Table of Contents

A new report from Dune Analytics, commissioned by Visa, makes the case that non-USD stablecoins have crossed a meaningful threshold.

The numbers are hard to dismiss: $10 billion in monthly transfer volume, 1.2 million unique holders, and transfer velocity growing 16x since January 2023, all for a category that most institutions still treat as experimental.

The data suggests the window for treating local currency stablecoins as a niche phenomenon is closing.

Key Takeaways

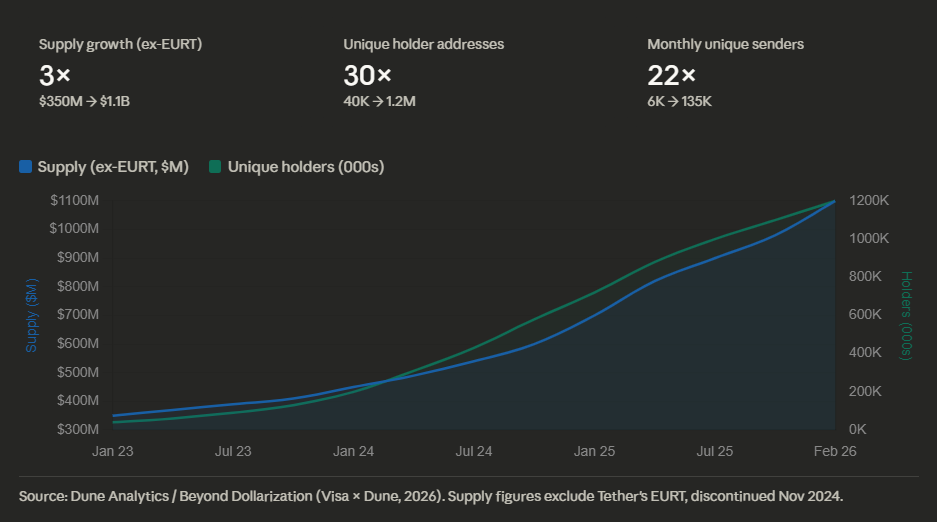

- Local currency stablecoin supply grew 3x (ex-EURT) from January 2023 to February 2026, while unique holders expanded 30x, distribution is outpacing issuance

- Transfer volume hit $10B monthly in February 2026, up from $600M in January 2023, a 16x increase that far outpaces supply growth, signaling genuine operational use

- Euro stablecoins now represent 80% of the $1.2B tracked market cap, with EURC alone processing $10–$20B in monthly transfer volume

- Regulatory frameworks: MiCA, Singapore's MAS SCS, Brazil's 2026 Central Bank resolutions, Japan's Payment Services Act amendments, are the clearest predictor of sustained adoption

- Weekend volume slowdowns in non-EURC stablecoins point to business payments, payroll cycles, and treasury settlement as the dominant use cases

1. The Market Has Quietly Tripled

Local currency stablecoins are no longer a rounding error. The aggregate picture from Dune's onchain data shows a market that has compounded steadily even after absorbing a structural shock, Tether's EURT was discontinued in late 2024 following MiCA compliance requirements, wiping roughly $350M in supply overnight.

- Adjusting for EURT's exit, total non-USD stablecoin supply grew from ~$350M in January 2023 to ~$1.1B by February 2026, a 3x expansion, outpacing the 2.3x growth of USD-denominated stablecoins over the same period

- Unique holder addresses grew from roughly 40,000 to over 1.2 million, a 30x increase that indicates adoption is broadening across user types, not concentrating in large institutional wallets

- Monthly unique senders expanded from ~6,000 to ~135,000, a 22x increase that points toward repeat, operational usage rather than speculative accumulation

The SI read: Supply growth is interesting; velocity growth is what matters. When transfer volume grows 16x while supply grows 3x, you're looking at assets being used as money, turned over repeatedly in settlement flows, not sitting in cold storage. That's a qualitatively different market than it was two years ago.

