alerts: Most platforms and some third-party tools let you set up alerts. Configure them to ping you if your LTV starts to climb into a warning zone, say 65%. This gives you a heads-up to add more collateral or pay down the loan before things get critical.

- Keep Repayment Funds Ready: Always have some stablecoins or other easily accessible funds on hand. If the market turns south, you can de-risk your position in minutes instead of scrambling to sell other assets under pressure.

Just as it's common sense to understand the importance of regularly reviewing your loans in traditional finance, the fast-paced world of crypto makes it essential to constantly keep an eye on your borrowing terms.

Key Practices for Lenders

If you're on the other side of the table, supplying liquidity to a lending pool, your focus shifts from LTV to the quality of the protocol itself. Your success hinges on the security of the platforms you use and the type of collateral they allow.

As a lender, you're not just earning interest—you're underwriting risk. Your best protection is solid research. Your returns are only as safe as the platform's code and the assets that back the loans.

Follow this checklist to minimize your risk when lending:

- Thoroughly Research Protocols: Dig into the platform’s security audits, its history, and whether it has an insurance fund. A clean track record without major hacks is a huge green flag.

- Assess Collateral Quality: Stick to platforms that prioritize high-quality, liquid assets like Bitcoin and Ethereum as collateral. Protocols that accept a wide range of less-established altcoins can bring a lot more risk to the entire lending pool.

- Diversify Across Platforms: Don't put all your eggs in one basket. Spreading your capital across two or three well-vetted platforms protects you if one of them suffers a catastrophic smart contract bug or exploit.

Got Questions? We've Got Answers

Even after getting the hang of how stablecoin loans work, you probably have a few practical questions kicking around. Let's tackle the most common ones head-on to clear up any lingering confusion.

How Much Do I Need to Borrow?

This really depends on where you go. In the world of decentralized finance (DeFi), you'll find that most protocols have no official minimum borrowing amount. You could, in theory, borrow just a few bucks, but the network fees (gas fees) would probably make it a bad deal.

Centralized finance (CeFi) platforms, on the other hand, usually play by different rules. They often set minimums, which could be as low as $50 or as high as $1,000 or more. The best advice? Always check the fine print on a platform before you commit your collateral.

Do I Have to Pay Taxes on the Loan?

Here’s one of the biggest draws of a crypto loan: in most places, like the United States, simply borrowing against your assets is not a taxable event. Think about it—you’re not selling your crypto and locking in a gain. You're just accessing its value.

But a word of caution: tax laws are notoriously tricky and always evolving. It’s a smart move to chat with a tax professional who actually gets the crypto space. They can give you advice that fits your specific financial picture.

The Bottom Line: A stablecoin loan lets you tap into the value of your crypto without having to sell and trigger a potential tax bill. It’s a key strategy for savvy investors looking to manage their portfolio without giving up their position.

How Fast Can I Get the Money?

This is where DeFi really shines. The speed is a game-changer.

- DeFi Platforms: We're talking almost instant. As soon as your collateral is locked in the smart contract, you can borrow. The stablecoins usually hit your wallet in a matter of minutes, depending on how busy the blockchain is.

- CeFi Platforms: It’s still quick, but there can be a few extra steps. You might have to go through an identity check (KYC), and from there, loan approval can take anywhere from a few minutes to a couple of hours.

Can I Pay the Loan Back Whenever I Want?

Absolutely. Flexibility is a core feature here. Whether you're on a DeFi protocol or a CeFi platform, you can almost always pay back your loan early—in part or in full—without getting hit with the prepayment penalties you often see in traditional banking.

The moment you clear the principal and any interest you owe, your collateral is unlocked and ready for you to withdraw. This lets you react to market shifts and manage your debt on your own terms.

At Stablecoin Insider, we provide the essential insights you need to stay ahead in the world of digital assets. For expert analysis and the latest news on stablecoins and decentralized finance, visit us at https://stablecoininsider.com.

{kind=link}