Table of Contents

After years of USDT dominance, Circle’s USDC has taken the lead in meaningful on-chain activity.

This marks the first time since 2019 that USDC has surpassed Tether’s USDT in adjusted transaction volume.

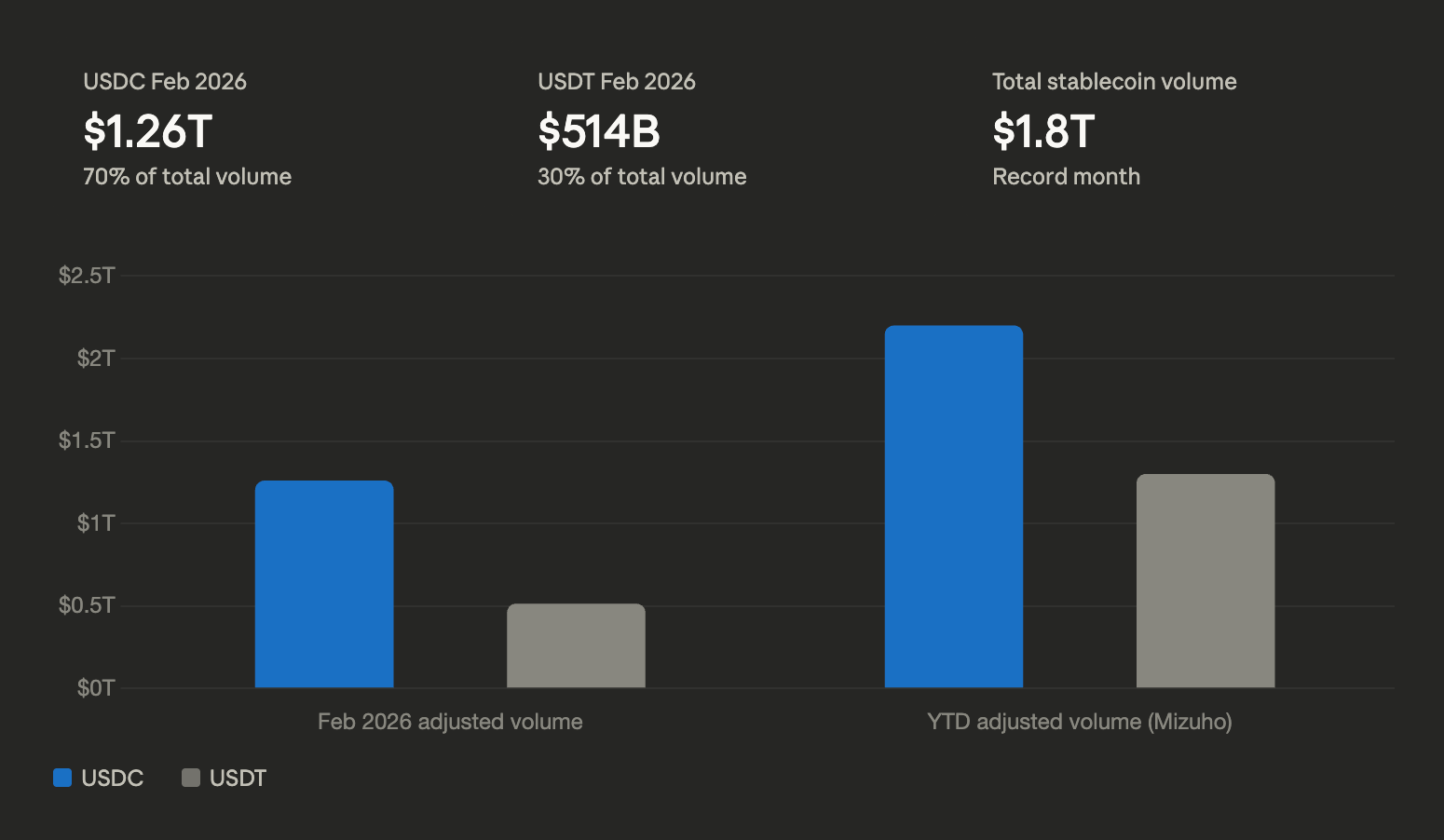

Blockchain analytics firm Allium reported a record $1.8 trillion in total stablecoin transfer volume for February 2026. USDC accounted for $1.26 trillion (about 70%) while USDT handled just $514 billion.