2. Payments Dominate, But the Mix Tells the Real Story

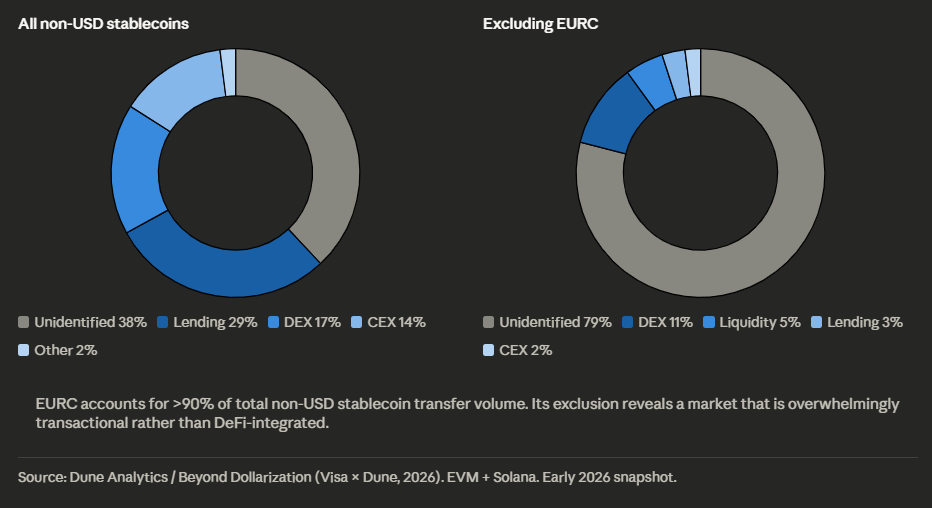

The report's most analytically useful insight is what happens when you strip EURC out of the aggregate data.

EURC alone accounts for more than 90% of total transfer volume across all tracked non-USD stablecoins, and it behaves differently from the rest of the market, with deep DeFi integration across Aave, Morpho, and major DEXs.

Remove it, and the picture that emerges is almost entirely payments-driven.

- Ex-EURC, approximately 79% of transfer volume falls into unidentified transfers, peer-to-peer, payment processor flows, and treasury settlement consistent with B2B and payroll activity

- DEX activity drops to ~11% and lending to ~3% ex-EURC, confirming that DeFi depth in non-USD stablecoins is largely a EURC-specific story at this stage

- Non-EURC stablecoins show consistent weekend volume declines, a pattern that does not appear in crypto-native assets, but is characteristic of business payment and treasury settlement cycles

The SI read: For banks and payment companies evaluating local currency stablecoins, the practical implication is straightforward, outside of the euro, these assets are functioning primarily as settlement rails, not yield instruments.

That's actually a cleaner integration story: the compliance model, the use case, and the liquidity profile all point toward operational treasury and cross-border B2B payments.

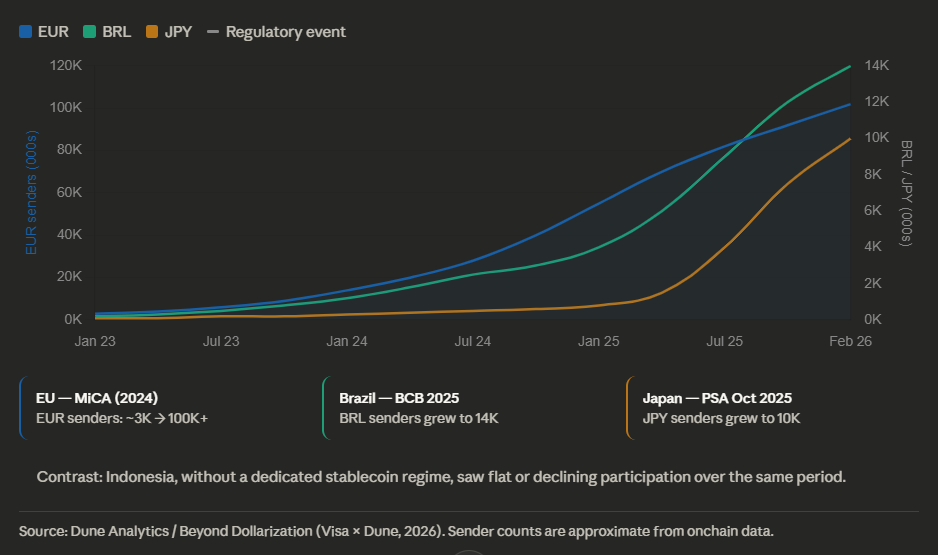

3. Regulatory Clarity Is the Single Biggest Adoption Driver

The report identifies a consistent pattern across jurisdictions: where dedicated regulatory frameworks exist, adoption accelerates. Where they don't, markets stall.

