Table of Contents

Earning a high APY on stablecoins really just means putting them to work. You're not securing a network like you would with other cryptos; instead, you’re using decentralized (DeFi) or centralized (CeFi) platforms to lend them out, add them to trading pools, or get a bit more complex with yield farming.

While everyone calls it "staking," it's more accurate to think of it as a collection of yield-generating activities.

Decoding High-Yield Stablecoin Strategies

When you see a tempting APY advertised for stablecoins, what's happening behind the scenes is you're acting like a small-scale lender in the crypto economy. The term "staking" has become a casual shorthand for just about any activity where you lock up crypto to earn a return.

For stablecoins, this almost always boils down to one of three things:

Lending: This is the most straightforward method. You deposit your stablecoins into a lending protocol like Aave. From there, borrowers can take out loans against their own crypto collateral, and the interest they pay gets passed back to you as yield. Simple.

Providing Liquidity: Here, you deposit your stablecoins into a liquidity pool on a decentralized exchange (DEX), such as Curve. These pools are what allow traders to swap between different assets smoothly. In return for providing the funds that make these trades possible, you earn a cut of the trading fees.

Yield Farming: This is the more advanced play. It often involves chaining strategies together. For instance, you might lend your stablecoins, get a "receipt" token in return, and then use that receipt token on another platform to earn even more rewards. It's all about moving your capital around to squeeze out the maximum possible return.

So, Where Does the Yield Actually Come From?

A high APY isn't just free money—it’s generated by real economic activity. The yield you pocket comes directly from market demand. Lenders earn from people who need cash for trading or leverage, while liquidity providers get paid by traders who need deep, liquid markets to make their moves.

The single most important question you should ask is: "Who is paying for this yield?" If the answer seems to be "new investors" or it's just funded by printing more of a platform's native token, that's a massive red flag. Real, sustainable yield comes from borrowing demand and trading fees.

This is precisely why stablecoins like Tether (USDT) and USD Coin (USDC) are at the heart of this entire ecosystem. Their massive liquidity and established trust make them the go-to assets. It's no surprise that USDT is one of the most popular staked stablecoins out there.

To put it in perspective, the combined trading volume for USDT and USDC hit a staggering $23 trillion in 2024. That colossal volume is what fuels the engine for these yield platforms.

Here’s a quick rundown of how these common strategies stack up against each other.

Common Stablecoin Yield Strategies

| Strategy | Typical APY Range | Risk Level | Complexity |

|---|---|---|---|

| Lending | 3% - 10% | Low | Low |

| Liquidity Providing | 5% - 20% | Medium | Medium |

| Yield Farming | 15% - 50%+ | High | High |

As you can see, higher potential rewards almost always come with more complexity and, crucially, more risk. Starting with simple lending is a great way to get your feet wet.

The Role of Major Stablecoins

Think of USDT and USDC as the digital U.S. dollars of the crypto market. They are the backbone for countless trading pairs and the most accepted form of collateral for loans. This creates a constant, powerful demand from users who need them for:

- Arbitrage: Making quick profits from small price differences between exchanges.

- Leveraged Trading: Borrowing stablecoins to amplify their trading power.

- Market Making: Supplying liquidity to exchanges to keep trading smooth.

To really get a handle on the nuances and avoid the pitfalls, it pays to do your homework. Learning how to conduct a thorough literature review can be a huge help in separating the solid opportunities from the risky ones.

Ultimately, it's the stability and widespread adoption of these top-tier stablecoins that make generating a reliable return possible in the first place. And while these are the mainstays, new types of assets are always on the horizon. You can learn more about what’s next for yield-bearing stablecoins in 2026 in our detailed guide.

Choosing Your Arena: CeFi vs. DeFi Platforms

Alright, your first big decision is where you’ll actually put your stablecoins to work. This choice boils down to two worlds: Centralized Finance (CeFi) and Decentralized Finance (DeFi).

Think of this as choosing between a traditional bank and a fully automated, user-owned financial system. One isn't inherently better than the other; they just serve different needs and comfort levels with risk. Your decision here will define everything from your user experience and security responsibilities to the potential returns you can expect.