The shift was confirmed on March 13 by Mizuho Securities: year-to-date adjusted volume reached USDC $2.2 trillion versus USDT $1.3 trillion, giving USDC a 64% share of combined adjusted flows.

→ Keep in mind that adjusted volume removes wash trading and internal cycling to reflect genuine economic use in payments, settlements, DeFi, and institutional transfers.

Here are the five key reasons behind USDC’s decisive momentum:

1. Post-GENIUS Act Regulatory Clarity and Institutional Preference

On February 25, 2026, the Office of the Comptroller of the Currency (OCC) issued its long-awaited Notice of Proposed Rulemaking, detailing licensing, capital standards, redemption rules, and oversight for banks and qualified issuers. Comments close May 1.

This clarity has accelerated adoption by corporations, fintechs, and institutions that prioritize auditability and regulatory alignment.

USDC’s transparent monthly attestations and full reserve reporting give it a measurable compliance premium, making it the preferred rail for treasury management, B2B settlements, and enterprise workflows.

USDT retains strength in retail and offshore venues but faces headwinds among regulated entities.

2. Explosive Growth in Real-World Use Cases and Payments Velocity

USDC is winning where money actually moves the economy. Corporate and fintech players are replacing slow, expensive bank wires with near-instant, low-cost USDC settlements.

February’s record transfers highlight higher velocity: despite trailing in total supply, USDC processes significantly more genuine economic activity across payments, cross-border remittances, payroll, real estate, and tokenized asset transfers.

Data shows stablecoin B2B and payment volumes surging dramatically, with USDC capturing the majority of adjusted flows in sectors demanding clean liquidity. On high-performance networks like Solana and Ethereum Layer-2s, USDC’s speed and cost advantages amplify this edge.

In contrast, a large portion of USDT activity remains tied to retail trading, derivatives, and internal cycling.

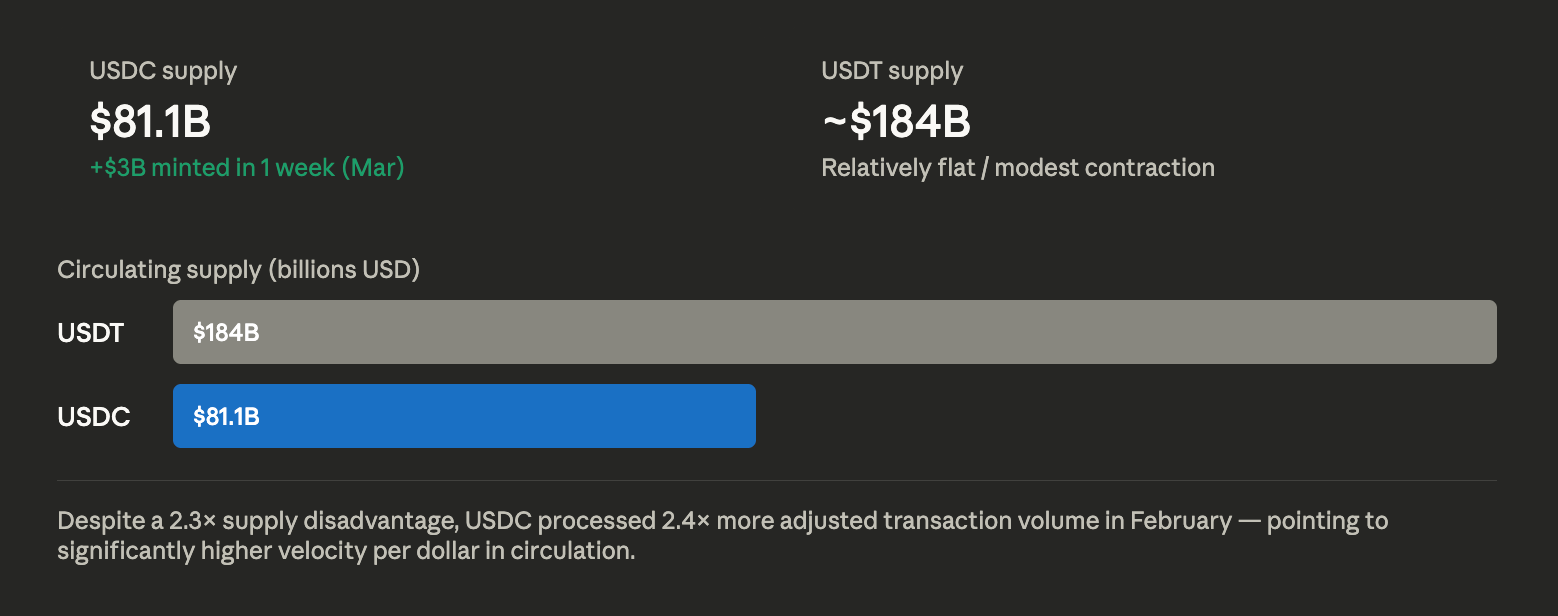

3. Strong Supply Growth and Fresh Minting Momentum

USDC supply has accelerated sharply, reaching a new peak near $81.1 billion.