This isn't coincidental, it reflects how institutional participants actually make decisions about integrating new settlement assets.

- Euro stablecoins saw a sharp acceleration following MiCA's implementation in 2024, with unique senders expanding from ~3,000 to over 100,000 and user share rising from 42% to over 78% of all non-USD stablecoin activity

- Brazil's BRL stablecoin monthly senders grew to 14,000 following 2025 Central Bank resolutions and PIX integration; Japan's JPY stablecoins reached 10,000 monthly senders after Payment Services Act amendments enabled regulated yen issuance via JPYC

- Indonesia, which lacks a dedicated stablecoin issuer regime, saw flat or declining participation over the same period, a direct contrast to regulated markets

The SI read: The MiCA effect should be studied closely by every institution evaluating which currency corridors to prioritize. Regulatory clarity does two things simultaneously: it gives banks and fintechs the legal certainty needed to build products, and it gives issuers the framework to structure reserves in ways that satisfy institutional treasury standards.

Markets without that clarity will continue to lag regardless of macro demand.

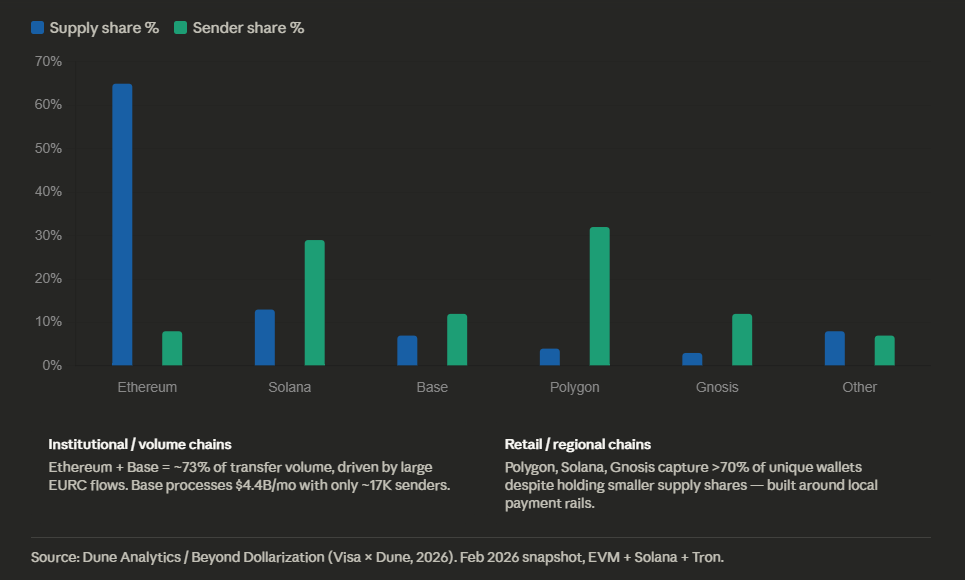

4. Chain Distribution Reflects Regional Strategy, Not Global Scale

Unlike USD stablecoins, which optimize for global liquidity depth, local currency stablecoins are being deployed with a regional specialization logic, choosing chains that allow tight integration with domestic payment infrastructure.

- Ethereum leads in supply (~65%), but Gnosis, Celo, and Polygon collectively account for over 70% of unique wallets, networks selected for their integration with local wallets, card programs, and national payment rails

- Base processes $4.4B in monthly volume with only ~17,000 senders, driven almost entirely by large institutional EURC flows; Polygon and Solana lead in unique sender counts (~45,000 and ~39,000 respectively), reflecting retail and SMB payment activity

- Gnosis Chain's integration of BRLA with PIX via Gnosis Pay, launched in Brazil in mid-2025, exemplifies the model: a vertically integrated fiat-to-stablecoin stack built around a domestic instant payment system

The SI read: The chain selection decision for local currency stablecoins is fundamentally a payment infrastructure decision, not a DeFi liquidity decision.