The CeFi Experience: Simple, Familiar, and Custodial

If you're just getting started, CeFi is likely the most comfortable on-ramp. These platforms are run by established companies—think big crypto exchanges or lending services—and their apps feel a lot like your online banking portal. You sign up, verify your identity, deposit your stablecoins, and the platform handles the rest.

They take custody of your assets and put them to work, sharing a slice of the profits with you. The trade-off for this simplicity is counterparty risk. You're trusting a company to keep your funds safe and to stay in business. While many are reputable, we’ve all seen headlines about platform failures. Because of their overhead and more cautious approach, yields are generally more modest, often in the 2% to 6% APY range for top stablecoins.

My Take: CeFi is perfect for a "set-it-and-forget-it" strategy. It's a great starting point if you value ease of use and are comfortable letting a trusted third party manage your assets.

For instance, a major exchange might have an "Earn" feature where you deposit USDC and start collecting interest within minutes. It’s a fantastic way to test the waters. For a look at how larger players approach this, check out our guide on earning stablecoin yield with Coinbase Prime.

The DeFi Frontier: Higher Yields and Total Control

DeFi is where things get really interesting, and it’s typically where you’ll find the highest APY. These platforms are just open-source code running on a blockchain. Protocols like Aave or Curve let you interact directly with smart contracts from your own crypto wallet.

You hold the keys, you control the funds. This is the heart of the "not your keys, not your crypto" ethos. Because DeFi cuts out the corporate middleman, the protocols are more efficient and can pass those savings on as higher returns. It's not uncommon to see yields ranging from 3% to 10% or even more when market demand is high.

The catch? You’re the captain of your own ship. This means you’re responsible for your own security—safeguarding your wallet’s seed phrase is paramount. You also need a basic grasp of how to use a wallet, sign transactions, and pay for network "gas" fees.

The main danger here is smart contract risk. A bug or an exploit in a protocol's code could put your funds at risk. That's why I can't stress this enough: stick to battle-tested protocols that have undergone multiple security audits.

Your Platform Due Diligence Checklist

Whether you go with CeFi or DeFi, your homework process should be rigorous. Before you even think about connecting your wallet or depositing funds, run through this checklist.

- Security Audits: Has the platform been audited? By who? Look for reports from top-tier security firms like Trail of Bits or OpenZeppelin. For any DeFi protocol, this is an absolute must.

- Total Value Locked (TVL): TVL is the total amount of money users have deposited. A high TVL is a strong signal of trust and liquidity. It means lots of other people have kicked the tires and feel comfortable deploying their capital there.

- Team and Reputation: Who is behind the project? A transparent, experienced team with a solid track record is a huge plus. Be very wary of anonymous teams or platforms with a shady past.

A fantastic tool for this research is DeFiLlama. It gives you a bird's-eye view of the entire DeFi ecosystem, letting you sort protocols by TVL and see who the established leaders are. Protocols with billions in TVL like Lido and Aave have proven their resilience over time, making them a much safer bet than some new, unaudited project promising astronomical returns. Use this data—it’s your best defense.

High-Yield Strategies for Every Risk Level

Alright, let's get into the practical side of things. Earning a solid APY on your stablecoins isn't a one-size-fits-all deal. The best strategy for you has everything to do with your comfort level with risk and tech.

The goal is to match the method to your mindset. Are you looking for something simple you can set and forget? Or are you willing to get your hands dirty with more complex protocols to chase those higher returns?

We can break down the options into three main categories, each with its own balance of risk, reward, and required effort.

Low-Risk Simple Yields

If you're just starting out or your number one priority is protecting your capital, this is the place to be. These strategies are the bread and butter of stablecoin yield, usually found on big, well-established platforms in both CeFi and DeFi.

Think of this as the crypto-native version of a high-yield savings account. You deposit your stablecoins, and the platform handles the rest.

- Simple Lending on DeFi Protocols: This is a classic. Platforms like Aave are cornerstones of DeFi. You supply your USDC or DAI to their lending markets, and you start earning a variable interest rate from people who borrow it. It's all on-chain, you keep custody of your keys, and the whole system is secured by borrowers having to over-collateralize their loans.