Over $3 billion was minted in the first week of March alone, with large issuances on Solana and other chains.

This reflects sustained institutional demand and capital inflows into compliant rails. USDT supply, by comparison, has remained relatively flat or seen modest contraction at ~$184 billion, underscoring diverging trajectories driven by use-case preferences.

4. Enterprise and Fintech Partnerships Favoring Transparency

Major players including Visa, Stripe, PayPal (via PYUSD expansion), BlackRock, and others have deepened integrations with USDC for settlements and treasury operations.

Circle’s focus on regulated partnerships and global payment rails has translated into higher real turnover.

Mizuho analysts explicitly cited this institutional shift when raising Circle’s (CRCL) price target to $120 from $100, calling USDC volume leadership a “key fundamental driver.”

5. Perception and Compliance Edge in a Bifurcating Market

Both issuers support blacklisting for sanctions compliance, but USDC benefits from more frequent, detailed public reporting and a perception of tighter alignment with U.S. standards.

The GENIUS Act’s emphasis on federal oversight and attestations is widening this gap, rewarding the issuer seen as lower-risk for regulated counterparties.

USDT continues to dominate global retail liquidity and emerging-market remittances, but the “adjusted” metric highlights where institutional and economic activity is concentrating.

What’s Expected Next: The 2026 Outlook for USDC vs USDT

The rivalry is entering a new phase defined by velocity, legitimacy, and regulatory alignment rather than raw supply alone.

USDC’s Path:

Analysts expect the volume lead to hold or widen in coming quarters if institutional adoption and payments growth continue.

Sustained minting, deeper enterprise integrations, and full GENIUS Act implementation (final rules anticipated later in 2026) could push USDC toward greater parity in overall market share.

Watch for further supply gains and expanded use in RWAs, tokenized Treasuries, and cross-border corporate flows. A multi-chain strategy (Ethereum, Solana, and beyond) will likely amplify velocity.

Tether’s Response:

The January 27, 2026 launch of USAT (USA₮) represents Tether’s direct counterpunch.

Positioned for U.S. institutions and regulated flows, USAT starts small but carries Tether’s vast global network and liquidity advantages. Early listings on major exchanges signal scaling ambitions.

Tether’s strategy appears bifurcated: legacy USDT for retail, emerging markets, and high-liquidity trading; USAT for compliant U.S. and institutional use. Success will depend on how quickly USAT captures share from USDC in regulated corridors.

Broader Market Dynamics:

The stablecoin sector could test $350–400 billion by year-end if inflows persist. Expect continued divergence with USDC leading in adjusted/real-economic volume and institutional rails, USDT maintaining supply and retail dominance.

A potential equilibrium may emerge, with multiple compliant issuers coexisting. Regulatory milestones (OCC final rules, parallel regimes in Europe via MiCA, and Asia) will shape competitive intensity.

Key Risks and Variables:

Faster-than-expected USAT adoption, shifts in reserve requirements, macroeconomic factors affecting Treasury demand, or changes in enforcement could alter trajectories. Geopolitical tensions may further boost stablecoins as a USD proxy.

The data confirms a structural shift is underway. Institutions are voting with real flows.

The dollar’s digital future is being decided in trillions of on-chain dollars and 2026 will reveal whether USDC’s momentum becomes lasting dominance or sparks a new era of intense, regulated competition.

Related Reports

- Would Anyone Miss Banking Rails?: New Report from Finery Markets & Stablecoin Insider

- 2025 Stablecoin Year-End Report (Insights, Data, and Adoption Trends)

Partner/Advertise with Stablecoin Insider

Fill out this form to partner and advertise on the only publication, dedicated entirely to the Stablecoin ecosystem.

See you next week,

- The Stablecoin Insider team

{kind=link}