Institutions building in this space should evaluate chains based on their domestic fintech ecosystem integrations, existing PIX/FPS/PayNow-adjacent partnerships, and card settlement capabilities, not purely on TVL or transaction throughput metrics.

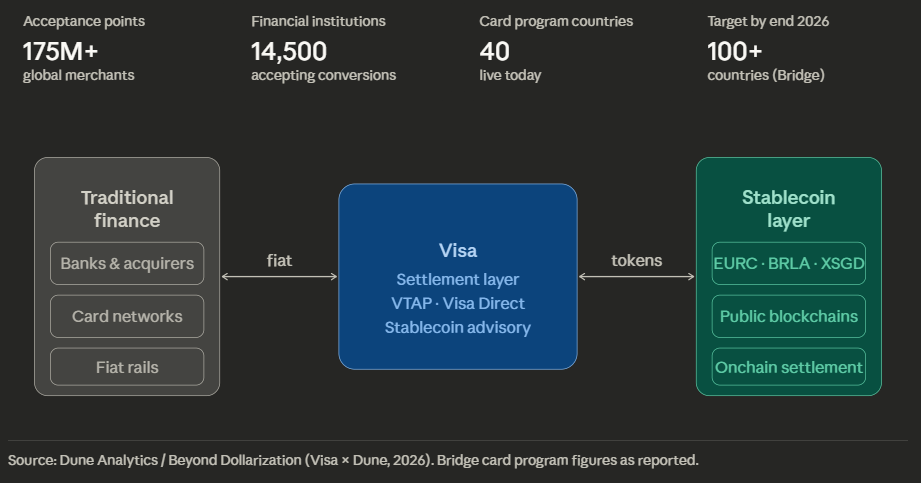

5. Visa's Infrastructure Play Sets the Template

The report's Visa case study deserves more attention than it typically receives in coverage of this space. Visa's role is not as a stablecoin issuer, it's as the bridge layer that makes local currency stablecoins institutionally accessible without requiring banks and acquirers to rebuild their compliance and acceptance infrastructure from scratch.

- Through Visa Direct, selected partners can execute cross-border payouts using EURC and other stablecoins, with automatic conversion to local fiat where required, supporting payroll, marketplace disbursements, and remittance flows

- Visa's Tokenized Asset Platform (VTAP) allows banks and fintechs to mint and manage their own fiat-backed stablecoins, including non-USD denominations, a direct path for regional banks to issue regulated local currency stablecoins under existing Visa compliance frameworks

- Stablecoin-linked card programs, including Bridge's Visa partnership now live in 18 countries and targeting 100+ by end of 2026, allow end users to spend stablecoins at any of 175+ million Visa acceptance points while merchants settle in local fiat

The SI read: The Visa model is significant because it resolves the core adoption problem for regulated institutions: how do you integrate stablecoin settlement without disrupting merchant acceptance, AML/KYC workflows, or existing treasury operations?

The answer, increasingly, is that you don't need to, you layer stablecoin settlement underneath existing infrastructure.

That's not a crypto-native story. It's a payments infrastructure story, and it's the one most likely to drive institutional volume at scale.

Bottom Line

The Dune/Visa report frames local currency stablecoins as the next wave of a payments landscape moving beyond dollarization.

The data supports that framing, but with an important caveat: this is not a uniform global phenomenon. It's a jurisdiction-by-jurisdiction story, driven by regulatory maturity, domestic payment rail integration, and the willingness of established networks like Visa to build the institutional bridges.

Banks and fintechs that move early in regulated corridors, the EU, Brazil, Singapore, and Japan, are positioning themselves at the infrastructure layer of a multi-currency digital payments stack that is, by all available evidence, already being built.

Related Reports

- The Institutional Gap in Stablecoins: B2B Payments vs End User Volume

- Here's The Best Blockchains for Each Stablecoin Use Case in 2026

Partner/Advertise with Stablecoin Insider

Fill out this form to partner and advertise on the only publication, dedicated entirely to the Stablecoin ecosystem.

See you next week,

- The Stablecoin Insider team

{kind=link}