- Staking on Centralized Exchanges: Major exchanges make this incredibly easy with their "Earn" or "Savings" products. You just find the right wallet on their platform, move your stablecoins in, and you're good to go. The trade-off is that you're giving up custody of your assets, but for many, the sheer simplicity is worth it.

With these methods, you're typically looking at a modest but reliable APY, often somewhere between 3% and 10%. The real win here is the simplicity and the peace of mind that comes from using battle-tested platforms managing billions of dollars.

Intermediate Strategies for Higher Returns

Once you've got the basics down, you can start exploring ways to capture more attractive yields. This usually means moving from simply lending your assets to providing liquidity, which makes you a more active participant in the DeFi ecosystem.

You're no longer just earning interest; you're helping facilitate trades and getting a cut of the fees.

A perfect example is becoming a liquidity provider (LP) for a stablecoin pair like USDC/DAI on a decentralized exchange such as Curve Finance. You deposit both stablecoins into a liquidity pool, and in return, you earn a percentage of the trading fees every time a user swaps between them. The LP tokens you receive can often be staked elsewhere for even more rewards.

This is a step up because you're introduced to new concepts like impermanent loss (though it's very low with stablecoin-to-stablecoin pairs). It also requires you to check in on your position and rewards. The reward for this extra effort? A potentially higher APY, often in the 8% to 15% neighborhood.

Advanced High-APY Tactics

Welcome to the deep end of the pool. This is where you can find some truly eye-popping APYs, but it comes with a matching level of risk. These advanced strategies are for experienced users who have a firm grasp of DeFi mechanics and are comfortable with the real possibility of losing money.

Leveraged yield farming is the most common path here. It's a high-risk, high-reward game that works something like this:

- First, you deposit your stablecoins into a lending protocol as collateral.

- Next, you borrow another asset against that collateral.

- Then, you use those borrowed funds to farm yield somewhere else, essentially "leveraging" your starting capital to earn more.

You can even repeat this loop to amplify your returns, but it also amplifies your risk. While a simple USDC liquidity pool might get you around 10% APY, more aggressive strategies using recursive borrowing and staking can push yields on USDT and USDC past 30% APY.

The big danger here is liquidation. If the value of your collateral dips below a certain point, the protocol will automatically sell it off to repay your loan, and you can lose a significant chunk of your funds. This means you have to constantly monitor your loan-to-value (LTV) ratio.

For anyone serious about mastering these advanced techniques, our deep dive into stablecoin yield strategies for 2025 is a must-read. It’s not for the faint of heart, but this is where the highest returns in stablecoin farming are hiding.

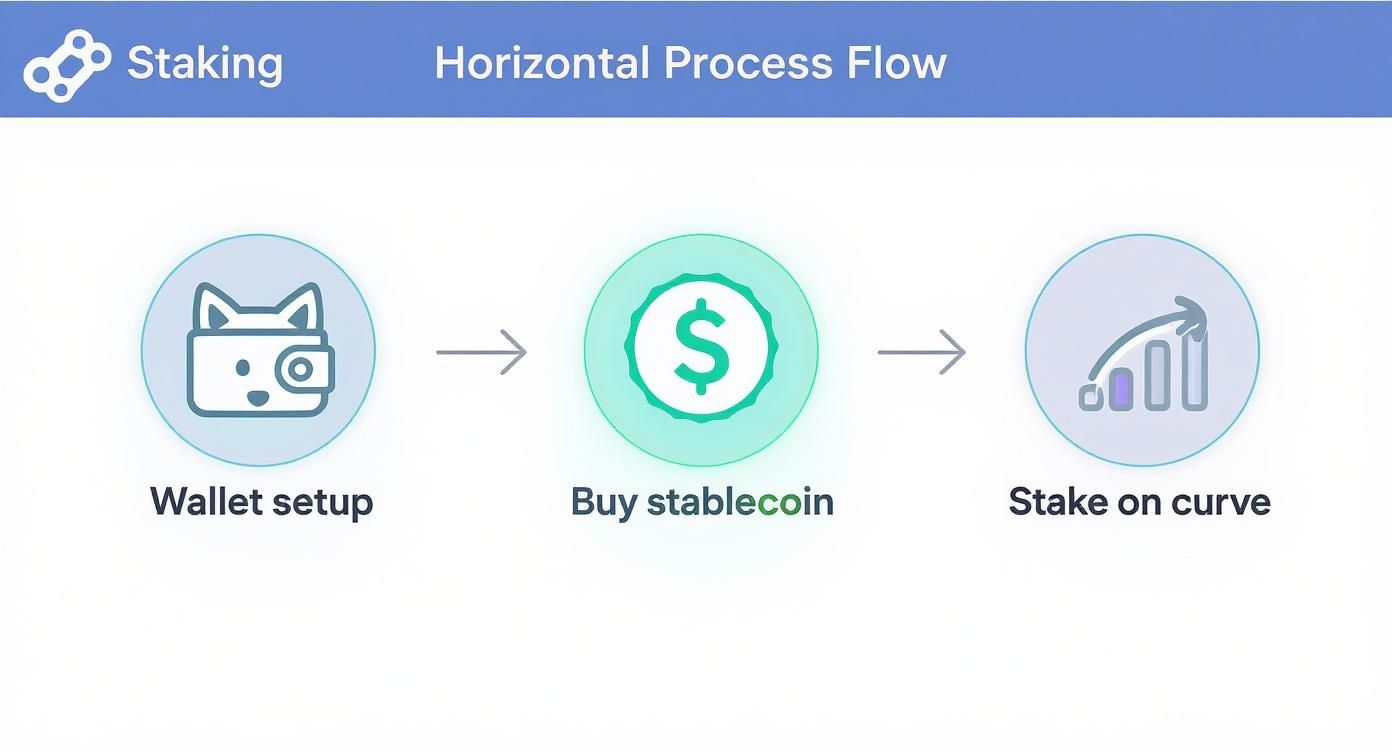

Your First DeFi Staking Walkthrough

Theory is great, but there's no substitute for getting your hands dirty. So, let’s walk through a real-world example of putting your stablecoins to work for a high APY on a decentralized finance (DeFi) protocol. We'll use Curve Finance for this example—it’s a true cornerstone of DeFi, famous for its hyper-efficient stablecoin swaps.

At first glance, the process might seem a bit intimidating, but it really just boils down to a few key moves. We'll go from setting up your wallet to acquiring the right coins and finally putting them into a yield-generating position on the platform.

Getting Your DeFi Toolkit Ready

Before you can even think about interacting with a DeFi protocol, you need a self-custody wallet. This is non-negotiable. It’s a type of wallet where you control the private keys, which means you have full control over your money. MetaMask is by far the most popular choice, and it conveniently works as a simple browser extension.

First things first: set it up and treat your secret recovery phrase like the keys to a vault. Write it down, store it somewhere safe and offline—never, ever save it on your computer or in the cloud. If you lose that phrase, your crypto is gone for good. There’s no customer support to call.

With your wallet up and running, you'll need two assets inside it:

- Stablecoins: You can buy stablecoins like USDC or DAI on a major centralized exchange (like Coinbase or Kraken) and then withdraw them directly to your new MetaMask wallet address.

- The Network's Native Token: Every single transaction on a blockchain costs a "gas" fee, which is paid in that network's native token. If you're on Ethereum, you need ETH. On Polygon, you need MATIC. Always keep a little bit of this native token on hand to pay for transactions. Without it, your funds are stuck.

Bridging to the Right Network

A classic rookie mistake is having your assets on the wrong blockchain. DeFi isn't just one big network; it’s a collection of them—Ethereum, Arbitrum, Polygon, and many others. The notoriously high gas fees on Ethereum often make Layer 2 networks like Arbitrum a much smarter and cheaper place to earn yield.

So, what if your stablecoins are on Ethereum but the high-yield Curve pool you want is on Arbitrum? You'll need to use a bridge. A bridge is just a tool that lets you move assets from one blockchain to another. It's the crypto equivalent of wiring money between two different international banking systems. Mastering this is crucial for chasing the best yields.

Pro Tip: I can't stress this enough: always triple-check that you are on the official website for any protocol you use. Scammers are experts at creating pixel-perfect fake sites designed to drain your wallet the second you connect. Bookmark trusted sites like Curve.fi and only use your bookmarks.

Depositing and Staking on Curve

Okay, your wallet is funded and you're on the right network. Time for the fun part. The process really has two main parts: you deposit your stablecoins into a liquidity pool, and then you stake the "receipt token" you get back.

Here’s how it typically plays out on a platform like Curve:

- Connect Your Wallet: Head over to the Curve Finance site and hit the "Connect Wallet" button. MetaMask will pop up asking for your permission. Go ahead and approve it.

- Find a Pool: Look for a stablecoin pool that matches what you're holding. The famous "3pool" (DAI, USDC, USDT) is a popular starting point. This is where you'll often find solid APYs.

- Deposit Your Stablecoins: Punch in the amount you want to deposit. The first time you do this for a specific token, the protocol will ask you to "approve" it—this is a one-time transaction giving Curve permission to interact with your stablecoins. After that's done, you'll submit the final deposit transaction.

- Receive LP Tokens: Once the transaction confirms on the blockchain, you won't see USDC or DAI in your wallet anymore. In their place, you'll find new tokens called Liquidity Provider (LP) tokens. These represent your slice of the pool.

- Stake Your LP Tokens: This is the final step that actually turns on the yield. Find the "Gauge" for your pool and "stake" your LP tokens. This is what makes you eligible to earn a cut of the trading fees plus any bonus token rewards the protocol is offering.

While this walkthrough focused on Curve, the core concepts—approve, deposit, stake LP token—are pretty universal across the DeFi world. For another popular take on earning yield, our guide on how to earn stablecoin yield with Aave breaks down a slightly different but equally powerful lending protocol. Once you get this workflow down, you've unlocked the ability to tap into countless stablecoin strategies.

Managing the Risks of Stablecoin Staking

Chasing high APY on stablecoins is a great strategy, but let's be real: yield and risk go hand-in-hand. Understanding what can go wrong isn't about scaring you off—it's about making you smart enough to build a strategy that won't get wiped out during a market downturn.

It's easy to get tunnel vision when you see double-digit returns, but ignoring the very real threats in both CeFi and DeFi is how a promising investment turns into a painful lesson. Let's break down the main risks you need to watch out for.

The infographic below shows a typical DeFi staking workflow. It looks simple on the surface, but each step has its own hidden dangers.

From setting up your wallet to staking on a protocol like Curve, the user actions are straightforward. The real challenge is managing the underlying risks, from keeping your wallet secure to trusting the protocol's code.

Smart Contract and Technical Risk

In DeFi, you’re not trusting a bank; you're trusting code. Smart contract risk is the ever-present danger that a bug, vulnerability, or clever exploit in a protocol's code allows a hacker to drain its funds. It doesn't matter how popular a platform is—if the code is weak, your money is at risk.

This is why security audits are an absolute must. Before you even think about depositing, you need to verify that the protocol has been audited by several reputable security firms. Even then, an audit isn't a get-out-of-jail-free card. It's a risk-reduction tool, not a guarantee.

A clean audit reduces the probability of an exploit, but it never eliminates it. Think of it like a home inspection: it spots most existing problems but can’t predict a pipe bursting a year from now. This is exactly why savvy DeFi users never go all-in on one protocol; they diversify across multiple, well-audited platforms.

De-Pegging and Reserve Risk

The whole point of a stablecoin is that it holds its 1:1 peg to an asset like the US dollar. De-pegging risk is the nightmare scenario where the stablecoin breaks that peg and plummets in value. This can be triggered by a crisis of confidence, shady reserve management, or just a full-blown market panic.

We’ve seen this movie before. A "stable" coin suddenly trades at $0.80 on the dollar. That 10% APY you were earning doesn't mean much when your principal loses 20% of its value overnight.

Here’s how to protect yourself:

- Don't Monogamble: Never go all-in on a single stablecoin. Spread your capital across a mix of proven leaders like USDC, USDT, and DAI.

- Follow the Money: Reputable issuers publish regular reserve reports and attestations. Actually read them. Make sure they’re backed by high-quality, liquid assets and not just wishful thinking.

Counterparty and Regulatory Risk

When you use a centralized (CeFi) platform, you're introducing counterparty risk. This is the risk that the company you gave your money to goes bankrupt, gets hacked, or gets a letter from a regulator that forces them to freeze withdrawals. In DeFi, you hold your own keys. In CeFi, you’re just another name on a list of creditors if things go south.

Regulatory risk is the other big elephant in the room. Governments are still trying to figure out how to handle crypto, and a sudden rule change can instantly impact the platforms you use or even the stablecoins themselves. Staying on top of the shifting legal landscape is part of the game. Moving assets between blockchains also has unique dangers, which you can learn more about by reviewing our guide on stablecoin bridging risks and user experience.

Lately, protocols like Falcon Finance have been gaining traction, offering a solid 8% APY on their USDf stablecoin, generated through arbitrage. With $1.5 billion in TVL, it certainly has the market's attention. Just remember, these yields come from complex strategies, and their plan to integrate Real World Assets will bring a whole new set of risks to manage.

Questions That Come Up All the Time

When you're getting started with stablecoin yield farming, a few questions always pop up. It's totally normal. Getting straight answers to these is the best way to build a strategy you're comfortable with. Let's dig into the big ones.

What’s a Realistic APY for Stablecoin Staking?

This is the million-dollar question, isn't it? The honest answer is that your APY is always tied directly to the risk you're taking. If a platform is promising a ridiculously high number that seems too good to be true, your first thought should be to question where that yield is actually coming from.

I like to think of returns in a few different buckets:

- The Foundation (4-10% APY): This is your bread and butter. We're talking about lending on massive, time-tested DeFi protocols like Aave or using the simple "Earn" programs on major, reputable centralized exchanges. The yields aren't flashy, but they're driven by real, verifiable demand from borrowers.

- The Next Level (10-20% APY): Here you’re wading into deeper waters, often by providing liquidity for stablecoin-to-stablecoin pools on a platform like Curve. You’re taking on a bit more complexity and a touch more risk (like tiny bits of impermanent loss), but in return, you're earning trading fees and sometimes extra token rewards.

- The High-Wire Act (25%+ APY): Anything in this territory is almost always an advanced, high-risk play. This could mean leveraged yield farming or staking on newer, less-proven protocols. The potential returns are huge, but so is the risk of getting liquidated or falling victim to a smart contract bug.

A key takeaway: Sustainable yield comes from real economic activity—people paying to borrow or paying to trade. If a high APY is just funded by a platform printing its own inflationary token, it's a house of cards waiting to fall.

How Does the IRS Handle Stablecoin Staking Rewards?

First off, I'm not a tax advisor, and you absolutely need to consult a professional who understands crypto. Tax laws are incredibly complex and different everywhere. That said, I can give you a general idea of how it's often handled in the U.S. to get you started.

Generally, the rewards you earn from staking are viewed as ordinary income. This means you owe income tax on the dollar value of the rewards at the moment you claim them. If you earn 10 USDC, that's $10 of income you need to report.

The story doesn't end there. Later, when you go to sell or trade those rewards, you're looking at capital gains tax. The profit or loss is calculated based on the difference between the token's value when you received it and its value when you sold it. The only way to manage this correctly is to keep obsessive, detailed records of every single transaction.

Can You Actually Lose Money Staking Stablecoins?

Yes. One hundred percent, yes. Let's be crystal clear: the word "stable" only refers to the coin's price target, not the safety of your investment strategy. The risks are very real, and you can lose some or even all of your money.

Here are the main culprits to watch out for:

- Smart Contract Hacks: A clever hacker finds a loophole in a DeFi protocol's code and drains the liquidity pools—taking your funds with them.

- De-Peg Events: A crisis of confidence, a flaw in the mechanism, or poor reserve management causes a stablecoin to permanently break its $1 peg. Your holdings are now worth significantly less.

- Platform Risk: A centralized platform you're using goes bankrupt (we've all seen the headlines) or gets shut down by regulators, freezing your assets indefinitely.

There's no magic bullet, but your best defense is diversification. Spreading your capital across different, well-audited protocols and a few different stablecoins is the smartest way to manage these risks.

Ready to dive deeper and stay ahead of the curve? At Stablecoin Insider, we provide expert analysis and up-to-the-minute news on everything from DeFi yields to regulatory shifts. Explore our insights today at https://stablecoininsider.com.

{kind=link}